So I wanted to get this quick piece out after the events at Jackson Hole over the weekend, where Jerome Powell gave a speech on Friday, following by the other G7 central bankers over the weekend.

Summary of Jackson Hole – No Fed Pivot… Yet

I’ve been talking about how market expectations of a “Fed Pivot”, and rate cuts in early 2023, are too early.

The Fed Pivot will come, but not as soon as the market is pricing in.

Jackson Hole seems to have confirmed that view for now.

Jerome Powell, as well as the other G7 Central Bankers came out to deliver very hawkish speeches on the importance of combating inflation, even as the expense of economic growth.

The full speech from Jerome Powell is here, and it’s a very short and readable one, well worth the read if you have some time.

Some snippets from Jerome Powell’s speech (emphasis mine):

The Federal Open Market Committee’s (FOMC) overarching focus right now is to bring inflation back down to our 2 percent goal. Price stability is the responsibility of the Federal Reserve and serves as the bedrock of our economy. Without price stability, the economy does not work for anyone. In particular, without price stability, we will not achieve a sustained period of strong labor market conditions that benefit all. The burdens of high inflation fall heaviest on those who are least able to bear them.

Restoring price stability will take some time and requires using our tools forcefully to bring demand and supply into better balance. Reducing inflation is likely to require a sustained period of below-trend growth. Moreover, there will very likely be some softening of labor market conditions. While higher interest rates, slower growth, and softer labor market conditions will bring down inflation, they will also bring some pain to households and businesses. These are the unfortunate costs of reducing inflation. But a failure to restore price stability would mean far greater pain.

We are moving our policy stance purposefully to a level that will be sufficiently restrictive to return inflation to 2 percent. At our most recent meeting in July, the FOMC raised the target range for the federal funds rate to 2.25 to 2.5 percent, which is in the Summary of Economic Projection’s (SEP) range of estimates of where the federal funds rate is projected to settle in the longer run. In current circumstances, with inflation running far above 2 percent and the labor market extremely tight, estimates of longer-run neutral are not a place to stop or pause.

Powell then goes on to quote the legacies of Paul Volcker, Alan Greenspan, and Ben Bernanke in the quest against inflation.

The message here is clear.

One does not go from talking tough about inflation and quoting Paul Volcker, to cutting interest rates to zero and resuming QE in 6 months – barring a huge financial collapse.

To do so would risk hurting the Fed’s credibility with market participants.

The short term path, for now, lies with higher interest rates, for longer.

Market Reaction

The market reaction can be split into 2.

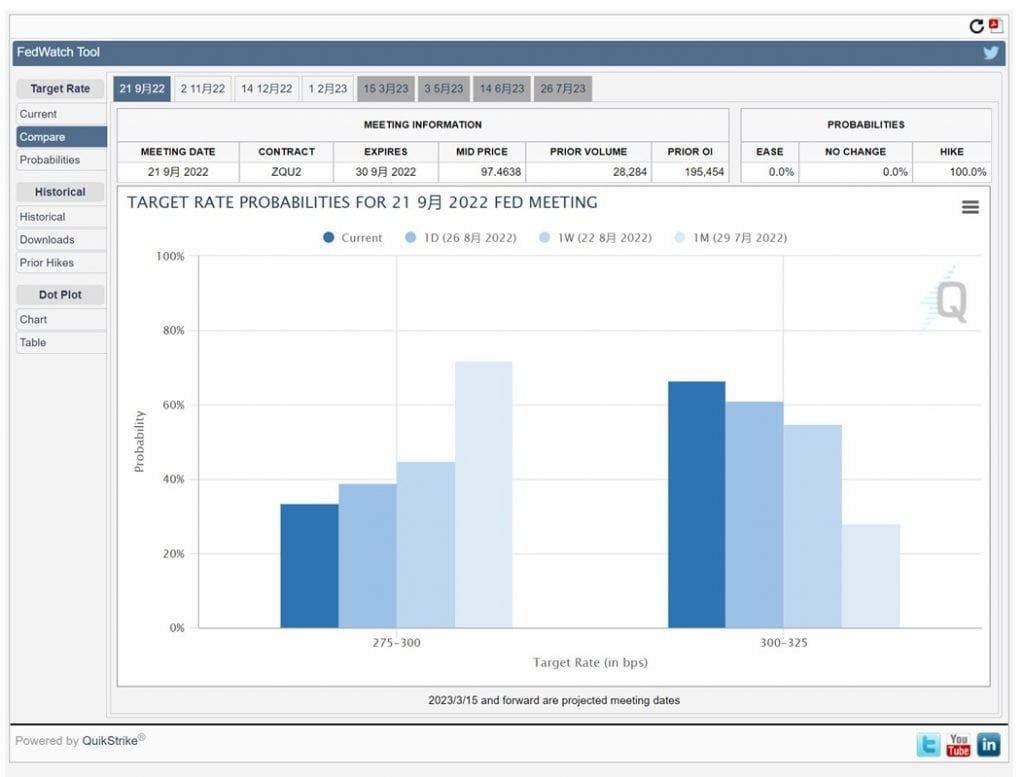

Short term wise, the market has increased the probability of a 0.75% rate hike in September (to >60%).

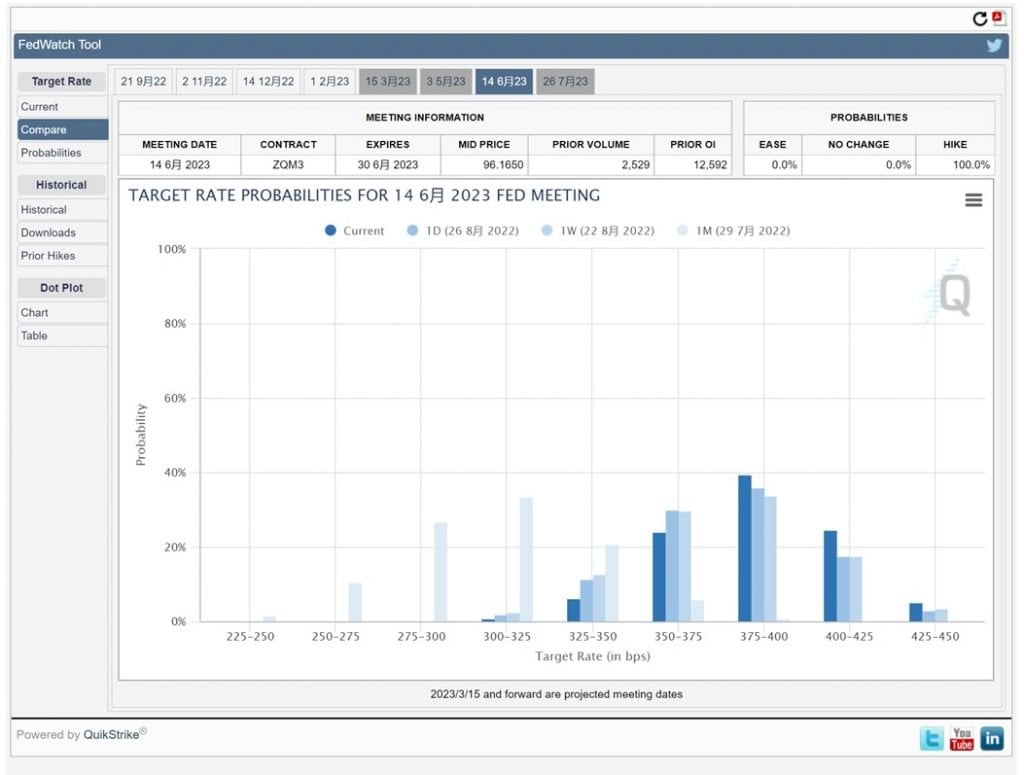

And it has increased the probability of higher interest rates in June 2023.

I don’t necessarily agree with the first view on September rate hike probabilities.

I think the Feds have made it clear they are going to be data dependant, so September is probably a 50-50 between a 0.5% and 0.75% hike for me.

But look into 2023, and I do agree interest rates are going to stay elevated for a while.

Like I’ve been hammering on and on in previous articles: higher interest rates, for longer.

But… Feds will eventually turn dovish

That said, it is easy to listen to Powell’s speech and believe that the Federal Reserve will do whatever it takes to crush inflation, even at the cost of the US economy.

I don’t believe that for one second.

As shared in previous articles, I think the underlying causes of inflation are structural.

Which means that trying to solve inflation by raising interest rates, is just a short-term solution.

They address the symptoms, but they don’t cure the underlying disease.

Once the short term financial tightness goes away, inflation may come back.

When will things start to break?

The way the global economy is set up these days, everything has become hyper financialised.

Think about what a period of interest rates at 3.75% will do to the global economy.

It will play out broadly like this:

- Phase 1 – Financial Assets that are most sensitive to interest rates get their multiples revised down (this has happened)

- Phase 2 – Economy starts to slow, and the slower growth is reflected in corporate earnings (this is in the process of playing out)

- Phase 3 – Companies run into refinancing difficulties, as they cannot roll over their loans at the higher rates (this will happen)

- Phase 4 – Financial market contagion starts to spread, and financial assets sell off together, as correlation goes to one (this may happen)

If things get really bad, and we go into a Phase 4 market meltdown, something similar to 2008 or March 2020, are the Feds going to sit by and watch as everything burns?

I don’t believe that.

I think when the metaphorical s*** hits the fan, the Feds will be forced to cut interest rates and/or resume QE, or governments will unleash fiscal stimulus.

Sparking a massive rally in financial assets, and resuming the path of this inflationary decade.

When will that happen?

The million dollar question is how to time this.

You want to be careful shorting Phase 2 / 3, because there will be vicious bear market rallies on the way down, like we saw the past 2 months.

The market will also probably bottom before the Feds actually pivot, as insiders start to buy, and the market starts to sniff out hints of a Fed pivot.

As shared in previous articles, I’m probably still going to watch for the point where it becomes obvious that the Feds will pivot, before I buy in size.

I know that by doing this I won’t be buying the bottom, but frankly that’s fine by me.

By maintaining elevated cash positions since early this year, I’ve already sat out a fair bit of the market decline, so I don’t need to take on a lot of risk to make it back.

I can still wait until it is clear a Fed pivot has happened, then buy at that point, and ride the subsequent bull market up.

If the Feds are to be believed, we’re going to be looking at a 3.5% – 3.75% yield on short term cash by end of the year / early next year.

That’s just crazy to me.

Blue chip REITs like Ascendas REIT are trading at a low 5% yield. All that additional risk of being in leveraged real estate, just for a meagre 1.5% spread against the risk free?

I’m just going to sit with a big chunk of cash and get that 3.5% risk free yield, until we get a market sell-off, or the Feds turn dovish.

Possible exception for commodities

The only exception here is commodities.

Because of how inflation may be structural, I think commodities have room to go up a lot more this decade.

I just have no clue where commodities are headed in the short term (6 to 12 months).

Maybe they have a vicious sell-off as we head into a recession, maybe they just go higher everyday due to demand/supply mismatch.

I have a fairly sizeable position in oil that I accumulated in 2020, and I’m still holding that for now.

If we do get another commodities sell-off (there was one in June), I would probably use the opportunity to add.

As always – love to hear what you think!