So the allotment results for the July 2022 Singapore Savings Bonds are out.

And I mean… we all knew that these Singapore Savings Bonds would be hot.

But wow… they are sizzling hot indeed… only S$9,000 allocation per person!

Singapore Savings Bonds Allotment – Only $9,000 per person!

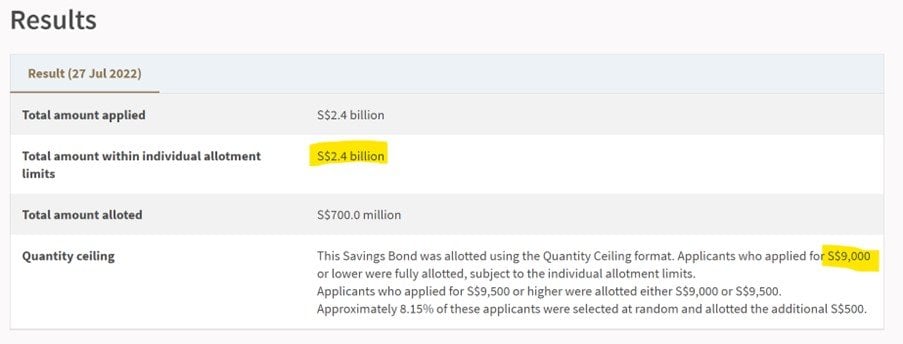

Out of an issue size of $700 million, applications were received for $2.4 billion, which is almost 3.4 times subscribed.

And the amount that each person gets?

A whopping S$9,000.

If you’re really lucky you get $9,500, but only 8.15% of applicants had this privilege.

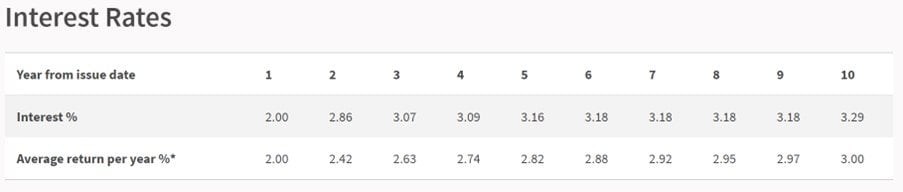

For the record, this was the interest for the July Singapore Savings Bonds.

2.0% for the first year, stepping up to 3.29% for the 10th year, and an average of 3% per year over 10 years.

What about the August Singapore Savings Bonds?

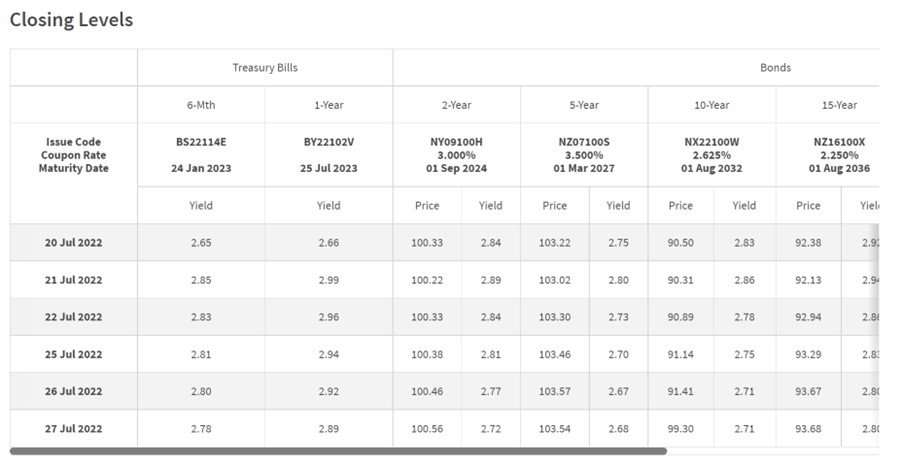

Out of curiosity, I decided to check out the latest SGS yields to see what the August Singapore Savings Bonds would look like.

The short end of the curve has moved up significantly since, and the long end of the curve has come down.

Or more specifically, the 1 year SGS now yields 2.89%, and the 10 year SGS yields 2.71%.

This is an inverted yield curve, but of course the Singapore Savings Bonds cannot have a short end interest that is higher than the long end – it will be artificially smoothed out.

But FH… what does this mean for the next month’s Singapore Savings Bonds?

In plain English – this means that the 1 year interest rate for the August Savings Bonds will be higher than the July ones.

You’re probably looking at about 2.4-2.5%.

While the average interest rate over 10 years will come down, probably about 2.7-2.8%.

Ie. Short term interest rates go up, long term interest rates go down.

Will August Singapore Savings Bonds be even more attractive?

It really depends the kind of time frame you’re looking at.

Those who plan to hold long term will prefer the July SSBs, those who only plan to hold short term will prefer the August SSBs.

For me though – I don’t plan on holding these SSBs for long, probably 1 – 2 years tops.

So I actually prefer a higher short term interest rate.

But frankly given how hot the Singapore Savings Bonds are, your limitation here probably isn’t interest rates anymore.

It’s going to be getting a meaningful allotment.

So I wouldnt be in a rush to redeem my older SSBs.

At this rate, it’s going to take almost 2 years to hit my full allotment of $200,000!

As always, love to hear what you think!

Refinancing tool

With rapidly rising interest rates – it might pay off to look into refinancing if your loan is coming due.

I know a lot of you have been writing in for my views on fixed vs floating loans, and I plan to write a full article for this.

But in this market – I think you’re pretty much forced into taking floating. The banks themselves know interest rates are going up quick, so the fixed rate loans are priced in such a way that they aren’t sufficiently attractive (in my view).

In the meantime, there’s a fantastic tool by Property Guru.

Do give it a try if you’re close to refinancing.

It’s completely free – you just input your mortgage details, and the tool lets you know whether you’ll save money by refinancing.

If the answer is yes, they’ll give you recommendations on what loan to take.

If the answer is no, you can set up a reminder for the tool to remind you when its time to refinance.

I set up the reminders for my own properties just this week and it’s pretty neat.

Do give it a try here.

Should be August and September SSB instead.

Oh yes you are right – thanks for the heads up! Appreciated.

Hi FH,

Do you know how to buy and sell Singapore Government T-bills outside of Auctions? Are they liquid enough to be bought and sold readily outside of auctions?

Thanks!

Hi CMC, yes I wrote an article on this for patrons, will see if I can release it on the public site.

Short answer is that no, T-Bills are not liquid, and you should not count on being able to exit before maturity. If you buy, you should buy with the view of holding them to maturity.