In the spirit of full disclosure, please note that I hold an existing stake in Keppel KBS US REIT. As background, when the unit price crashed to the 0.56 range in December 2018, I thought that the market was massively mispricing this REIT so I loaded up on this counter. Unfortunately I only managed to get around to writing this article today and the unit price has appreciated by more than 12% since, so huge apologies for the delay (I do share all my favourite stock picks on the FH Stock Watch, and Keppel KBS US REIT was included in mid Dec – it’s just 5 bucks a month and you get to support the site ?). Anyway, even at its current price I still think this REIT is a steal, so I do hope the following analysis will be useful for all readers.

Do note that I’ve conducted this analysis in line with the Financial Horse Framework to Analyse REITs.

Basics: Keppel KBS US REIT

From the Keppel KBS US REIT website:

Keppel-KBS US REIT is a distinctive office REIT with properties located in key growth markets of the United States (US). The REIT’s investment strategy is to principally invest in a diversified portfolio of income-producing commercial and real estate assets in key growth markets of the US to provide sustainable distributions and strong total returns for Unitholders.

Or in other words, they’re a Singapore listed REIT that holds US offices.

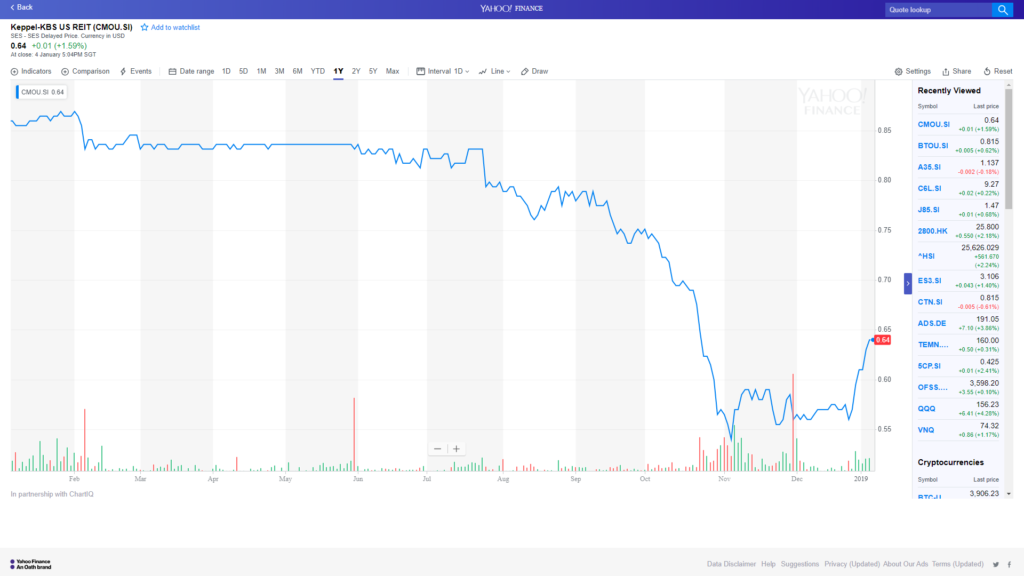

The really interesting stuff about this REIT, is the 1 year chart, as set out below. There’s a bit of background required here. Back in September 2018, Keppel KBS US REIT announced that they were going to purchase a new property in US (Westpark), and that this was going to be funded via a mix of debt and equity. Everything was still okay then, and investors barely flinched. In October 2018, Keppel KBS US REIT then announced that there would be a a huge rights issue (295 new units for every 1000 existing units held), and the price of the new units would be issued at US$0.50, a massive 30% discount to the existing unit price of US$0.715.

That was when all hell broke loose. Not only was the REIT doing a big capital call barely 1 year after IPO, it was also pricing at a massive discount to prevailing market price. That promptly resulted in the collapse of the unit price to the 0.50s range in the chart below, where it languished for the rest of the year. Of course, the fact that US equity markets were melting down in December didn’t really do them any favours too. It was such a huge collapse in unit price that I penned an article advising readers on whether to take up the rights issue, and you can check it out here.

Sponsor

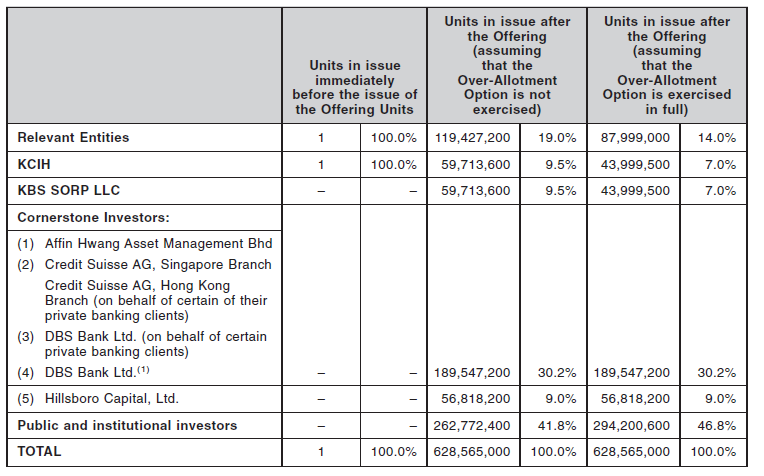

The 2 sponsors of Keppel KBS US REIT are technically, (1) Keppel and (2) KBS. Unfortunately, due to tax reasons, no one unitholder can hold more than 9.8% of this REIT, otherwise the REIT loses its tax transparency status (it’s a requirement under the US tax code). This is why both “sponsors” only hold about 7.0% of the Keppel KBS US REIT.

I wouldn’t say that this creates a misalignment of interest because they’re all professionals here, but it’s still a point noting nevertheless. It’s not like a Mapletree or CapitaLand REIT where the sponsor is going to hold 30% of the REIT. Although to be fair, this is a side effect of the US Tax Code and Manulife REIT (another US REIT) has the same problem as well.

The other notable effect of this though, is that because no one unitholder can hold more than 9.8%, and because the market cap of this REIT is so small (about $500 million), a large proportion of the units are held by retail investors. And when a counter is held predominantly by retail investors, you can expect large volatility and big price swings, because as the argument goes, retail investors are less sophisticated and more prone to undisciplined selling. And that volatility is exactly what we saw in the past 3 months. Of course, it’s not necessarily a bad thing because it allows savvy investors to exploit the insanity of other investors, but if you do buy into this REIT, be prepared to buckle up.

The full list of investors as at IPO date for information:

Yield

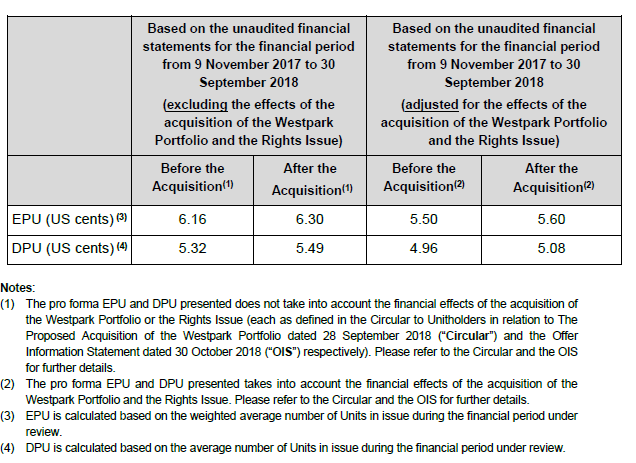

It’s tricky to calculate the yield for Keppel KBS US REIT because they made 2 acquisitions in the past 3 months, Westpark and Maitland Promenade I.

What I did was to take the pro forma numbers from their latest acquisition announcement (Maitland Promenade 1), checked them against the pro forma numbers in the Westpark acquisition circular, and double checked the assumptions made. The conclusion I came to, was that the numbers they published are generally quite accurate, but of course, don’t take my word for it. If you’re buying this REIT please double check the numbers again.

Anyway, if you use their published numbers of 5.08 cents distribution per unit (DPU) for 9 November 2017 to 30 September 2018, and annualise it for 365 days, you get an annualised DPU of about 5.68 US cents. Based on the 0.56 unit price in Dec 2018, that’s a whopping 10.1% yield. At today’s price of 0.64, that’s a yield of 8.88%, which while less ridiculous, is still really high (and much more auspicious…).

Even if we discount the DPU slightly for forex (USD has weakened a bit since) and we assume some negative rental reversions, that’s still a really high starting yield to play with.

Price/Book

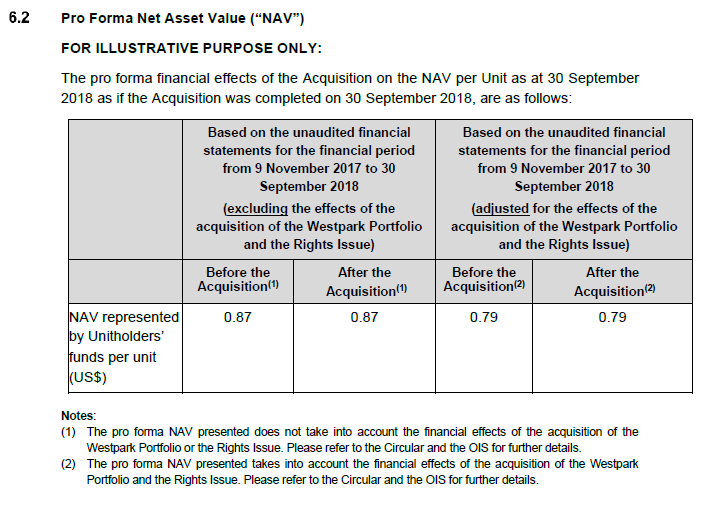

The Price/Book numbers are equally crazy. At a US$0.79 NAV per unit, the Dec 2018 price of 0.56 is a whopping 30% discount to book, while its current price of 0.64 is a 20% discount to book.

Assets

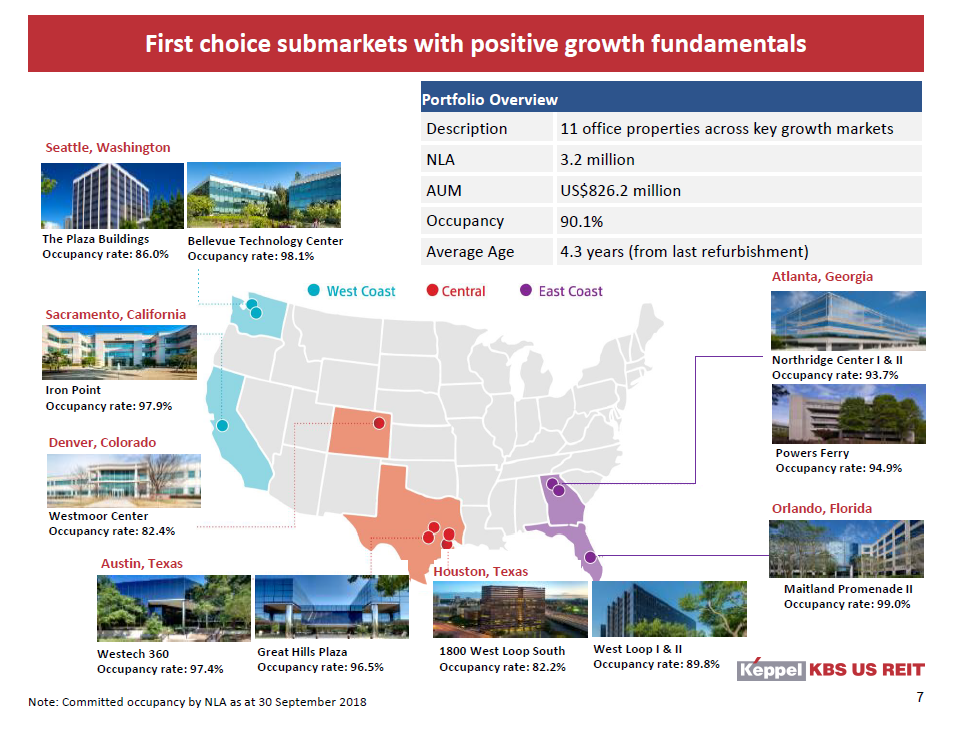

The IPO portfolio is set out below, and I did some digital sleuthing poking around google maps and google streetview, and the properties are generally well located near big cities with easy transportation access. Of course, with things like this there is no replacement for being on the ground and inspecting the property yourself, but I didn’t have this luxury, and would love to hear from anyone who knows these assets personally.

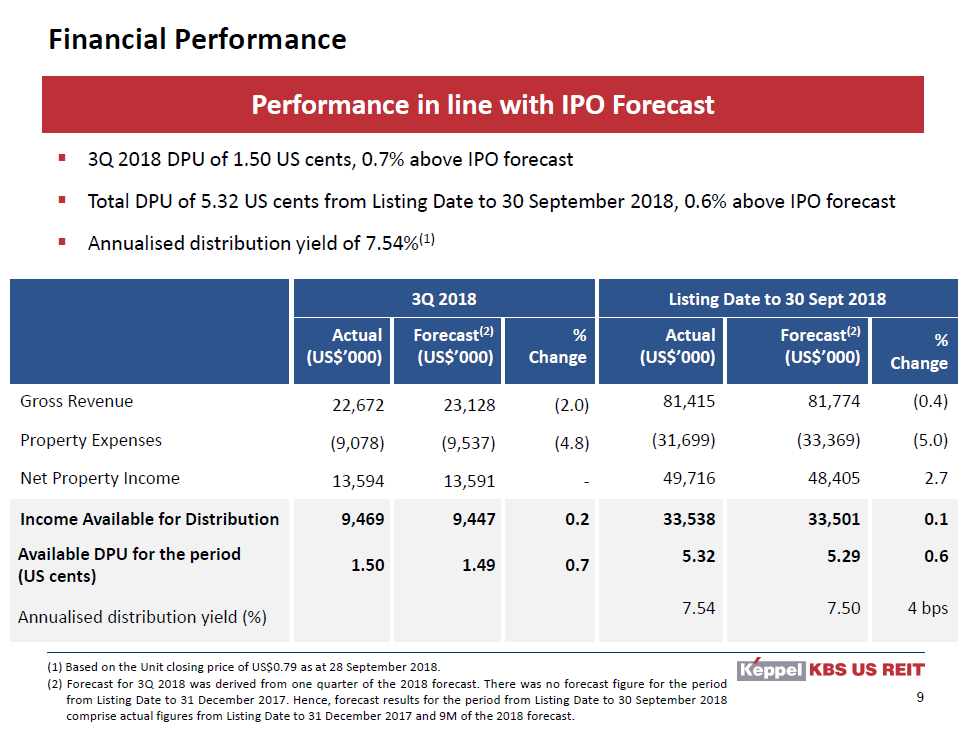

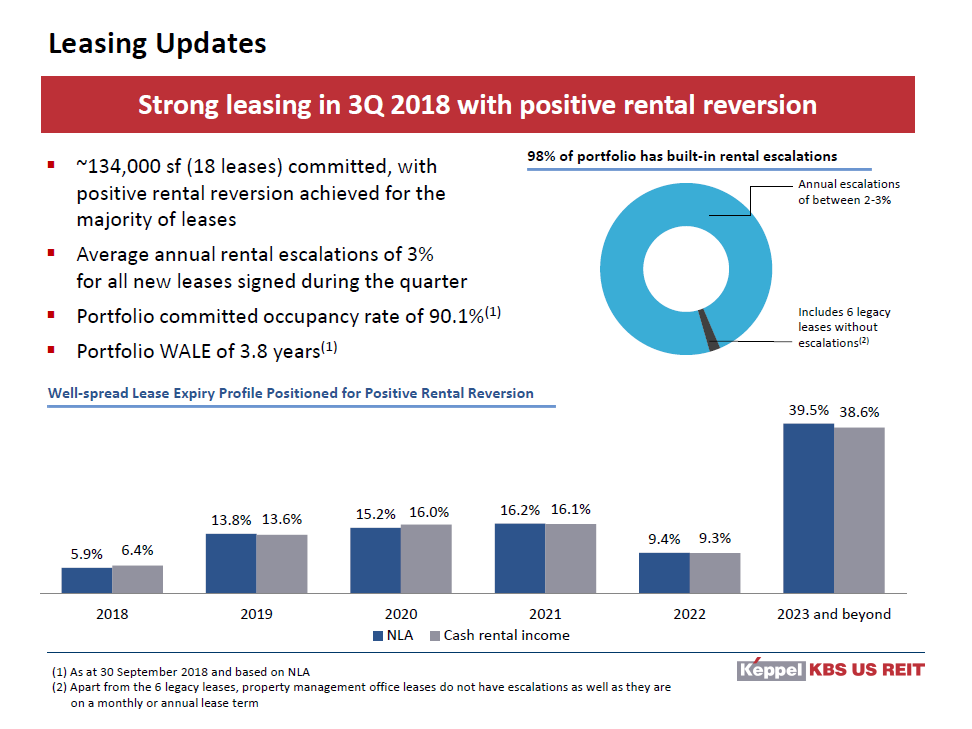

The 3Q numbers are set out below, and again they paint a rosy picture. Performance is well in line with the IPO forecast numbers, and looking forward, rental reversion has been positive as well. Nothing out of the ordinary really.

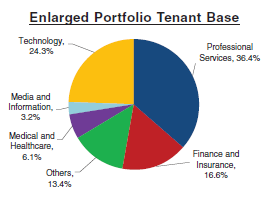

Geographical / Sector Allocation

You would’ve thought that you’d only see these numbers from a REIT holding Emerging Market assets in Indonesia or a non-core city in China. But no sir, these are assets in the US of A, the sole superpower and the largest and strongest economy in the world today. So that’s definitely a plus.

However, my second biggest fear about Keppel KBS US REIT (the first is another big rights issue), is the exposure to the US economic cycle. Personally, I think we are nearing the end of this short term debt cycle in the US, and that this is likely to come into play in the next few years.

Keppel KBS US REIT’s portfolio tenant base is highly exposed to Professional Services, Tech, and Finance, all of which are likely to be hit in a US recession. It’s incredibly hard to predict in advance how much a recession would affect net property income (NPI) because it really depends on the strength of the tenant’s core business, and the ability of the manager to negotiate and find replacements. Just imagine yourself owning 100 condos in Singapore, and you’re leasing them all out. Do you know for certain how much your rental would be hit if there is a recession in Singapore? There’s just too many variables here, and while we can expect NPI to drop, it’s a bit of a fool’s errand to predict how much it will drop.

Risks

Tax controversy

Back in Dec 2018, one of the largest risks was centered around the US tax code. Long story short, Keppel KBS US REIT utilises hybrid entities via Barbados to repatriate cash from US to Singapore, and there was a risk that changes in the US tax code would affect this tax structure.

Worst case, this would have led to withholding tax on all distributions – a 30% cut to DPU, and a possibility that this could be applied retrospectively, which would probably halve DPU for a few quarters.

Of course, this was the absolute worst case scenario, which I felt was incredibly unlikely, given the prevalence of such tax structuring for global companies.

Anyway, on 27 Dec 2018, Keppel KBS US REIT issued an announcement to clarify that they expected no tax impact as a result of the new US tax regulations. This immediately cleared up the whole issue, and catalysed the increase in unit price from 0.56 to 0.64 today. So if you’re buying in today, you no longer need to worry about this tax issue, but you’re paying a higher price because of the reduced uncertainty. The market can be quite efficient sometimes.

Rights Issues

My biggest fear with Keppel KBS US REIT is a large equity fund raising.

The fear goes like this. Keppel KBS US REIT has a tiny portfolio size, when compared to the other big boys like CapitaLand Mall Trust. Accordingly, the manager is going to want to grow its portfolio aggressively going forward (for acquisition fees, bigger base fees etc). With the gearing levels already quite near the 45% limit, any new acquisition is going to be funded by equity. And if they do another big rights issue, or a preferential offering / placement at a big discount, the unit price may sell off sharply again.

I think the risk of this is limited at the current unit price. When your equity is trading at close to a 9% yield, the cost of raising new equity is far too high, and it’s suicidal to even try unless you’re facing a 2008 style liquidity crunch. So if everything stays like this, the downside should be limited.

The problem though, is when the unit price goes up. Once unit price hits the 0.7x range, the cost of new equity becomes a lot less prohibitive, and I think this fear may come into play.

This puts me in a very strange situation as a Unitholder. On one hand, I want the unit price to go up, because that’s capital appreciation. On the other hand, if the unit price goes up too much, the REIT does a big equity fundraising, and not only do I need to cough up more cash, the price could sell off again. So you do need to watch the unit price closely for this one.

Gearing is high

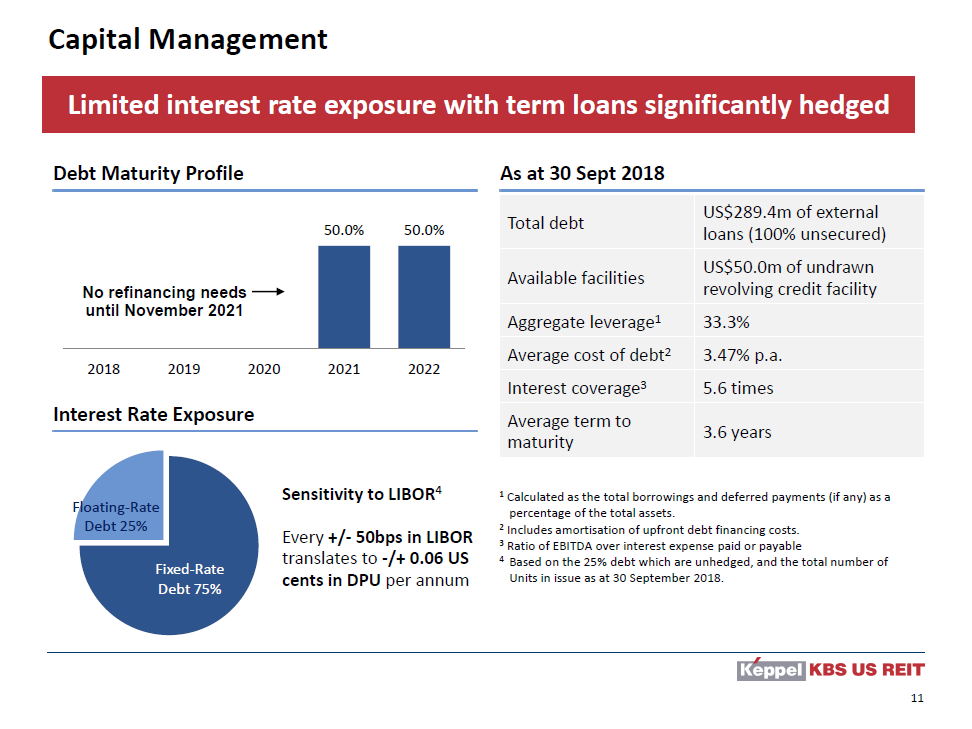

Because the recent Maitland Promenade I acquisition was fully debt funded, the post-acquisition gearing should be in the high 30s.

Based on the recent 3Q results presentation, Keppel KBS US REIT is on 75% fixed rate debt, with no major refinancing needs until 2021, so the rising interest rate environment shouldn’t hit them too badly. In any case, we’re probably nearing the end of this rate hike cycle, so I do expect the pace of hikes to moderate somewhat in the coming quarters.

Don’t forget your W-8BEN !

One minor annoyance if you do buy into Keppel KBS US REIT, is that all individual unitholders (ie. if you’re buying the REIT as an individual and not a company), need to fill up a W-8BEN tax form to avoid withholding tax on their distributions. So unless you want to lose 30% of your yield to the US tax man, just do yourself a favour and fill up this form, mail it to the unit registrar (Boardroom), and be done with it. You only need to do it every 5 years, so it’s not that bad.

Closing Thoughts

Analysing Keppel KBS US REIT reminded of the story of Mr Market. It goes like this. Imagine that the stock market is a schizophrenic salesman. Every day, he drops by your house and offers to sell to you a product (let’s imagine it’s an iPad). On the first day, he tells you the price of the iPad is S$500. Because you were in the apple store earlier, you know that the price of the iPad is S$500, so you politely decline him. The following day, he drops by your house and offers it to you at S$600. You know that it’s above the cost of the iPad so you tell him to go away and stop bothering you. On the third day, he offers it to you at S$200. You think he’s absolutely crazy, why would anyone sell it at such a large discount? You check the product thoroughly but they seem to be genuine apple products, so you proceed to buy 10 of them.

That’s exactly what I thought about this REIT when I was going through the financials in December. I remember thinking that the market was mispricing this REIT so horribly that I was quite sure I was missing something big. But I just couldn’t find it (Of course, if any of you guys spot something I didn’t, please please let me know in the comments below!).

Of course, this REIT isn’t without its risks. The risks of a large equity fund raising, or a US economic downturn are very real. But when you’re buying in at a 10% yield and a whopping 30% discount to book, and these are US assets, there’s a heck of a margin of safety. Even at its current price, it works out to a 8.88% yield and 20% discount to book, which is still really decent.

Back in Dec 2018, I would have given Keppel KBS US REIT a 5 Horse rating because it was THAT good. But after a 12% unit price appreciation, I think it’s no longer a 5 Horse, but still a really good buy nevertheless.

But of course, don’t just blindly buy this REIT based on this article. Reread my analysis, go through the financials and the company presentations, and decide for yourself whether this REIT is for you. You may not agree with my analysis, which is great, because one of the most important things as an investor is to be able to develop your own independent opinion, after evaluating all relevant facts.

The only thing that I know with absolute certainty is that mismatches in market pricing will definitely appear multiple times in the course of our investing career. The key here is to be able to build up the analytical skillset and judgment to be able to identify such stocks when they happen, and to have the conviction to believe in your analysis. Or you know… you could always just sign up for the FH Stock Watch at 5 bucks a month ?.

Financial Horse Stock Rating – Keppel KBS US REIT

Financial Horse Rating Scale

Till next time, Financial Horse, signing out!

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. Enter your email below to receive a copy!

[mc4wp_form id=”173″]

Enjoyed this article? Do consider supporting us and receiving additional exclusive content!

Like our Facebook Page for more great articles, or join the Facebook Group to continue the discussion!

Similar thoughts. Bought in at 0.57 and sitting tight for the good returns in many years to come.

One other reason I like this is the strong macro factors of employment and economic GDP in america. It is a boon for this industry.

Add the freehold factor and tax reform (unlikely to change drastically for quite a while), it could be a homerun multibagger.

Agreed! That being said, if the price goes up by too much, I may actually look to cash in, because the risk of another big rights issue going forward does trouble me.

Cheers!

Good post. I have this counter and bought the excess rights as well.:)

Great! Thanks for sharing! 🙂

Thanks Financial Horse for the detailed analysis and sharing on KBS…appreciate! I am worried about the current trade war between US and China and the spillover impact on global economies….Trump is just too unpredictable and there is a high chance that he may sink US economy while under his watch soon….but long term wise coupled with the freehold assets will be good. If I have more cash available, will look into accumulating some of it. 🙂

No problem! Yes, the macro environment is quite uncertain now, we’re quite late cycle and the chance of a recession in the next 2 to 3 years are high. At the current price, it’s less of a must buy, but if it dips to the 0.5x range again, it could be interesting.

Hi, thanks for the great article! I have a question regarding what you wrote about W8BEN.

My understanding is that as long as I (SG citizen) has previously traded US stocks (whether SG brokerage or such as InteractiveBroker), it would have been mandatory for him to have submitted the W8BEN. I recalled doing so in the past – but am not sure whether it has expired (I’m still holding onto US stocks).

By right they will send you a reminder to re-submit the W8BEN near expiry correct?

Hi there! That’s a really good question. Unfortunately I’m not a tax advisor so I’m not able to provide a definitive answer on this, but my suspicion is that the answer will depend on how Keppel KBS US REIT files their withholding tax with the IRS.

To be on the safe side, I would just fill in the W8BEN and submit to boardroom for Keppel KBS US REIT. Otherwise, the only other way to know for certain is to wait for your next distribution and check if 30% was taken off for withholding tax.

Unfortunately, Keppel KBS will not send you a reminder to re-submit the W8BEN, the admin costs to do that for all unitholders (and keep track of the numbers) would be crazy. The onus is on the unitholder to ensure the right forms are filed.

Really great question though, and I’ve answered based on my understanding as an investor, so I may not be as accurate as a tax advisor would be.

Hi, thanks for your advice!

I did find this on their website: “Boardroom Corporate & Advisory Services Pte. Ltd, the Unit Registrar of Keppel-KBS US REIT, will dispatch US Tax Forms to each non-US Unitholder that does not have valid documentation on file prior to Keppel-KBS US REIT making any distributions to Unitholders.”

Though, I believe you are right that they will likely not send a reminder to every unit-holder. As such, I’ll take the conservative way and resubmit a W8BEN to the Unit Registrar.

Thanks again!

Yep, I do think it’s better to be safe than sorry here, since it’s as straightforward as filling in a form and mailing it to them.

Cheers!

Compared this to Manulife REIT, which would you think would be suitable for long term?

THey’re quite different really, one is business park style one is office. At the same price/book and yield, probably Manulife REIT. But Manulife usually trades a bit more expensive than Keppel KBS. 🙂

Hi there,

I was reading your article about withholding tax which had led me to this article.

In that article, it was mentioned that by filling up the W8 Ben form, we are declaring our status and allowing the IRS to take out 30% from our dividends income.

However, in the article, it is mentioned that we can avoid 30% withholding tax on the distributions(aka dividends, if I am not mistaken) by filling up the W8 Ben form.

I am a quite confused. I have made queries to different brokerage to ask them about the W8 Ben form and got back different answers.

It will be really helpful if you can help me on this.

Thank you.

Hi!

Withholding tax applies to dividends. The REIT structuring employed by these Singapore listed US REITs are exempt from withholding tax (there are certain restrictions – eg. No unitholder can hold more than 10% etc), as long as you fill up the W8BEN.

So yeah, long story short, definitely fill up the W8BEN. 🙂

Ok. Thank you very much for your reply.

So can I say that all Singapore Listed US REITs will be exempted from withholding taxes as long as we fill in the W8 Ben form?

Are there any other instruments that will allow us to be exempted for the 30% withholding tax on dividend income?

How can one know which one is exempted and which is not?

Best Regards

Shwu Shenn

Well I can’t speak for future REITs, but all those listed on Singapore now are structured to avoid withholding tax (otherwise it doesn’t make sense to list here). With withholding tax they will not be competitive investments.

Treasury bonds are also exempt – but the exemption procedure for Treasuries is more complex. You will need to check with your broker on the procedure. Some brokers will fill up the paperwork for you, some will not.

No blanket rules here, it’s based on the tax code, so it’s really just experience and knowledge. The 2 products above are the main exemptions for now.

Hope this helps! 🙂