In case you missed it – Keppel Pacific Oak US REIT dropped as low as $0.34 last week.

At that price, it works out to a 56% discount to book, and a whopping 17% dividend yield.

So yes, we all know that the US office market is in a rough patch right now.

But at what price would this start to be priced in?

Let’s take a closer look.

Note: This is a premium Patreon post written on 3 April 2023. I am releasing it to all readers as I have been getting quite a few questions on US REITs – and hopefully this might help you in your investing journey.

Please note that this article has not been updated to account for new information since 3 April 2023.

For latest views, do support Financial Horse as a Patreon. You can get regular premium updates just like this, together with my full REIT and stock watchlist.

Sign up here.

Keppel Pacific Oak fell on high volume, but no notable news

Worryingly – Keppel Pacific Oak fell from 0.39 to as low as 0.34 last week on very high volume.

It’s since recovered to 0.38, but you can see quite clearly that the recovery volume is significantly smaller than the volume during the drop.

So this is quite bearish.

I tried digging around to see if there was any news to explain the decline, but I couldn’t really find anything on this.

No news reports, no SGX announcements.

Sell-off due to Manulife REIT?

Perhaps some of the sell-off might have been due to investors worried about what is going on with Manulife REIT.

Or perhaps it could just be high net worth individuals getting margin called and forced to dump their positions.

Who knows.

Sidenote: Manulife REIT itself is a story for another day, but for now let me just say that Manulife REIT is in a big enough mess that I don’t see myself touching that REIT even at these prices. I think the situation there is very concerning, and it’s hard to see how they can restructure their way out of it without significant dilution of equity holders.

DBS thinks US REITs are close to a bottom

For what it’s worth, DBS Research thinks that the bottom is near.

Here’s what they say:

“The US-listed office REITs are currently trading at 0.75x price-to-book (P/BV), close to the lows seen during the global financial crisis (GFC), writes Tan in a March 27 note. “While the US office S-REITs do not have sufficient trading history stretching back to the last crisis, we believe that at 0.5x P/B, it is close to the bottom and awaiting a catalyst.”

Tan believes the re-rating catalyst lies in the Fed moderating or pausing interest rate hikes, which will also drive a turnaround in the share price.

DBS’s preferred pick is Keppel Pacific Oak US REIT (KORE) CMOU 0.00% , which has shown more resilient operations compared to its peers. On the other hand, Manulife US REIT (MUST) BTOU 2.33% has de-rated the most and would probably see the overhang lifted once it resolves its capital management issues, writes Tan.”

Just to put it out there that DBS Research has been out with a buy call on REITs for most of the past 12 months as REIT prices kept sliding, so I wouldn’t take DBS’s views too strongly from a timing perspective.

That being said, I do agree with the general points they raise.

In that among the US office REITs, Keppel Pacific Oak is probably my favourite if I had to pick one.

And that at 0.5x book value, market is pricing in very severe distress here.

To the point where it warrants a second look at some of these REITs.

Keppel Pacific Oak US REIT – High level overview from a fundamentals perspective

I’ll just survey the high level figures quickly.

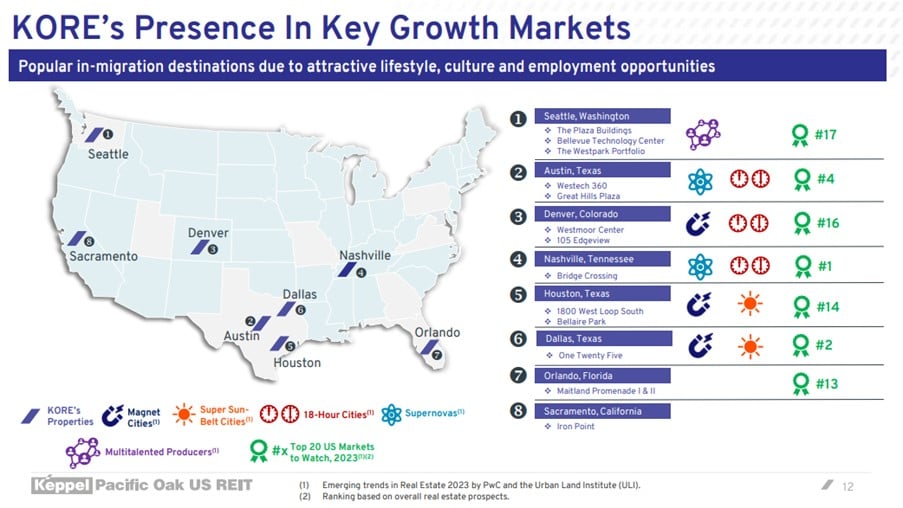

Property Portfolio of Keppel Pacific Oak US REIT

It’s worth noting that Keppel Pacific Oak’s portfolio stays away from the big gateway cities like New York and SF.

But instead focusses more on the sun belt cities like Texas.

I see this as a good thing because I would be more worried about highly priced New York / SF office real estate in the next 12 months.

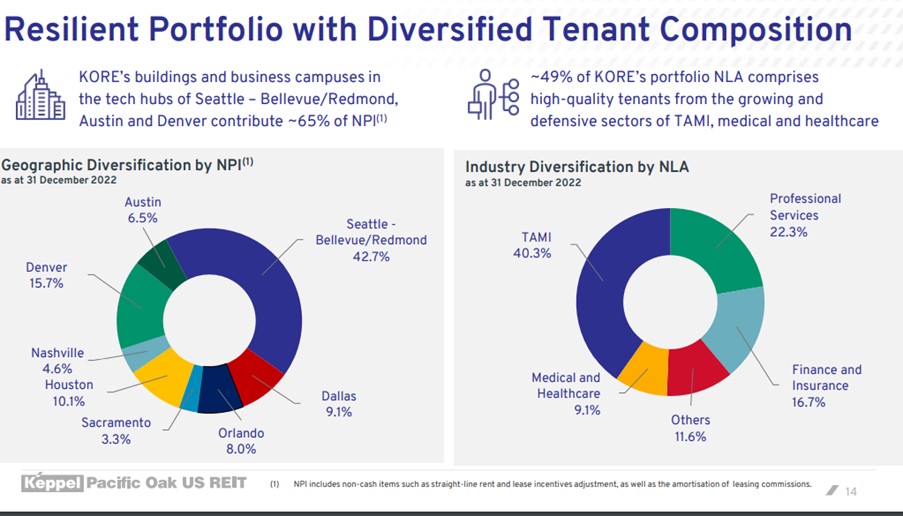

You can see rental split below.

Big exposure to the tech sector in Seattle, and big exposure to professional services / finance.

We look to be headed into a patch of economic weakness in 2H 2023 / 1H 2024, so this portion will no doubt get hit in the months ahead.

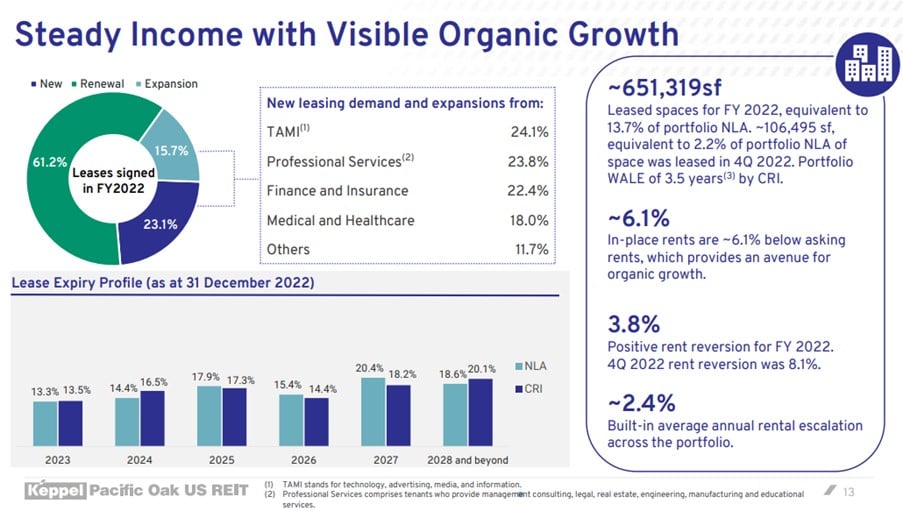

Note that they have about 14% of their lease that are expiring each year.

Whether they will be able to roll over these leases at existing levels of rent is a bit of a question mark too as we head into the economic slowdown.

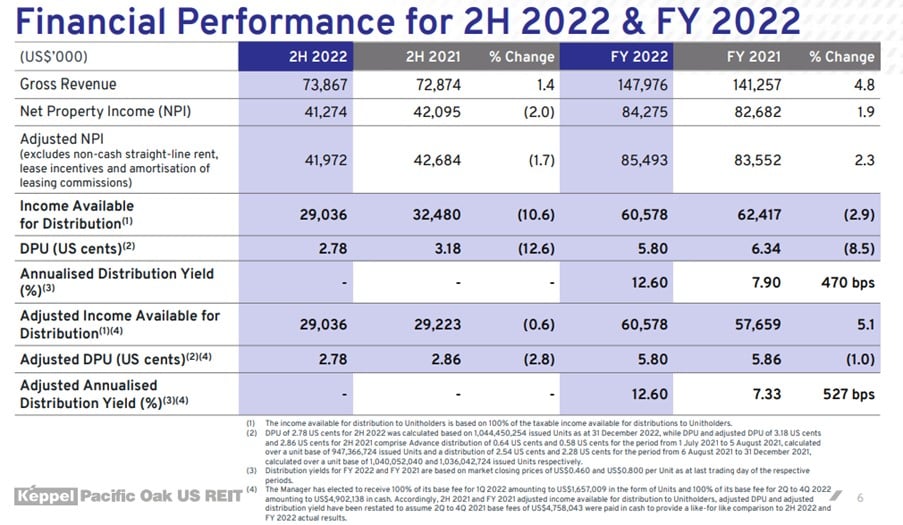

Financial numbers of Keppel Pacific Oak US REIT

FY 2022 DPU is 5.8 cents which works out to a 15% yield at latest price of $0.38.

Even if you assume a 10% drop in DPU, you’re still looking at double digit 13%+ yields.

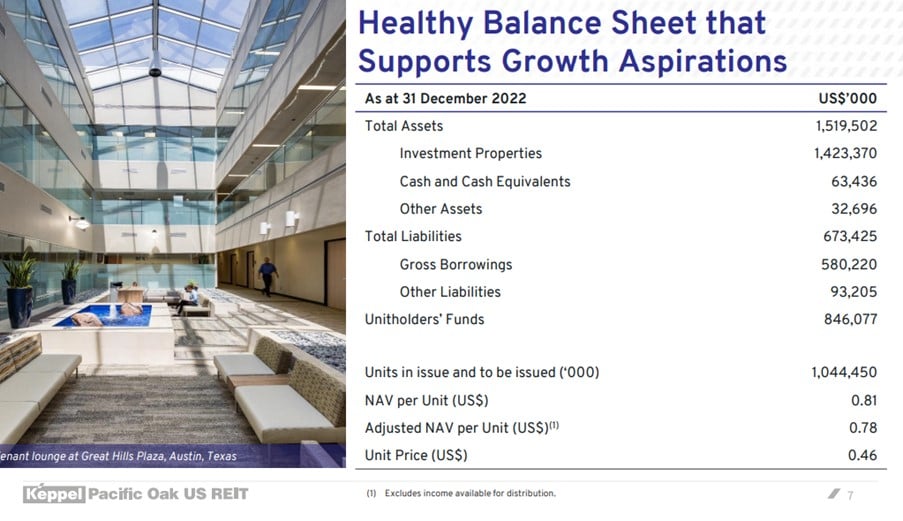

NAV is $0.78 which means a 50% discount to book at this price.

Keppel Pacific Oak US REIT’s property portfolio is valued at a 5.9% cap rate on average.

At a 50% discount to book, you’re basically buying in at an 11.8% cap rate for real estate portfolio.

At last week’s low of $0.34, that would have gone as high as a 13.5% cap rate.

US Office is pricing in deep distress

For those who haven’t been following US real estate, the office space in the US is not doing well.

Post COVID, many companies transitioned to a hybrid working model which drastically reduced the need for office space.

This led to a lot of excess office space across the board, and a big drop in occupancy rates.

Many offices are starting to be repurposed to residential spaces.

For now, you haven’t really seen the true impact on valuations yet because owners are still trying to keep afloat by rolling over their debt.

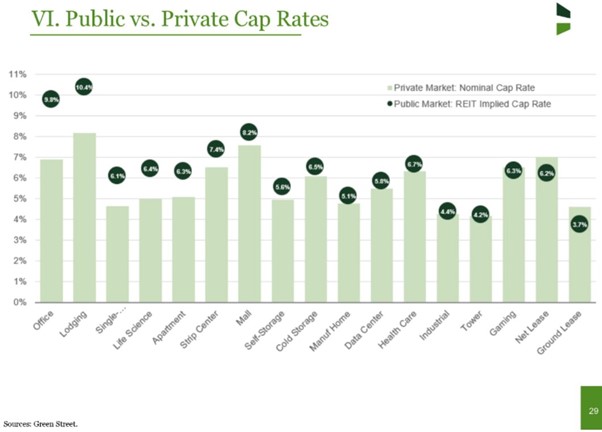

But you can see from the chart below that public markets have already sniffed out the coming distress and started to price this in.

This chart shows the difference in public vs private cap rates for US real estate.

Private markets are still valuing offices using 2021/2022 prices of 7 – 8% cap rates.

Whereas public markets have already priced in higher interest rates and potential distress in the next 12 months – with cap rates at 10% range.

11.8% cap rates – Is that reasonable?

Whatever the case though, Keppel Pacific Oak at around 12% cap rates is on the higher side of the cap rates of the table above.

If you ask me, I think 12% cap rates are probably close to pricing in the distress from a fundamentals perspective.

Of course there is a good chance that valuations will overshoot to the downside in the next 12 months as we progress into the downturn.

Especially since we haven’t even gotten to the stage of forced sales yet.

The longer interest rates stay at these levels, the more you’ll start to see private owners being unable to roll over their debt and forced to dump their properties into a market where there is no liquidity – meaning there is a good chance that prices will overshoot to the downside.

But fundamentals wise, I think 12% cap rates probably starts to price in the distress.

Insolvency risk of Keppel Pacific Oak US REIT?

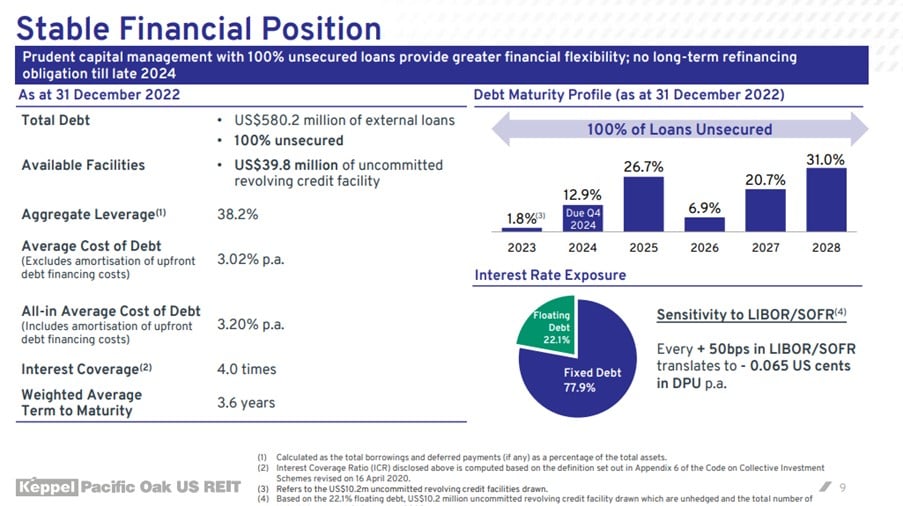

All the debt is unsecured which is a good thing.

No immediate refinancing needs until Q4 2024.

After that – there is a $74 million chunk of debt due by Q4 2024 that needs refinancing.

And then a massive $154 million chunk of debt due in 2025.

That said if we’re still sitting at 5% interest rates by end 2024, I think bigger things would already have broken elsewhere in the economy.

Shareholders of Keppel Pacific Oak

Probably a bit concerning is the fact that the 2 sponsors – Keppel and Pacific Oak, only hold about a 7% stake in the REIT each.

This raises some questions over alignment of interests.

In the event that the REIT needs sponsor support in the next 6 – 12 months, can you count on the sponsors coming in in a way that would safeguard unitholder interests?

Not so sure.

My personal views on Keppel Pacific Oak US REIT

The way I see it, at these prices (low 0.30s) I could be convinced to pick up a position.

I shared before that Keppel Pacific Oak US REIT is my favourite of the US REITs.

And at 12 – 14% cap rates (0.34 – 0.37) I think it starts to price in the coming distress from a fundamentals view.

But don’t kid yourself though, there’s no free lunch in this world.

The market is pricing in double digit cap rates / dividend yields because there are very real risks here.

The US office market is not in a good place, and you’ll see vacancy rates go up the next 12 months due to economic slowdown, and probably a lot of forced sellers once their debt comes due for refinancing.

I would expect the next 12 months to be bumpy for US Commercial Real Estate (CRE), especially so for office space.

Based on the above it doesn’t look like there is a material risk of insolvency or a dilutive equity fundraise.

But hey – sometimes you don’t know what you don’t know.

What catalyst could spark a recovery in share price?

From the DBS article:

Tan believes the re-rating catalyst lies in the Fed moderating or pausing interest rate hikes, which will also drive a turnaround in the share price.

I’m not so sure about this one frankly.

I don’t see how these US REITs will rally simply because interest rates are going to stay at 5%.

With 5% interest rates a lot of owners are going to be unable to refinance their debt or cover interest expense, and be forced to default or sell into a market with no liquidity.

Just like with the China real estate crisis last year, I don’t see any silver bullet out of this crisis.

Remember all the criticism from the West last year on how China after inflating a huge real estate bubble needs to either (1) allow all the real estate debt to default and take a huge writedown in real estate prices, or (2) allow real estate prices to drop over an extended period (like Japan in the 1990s).

Well, now that the tables are turned, I see exactly the same for US CRE.

US CRE was inflated into a massive bubble on the basis of zero interest rates.

Unless interest rates go back to zero, you’re going to be faced with the same 2 options:

- Allow the debt to default and take a huge writedown in real estate prices, or

- Allow real estate prices to drop over an extended period (ie. Japan in the 1990s)

Basically, you either let the pain play out quickly, or you let it play out slowly.

The underlying problem here is that this asset class is priced based on interest rates at 0%, and interest rates are now at 5%.

So while a true Fed pause can spark a short recovery, I find it hard to see a sustained recovery short of a change in Fed policies.

So buy this REIT now… or buy later?

So… should one buy now when we are still early in this crisis, or wait until 2H 2023 when the crisis plays out a bit more?

And frankly, I don’t have any easy answers to this one.

Investors with high risk appetite might consider buying a position at these prices to hold for the long term (or to sell if we get a short term rally).

Investors who are more risk averse might want to let things play out a bit more (or avoid the counter entirely).

For me, I think at the low 30s I could be convinced to buy a position to hold long term (or sell if we get a rally).

But I am going to position size carefully, and I may have a stop loss in place to limit my losses here.

Note: This is a premium Patreon post written on 3 April 2023. I am releasing it to all readers as I have been getting quite a few questions on US REITs – and hopefully this might help you in your investing journey.

Please note that this article has not been updated to account for new information since 3 April 2023.

For latest views, do support Financial Horse as a Patreon. You can get regular premium updates just like this, together with my full REIT and stock watchlist.

Sign up here.

WeBull Account – Get up to USD 500 worth of fractional shares + chance to win USD888 / Tesla Model 3 (expires 30 May)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares, and a chance to win USD 888 or a Tesla 3.

You just need to:

- Sign up here and fund any amount

- Maintain for 30 days

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Looking for the best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Dear FH

Agree and echo your views as regards CRE

This is a very difficult situation and I hold all three US office REITS and rue my decision of chasing yield – but these were bought preCOVID when the world was a different place!

Looking forward, I have desisted from averaging down and will not touch these until rates start falling

Honestly, the risk reward is much better if I deploy funds elsewhere wherein capital preservation can be expected for sure

No point in trying to average down when you cannot predict the way office space will do, these properties cannot be redesigned easily and put to alternate use

They will not find buyers either

Actually, I am mentally preparing to write off my investments

You cannot win all battles all the time and these have been my biggest losers

Regards

Garudadri

Hi Garudadri,

Thanks for the great sharing as always.

The US REITs did indeed look very good in the past, but what a difference COVID and interest rates going from 0% to 5% has done!

I think the way things are playing out, the Feds may eventually be forced to cut interest rates when the economic slowdown hits. The only question is one of timing.

So for investors who can pick REITs with solid real estate, and which will not go bankrupt / dilute massively over the next year or two, and pick them up at attractive pricing – there could be an opportunity to outperform here.

Of course, question then is does Keppel Pacific Oak fit the bill, and if so at what price would it be sufficiently attractive?

hi FH

Yes, position sizing is key, especially when the future is quite murky.

The current price likely has priced in a lot of downsides. The question is whether one is comfortable to hold KORE if Fed interest rate is 5.x% for next few years.

If you have Tikr account, the transcripts of last two earnings call on KORE are in Tikr. From the transcript, KORE’s loans could be from Singaporean bank(s), which reduces the risk of not able to borrow from US regional banks (which is holding a lot of CRE loans).

Thanks for sharing this, very helpful.

If you tell me the Fed rates will stay at 5% for the next few years, there is absolutely no way in hell I am touching US CRE right now.

But I doubt the Feds will be able to keep rates at 5% for that long. Other parts of the economy will show serious problems by then.

The only question now is one of timing.

I think the market cap implied net property yield is not 11.8% as there is debt and leverage here. The NPI yield on the book is on a unlevered basis.

The number is closer to 8-9%

You are right, thanks for pointing this out. I did not account for the debt in my numbers.