I’ve been getting quite a few questions on the US REITs recently.

In case you missed it, most of these REITs are trading at double digit dividend yields.

At current price of $0.44, Keppel Pacific Oak US REIT trades at a 13.7% dividend yield, and 0.55x book value.

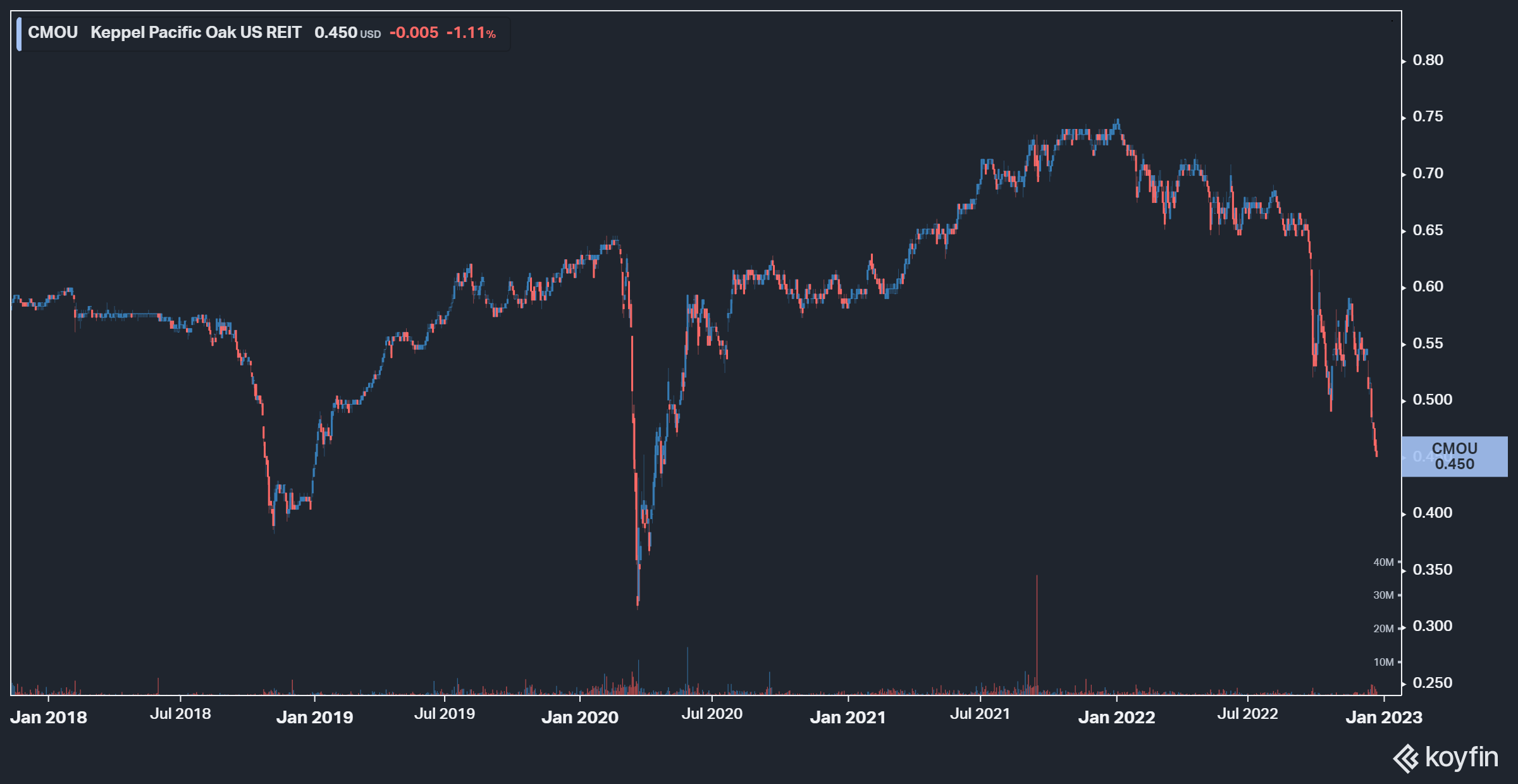

Here’s the chart since IPO, you can see what a complete disaster it’s been since Jan 2022:

So yes – we all know the US macro situation is bad and likely to get worse before it gets better.

But… at this price, is Keppel Pacific Oak US REIT worth a buy?

Dividend yield of Keppel Pacific Oak US REIT

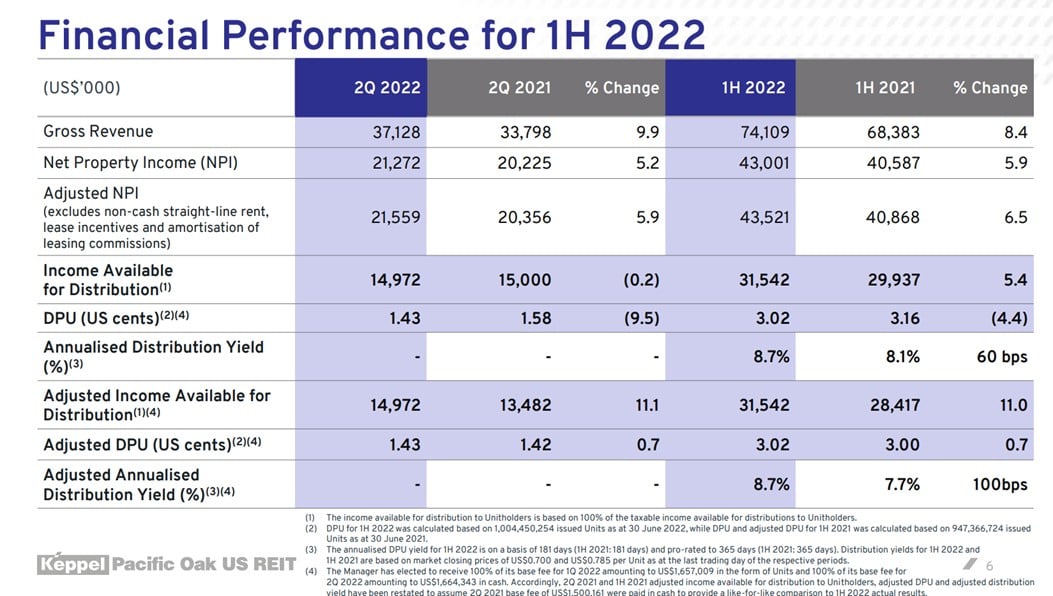

DPU for 1H 2022 was 3.02 cents.

If we annualise that, and using the current unit price of $0.44 – that’s a mind blowing 13.7% dividend yield.

You can see this visualised in chart form below.

This is the highest dividend yield Keppel Pacific Oak US REIT has traded at since COVID in March 2020.

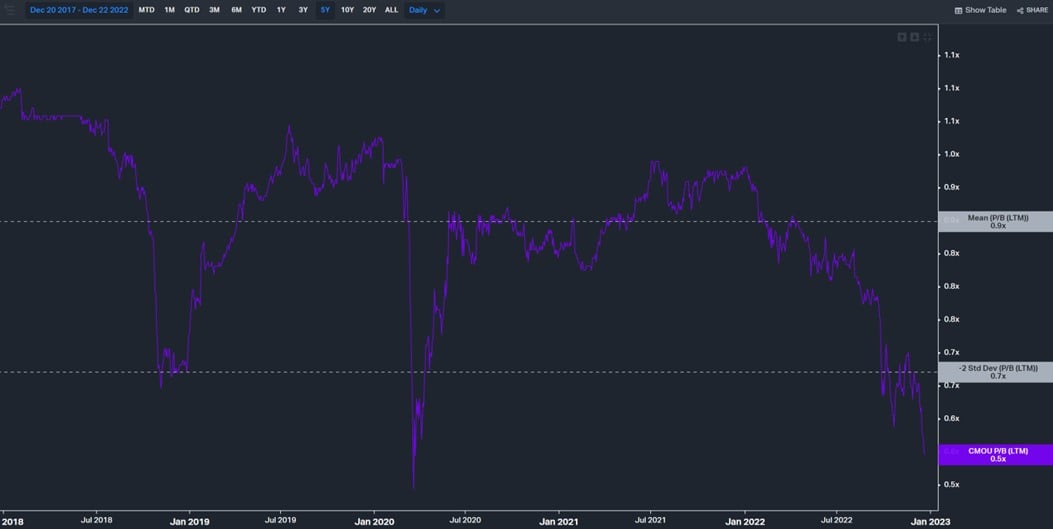

Price / Book of Keppel Pacific Oak US REIT

Price to Book ratios are equally ridiculous.

0.55x Book Value.

Again, this is the lowest it’s been since COVID in March 2020.

Well below 2 standard deviations below mean.

Running a very simplistic analysis, the Keppel Pacific Oak US REIT property portfolio is valued at about a 5.9% cap rate.

At the current 0.55x book value, you’re basically buying into the real estate portfolio at 10.3% cap rates.

So yes – we all know the US macro situation is bad and likely to get worse before it gets better.

But… at this price, is Keppel Pacific Oak US REIT worth a buy?

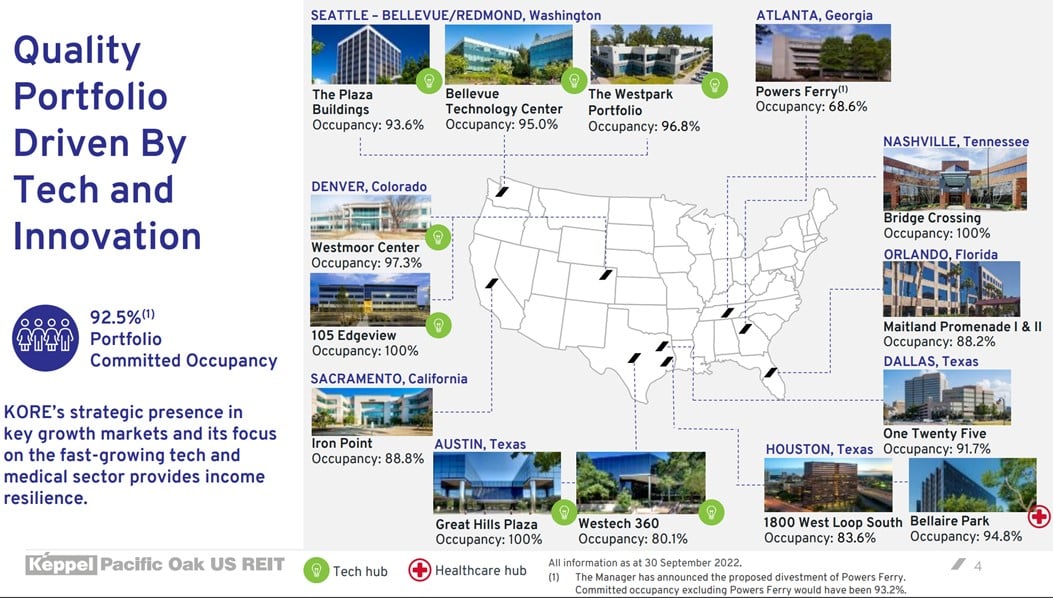

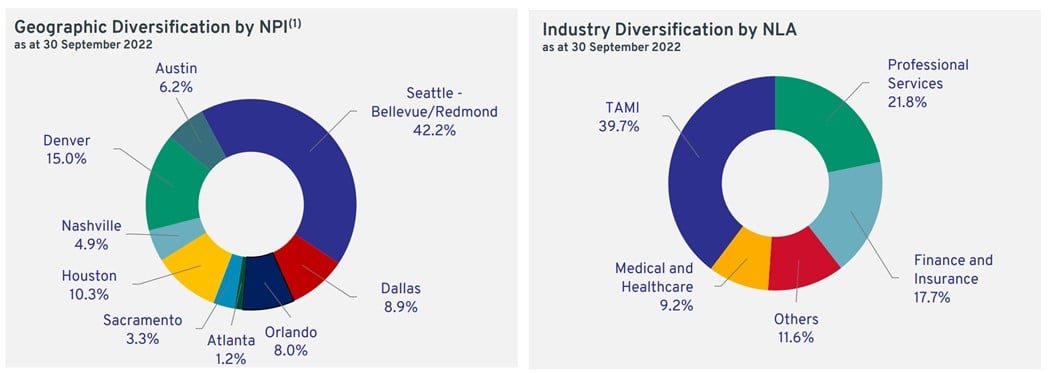

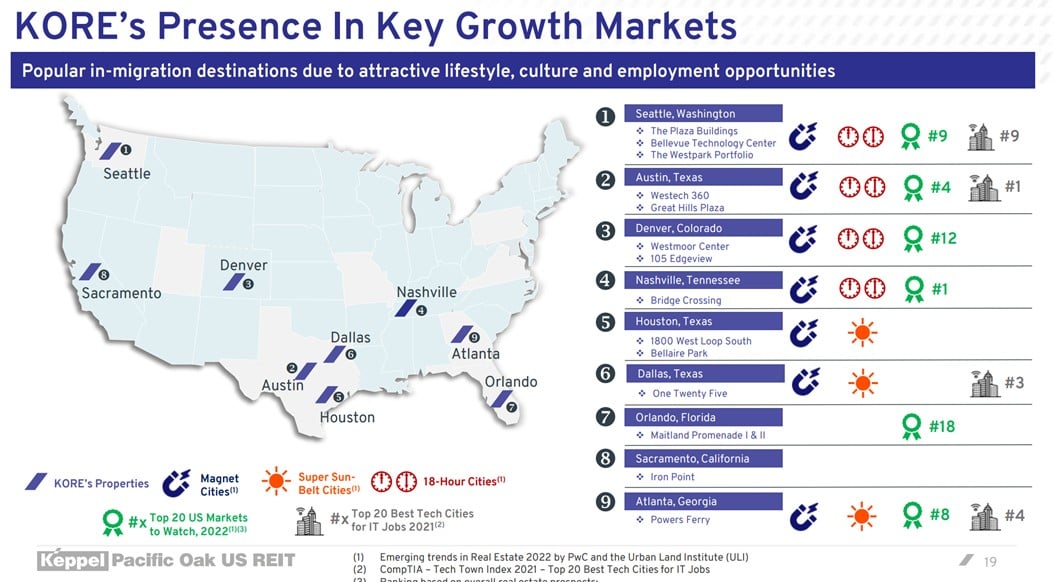

Property Portfolio of Keppel Pacific Oak US REIT

Let me just put it out there that between the SGX listed US office REITs, Keppel Pacific Oak US REIT is probably my favourite.

I like how the property portfolio is structured – with properties in key growth markets, and focussing on the tech sector.

They stay away from the “Tier 1” cities where prices are high and yields are lower.

And focus more on the “growthy” cities like Austin, Dallas, Denver etc where you can get cheaper valuations and higher yields.

For those familiar with China real estate, this is a similar strategy to how most of the Singapore listed China REITs play it.

The Tier 1 cities are usually very fully valued, which means you cannot make DPU accretive transactions there, and growth potential is low.

Whereas by focussing on the Tier 2 cities, you get higher yields, and higher growth potential.

Yes not denying that this is a higher risk play because you’re not buying in the Tier 1 cities.

But personally for a REIT this would be how I would want to do it, it’s a measured approach to taking risk in my view.

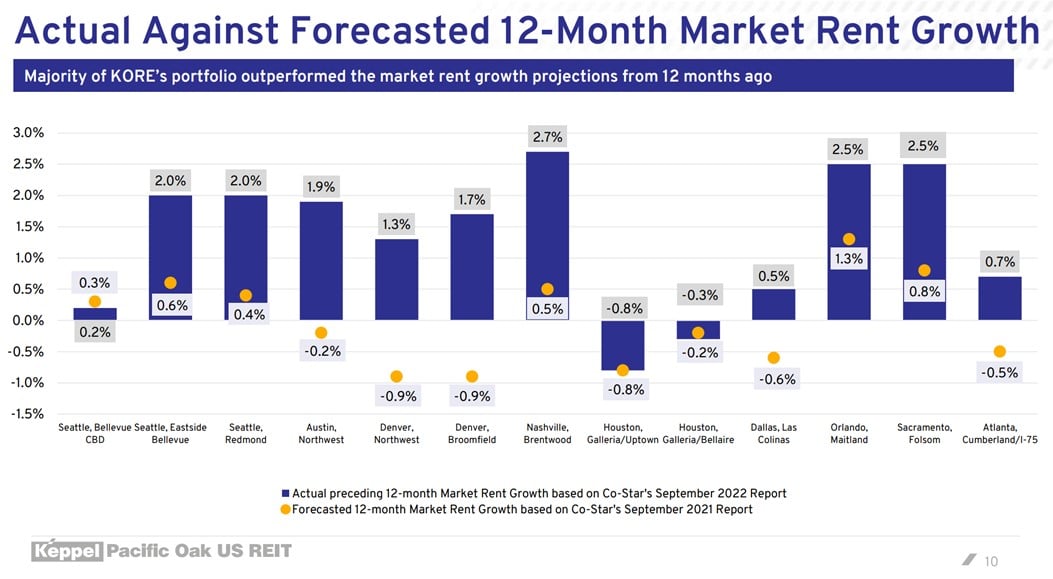

Property Performance of Keppel Pacific Oak US REIT

Property performance looks good.

Rental growth generally outperforms the benchmarks in the same city:

Top 10 tenants are quite diversified, so there’s no big concentration risk.

What worries me about Keppel Pacific Oak US REIT

Okay who are we kidding.

The market does not value a REIT at a 13.7% dividend yield and 0.55x book value unless it expects something very bad to happen.

So let’s talk about the risks that concern me for Keppel Pacific Oak US REIT:

- US Macro Risk from rising interest rates

- Potential Insolvency Risk?

- Dilutive Rights Issue?

US Macro Risk from rising interest rates

I know we are all sick of talking about interest rates at this point.

But frankly, I think any trade you make the next 6 – 12 months is going to be a pure macro trade.

The time will come for fundamental bottom up stock picking, but for now at least, I think it’s all macro.

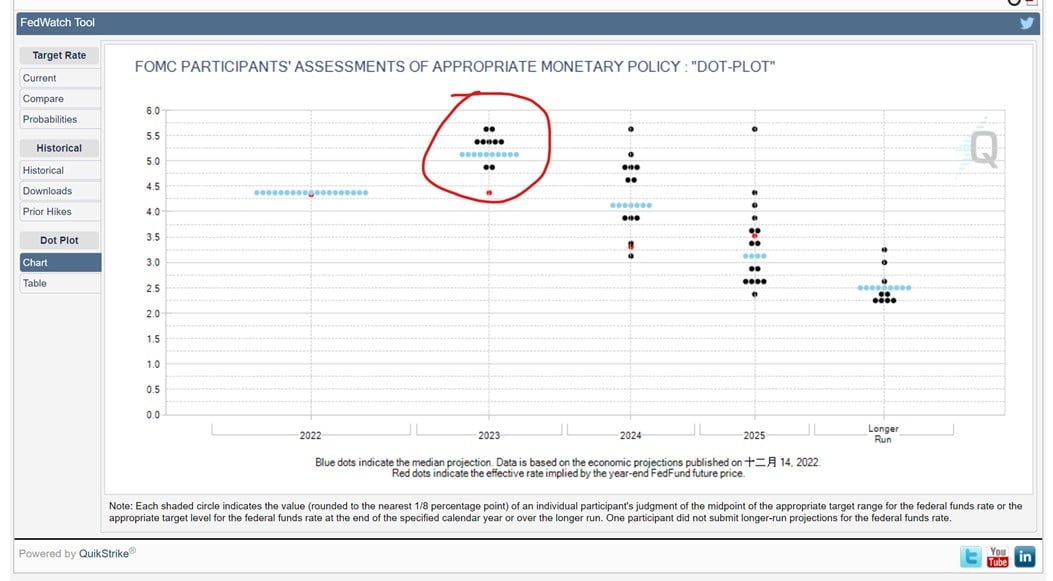

Latest FOMC dot plot shows that the Feds expect interest rates to peak at 5- 5.25% in 2023, before declining in 2024.

That’s crazy stuff.

A year ago you tell anyone that interest rates would be going to 5%+ in the span of 12 months, and they would have laughed you out of the room.

And now that it’s actually happening, and people are expecting a “soft landing”.

Markets are pricing in interest rates to stay high for at least the next 6 – 12 months, before declining after.

Which leads us to the question – if interest rates stay at 5%+ until mid to late 2023, what is that going to do to the US real estate sector?

We’re already seeing early signs of the impact.

In my previous REITs article I talked about how Blackstone has gated redemptions from their private REIT due to capital outflows.

The problem here is that a lot of real estate (both in the US and globally) is locked up in private real estate funds.

As interest rates go up and losses mount, investors start pulling funds.

Even if the real estate fund is doing well, investors nursing losses elsewhere may start to pull funds.

And real estate is an illiquid asset class – you cannot raise liquidity without selling properties, which takes anywhere from 6 to 12 months to complete.

In 2023, a lot of these private funds are going to shift from net buyers to sellers, to meet redemption requests.

That’s going to impact real estate valuations, not in a good way.

A storm is coming for commercially real estate globally (not just the US), in my view.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

But FH… there is no point in market timing as a long term investor…

Okay, I know what a lot of you are going to say.

You’re going to say that there is no point trying to market time as a long term investor.

Keppel Pacific Oak US REIT is cheap, so you can just buy now, and average in over the next 12 months, and you’ll make a lot of money once we emerge on the other side of this cycle.

Fair enough.

To execute a strategy like that though, there are 2 things you need to watch out for:

- Insolvency Risk

- Dilutive Rights Issues

Insolvency Risk?

To buy and hold a REIT, you need for it to well… not go bankrupt.

Let’s start by taking a look at refinancing risk.

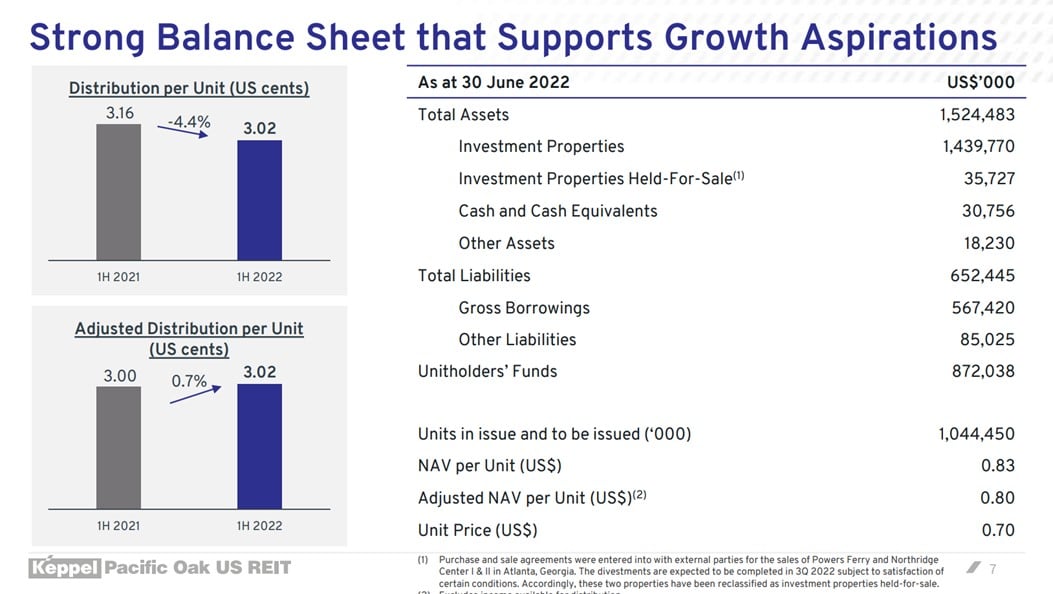

Debt situation of Keppel Pacific Oak US REIT

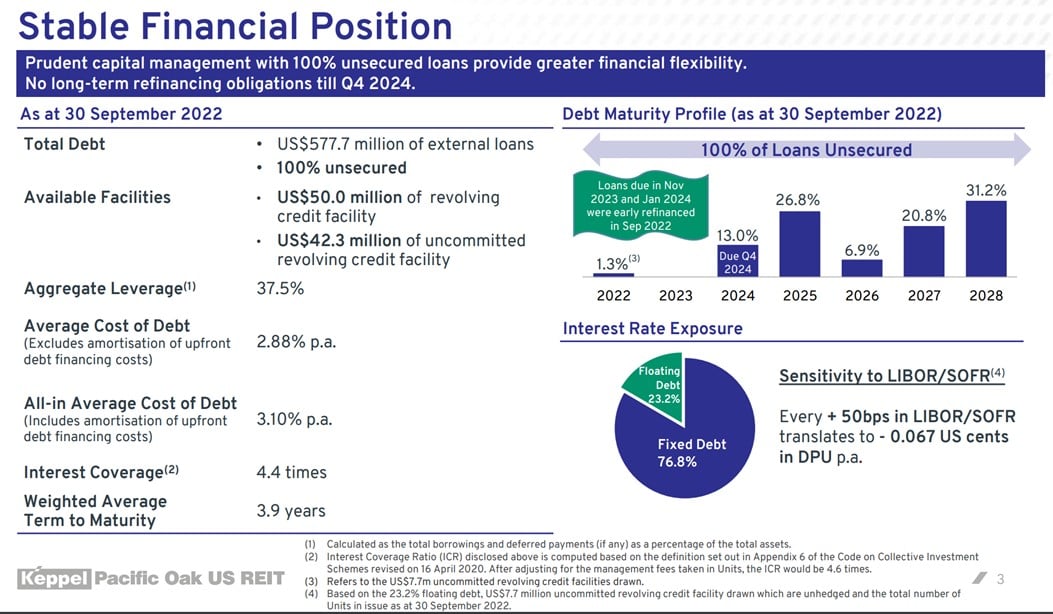

Fortunately, management has done well in refinancing all their debt out till Q4 2024.

So no refinancing risk until Q4 2024, which is great comfort.

If we are still at 5% interest rates in Q4 2024, boy… have we got bigger problems.

And currently, only 23% of their debt is floating rate in nature.

This means that every 0.5% increase in LIBOR translates to a $0.067 drop in DPU.

Or in other words – 1.1% drop in DPU for every 0.5% increase in LIBOR.

Pretty decent.

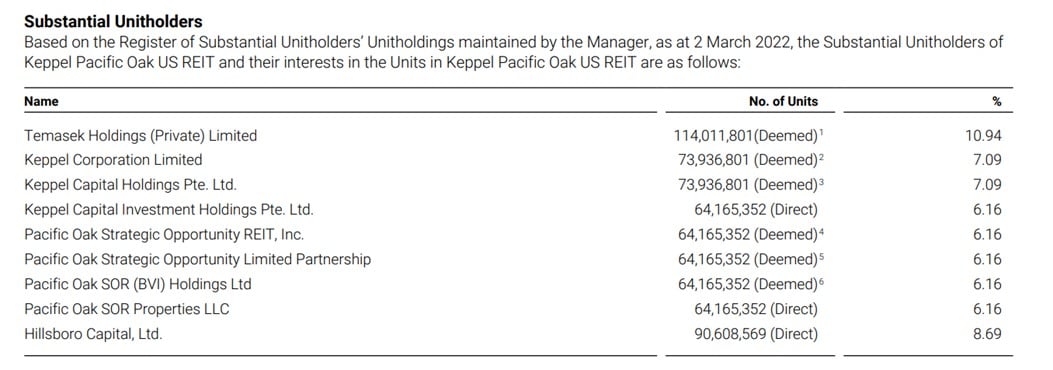

Unitholders of Keppel Pacific Oak US REIT

The 2 key Sponsors are Keppel and Pacific Oak (a US real estate company).

Because this is a US REIT, the tax code prevents any one company from holding more than 10% of the REIT.

So Keppel has about a 7% stake in the REIT, and Pacific Oak has about 6%.

I suppose this will lead to questions about the “alignment of interest” between the Sponsors and the REIT, given that they hold a relatively low stake.

What I would say though, is that I have been observing Keppel Pacific Oak US REIT since IPO, and the sponsors have not done anything really negative for the REIT.

Unlike other REITs where you know, the sponsors actively took steps that were “not so great” for the REIT.

In any case, I leave readers to decide whether this point is a concern for you.

Dilutive Rights Issue?

The other big risk of course, is a big dilutive rights issue.

You know, the kind where the REIT buys a big property and does a huge equity fundraising.

It’s not so bad if it’s a right issue available to all investors, because you can just pay up your proportionate stake and not get diluted.

But it’s absolutely terrible when the REIT does a private placement at a dilutive price, and you as a retail investor don’t get to participate (and get diluted).

That said, logic would dictate that when your REIT is trading at a 0.55x book value, you would never touch equity markets for funding because it would be too dilutive.

And with all debt refinanced out to Q4 2024, there’s no need to tap equity markets for refinancing.

But hey – you never know sometimes.

Can the price of Keppel Pacific Oak US REIT continue to drop?

Everytime I write an article like this, someone will ask if this is a falling knife.

Technicals of Keppel Pacific Oak US REIT

Well, the technical are not pretty.

The unit price is on a clear downtrend:

And the next level of support is at low 40s, and if that breaks the next one is low 30s.

Not pretty indeed.

Full Disclosure on my positions – Keppel Pacific Oak US REIT

Full disclosure that I do not hold any position in Keppel Pacific Oak US REIT today.

The last time I traded this REIT was in 2018, when I bought the REIT at the low 40s (after the market freaked out over the US tax treatment – if any old timers still remember that saga, the REIT was called Keppel KBS US REIT back then).

I flipped it shortly after the price recovered to the 60s, for a nice 50% profit.

And I’ve never bought back into the REIT again after.

Not even in March 2020 because there were just better opportunities out there.

Will I buy Keppel Pacific Oak US REIT at 13.7% dividend yield?

Let me put it out there that if you forced me to buy one of the US office S-REITs, Keppel Pacific Oak US REIT would probably be one of my top choices.

I like the investment strategy of focussing on the “Tier 2” cities and tech clients.

And there’s no denying that on a fundamental valuations basis, the REIT does look cheap.

13.7% dividend gives you a huge margin of safety.

Even if dividend is cut by 20%, you’re still sitting comfortably in double digit yields.

What worries me – and it worries me a lot, is the macro outlook.

If interest rates stay at 5% for an extended period like the Feds are calling for, I can’t imagine the pain it will wreak for US commercial real estate (and globally).

Will Rental Growth be sufficient to offset higher interest rates?

The question I get most often is whether rental growth can offset higher interest rates.

I think the problem here is that rental growth is more of a mid term thing, while higher interest rates are a short term thing.

In other words – higher interest rates kill you today, while rental growth only kicks in tomorrow.

And the problem if rental growth keeps up the interest rates increase – means that you have not really “solved” inflation.

What would that mean for the longer term outlook for interest rates?

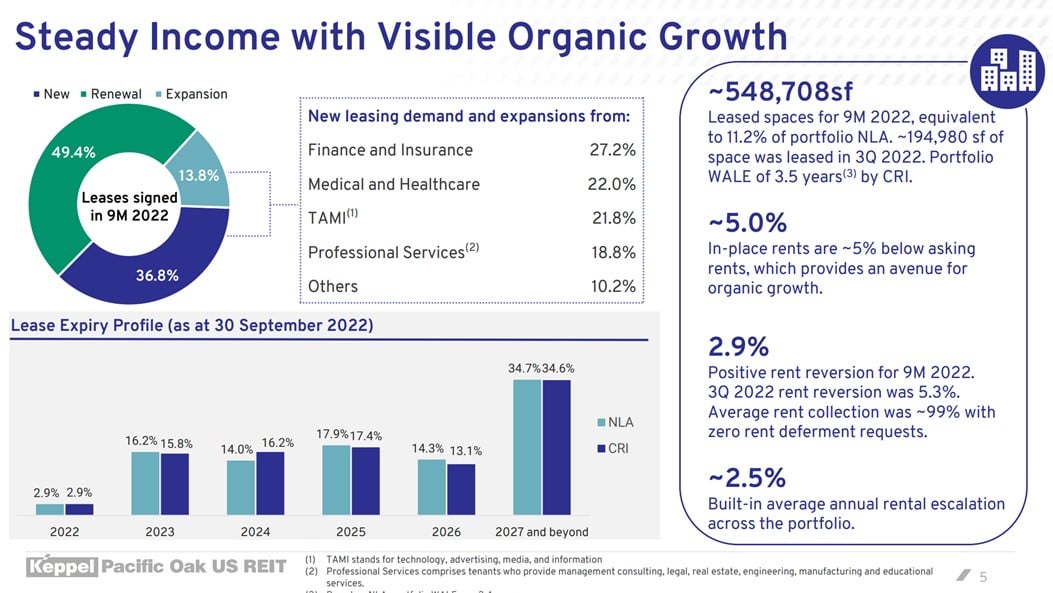

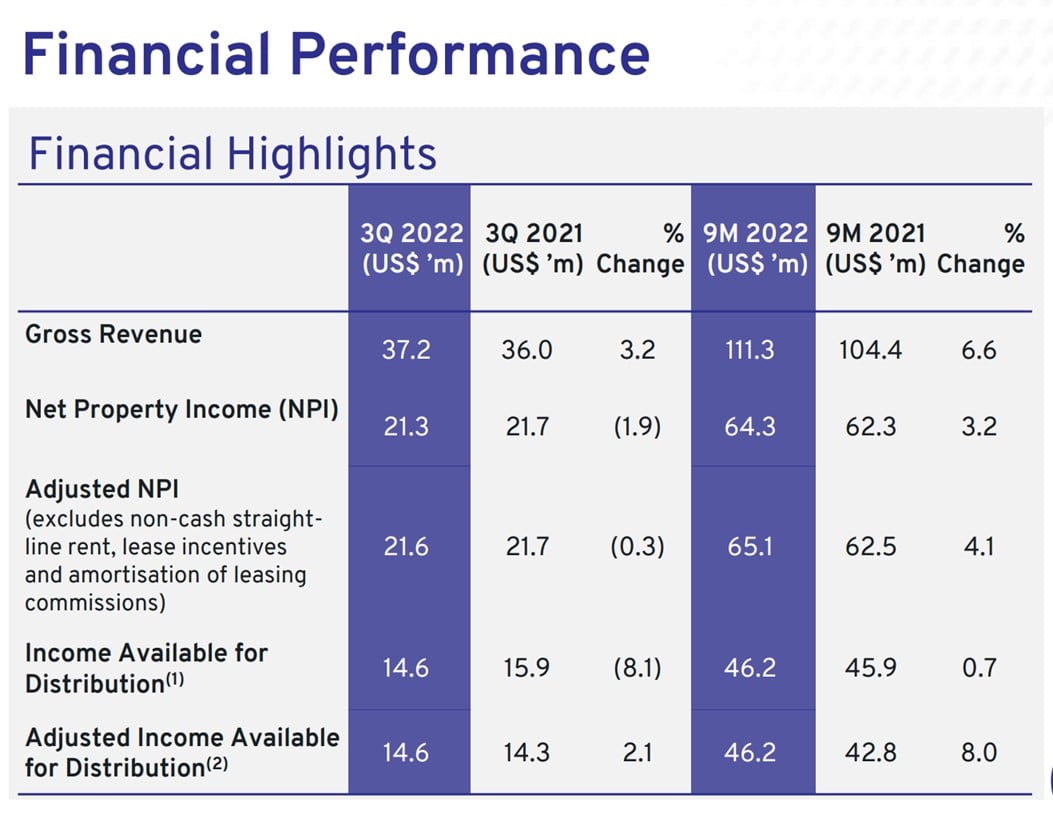

For now at least, the numbers are holding up.

You’re looking at 5.3% rental reversion for 3Q 2022.

And Net Property Income is only down slightly at 1.9%.

But frankly, it’s not the 2022 numbers what worry me.

It’s the 2023 numbers that I would be more concerned about, as the higher interest rates work their way into the economy.

Will I buy Keppel Pacific Oak US REIT at 13.7% dividend yield?

I know all the arguments why Keppel Pacific Oak US REIT is a great buy.

But I’ve been staying on the sidelines all year for REITs, waiting for the macro to improve and/or better prices to emerge.

I just don’t think we are there yet.

When I can get 4.28% risk free on a 6 month T-Bill, I see very little need to risk capital on REITs.

Not when we look to be going into a massive storm in 2023 for commercial real estate globally.

That being said though, I can see a scenario where I would start adding heavily to REITs, and possibly even Keppel Pacific Oak US REIT, in the next 6 – 12 months.

The key factors I look at to determine whether to buy – will be the global macro outlook, and pricing for the REIT.

Patreon members will get regular updates on my macro thinking as it plays out, including when and what I decide to buy.

My full REIT watchlist is also available there.

You can sign up here if you are keen.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

WeBull Account – Free USD150 ($212) cash voucher

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with a free USD 150 (S$212) cash voucher.

You just need to:

- Sign up here and fund S$2000

- Make 1 US Stock or ETF trade (you get USD100)

- Make 1 Options trade (you get USD50)

1080-1080-002-1024x1024.jpg)

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there

Hi FH, just for fun can you do a piece on comfortdelgro haha

Haha why Comfortdelgro? Not the biggest fan of this company… I traded this position post COVID, but fully exited the position already.

Dear FH

Thank you

However, let me be frank here and I hope you don’t mind!

Even before starting reading, I knew what your conclusion would be! So predictable!!

The fact is that higher rates are here and REITS will all suffer, to variable extents

The US REITS – all 4 of them including the non-office UH REIT have all suffered much more in account of not only direct full pass through of rate hikes with finances in USD but also the WFH and other idiosyncrasies of the “freedom loving but litigious” US environment

More importantly, the SG public have always shied away from “foreign” REITS on account of what could be construed as potential trust deficit as they “cannot see and feel” these assets

Consequently, even prior to the current rate hikes, these REITS traded at lower valuations

It is a no brainer that these REITS will continue to suffer

The enticing yields are juicy no doubt but risky

I hold all the 4 of these and am suffering alongside others – but I have desisted from adding more throughout this year

However, if these fall further by say another 10-15%, the risk reward equation gets skewed in favour of higher returns with time

The rest of the SG REITS are fairly valued or even arguably slightly overvalued now and I will add to these first at pullbacks before adding the likes of KP UHR Prime etc

More importantly, I am hoping that the SG banks will drop in early 2023. If that happens, they will be my top priority than any REITS

Once that is done, I will repair my balance sheet by averaging down on the US REITS

The USRE market as exemplified by the barometer XLRE as well as individual equities is in the doldrums but has always recovered historically, as rates start falling

This will hopefully be the case with all the REITS

Yours sincerely

Garudadri

Haha well, I’m not about to risk capital on a trade just because that would be unpredictable to readers! 😉

Agree with most of the views that you raised. The US REITs are all trading at very “cheap” valuations and high yields, but until the macro calms down, I find it hard to see myself taking a position.

With these small cap REITs, it’s very hard to tell what could go wrong when we head into 2023.