So the latest Singapore Savings Bonds are out.

And interest rates are definitely on an uptrend.

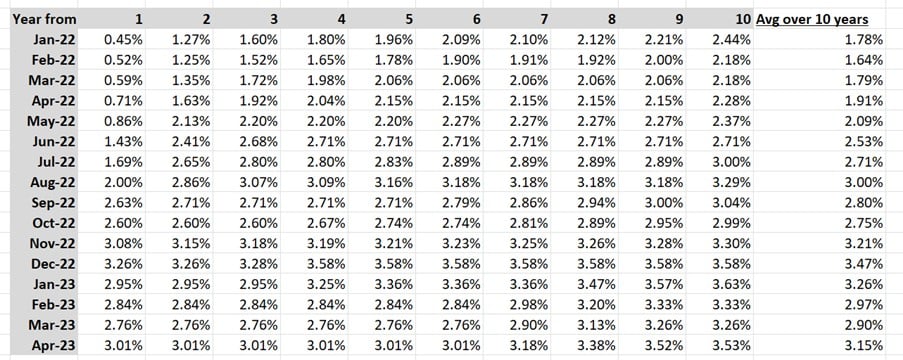

You’re looking at 3.01% for the first year (vs 2.76% for the previous month).

And 3.15% over 10 years (vs 2.90% the previous month).

There are 3 big questions I wanted to discuss for Singapore Savings Bonds:

- Will Singapore Savings Bonds interest rates keep going up?

- Should you buy Singapore Savings Bonds now or wait for interest rates to go higher?

- Are Singapore Savings Bonds a good buy vs T-Bills or Fixed Deposit?

Singapore Savings Bonds interest rates have gone on a roller coaster ride the past 12 months

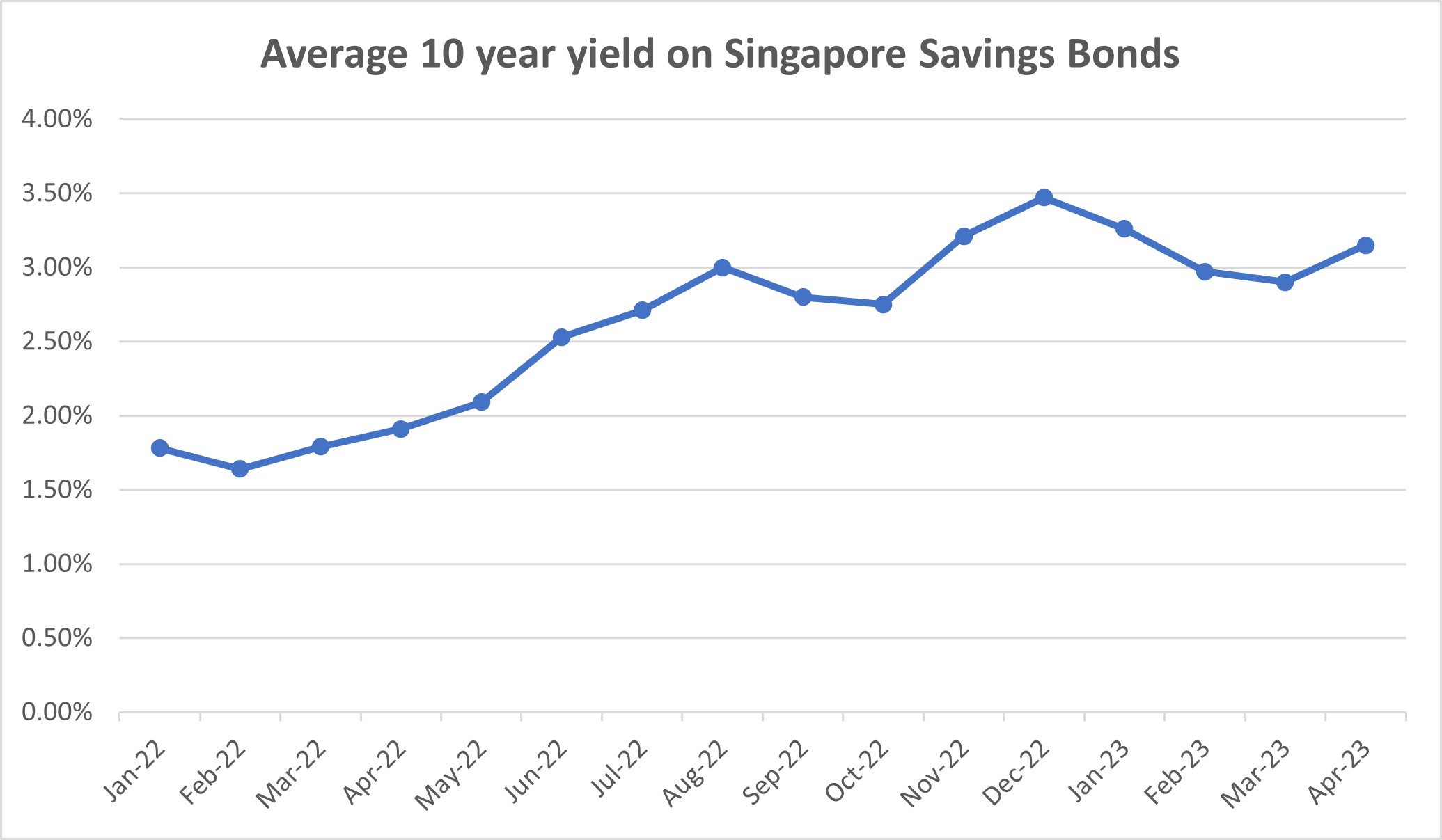

Just to put things in perspective.

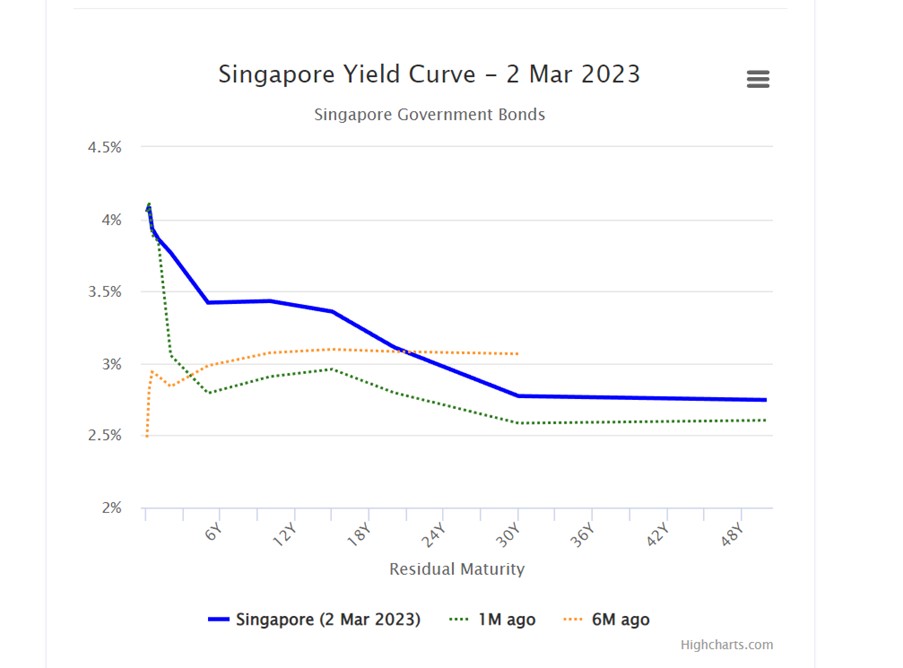

Here’s how the 10 year yield on the Singapore Savings Bonds has evolved since Jan 2022.

It went up most of 2022, before peaking in December 2022.

And as of April 2023, interest rates are going up again.

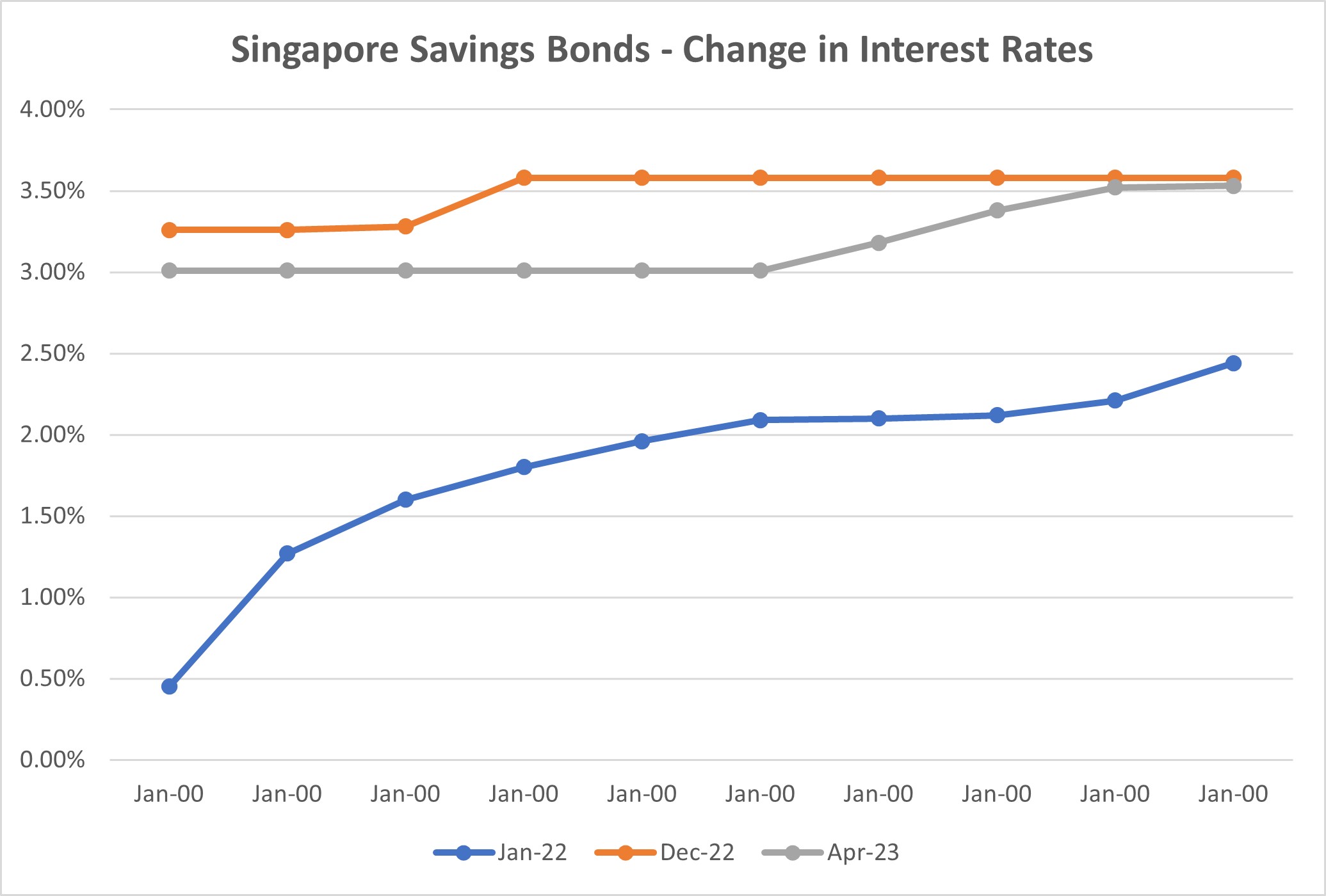

The difference is especially stark when you look at the full interest rate curve.

From Jan 22’s low (blue), to Dec 22’s high (orange).

To the latest April 2023’s Singapore Savings Bonds (grey).

It’s pretty astounding to see how much interest rates have moved over the past 12 months or so.

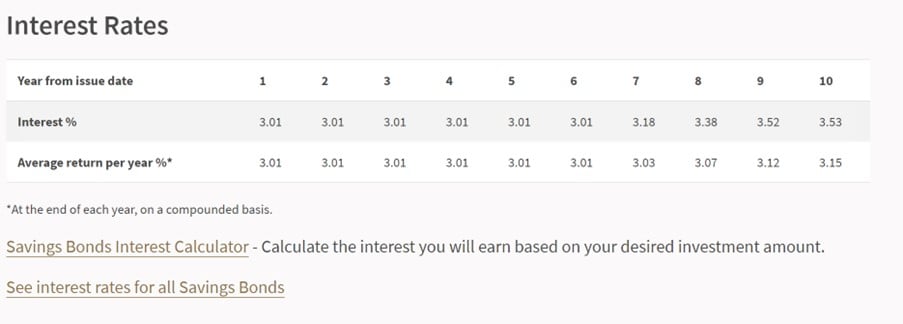

Full table below for those who are interested:

Will Singapore Savings Bonds interest rates keep going up?

Okay the million dollar question – will Singapore Savings Bonds interest rates keep going up?

My simple view – yes.

In fact, I think it may eventually even surpass the 3.47% high reached in December 2022.

The US economy is proving to be very resilient despite higher interest rates.

Which means the Federal Reserve needs to hike interest rates even higher for even longer to combat inflation.

Which means the 10 Year interest rates need to go up even further before this cycle is over.

Ie. Singapore Savings Bonds interest rates will go higher before the end of this cycle.

The slightly longer version…

The slightly longer version of the answer.

Is that the interest rates on Singapore Savings Bonds are smoothed out such that they will step up every year.

This is a problem when you have an inverted yield curve like right now – where the 6 month interest rates are much higher than the 10 year interest rates.

Because of the smoothing out of the yields, you end up with a situation where the first 6 years of the Singapore Savings Bonds interest rates are flat.

Now why does this matter?

This matters because it means that the biggest determinant of Singapore Savings Bonds interest rates going forward is not the short end of the curve.

Rather, it is the long end of curve.

The short end of the curve, things like T-Bills or Fixed Deposits with 12 months duration or less, is primarily determined by the US Federal Reserve interest rate hikes.

Whereas the long end of the curve (10 Year), is primarily determined by market expectations as to future growth and inflation.

This makes it a lot harder to predict.

And much more volatile.

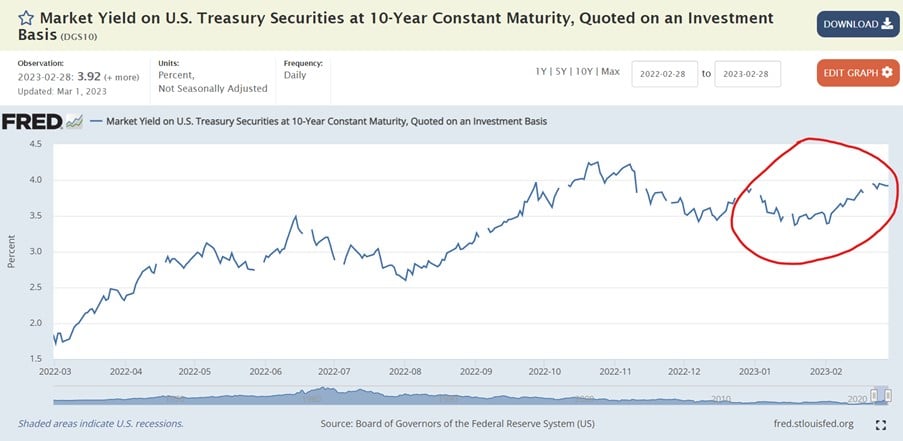

A few months ago, the market was expecting inflation to drop back down to 2% in 2023, allowing the Feds to slash interest rates in the second half of 2023 – resulting in low long term interest rates.

Now, the market is starting to wake up to the reality that inflation is not going to come down so easily in 2023.

Which means no interest rates cut in 2023, but possibly even more interest rate hikes.

Hence the long end is going back up:

Will this keep going?

Yes I believe so, when you look at how strong the US labour market and consumer spending is.

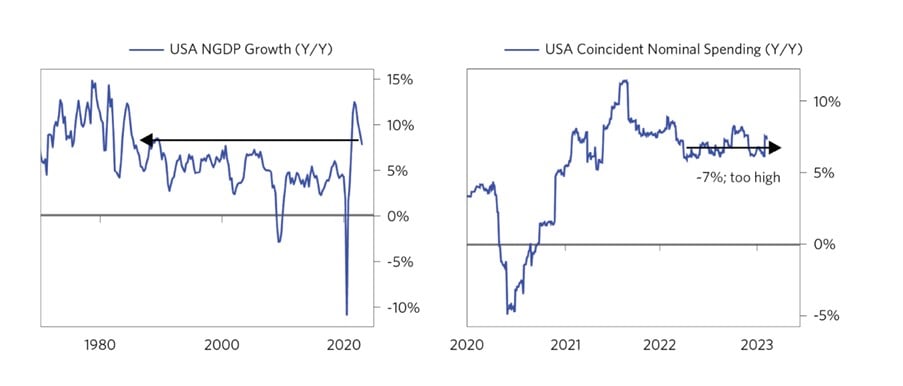

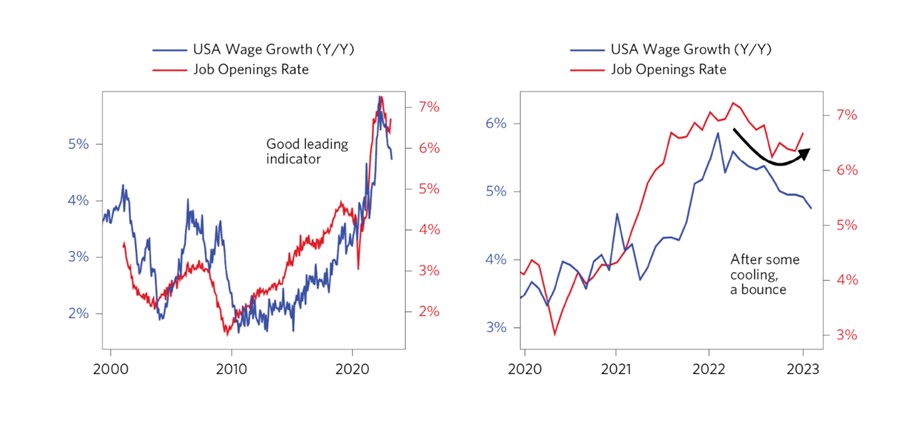

Here’s some great charts from Bridgewater.

It shows US consumer spending stabilising at a way too high 7% increase year on year.

While the US labour market is still waaay too tight.

You’re looking at 5% wage growth and job openings rebounding (instead of going down).

Long story short – as shared in my January macro piece.

The high frequency data is actually showing a pick up in economic growth.

Which will inevitably lead to a pick up in inflation.

To expect interest rate cuts in the face of that seems almost laughable.

The long end will go higher before this is over.

Will interest rates on Singapore Savings Bonds cross 3.5%?

I suppose the logical next question is how high will interest rates go.

The previous high on the Singapore Savings Bonds was 3.47% over 10 years (Dec 2022).

Will we surpass that this cycle?

This is not an easy question.

Because as shared above, interest rate hikes only affect the short term interest rates (think T-Bills or Fixed Deposit).

The long term interest rates are determined by the market.

Make an educated guess FH

Gun to my head though?

The previous high on the US 10 Year Treasury was 4.25% in October 2022.

But the Feds will need to hike even higher (possibly 6%) because of reaccelerating economic growth.

So conservatively, I think you may see the US 10 Year go back up as high as 4.25% – 4.5%.

Which could imply a peak SG 10 Year of 3.5% – 3.75%.

Do note that Singapore Savings Bonds track the average interest rates of the previous month though.

So to see a Singapore Savings Bonds interest rate of 3.75% you need the SG 10 Y average 3.75% for the previous month, which we may or may not see.

So… do take these numbers with a pinch of salt.

Interest rates will likely go higher, but exactly how high they go, and when they hit those highs, is a much tougher call.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Should you buy Singapore Savings Bonds now or wait for interest rates to go higher?

So… should you buy Singapore Savings Bonds now, or wait for interest rates to go even higher?

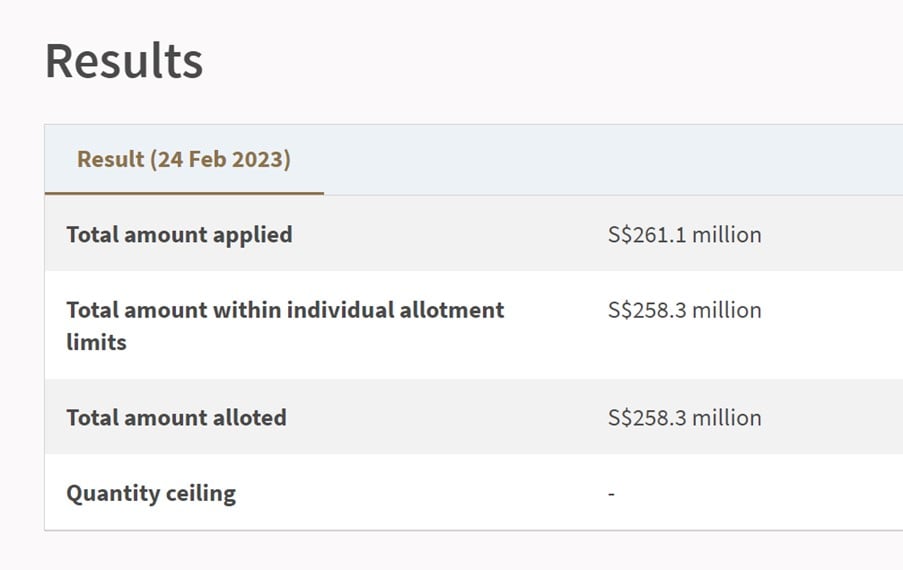

The recent March Singapore Savings Bonds were ridiculously undersubscribed – $261 million applications for $600 million on offer.

That means full allocations for everyone.

The interest rates did pick up quite a bit this month though, so I think you’ll see better demand.

But I still think you have a good chance of getting close to full allotments.

Whereas if you wait till Singapore Savings Bonds go back to their highs, you may not be able to get full allotments then.

So… buy Singapore Savings Bonds now or wait for interest rates to go higher?

I think ultimately, it depends on the Singapore Savings Bonds you’re already holding.

If you’re holding those from years ago that are paying 2% interest rates, it’s a complete no brainer to redeem and buy the latest Singapore Savings Bonds.

If you’re holding those from a few months ago that are paying just 0.1 – 0.2% below the latest Singapore Savings Bonds.

You might be better off just waiting.

Will I buy these Singapore Savings Bonds or wait?

For me personally, I’ll probably wait.

Most of my Singapore Savings Bonds are yielding about 3% in their first year.

Not really worth the effort to redeem just for a few bps difference.

I do think interest rates will go even higher in 2023 too, so I’ll just wait until much more juicy yields before swapping out my old Singapore Savings Bonds.

Are Singapore Savings Bonds a good buy vs T-Bills or Fixed Deposit?

The final question is whether to buy Singapore Savings Bonds or Fixed Deposit.

I don’t think the answer has changed very much from a few months ago.

Namely:

Buy T-Bills / Fixed Deposit if you want high short term interest rates, with a bias towards Fixed Deposit if you want the option of getting your money back early (by forfeiting your accrued interest).

Buy Singapore Savings Bonds if you want to lock in money for potentially long term, with the option to get your money back any time with accrued interest.

And really, I think that’s your answer.

What am I doing personally with my cash – Singapore Savings Bonds vs Fixed Deposit vs T-Bills?

Personally I’ve maxxed out my Singapore Savings Bonds allotment.

I use it primarily to park excess liquidity or emergency funds.

And the rest goes into a mix of T-Bills or Fixed Deposit for higher interest rates.

I also put some liquidity into high yield savings accounts like UOB One (close to 5% on $100,000, pretty worth it if you fulfil the conditions).

So I do think there is a place for Singapore Savings Bonds, Fixed Deposit, and T-Bills in every Singapore investor’s portfolio.

Ultimately though, each investor needs to find the right mix between yield and liquidity that suits them.

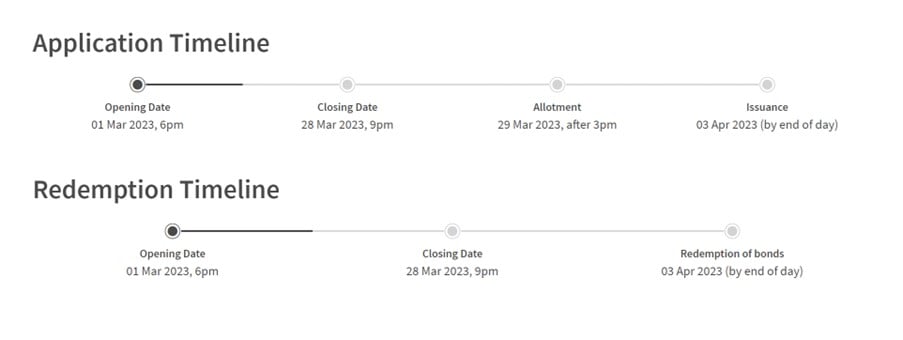

Application / Redemption Timeline for Singapore Savings Bonds

In any case, if you’re interested, do get your applications for Singapore Savings Bonds in by 9pm on 28 March 2023.

Same timing for redemption of older Singapore Savings Bonds!

As always, this article is written on 3 March 2023 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon, together with weekly premium macro updates. You can access my full personal portfolio to check out how I am positioned as well.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

WeBull Account – Get up to USD 500 worth of fractional shares

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares.

You just need to:

- Sign up here and fund any amount

- Maintain for 30 days

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!