I’ve been seeing a lot of interest around leveraged ETFs recently, especially the 2x and 3x short ETFs.

And I get it.

The market is crashing every day, so if you buy a 3x short ETF on the Nasdaq QQQ, you stand to reap big returns right?

What’s more, with a 3x leveraged ETF the fund manager does all the work for you, and you can never lose more than what you put in. What’s not to like?

As you would expect – things are never that convenient in real life.

So if you only take away one thing from this article, let it be this:

Leveraged ETFs are designed to track the daily performance of their index. They are short term, trading instruments.

If you hold them for the long term, you are literally bleeding returns.

An example – the UltraPro QQQ 3x NADSAQ ETF (TQQQ)

Let’s take the TQQQ for example.

The mandate states that:

This is important – ETF is designed to track the daily performance of the index.

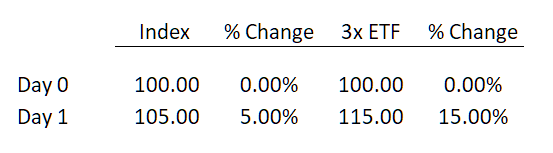

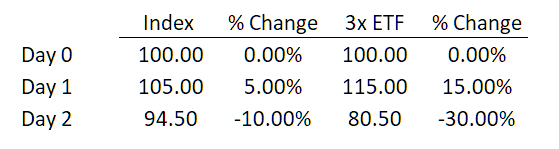

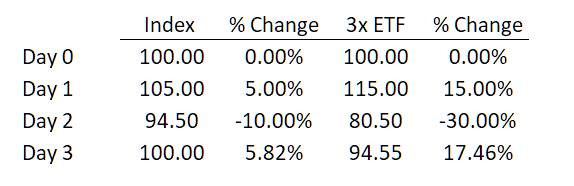

Let’s run an example.

Day 1 – Index gains 5%

Day 2 – Index loses 10%

Day 3 – Index recovers 5.82%

Basically, over this sequence of events, the underlying Nasdaq 100 ETF closes completely unchanged.

And yet the TQQQ (3x QQQ), is down 5.45% from its starting point.

The reason why of course, it because the TQQQ is not designed to track the leveraged returns of the QQQ over a 3 day period.

It is designed to track the leveraged returns of the QQQ over a daily period.

Why does this happen?

To be a bit more technical, the reason why you cannot build an ETF that tracks the leveraged returns of an index over any period longer than 1 day is because of margin requirements.

If you short the index yourself, and the index goes up, you need to put up more margin (or get margin called).

If you are an ETF, there is no way for the ETF to go to the ETF holders to ask for more margin.

Which means the options for the fund manager are:

- ETF needs to hold cash

- ETF needs to close off all its positions on a daily basis

1 is too complicated to pull off.

How much cash do you hold each day, do you hold more cash in periods of high volatility, what if you run out of cash etc.

Going down Option 1 basically makes you an active fund manager, and the fees are very different for that.

Which is why all the leveraged ETFs go with option 2.

They only track the leveraged daily returns of the index.

And at the end of each day, they will close off their positions, and ensure that whatever happens the next day, the ETF will be able to track the 3x returns of the index.

Side effect – this is why the end of day liquidity is so high, and why volatility drives volatility

This kind of mechanical buying/selling creates 2 big side effects:

- High end of day liquidity

- Volatility driving volatility

High end of day liquidity

As you may have noticed, the end of day liquidity in the US market is always the highest.

In the last hour to last 5 minutes of every trading day, you’ll find that trading liquidity is very high.

The reason why is somewhat tied to how the mechanical buying of all these ETFs work.

At the end of the trading day, many of these ETFs are forced to buy/sell positions mechanically based on how the market performed on that day.

They buy/sell based on their mandate, to prepare for the next trading day.

Everybody in the market knows that, so the savvy traders will usually save most of their biggest trades for the end of the day, when the big ETF mechanical buying/selling triggers.

Hence end of day liquidity is so high.

FYI, you can trade ETFs via Saxo TraderGo.

Volatility driving volatility

Especially for leveraged ETFs, the more the market moves, the more they have to buy/sell at the end of the day.

If the NASDAQ moves 1%, the TQQQ needs to buy/sell enough positions to offset a 3% move.

If the NASDAQ moves 3%, the TQQQ needs to buy/sell enough positions to offset a 9% move.

Basically, the more the index moves, the more the leveraged ETFs need to buy/sell at the end of the day.

Which means that sometimes, when liquidity in the market is very tight, you have these leveraged ETFs coming in at the last 5 minutes of trading and dumping/buying big positions to further drive the volatility.

Long story short – Don’t hold a leveraged ETF long term

As would be obvious by now, leveraged ETFs are not designed to be long term holdings.

If you want to do a 3x short on the NASDAQ (or long), your options are:

- Short the index directly (but you must manage risk and margin to avoid margin calls, as bear market rallies are very real and very vicious)

- Short via options strategies

Leveraged ETFs may seem like a convenient third solution, but frankly, if you use them you really are bleeding returns because of the scenario described above.

If you don’t know how to do them or are not confident you can pull them off, but really want to learn how to do it, my suggestion is to start small.

Play around with small amounts (say a couple hundred dollars) such that the amount you lose either way is little. Or open a trading demo account and experiment with trades there, with no risk to your own money.

It’s easy to describe this in theory, but much harder to actually do it.

Even if you are a long only investor, the above could be helpful for those who want to do leveraged long plays, or to capitalise on how these ETFs work. In fact there are even hedge funds out there who make money by systematically shorting a 3x leveraged ETF and longing a 3x short leveraged ETF, on the idea that over time they will make money from the decay mechanic described above.

But that’s probably going beyond the scope of this article.

As always – love to hear what you think!

A note from our partner: Trading with Saxo Markets: The Long and Short of It

A quick note from our partner, Saxo markets:

What is shorting?

You need two types of trades – long and short – to take advantage of market ups & downs. Shorting allows you to take advantage of both rising and falling prices.

Trading short

Just how do you short-sell? Instead of buying a stock to profit when its price goes up, you sell a position on a stock to profit when its price falls. When you’re ready to close your short position, you simply buy the position back, closing the position and realising the price difference.

Using stop-loss orders to limit losses is an important risk-management tool.

CFD Trading

CFDs (Contracts for Difference) are traded on margin, allowing you to short a wide range of products, from stocks and indices to forex pairs and commodities like gold and oil.

Whichever tools you choose, Saxo Markets offers you a range of options so that you’ll be ready to make your move whichever way the market moves.

Saxo Account Opening Bonus for FH Readers

Saxo account opening bonus for FH readers

Drop an email to [email protected] for the full steps: Financial Horse x Saxo Affiliate Link

Note: This post is in collaboration with Saxo Markets. All views and opinions expressed in this post are from Financial Horse.

And yet SQQQ is up 98.8% YTD?

The decay is well-known, here’s an alternative viewpoint with more nuance.

https://www.afrugaldoctor.com/home/leveraged-etfs-and-volatility-decay-part-2

Understand where you’re coming from, and that’s a very interesting article.

If you’re comfortable with the exposure and know what you’re getting into – by all means go ahead!

Cheers

Hi there, thanks for sharing this timely useful article. Didnt know about the bleeding until your article. May I ask how about SARK? Does it work the same way?

SARK is a 1x inverse ETF. The problem described in this article mainly applies to leveraged ETFs – for example 2x or 3x ETFs. 🙂

How about Gold ETF like JDST traded on NYSE ? Been holding 1000 shares split up to 40 shares since a few years . Does rising and falling gold prices now affect trend of JDST ( once soared to USD 100,000)? I tend to cling to belief GOLD is different from Stock movements ? Your view please, thanks !

Yes – all the 2x or 3x ETFs are subject to the same underlying problem.

Leveraged ETF achieve their leverages via futures contract with investment banks and not via mechanical buy sell of actual physical stocks at end of day.

Leveraged ETF like TQQQ achieve their leverages via futures contract with investment banks and not via mechanical buy sell of actual physical stocks at end of day.

That’s a good point. Although I suppose the market maker who takes on the risk needs to hedge it with the physical – so at the end of the day someone in the market needs to hedge their risk.