I received this question recently:

Hi FH,

To give context, I’m quite young and only just recently got access to brokerage services.

I invested into crypto at the peak and used leverage so suffice to say I’ve paid quite a bit in “tuition fees”.

Recently, I’ve been quite interested in US equities domiciled in Singapore such as KORE and Digital Core REIT given their attractive yield spreads.

However, I’m concerned about the recent rate hikes, recession and possibility of high FX risk given the fact that USD/SGD is so high right now.

Do you think such REITs would be good to scoop up around 2023 Q1 -Q2 when things settle down?

Or do you think the macro condition will further deteriorate longer?

Thank you so much for your blogs, look forward to reading them everyday!

What to do as a Singapore REIT investor in 2022 / 2023 – Buy, Sell or hold?

A lot of you have reached out with questions on REITs recently.

Investors who bought REITs in 2021 are deciding whether to sell, hold or buy more.

Investors who didn’t buy previously are excited about the sell-off, and trying to decide when to buy.

I cannot answer every question that comes in, and what you do with your own money is ultimately your own decision.

But I figured I would share my own framework to approaching this, and hopefully it helps.

I will split this into 3 parts:

- Where will REIT prices go in 2022 / 2023?

- Is XXX REIT worth buying, at what price?

- How do I know when to buy, sell or hold?

And please – this is not financial advice. If you don’t know what you should be doing with your own money, call your financial advisor.

Question 1 – Where will REIT prices go in 2022 / 2023?

Let’s say you have an asset class that is very vulnerable to interest rates.

Let’s say you take up 35% leverage to buy that asset.

Now imagine that interest rates go up 400% in 12 months, and stays there.

What happens to your investment?

That’s REITs for you.

This is a leveraged play on real estate, which classically is one of the most interest rate sensitive asset classes.

Investors thinking that REITs will be immune to rising interest rates need to relook their assumptions.

When will I start buying REITs in 2022 / 2023?

Because of this, I’ve been saying for a while that I will only buy REITs if (1) valuations are cheap on a fundamental basis, or (2) macro has bottomed.

Let’s discuss each of them.

REIT Valuations – Ascendas as a case study

Let’s use Ascendas REIT as an example.

I picked Ascendas REIT because unlike CICT or MPACT, there hasn’t been any big merger in the past 10 years that would skew the historical valuations.

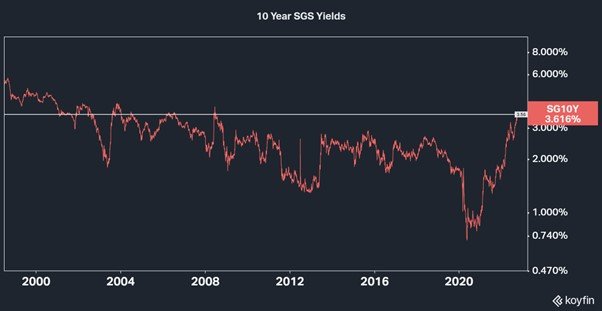

10 year historical valuations for Ascendas REIT

The 10 year average for Ascendas REIT’s dividend yield is 5.63%.

The 10 year average for the 10 year Singapore Government Security (SGS) is 2.03%.

This means that the 10 year yield spread (dividend yield – risk free rate) for Ascendas REIT is 3.6%.

With the 10 year SGS at 3.5% today, that implies a fair value dividend yield of 7.1% for Ascendas REIT.

Ascendas REIT today trades at a 6.0% yield.

Which means even after the drop, Ascendas REIT still looks expensive, compared to historical yield spreads.

How high will Singapore interest rates go this cycle?

And don’t forget, this rate hike cycle is not even over.

Futures markets are pricing in a peak Fed Funds rate of 4.75% – 5.25%.

Working backwards, I think a peak 10 year SGS yield of 4.0% – 4.75% may be reasonable.

Using historical valuations of 3.6% yield spread, that’s implies fair value for Ascendas REIT is about 7.6% – 8.35% dividend yields.

That means a unit price of about $1.85 – $2.03.

A-REIT trades at $2.60 today (6.0% dividend yield), which means if you use historical yield spread – there could still be 20-30% drop from here.

Valuations are NOT a timing tool

That said, my numbers above are a very crude analysis.

All valuations do is tell you whether a REIT is cheap / expensive relative to historical prices.

Valuations are NOT useful as a timing tool.

A cheap REIT can get cheaper, an expensive REIT can get more expensive.

But the point is mainly to illustrate that on a fundamental valuations basis, it is hard to say that REITs are dirt cheap right now.

You really need to factor in the rapid rise in risk free rate here.

The 10 year SGS yield is going back to 2005 levels – and we’re not even at cycle peak.

Be careful of linear thinking…

I also wanted to caution against linear thinking.

I see many investors talking about dividend yield and Price/Book in abstract, without appreciation of how everything comes together.

You need to understand that the economy doesn’t work in a vacuum.

If risk free T-Bills are yielding 3.77%, how will that impact:

- Rental price growth

- Real estate valuations

- Interest Expense Costs

For (1) and (2), if interest rates stay high, what is the knock on effect on economic growth, and real estate cap rates?

For (3), I ran the numbers for Patreons this week, a mere increase in cost of debt for Ascendas REIT from 2.1% to 4.2% can drop dividend yields by 20% (once hedging falls away).

Which means what you thought was a 7% yielding REIT, is now a 5.6% yielding REIT. Just from higher interest expense.

Long story short – I will buy REITs if I think they are cheap on a fundamental valuations basis, but I do not think they are cheap at these prices.

If this is cycle bottom, I am happy to pass.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Has the Macro bottomed? Or will it get worse?

The other scenario in which I will buy REITs – If the macro has bottomed.

And on the macro… man… where to begin.

Every week on Financial Horse I write that the macro is a disaster, and a Fed Pivot is still a 2023 story.

And every week I get questions on whether the macro has bottomed, and whether it is time to buy.

To sum it up:

- Leading inflation indicators are starting to roll over, but US labour market is still very tight – driving wage growth and services inflation

- This means the chance of a Fed pivot in 2022 are still very low

- Any Fed pivot is probably more of a 2023 story, and the exact timing will depend on (a) when markets break, or (b) when inflation starts to roll over

If you want to frontrun the Feds, be my guest.

Just like March 2020, I’m not buying until the Feds start to waver.

This leverage unwind could be epic, and I’m prioritising capital preservation over capital growth here.

Question 2 – Is XXX REIT worth buying, at what price?

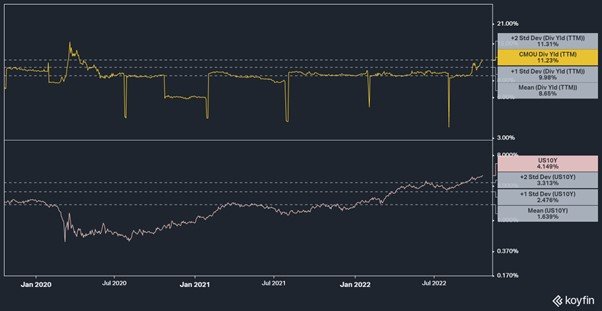

The reader mentioned Keppel Pacific Oak US REIT (KORE), so I figured let’s pull up the charts for this REIT.

Historical yield spread for Keppel Pacific Oak US REIT is 6.8%.

Assuming a peak US 10 year of 4.5%, you’re looking at a fair value of 11.3% for Keppel Pacific Oak US REIT.

Keppel Pacific Oak US REIT trades at 10.90% yield, which makes it look about fairly valued.

But this is where I caution against linear thinking.

Keppel Pacific Oak US REIT is a $500m market cap REIT.

This makes it miniscule, in the US REIT market (big US REITs regularly go for $20-$30 billion market cap)

You tell me that US 10 Treasuries move from 0.5% to 4%+, and you’re happy to buy a small cap US REIT at a 2% higher dividend yield than average?

Individual REIT level risks

That’s even before we delve into the individual REIT level risks.

You can check out my Prime REIT article for the kind of concerns you need to think about when buying US REITs.

And look at the chart of KORE below.

Do you think (a) March 2020, or (b) the 2022/2023 rising interest rate scenario, will prove more deadly for Keppel Pacific Oak US REIT?

Each REIT needs to be valued on its own merit

So I leave it to you to evaluate the merits of each individual REIT.

What I will say though, is that I think by and large S-REITs as an asset class have not sufficiently priced in the rise in risk free rate, and the potential second order effects to come.

And don’t forget there is a chance we see a liquidity crisis before all this is over.

You already see the signs of stress building up in the system, with things like the UK Gilts market.

I just spent the past week painstakingly updating price targets for every single REIT on my watchlist to reflect the higher risk free rates.

And I also added a whole bunch of new REITs to the watchlist due to rapidly declining prices opening up interesting new opportunities.

If you’re interested, do considering throwing this horse a bone and subscribing for Patreon.

It’s literally just S$25 a month for the watchlist, you spend more on brokerage fees alone.

Question 3 – How do I know when to buy, sell or hold?

When you buy any financial asset, you need to decide if you are an investor, or a trader.

A Trader buys to sell at a higher price.

An investor buys to own.

You MUST, MUST, MUST know which you are.

Bad things happen when you confuse the two, and traders becomes investors.

Everyone thinks they are Warren Buffet and a “Buy and Hold long term investor”.

Until prices start to drop…

Trader – Focus on Risk Management

If you are a trader, you must have a stop loss / exit plan in place.

If you’ve blown pass your stop losses, sell the position, no questions asked.

If you’re down as a trader and you don’t have a plan, or when in doubt, just exit the position.

Hope is not a strategy.

Risk management is the key to becoming a good trader.

Investor – Think like an owner

If you are an investor, then you need to think like an owner.

Think as if you bought a condo.

Imagine you spent 12 months visiting every condo in the neighbourhood, walking around the area.

You buy the condo because you believe in the rejuvenation plan that will play out over the next 10 years.

Now imagine the day after you close, a buyer comes to you and offers to buy the property 30% below what you paid.

Do you sell?

If you are an investor, you should be thinking like an owner of the real estate.

If there is a good reason to sell – for eg. The property is defective and fair value is down 50%, okay.

Or maybe interest expenses have gone up due to rising rates, and your initial return calculations are now wrong.

Then of course selling makes sense, and it’s not true that an investor will never sell a REIT.

All I’m saying is that as an investor, look beyond the price – think long term.

Think value.

Closing Thoughts: Answering the Reader’s question

Coming back to the reader’s question:

Do you think such REITs (US REITs) would be good to scoop up around 2023 Q1 -Q2 when things settle down?

Or do you think the macro condition will further detoriate longer?

As shared above, I think a Fed pivot is unlikely in 2022, its more of a 2023 story.

And right now, I dont see value in the S-REITs as an asset class just yet, because of the higher risk free rate and potential second order effects. I do expect value to emerge before all this is over, but I don’t think we are there yet.

And frankly, I don’t see a need to speculate on the exact timing.

Just watch the macro play out, and buy when things get really bad and the macro starts to bottom.

Whether that is early 2023 or late 2023, I frankly don’t know at this point.

I just spent the past week painstakingly updating price targets for every single REIT on my watchlist to reflect the higher risk free rates.

And I also added a whole bunch of new REITs to the watchlist due to rapidly declining prices opening up interesting new opportunities.

If you’re interested, do considering throwing this horse a bone and subscribing for Patreon.

It’s literally just S$25 a month for the watchlist, you spend more on brokerage fees alone.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- Whole bunch of freebies – A free packet of rice (1kg), a free Kopitiam Kaya Toast set, a $1.99 Double Mushroom Swiss at Burger King, and 50% off KFC Zinger Set just to name a few.

- 1.0% base interest on your first $50,000 (up to 1.4%)

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

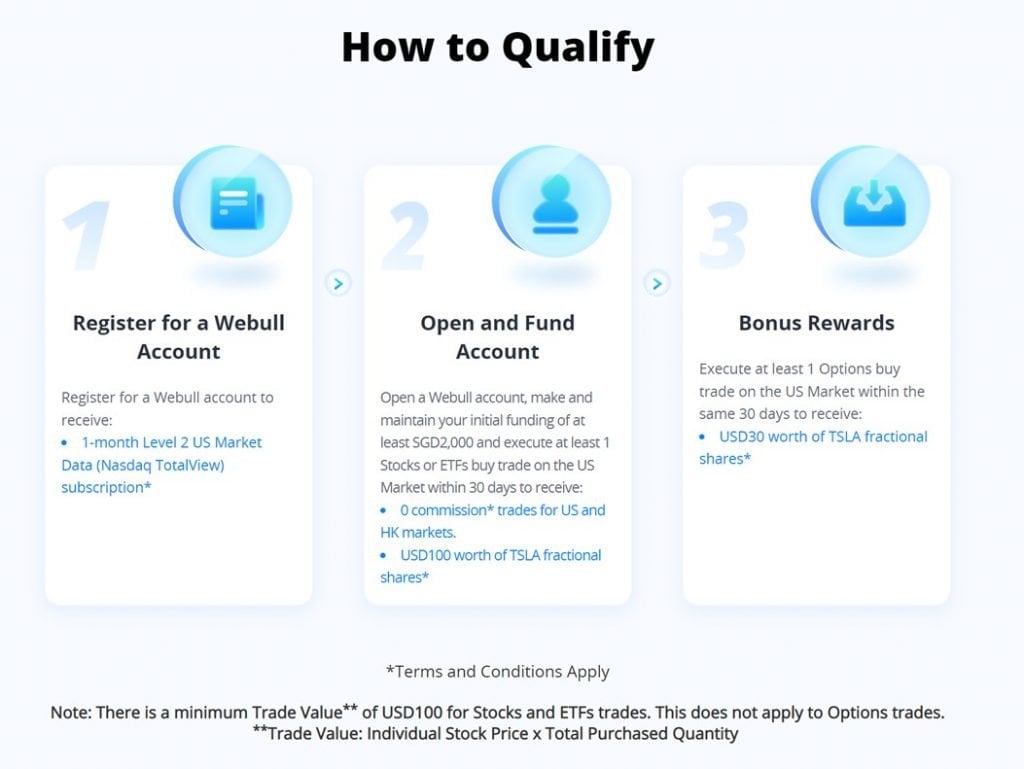

WeBull Account – Free US Stock, Options and ETF trading (Free USD130 (S$185) in Tesla shares)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

To get the USD130 (S$185) in Tesla shares, you just need to:

- Sign up here and fund S$2000

- Make 1 US Stock or ETF trade (you get USD100 in Tesla Shares)

- Make 1 Options trade (you get USD30 in Tesla Shares)

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 100 USD in Apple Shares with Webull, a zero commission broker.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

FH! I feel your “frustration” haha. Just wanna share an interesting conversation recorded by Bloomberg with Nouriel Roubini, prolly a good one for people to listen, to at least to understand the whole complexity on macro factors: No one can predict how it will play out.

https://www.bloomberg.com/news/articles/2022-10-20/nouriel-roubini-foresees-an-ugly-mix-of-the-1970s-and-the-global-financial-crisis

Haha thanks – will check it out! 😉

Great article as usual FH. I wonder if the historical valuations of 3.6% average yield spread was derived largely during a time of rock bottom interest rates, and is therefore a bit exaggerated. When rates are rock bottom, they have nowhere to go but up, and investors therefore need to price in some risk of them going up – hence the 3.6% yield spread. However, when interest rates are relatively high, I wonder if that yield spread we should factor in should be lower because investors also have to price in the possibility that inflation may be peaking and rates may eventually hold steady or go lower. It’s no longer a case of rates have ‘nowhere to go but up’ but instead – ‘it could go either way’.

Good point, I understand where you’re coming from.

Not sure if I agree though.

The risk free rate determines the cost of money. When it goes up, all global financial assets need to reprice – which we are seeing right now.

I would add though, that interest rates are just 1 variable to consider. You also need to look at inflation and economic growth. Which is why I said my numbers in this article are a very crude analysis, I did not adjust for inflation/growth here.

For eg. the past 10 years was a period of low growth low inflation. That might look very different this decade.

FH, don’t you think as per your analysis, you are not considering DPU growth to increase yield but only by stock price. Rental growth in residential market is going on roof, will that not be the case for commercial while rate are increasingly. Do you have any data point for 2008 crash for REIT, which was too much and since then our financial system has become quite mature still be are already at this stage. The point i am trying to make here that while i don’t think REIT price will recover soon but downside also look limited. Your view pls.

Simple view is that rental growth will not move up quick enough in the short term to offset the rise in interest rates (which is very aggressive).

The SG residential market has unique supply-demand characteristics, the same cannot be said for commercial real estate.

Rental growth will matter in the mid term, but the overriding consideration in the short term is interest rates.

Thank you FH, somehow i feel this is the dip of century and it will be missed if we keep on reducing our target price once things are on way down just like any typical bear market. I think other than price correction there is enough timewise correction that has happened to REITs. Anyway respect your views and above comments are more technical in nature rather your fundamental analysis.

Fair enough, get your point.

I could be wrong as well, who knows.

I leave it up to each investor to decide what to with their own money. 😉

FH,

Interest rate party is not over yet, Core CPI is still raising MoM. Unemployment numbers drop in sept. I guess market liquidity is the weakest link now. FEB need to have a reason to pivot, 2022 is out of the question. If there is no black swan event. Going to sit back relax n watch the firework now. Short Relive rally could happen after the mid term election in Nov. i have booked my ticket and off to my holidays. 😉 all the best.

-Above message is only for entertainment purposes only, NOT financial advice, DO NOT follow.

Fastpace

The next 12 months should be interesting, to say the least!

Dear FH,

I currently hold ascendas reit and Capitaland int com Trust(CICT). I have suffered capital losses as I bought them before the Feds started hiking aggressively. Should I sell them now and buy them again when the Feds pivot?

Haha, only you can decide this. The third question might come in handy – on whether you see yourself as a trader or investor. The considerations for each are very different.

“Everyone thinks they are Warren Buffet and a “Buy and Hold long term investor”.

Until prices start to drop…”

????

😉