A few months back, I wrote about how I hated the Mapletree Commercial Trust (MCT) – Mapletree North Asia Commercial Trust (MNACT) merger.

Well… this morning MCT came back and announced a revised offer:

MCT will now buy out MNACT with an all-cash offer.

To be funded via a preferential offering at $2.0039 per MCT Unit.

That is 100% backstopped by the Mapletree Sponsor.

Spoiler alert – I like this new merger.

As a MNACT unitholder, it was like Christmas come early.

As a MCT unitholder, I mean I still hate the merger, but it’s significantly better than the previous position.

Market seems to agree with me in any case.

MCT closed the day up 0.5%.

While MNACT closed the day up a whopping 8.9%.

What changed with the new MCT offer for MNACT?

There are 3 big parts to the new offer:

- MCT all cash offer for MNACT

- Funded via a preferential offering at $2.0039 per MCT Unit

- Mapletree Sponsor will backstop the entire preferential offering

Let’s run through each.

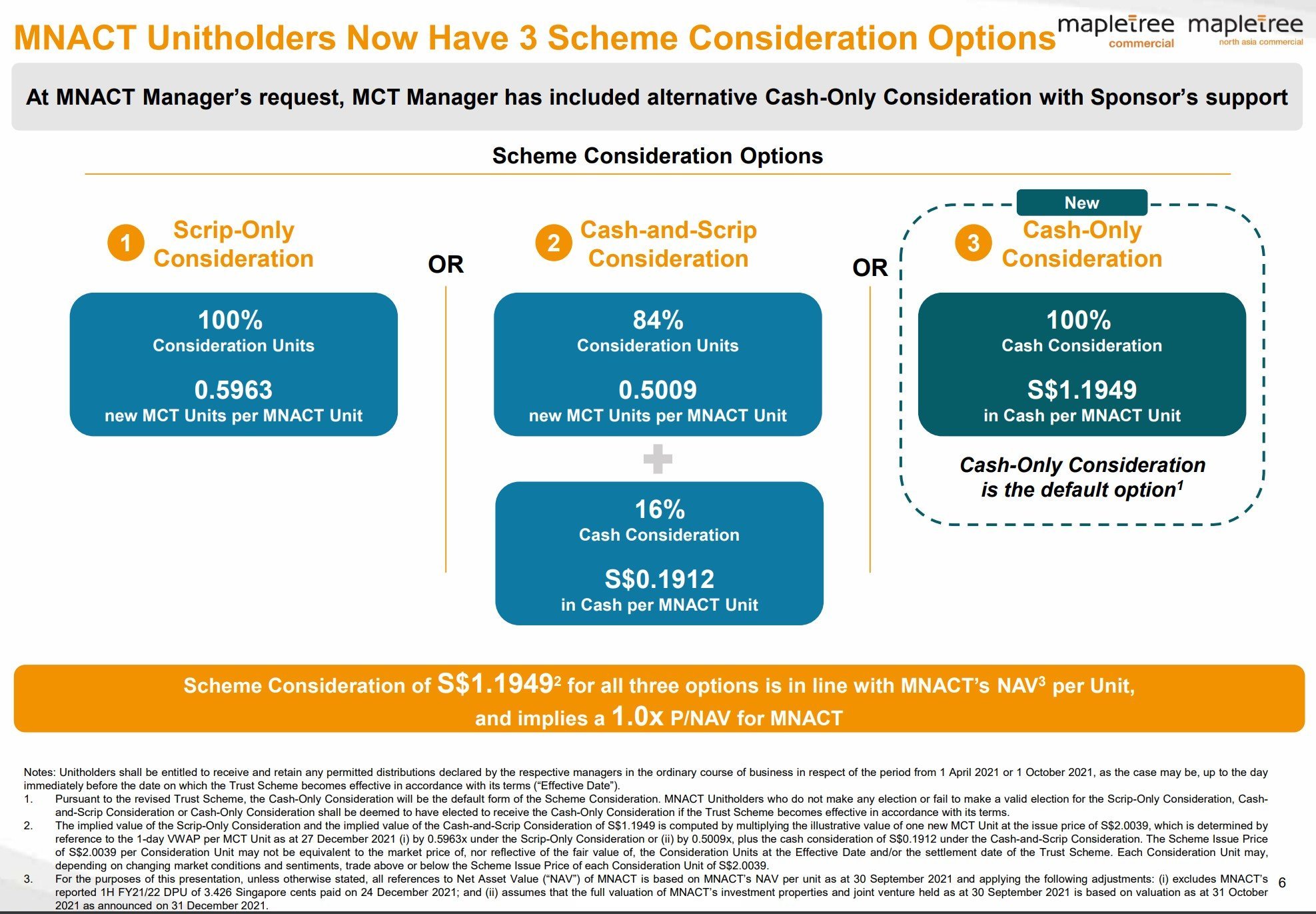

MCT all cash offer for MNACT

Previously MNACT unitholders were bought out in MCT units.

This is bad for MNACT unitholders because it exposes them to uncertainty in MCT’s unit price. If you didn’t want to hold MCT, you have to sell, but you don’t know what price the MCT units will be when you get them.

For MCT unitholders this was bad because it would have led to massive dumping of MCT units from disgruntled ex-MNACT unitholders.

Kinda like the Keppel offer for SPH – messy all round.

Well, MNACT unitholders will now have a new option – a buyout offer with 100% cash, at S$1.1949 per MNACT unit.

In fact – this is going to be the default option.

Fantastic.

MCT will fund the merger via preferential offering at $2.0039 per MCT Unit

Previously, the merger would be funded by giving MNACT Unitholders units in MCT.

But now MNACT unitholders get cash right?

So where does the cash come from?

Answer – MCT will fund it via a preferential offering at $2.0039 per MCT Units.

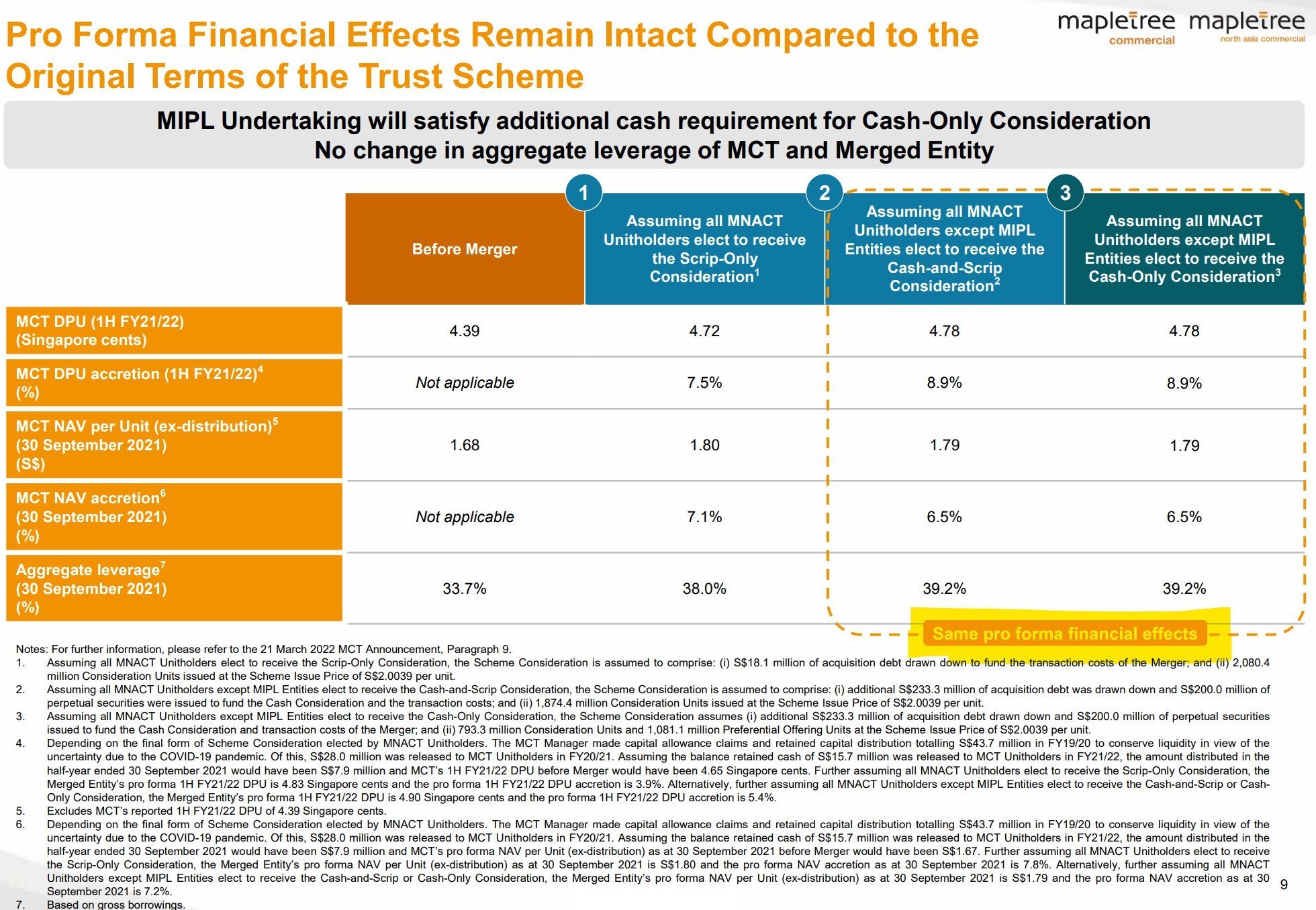

The reason why this is good is because the pro-forma impact to DPU and NAV does not change.

Or in simple English – the financial impact on MCT is exactly the same with the new merger, as with the previous merger.

MCT doesn’t need to take on any additional gearing or debt with the new merger.

And the advisors don’t need to redo the numbers. Yay…

Mapletree Sponsor will backstop the entire preferential offering

Don’t worry, I saved the best part for last.

The Mapletree Sponsor (Mapletree Investments Pte Ltd) will backstop the entire preferential offering.

To better understand what this means – MCT units trade at $1.9 today.

MCT is doing a big $2.2 billion preferential offering at $2.0039 per MCT Unit, to fund the acquisition.

But nobody in their right mind will take up the preferential offering at $2.0039 right, when the price on the open market is $1.9.

But… Mapletree Sponsor just said they will buy all the excess units that MCT unitholders won’t buy.

And no MCT unitholders will buy the preferential offering.

Which basically means – Mapletree will fund the entire MNACT acquisition themselves.

I mean… Whaaaaaat?

Don’t worry, you didn’t read that wrong.

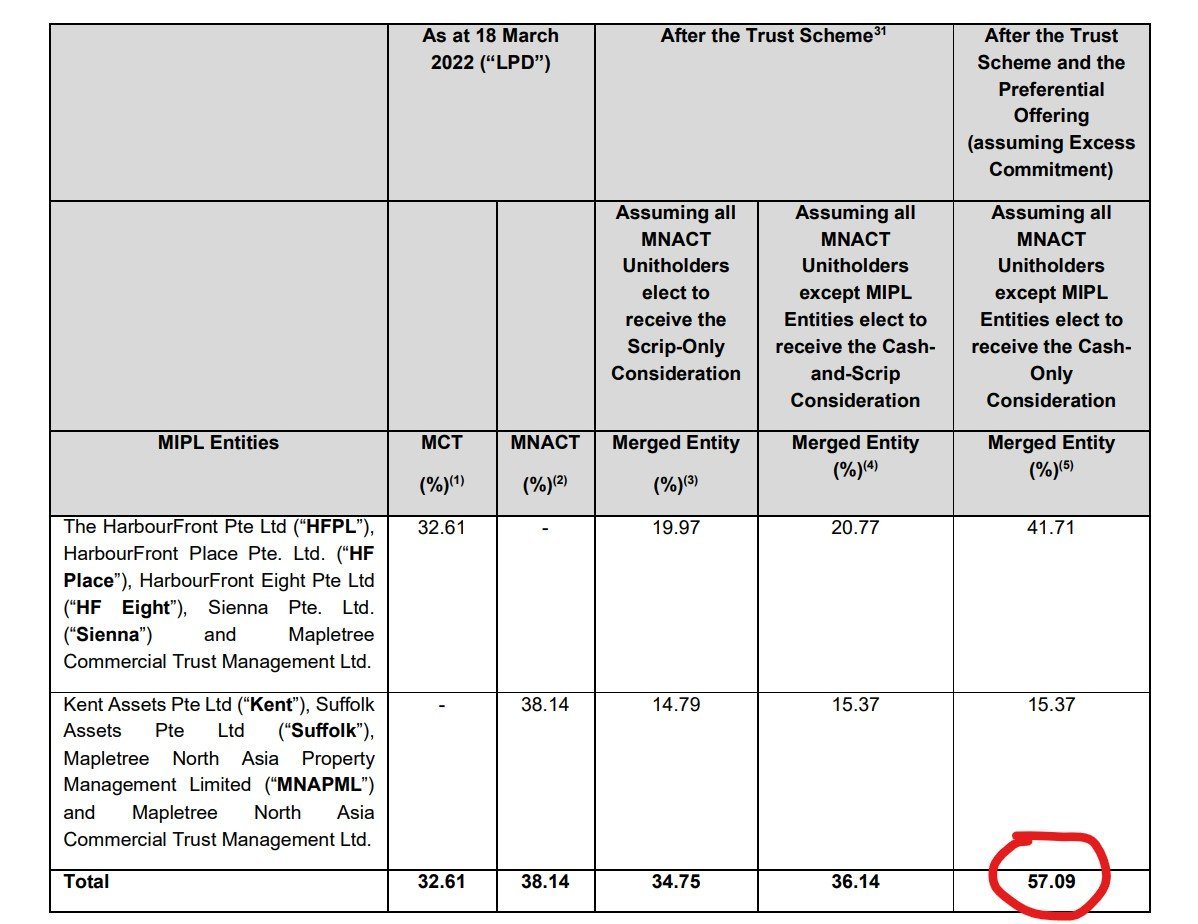

Assuming that no MCT unitholders take up the preferential offering, and all MNACT unitholder opt to take cash (which is basically a 99% chance at this point), then basically Mapletree Sponsor is going to buy all the new MCT units that are being issued to fund this acquisition.

And Mapletree’s stake in MCT will go up from 34.75% pre acquisition to 57.09% post acquisition.

To show how committed they are, Mapletree Sponsor even committed to not sell any of their units for 6 months.

Whaaaaat?

So FH… you are telling me that MNACT will effectively be privatised with an all cash offer at $1.1949.

And Mapletree will inject MNACT into MCT in exchange for units in MCT at $2.0039, which is 5% above MCT’s market price?

Well yeah… if you break it up and look at substance over form, it sure looks that way.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Just created a Discord server where I collate analyst reports and investing resources that I come across in my research. Hit us up here if you’re keen.

Why is Mapletree doing this?

I suppose the big question is why is Mapletree doing this?

This will cost them $2.2 billion to buy out all the unwanted MCT units in the preferential offering.

$2.2 billion they did not need to spend under the previous merger.

At a 5% premium to the latest closing price of MCT.

I mean… last I checked, Mapletree wasn’t a charity. Why are they suddenly so generous?

I suppose one way of looking at it is that maybe the brains behind this merger genuinely misgauged the market reaction.

Maybe they thought MCT and MNACT unitholders would have loved the offer.

And they were genuinely surprised by the horrible market response, that even led to shareholder activist action for MNACT.

And maybe after all that hoo-ha, they decided to return to their roots as one of the best Sponsor for S-REITs, and switch to a more unitholder friendly merger?

Okay I’m not an idiot, I know some of you may call me naïve for choosing to believe this sequence of events. And I know there are “alternative” interpretations of why they had to do this floating around.

But hey… a horse can dream right?

I love this merger as a MNACT unitholder

In any case, I love the merger as a MNACT unitholder (full disclosure – I own both MCT and MNACT units).

It’s effectively an all cash buyout for me, at NAV.

Which given how MNACT has been trading the past few years, is a pretty decent deal in my books.

In fact the market loved the merger so much, that MNACT units closed at $1.22 today, a whole 3 cents above the buyout price of $1.19.

This means that if you buy at $1.22 and the buyout closes, you only get $1.1949 in cash and whatever distribution from now until then (around $0.03).

Or in other words, the market is pricing in a very, very high probability (close to 100%) that this merger will close.

More neutral on the merger as a MCT unitholder

Okay, as a MCT unitholder I still hate the merger.

It does remove the short term uncertainty associated with MNACT unitholders dumping their positions on the open market.

And I don’t need to cough up any new capital for this merger.

So that’s good.

But longer term, it doesn’t really change the fact that I bought MCT for best in class exposure to the Greater Southern Waterfront via Vivocity and Mapletree Business City.

And now I’m only getting 50% of that, and the other 50% is a giant retail mall in Hong Kong and a bunch of offices in North Asia.

Kinda not what I signed up for… if you get what I mean.

But no denying that this is still a better deal than the previous one.

What will I do with my MCT/MNACT units?

Some of you have asked what I plan to do with my MCT / MNACT units.

For me it’s simple. If MNACT stays at $1.22 tomorrow I might just sell the entire position.

Time value of money, makes sense to cash out now and redeploy the funds, rather than wait till Aug to get the same amount back.

If it drops below (most likely), then I’ll just hold the units and take the cash when the time comes.

Unless of course MCT trades above $2.00 (when it’s time to choose) then I opt to take the MCT units, but frankly the odds of that are incredibly slim.

For my MCT units I will just hold.

It’s a core long term position for me, and I don’t see much point selling at this price.

MCT isn’t exactly a compelling must buy at this price too, so I won’t be adding in a big way too.

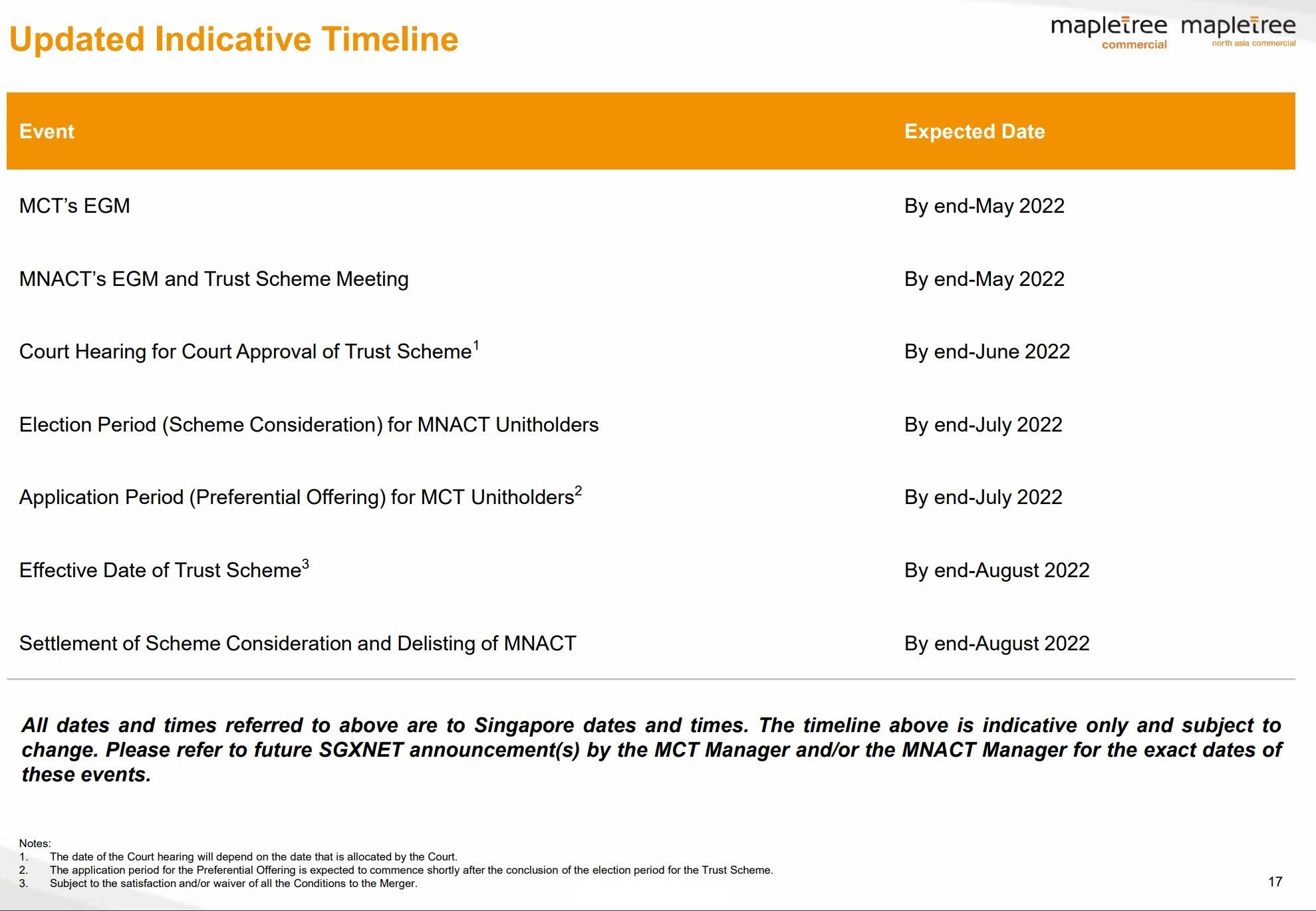

Timeline for MCT – MNACT merger

Timeline wise, the EGM for both Mapletree REITs is scheduled for end May, with everything wrapped up by end August.

As always – love to hear what you think!

Are you a Mapletree Commercial Trust or Mapletree North Asia Commercial Trust unitholder? Do you like this new merger?

As always, this article is written on 21 March 2022 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patreon.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 1 free Apple share (worth $230) you’re new to MooMoo and fund $2700.

Get a Free Apple stock (worth S$230) when you open a new account with Tiger Brokers and fund $2000.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

Hi, should I sell if I only own MNACT shares?

Thank you.

Well it’s really a personal call. For me I’ll prob hold on and take the cash in due course (and buy more MCT this year to replace my MNACT).

“And no MCT unitholders will buy the preferential offering.”

With regards to this point, wouldn’t a MCT unitholder’s shareholdings be diluted if he/she doesn’t buy the preferential offering?

I am a MCT unitholder. I am puzzled by this statement. Thanks.

Yes, but if so you can just buy on the open market at 1.9, instead of subscribing for the pref offer at 2.00. I mean of course the market is not efficient and some people will take up the pref offer, but the point is that Mapletree will probably backstop the bulk of the pref offer if price stays this way.

okay got you! thanks.

Dear FH

Like you, I hold both MCT and MNACT. Forgive my math, but who’s buying MNACT now at $1.23? Mapletree themselves? If retail investors’ intention is to own MCT post merger, why not simply buy MCT at current market price of $1.91 since the pref offer is $2.00? For dividends?

Hi,

Im investment noob holding MNACT. Whats the reason behind the prices hike to 1.23 abv the offer price of 1.19? And can i check if unitholder are generally waiting for Dividend ard May? (If there is even any plan to give dividend w the merger happening)

It is because of the distribution from now until privatisation. Should add up to about 3 – 6 cents, hence the market price is baking that in.

Can MNACT withhold distribution for period April 2022 to August 2022 and let MNACT merged with MCT in end August 2022 and then distribute it under the merged entity?

No, they will have to distribute before the merger.

Dear FH,

Your posts have been really helpful. About MNACT, did you only recently receive the Letter from them where MNACT holders are to indicate Options between (1) Cash-Only Consideration, (2) Scrip-Only, (3) Cash-and-Scrip Consideration?

I also think the same as you to go for (1) but am not sure whether things have changed that should make MNACT holders change our minds?

Think your assessment is probably right that last 2 options of MCT at 2.0039 is way above Market Price (checked MCT to be 1.87 today).

Yes, I would go with cash only. If one really likes MCT, they can just use the cash to buy MCT units on the open market today, which is below the rights issue price of 2.0039.

Hi FH,

Is it right to understand your article comments that you recommend (a) MNACT Cash-Only Consideration over (b) Scrip-Only Consideration because (b) gives us MCT units at much higher prices compared than ourselves purchasing from the Open Market, even after including transaction fees?

Yes – that is exactly right.