I took the opportunity with the recent correction in REIT prices to add to my position in Mapletree Commercial Trust (SGX: N2IU) at an average price of S$1.56. I am a long term admirer of Mapletree Commercial Trust (MCT), and in this article I will set out 5 reasons why I love MCT and plan to never sell my stake in this REIT.

Basics: Mapletree Commercial Trust

Mapletree Commercial Trust is a Singapore listed REIT, with a focus on Retail and Commercial/Business Park assets. All of its assets are based in Singapore, comprising:

VivoCity, Singapore’s largest mall located in the HarbourFront Precinct;

Mapletree Business City I , a large-scale integrated office and business park complex with Grade-A building specifications, located in the Alexandra Precinct;

PSA Building, an established integrated development with a 40-storey office block and a three-storey retail centre known as the Alexandra Retail Centre, located in the Alexandra Precinct;

Mapletree Anson, a 19-storey premium office building in Singapore’s Central Business District; and

Bank of America Merrill Lynch HarbourFront, a premium office building located in the HarbourFront Precinct.

This analysis is based on the long term REITs analysis framework, on which you can read more here.

1. Sponsor – Mapletree Investments Pte Ltd

Mapletree Commercial Trust is sponsored by Mapletree Investments Pte Ltd (MIPL), which was originally established to hold non-port properties transferred from PSA Corporation to Temasek Holdings. The ultimate holding company (ie. the owner) of MIPL is Temasek Holdings (Private) Limited.

Mapletree group has done very since it was established, having grown into a regional property developer today with strong operations across retail, commercial, business park, industrial and logistics asset classes, in Singapore, China, Hong Kong and Japan. The management team is very strong (a large amount of staff is CapitaLand alumni), and the company is very progressive and well run. As a group, Mapletree also tends to stay away from financial engineering when presenting their financials which I can really appreciate. As you may have gathered, I am a huge fan of Mapletree.

Mapletree, with its Temasek ties and behemoth status in the real estate industry, is in little risk of going under, and is unlikely to be pushed around at any negotiating table. Its large size and regional operations also gives it synergies and industry knowledge that smaller players will not enjoy.

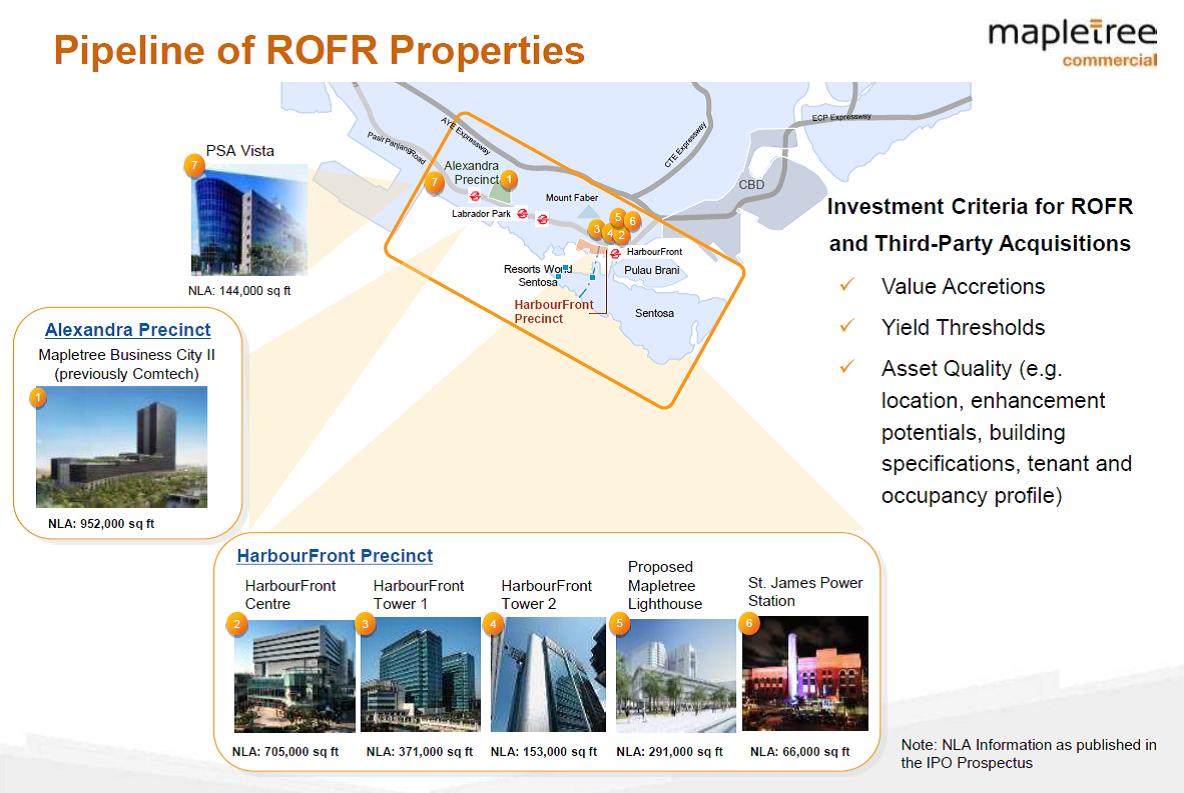

MIPL, as the sponsor, also provides MCT with an amazing ROFR pipeline as set out below. In particular, I am highly interested in the divestment of Mapletree Business City Phase II (MBC Phase II) to MCT. This is a best in class asset, with no true comparison in Singapore. As a long term investor, I am happy to wait patiently until the asset is eventually divested to MCT, as there is literally no other way of ever owning a stake in this asset (MIPL will never sell this gem to any other developer).

Source: 3Q 2017 Results Presentation

2. Premium to Book value

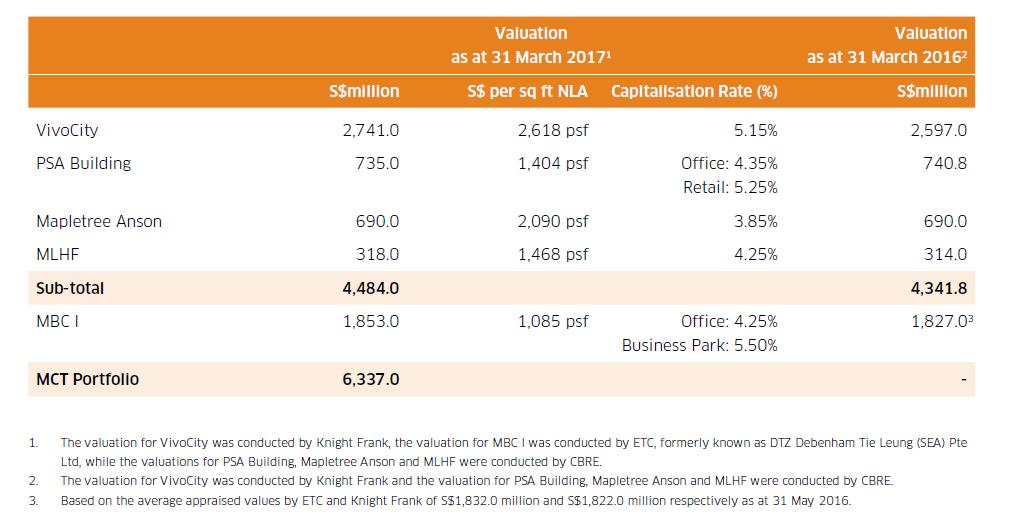

The NAV of MCT as at 31 December 2017 is S$1.37. At a price of S$1.56, I am paying 1.14 times book value, or a 14% premium to book.

There is no true comparison to benchmark MCT against, given the lack of any other blue chip Retail and Commercial/Business park S-REIT. As a rough gauge, CapitaLand Mall Trust (pure retail) is trading at 1.04 times book value, while CapitaLand Commercial Trust (pure commercial) is trading at book value. Frasers Commercial Trust, which owns commercial/business parks in Singapore and Australia, but which has assets of a much poorer quality, trades at 0.93 times book value.

MCT is definitely not cheap by any means, but still below the 15% premium soft limit that I set for all my REIT investments. Fortunately, its other qualities more than make up for this.

3. Sector / Geography

All of MCT’s assets are located in Singapore, split between the Retail and Commercial/Business Park classes.

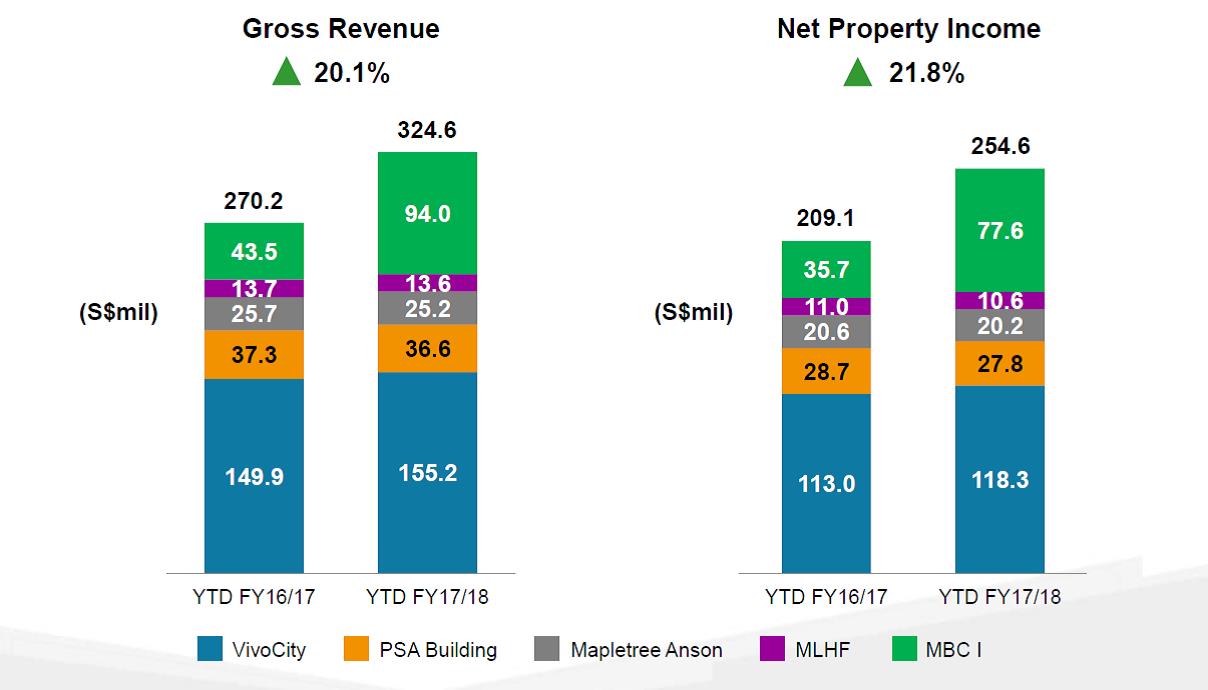

As evidenced below, more than 75% of its gross revenue is derived from Vivocity and Mapletree Business City Phase 1. Given that MBC Phase II is likely to be injected into the REIT once its yield stabilises, an investment in MCT is essentially an investment in Vivocity and MBC, with a smattering of offices and retail assets.

Source: 3Q 2017 Results Presentation

4. Quality of Assets

Fortunately, both Vivocity and Mapletree Business City (both Phase I and II) are best in class assets, with no true peer in the Singapore market. Let’s go through them individually.

Vivocity

With an NLA of 1.04 million sq ft, Vivocity is the largest retail mall in Singapore. It is located at Harbourfront MRT, the gateway to Sentosa and Singapore Cruise Centre. There is no other competitor mall of similar class anywhere near in the vicinity.

I have been to Vivocity countless times, and each time it seems to be even busier, with a swanky new wing. Singaporeans absolutely love this mall. The anchor tenants which draw crowds are Golden Village and Giant, and of course, there is no way to get to Sentosa or Singapore Cruise Centre without passing through Vivocity. Given its location by the sea, the Navy also holds its open house at Vivocity, which is a fantastic boost in traffic to the mall.

The mall layout is intuitive and encourages window browsing. There is a bit of everything for everyone, with a playground for young children, a nice boardwalk for couples and families, not to mention cinema, supermarkets, fashion, F&B and electronics.

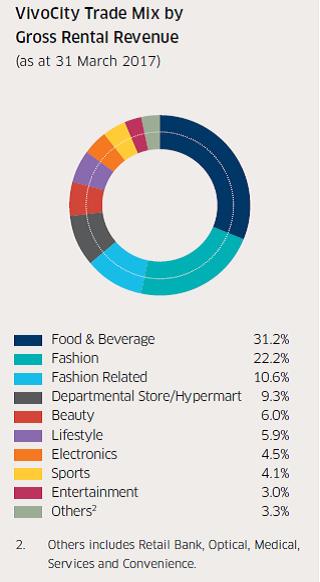

The tenant mix as set out below is well diversified with F&B capped at 31% which is typical. The higher yielding fashion retailers come in at a 22%, which is decent and should be manageable (too much fashion is worrying because of the impact of eCommerce on these retailers, but too low a mix affects the rental yield).

Source: FY2016 Annual Report

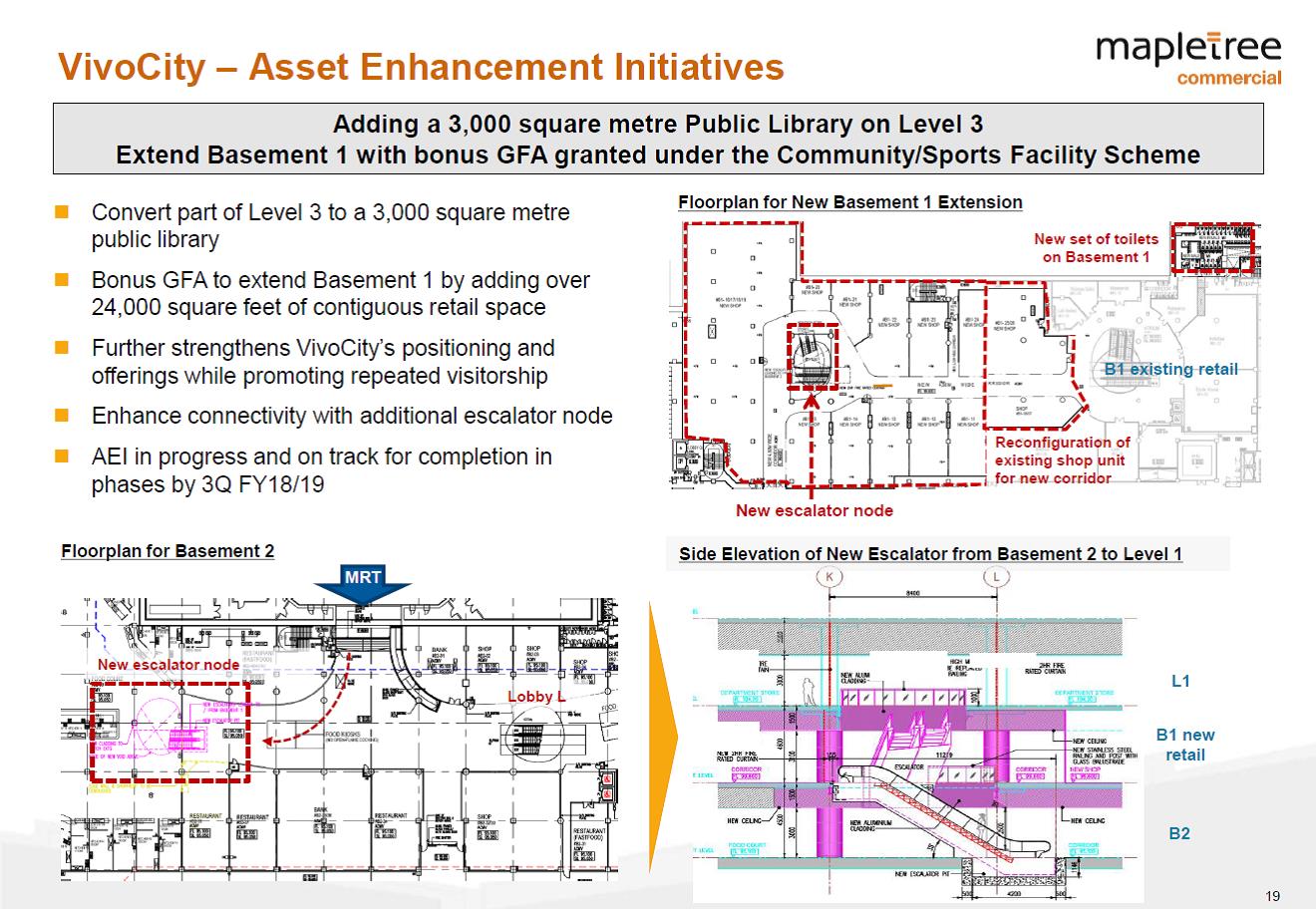

Vivocity is an endless source of Asset Enhancement Initiatives (AEI), as evidenced by MCT’s long track record in using AEI to open a new wing and improve NPI. Case in point – MCT is now building a library at Level 3, which is a fantastic move. Lever 3 rents are typically lower given the lower footfall, so MCT does not lose much on rent anyway, and the library serves as an additional anchor tenant to draw crowds to the mall, and boost overall stickiness. Parents can leave their children (or husbands) at the library at while they shop now, and the impact of these small intangibles can really add up to the mall experience. I am confident in MCT’s ability to value add to Vivocity going forward.

Source: 3Q 2017 Results Presentation

I would be worried if the capitalisation rate for a REIT’s assets is too low and not in line with competitors, as that may indicate an artificially inflated valuation. Fortunately, the capitalisation rate for Vivocity is 5.15%, which is decent and compares quite favourably with the approximately 5% used by CapitaLand Mall Trust for their malls.

Source: 3Q 2017 Results Presentation

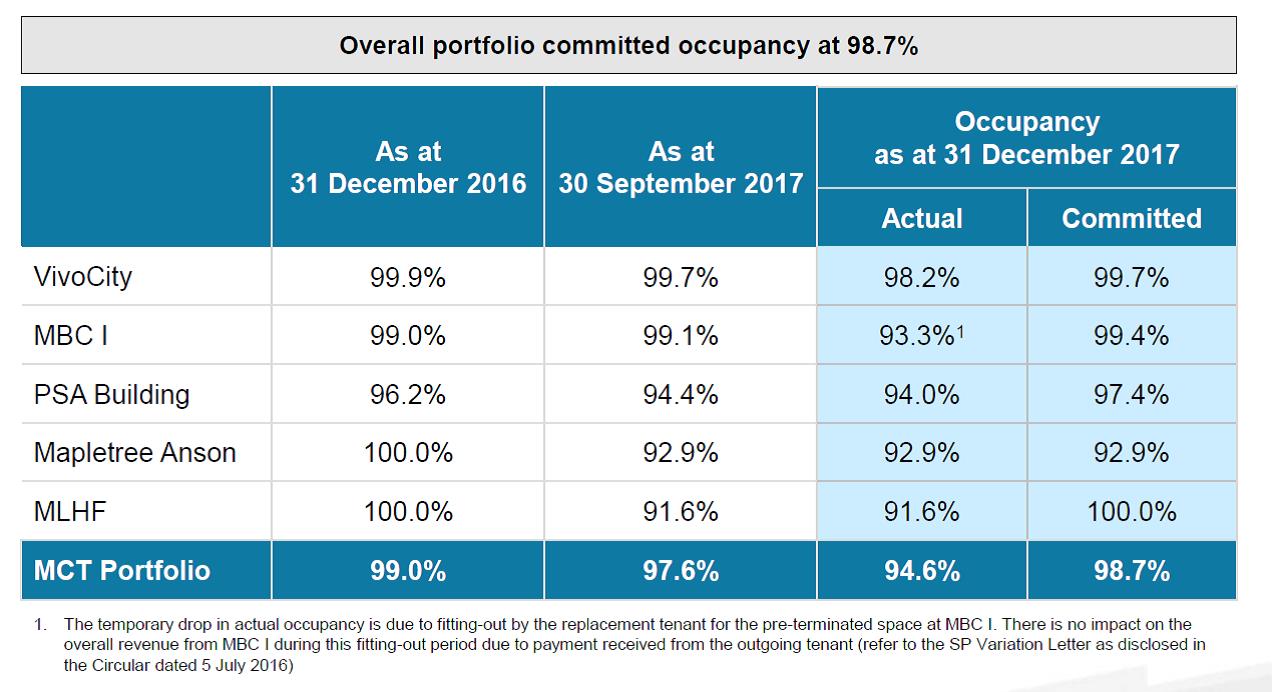

Committed occupancy numbers are close to 100%, and rental reversion has experienced low single digit growth, in line with what is seen at CapitaLand Mall Trust, the other blue chip retail player in Singapore.

Source: 3Q 2017 Results Presentation

Mapletree Business City (Phase 1)

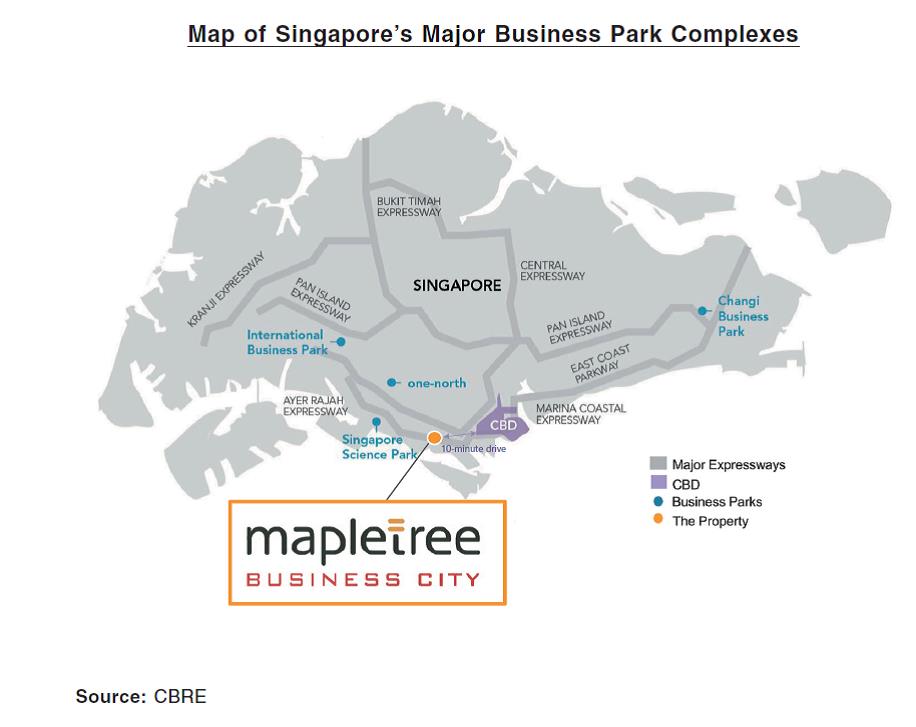

Mapletree Business City (Phase 1) has a NLA of 1.7 million sq ft. There is a scarcity of Grade A business parks in Singapore, and location wise, MBC is the closest business park (10 min drive) from the CBD. In this aspect, it is far superior to Changi Business Park or International Business Park, especially for businesses who want to enjoy Grade A office space at a significantly lower price, but yet remain close to the CBD. Mapletree’s own headquarters are at MBC, testament to the quality of the business park. Based on location and building specification alone, there really is no peer to MBC.

That aside, I personally am a huge fan of the intangible, business park feel at MBC, which I feel is not replicated at Changi Business Park. It is windy, well-constructed, has ample parking lots and lots of water and greenery, giving one a peaceful and tranquil feel. In recent years, tech companies such as Google and Facebook have moved their Singapore offices to MBC (perhaps for the reasons described above, and also the fact that is better replicates a silicon valley feel). If Singapore is to become a regional tech hub, I do foresee this trend growing in future. I highly encourage prospective investors to take a drive down to MBC and take a look for yourself, since this forms almost 25% of an investment in MCT (even more when MIPL injects MBC Phase II). If you don’t like the idea or concept of MBC, you should not be investing in MCT.

Source: Circular to approve acquisition of MBC Phase I

Key tenants at MBC include HSBC, GovTech, Samsung Asia Pte. Ltd., SAP Asia Pte. Ltd. There is a strong tech/industrial bent to their clients, and I expect this trend to continue going forward.

Source: FY2016 Annual Report

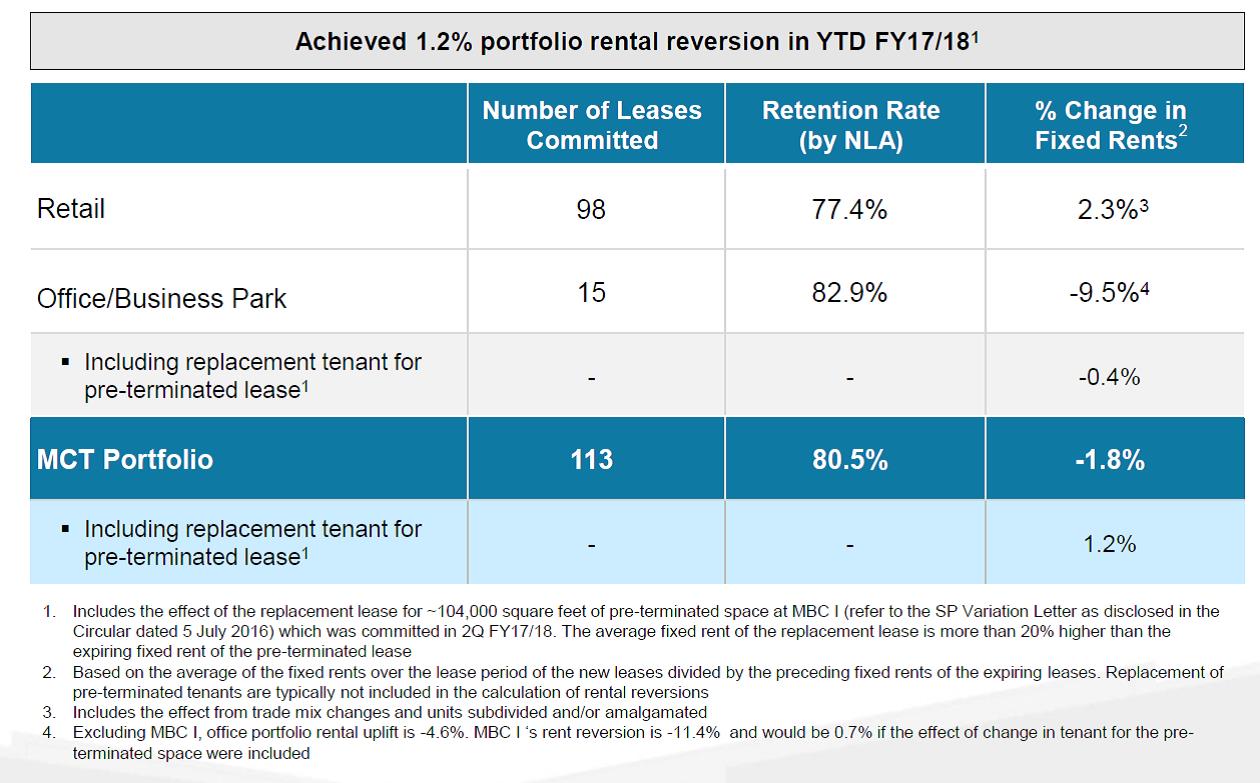

The capitalisation rate of MBC Phase 1 is 4.25%, which is comparable with the 3+% used by CapitaLand Commercial trust for their office assets. There was a drop in rental reversion, but it seems this was due to a change in tenant, with a new tenant already pre-committed at a higher rent.

Remaining Assets

MCT’s remaining properties are PSA building, Mapletree Anson, and Bank of America Merrill Lynch HarbourFront. These account for about 20% of MCT’s top line. I will not go through the properties individually, but will add that office rents are at a good place now, with Grade A core CBD rents on the uptick (3.3% qoq increase). This bodes well for Mapletree Anson, and may have flow on effects for PSA building and Bank of America Merrill Lynch HarbourFront.

5. Distribution Yield

A bird in hand is worth two in the bush. I love DPU as it is real money in your hands; unit price appreciation is not. Even if locked in, the tendency is to plough your gains into a new investment to offset the lost income. Eventually when the market corrects, the birds in the bush remain in the bush.

At a purchase price of S$1.56, the trailing twelve month yield is approximately 5.8%. Given the best in class assets held by MCT, I do not envisage that this yield will be at risk, barring a global financial crisis.

By comparison, CapitaLand Mall Trust pays a 5.5% yield, CapitaLand Commercial Trust pays a 4.7% yield, while Frasers Commercial Trust (a much riskier REIT given its lower quality of assets and Australian exposure) pays a 6.6% yield. MCT’s distribution yield is quite attractive by comparison.

Problems

What then, are the problems that I anticipate with an investment in MCT?

1. Interest rates

One real problem with an investment in REITs, or real estate in general, is the current rising interest rate environment. MCT’s 36.3% gearing is decent, but rising interest rates will affect the cost of refinancing, and consequently DPU. The finance team has done a decent job in spreading out the debt maturity profile, so I do not see any outsized risks.

My personal take is that rising interest rates will have a profound impact on global asset prices. However, standing by the sidelines is not a solution either, and given that much of the global macro climate is beyond my control, I will continue to stay invested while remaining vigilant to such risks. MCT, with its Mapletree and Temasek links, should be better placed to weather this rising interest rate environment when compared to other non-sponsored REITs.

Source: 3Q 2017 Results Presentation

2. Retail Exposure

With Vivocity contributing 50% of NPI, MCT is basically half a retail REIT. With the rise of eCommerce, a huge number of smaller retail malls and retailers are really starting to see the pain. This is likely to worsen in the coming years.

However, in land scarce Singapore where the national pastime is hanging out at a mall, I do not see the mall going away anytime soon. While I can now order a fridge online and not go to a mall, when meeting a friend, hanging out with loved ones, or going for a meal/movie, there really is no replacement for a Plaza Sing or Vivocity. I expect this to apply for all fellow Singaporeans as well. The death of the mall then, is something that is greatly exaggerated. What is likely to happen though, is that retail managers will adapt the tenant mix accordingly, to focus on retailers that can succeed in this changing climate. This may be a focus on F&B, or experiential shopping (see eg. the Funan project). I believe that we a likely to see a few years of pain for the retail industry (low single digit or flat rental reversions), until the retailers find their footing for the next stage of growth. CapitaLand Mall Trust, the other blue chip retail player in the Singapore market, is currently experiencing low single digit rental reversions, which does seem in line with this position.

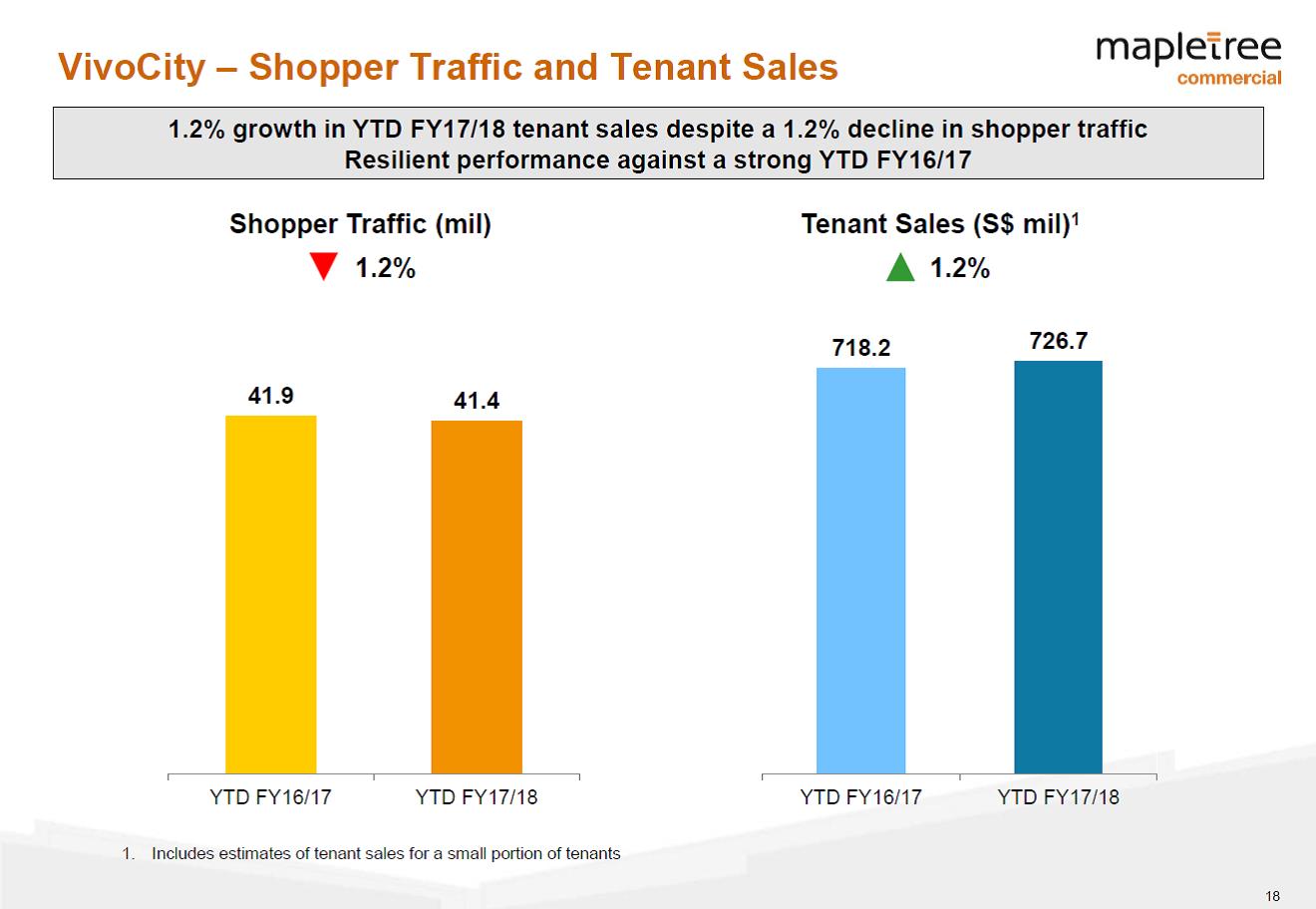

As seen from the chart below, Vivocity is experiencing a slight drop in shopper traffic, but a slight increase in tenant sales, which does indicate that the mall is still very relevant today.

Source: 3Q 2017 Results Presentation

Closing Thoughts

Outside of a global recession, I am fairly confident in Mapletree’s ability to continue to execute, to value add, and achieve DPU growth. The greatest tail risks to me are an increase in global interest rates, and a fall in competitiveness of Vivocity.

However, global interest rates impact all REITs and all asset classes, which Mapletree (basically Temasek) should be better placed than others to weather. Vivocity for now is still a best in class asset with amazing location, catchment, and a special place in the heart of every Singaporean.

The bottom line is that there is no investment without risk. Yet I am getting compensated a handsome 5.8% distribution a year for taking on these risks, which is significantly higher than the 2.5% risk free premium of a government bond. This is a risk I am comfortable to take, especially when the investment involves Vivocity and Mapletree Business City, two gems in the Singapore real estate market with no real rival. The injection of Mapletree Business City Phase II in the years to come is pure icing on the cake for a long term investor such as myself.

I will give Mapletree Commercial Trust a four Financial Horse Rating.

How about an investment in this 4.3% yielding bank stock to go with your S-REIT? Take a look at Financial Horse’s thoughts on DBS Bank here.

Mapletree Commercial Trust – Financial Horse Rating

Rating Scale:

Enjoyed this article? Like our Facebook Page for more great articles!

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. I share this with all my email subscribers at absolutely no cost. Sign up for the newsletter now!

[mc4wp_form id=”173″]

I think its very dangerous to say that you plan to never sell a REIT. A lot of things could change. There will be areas that we might not have considered before.

Hi Kyith,

Thanks for the comment, you are absolutely right. If Vivocity has a fall in competitiveness, or business parks fall out of favour, I may very well reevaluate my investment thesis. Perhaps a better title for this article would be Why I have no plans to sell MCT in the near future. 🙂

Cheers. I am a great fan of your blog, and very good to hear from you.

Never is a long time.

Hi Sir,

Yes that is absolutely right. My use of the word “never” is to highlight that I intend to take an ultra long, multi decade position in MCT. Of course, if my investment thesis no longer holds true, perhaps if Vivocity is no longer a premier mall, or Mapletree Business City faces massive competition, I would consider existing my position in MCT.

Cheers.

A quarter of leases up to 25.8% of rental revenue is expiring in FY18. About 2 times of that in FY17.

Any big tenants or renewal impact?

Does PSA’s planned relocation to Tuas concern you?

Does the planned relocation of PSA to Tuas concern you?