Mapletree Greater China Commercial Trust (MGCCT) recently announced that it would be acquiring a portfolio of six freehold commercial real estate assets located in Tokyo, Chiba and Yokohama, Japan. Following the completion of the acquisition, MGCCT will be renamed to “Mapletree North Asia Commercial Trust”.

I think a lot of pundits in the market have been calling this since MGCCT expanded their investment mandate to include Japan back in January, so this move didn’t come as a surprise to anyone. Having seen the finer details though, Financial Horse, a unitholder himself, is quite pleased with this acquisition.

Basics: MGCCT’s IPT acquisition of a Japan Portfolio from MJOF

Mapletree is acquiring the six Japan assets from MJOF Pte. Ltd. I extracted the full description of MJOF below, but basically it’s a private fund managed by Mapletree. The acquisition is likely due to end of fund life, so the divestment to the listed REIT allows the fund to exit its investment, while providing a ready portfolio of mature assets to the REIT.

MJOF is a private real estate closed-end fund which is managed by MIJ with Mapletree Real Estate Advisors Pte. Ltd. (“MREAL”) as the investment advisor. Both MIJ and MREAL are indirect wholly-owned subsidiaries of Mapletree Investments Pte. Ltd. (“MIPL” or the “Sponsor”). The Sponsor holds an approximate 36.0% stake in MJOF.

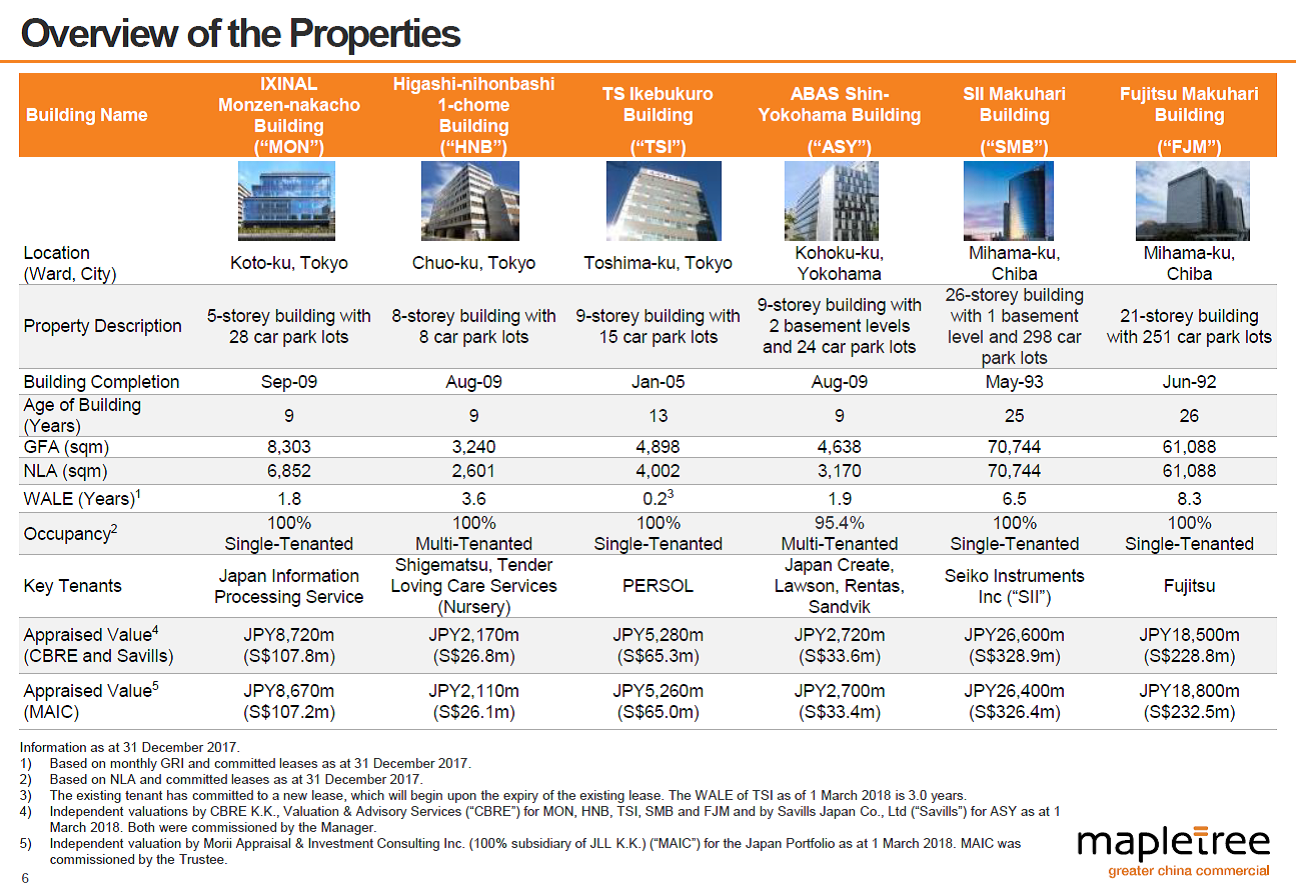

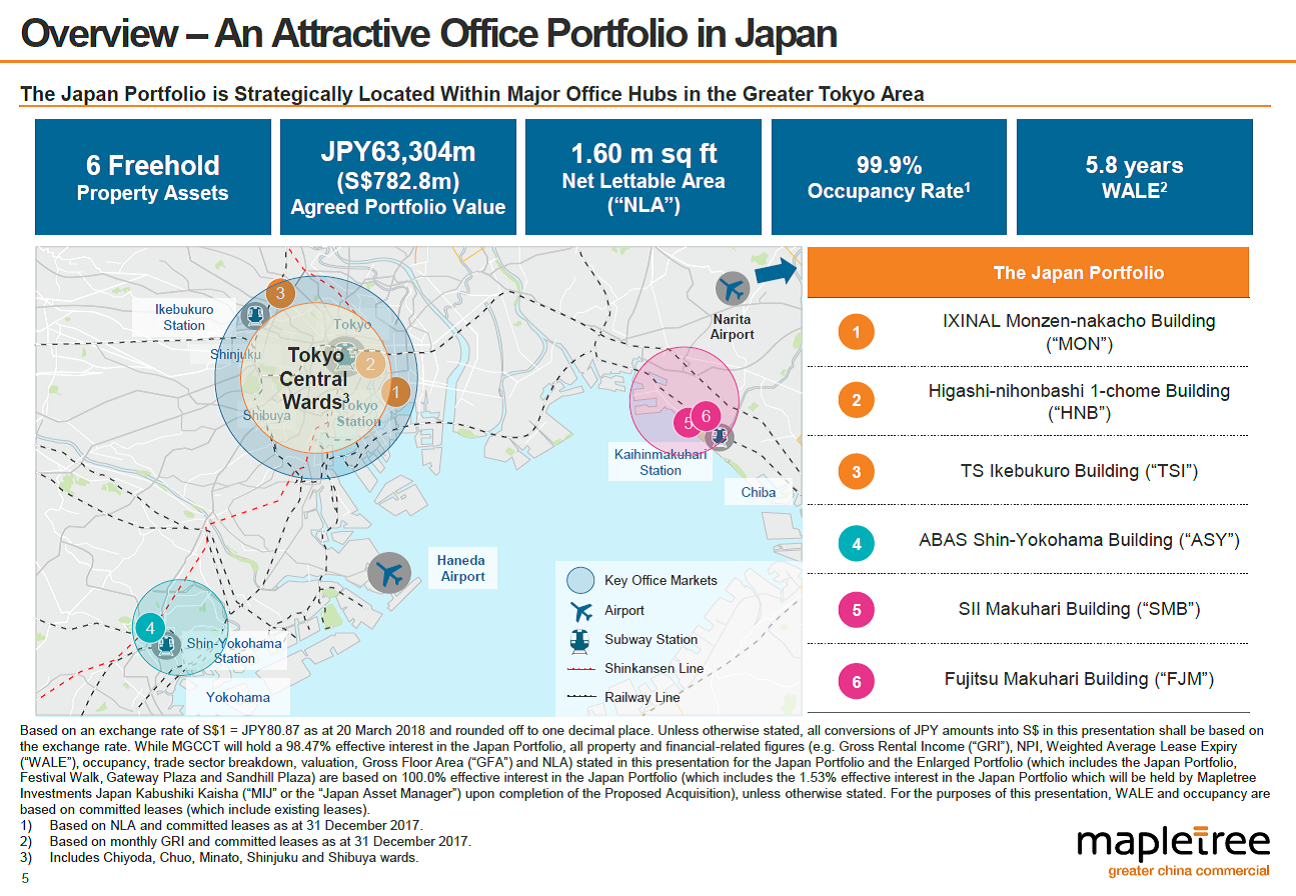

The slides below elaborate on the assets being acquired:

Source: Presentation Slides

What I like about the acquisition

1. DPU accretive

There is nothing a Unitholder likes more than the words “DPU accretive”. A lot of REITs throw the words around to the point that it has lost its meaning, but in this case, the acquisition truly is DPU accretive. Mapletree has a strong reputation of staying away from financial engineering, so I place a lot of weight on the numbers they publish.

I’ve extracted the numbers below from their acquisition announcement on SGXNET. There are strict disclosure requirements under the listing manual (it’s a Chapter 10 transaction), so these numbers can’t really be gamed.

It’s quite clear that the acquisition is DPU accretive to the tune of 3.6%, even assuming the issuance of 296.4 million new units at S$1.09 to fund the acquisition (which is an 8% discount to the latest closing price of S$1.18 as at 16 April – really large discount, please do not do this Mapletree). If the new units are issued at a smaller discount, the deal could be even more accretive.

Effect of the Proposed Acquisition Before the Proposed Acquisition After the Proposed Acquisition Total return before income tax (S$’000) 412.6 445.3(1) Income available for distribution to Unitholders (S$’000) 204.6 234.9 Units in issue at the end of the year (million) 2,795.4 3,097.1(2) DPU (S$ cents) 7.341 7.602 DPU accretion (%) – 3.6% Note(s):

(1) On a consolidated basis, based on 100% contribution of the Japan Portfolio. Includes expenses comprising net borrowing costs associated with the drawdown from the New Loan Facilities of approximately JPY 52,985.1 million (approximately S$655.2 million) (adjusted for non-controlling interest) and after the refinancing of certain of MGCCT’s existing bank loans, the Manager’s management fees, Trustee’s fees and other trust expenses incurred in connection with the operation of the Japan Properties.

(2) The total number of Units in issue at the end of the year includes (a) approximately 296.4 million New Units issued in connection with the Equity Fund Raising to partially finance the Proposed Acquisition and (b) approximately 5.3 million Acquisition Fee Units.

2. No income support

What I really like about Mapletree is that they do not do income support. There is nothing I hate more than a REIT buying a young asset with income support and selling it to unitholders on the basis that it is “DPU accretive”. It is not.

With this Japan portfolio, the assets are mature and will contribute to MGCCT’s NPI from day one, without the need for income support.

Given that this is MGCCT’s first foray into Japan, I would have expected nothing more from them.

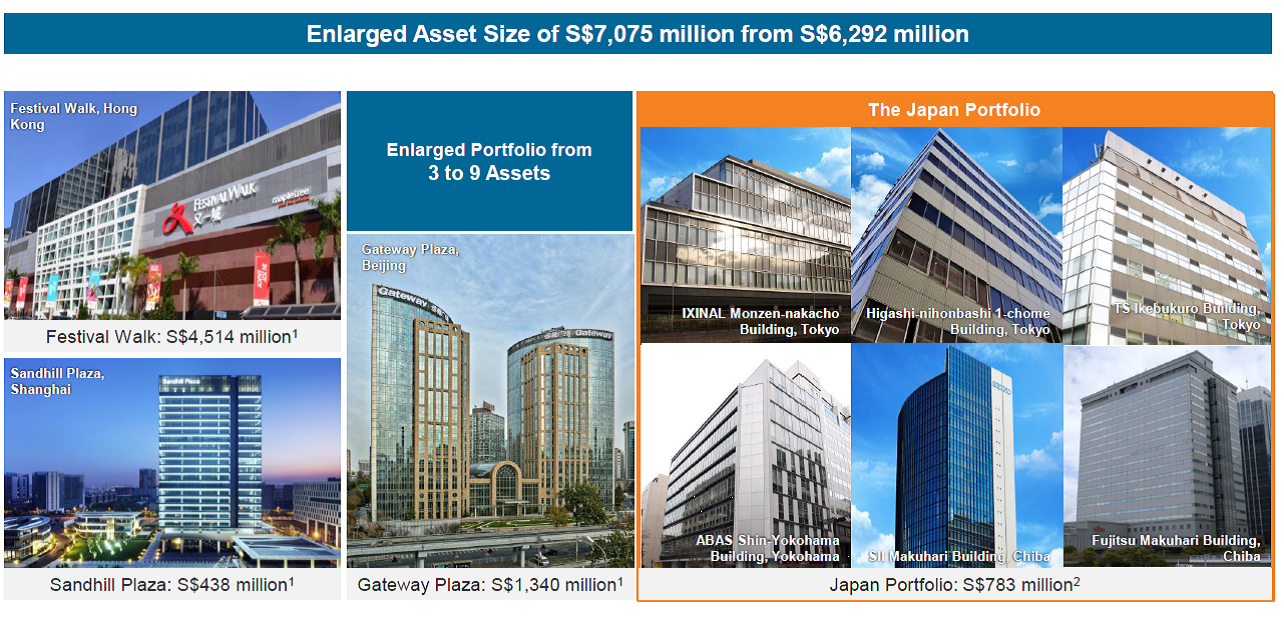

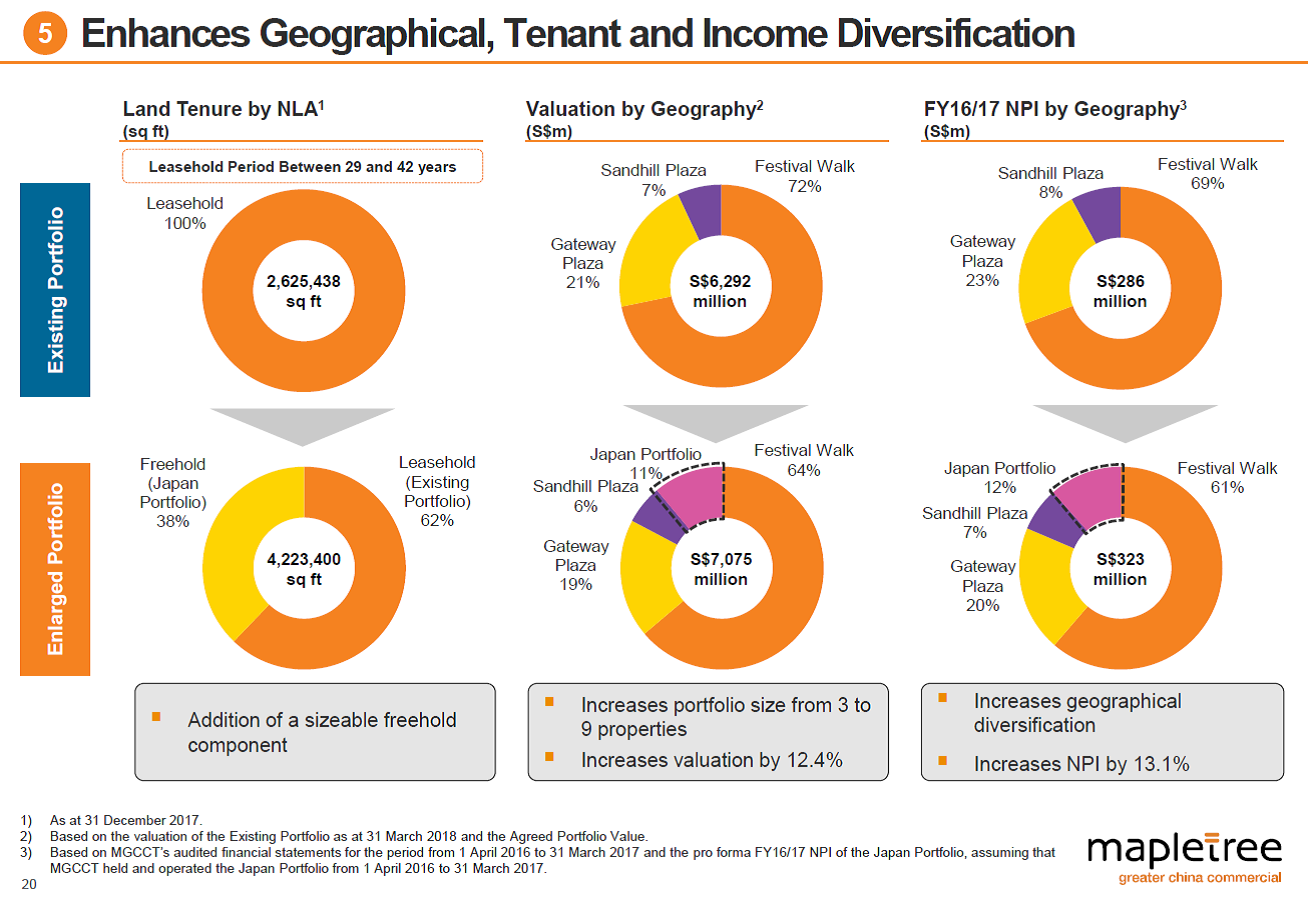

3. Diversification of NPI

Before this acquisition, my main gripe with MGCCT was how concentrated the portfolio was among HK assets.

As the slide below illustrates, this acquisition does a fair job in diversifying MGCCT’s portfolio, reducing concentration risk.

4. Mapletree North Asia Commercial Trust = MCT of China and Japan?

The name change to Mapletree North Asia Commercial Trust is really interesting. One problem that MGCCT had in recent years was trying to grow its asset portfolio, as they have found it hard to get a foothold into mainland China.

This expansion into Japan, and name change, seems to indicate that they may be looking at North Asia more generally going forward.

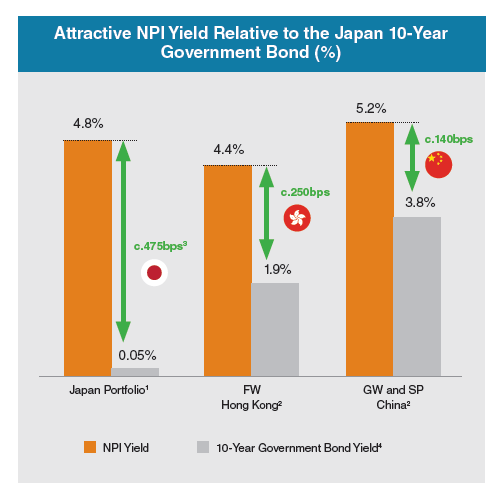

I do like Japan as a country, mainly because of their cheap debt, rivalled only by Germany. In Japan, it is easy to borrow at about an average cost of borrowing of 1%. By buying a 4.8% yielding portfolio, that’s a massive 380bps spread for unitholders. You need to look no further than Parkway Life REIT to see the marvels this can do for a REIT.

If they can turn MGCCT into the North Asia version of MCT, I would be a very happy unitholder indeed.

Source: Mapletree Circular

What I like less

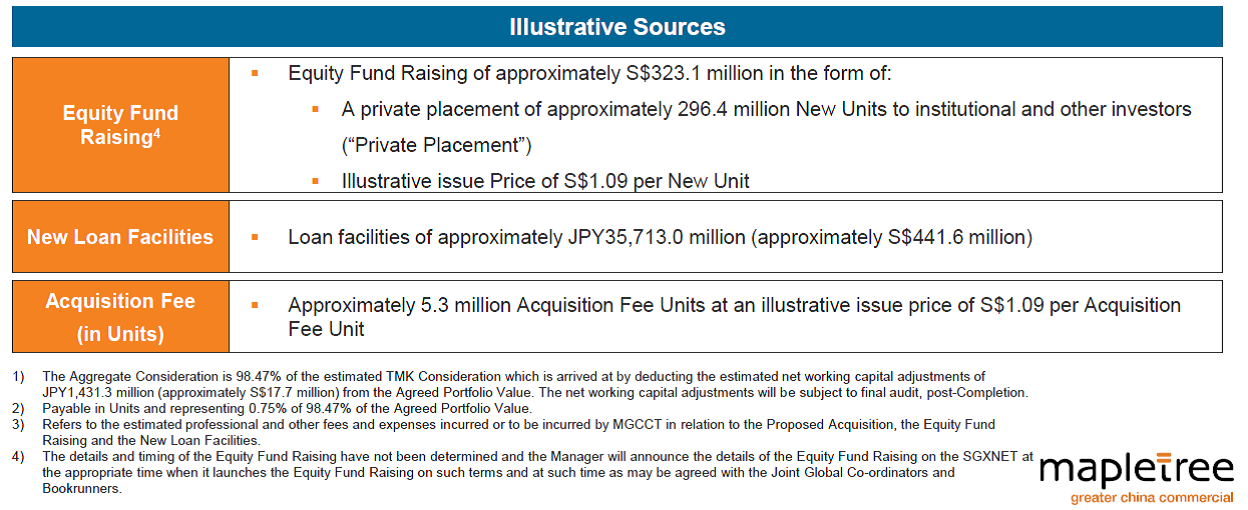

1. Where is my opportunity to participate in the EFR?

It looks a lot like the acquisition is going to be funded by an Equity Fund Raising (EFR) via placement. It even says so on the “Illustrative Sources” slide below. This means that retail investors have no chance to participate in the EFR, and will have to sit by idly while institutional investors mop up the units at a discount.

I am hoping for a rights issue/preferential offering, although frankly I am not optimistic, given the volatility in the financial markets currently. It’s a bit too risky to attempt a public EFR.

That said, if they do attempt a placement, I expect a far lower spread than the 8% discount they are pricing. A lot of unitholders, including myself, are going to be up in arms if the placement does eventually go ahead at S$1.09.

2. Certain assets are single tenanted

I can’t quite comment on the quality of the assets beyond what I read in the circular, having never visited them myself.

However, what stands out is that SII Makuhari Building, Fujitsu Makuhari Building and TS Ikebukuro Building are single tenanted to Seiko, Fujitsu and PERSOL respectively. These 3 building collectively form about S$500 million of the S$780 million portfolio being acquired.

There’s a bit of risk here given that if the existing tenant decides to uproot and go, it may be hard to lease out these buildings, which are likely to have been custom designed for the existing tenant.

In the grand scheme of things however, these ultimately form a small part of MGCCT’s overall portfolio, and the portfolio as a whole is fairly diversified even if such risks were to materialise.

Closing Thoughts

This Japan acquisition addresses 2 problems for me. Firstly, it answers the question of where MGCCT’s future growth would come from. Secondly, it diversifies MGCCT’s portfolio, which was a bit too concentrated in Festival Walk for my liking. I also love the fact that these are mature assets without income support.

The EFR is a bit of an unknown, because we don’t know how large a discount they would price the new units. However, this is understandable given the current volatility in the financial markets.

All in all, I do like this transaction, from the perspective of a long term unitholder.

Find out what I think about MGCCT’s sister REIT, Mapletree Commercial Trust here.

Enjoyed this article? Like our Facebook Page for more great articles!

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. I share this with all my email subscribers at absolutely no cost. Sign up for the newsletter now!

[mc4wp_form id=”173″]

how many horses do you give this acquisition?

Hi Jason,

I didn’t want to give this acquisition a rating originally since it ultimately forms only a part of MGCCT, and the REIT should be evaluated holistically.

But if I were to give a rating, I would give it four horses.

I like that (1) these are mature assets with no income support, (2) this clarifies the growth story for MGCCT going forward, (3) this is DPU accretive, and (4) it diversifies the asset portfolio of MGCCT. I don’t like the EFR (seems likely to be private placement), but to be honest, in this kind of market environment it is to be expected.

Cheers.

Are you concerned by Japan’s declining population and its potential impact on MGCCT’s Japan properties? For example, one of the tenants is described as a ‘Nursery’ and Japan’s dismal birthrate would have an adverse impact on its enrollment and long-term viability. That, in turn, would impact MGCCT’s rental yield and occupancy of its Japan properties.

Hi Ben, thats a really good question.

Yes, I agree that this is a potential issue, but one that affects the entire Japan market. There is no ready solution apart exiting the Japan market entirely. In fact, even Singapore has an ageing population issue, albeit less pronounced.

If we look at MGCCT holistically, this new Japan portfolio forms 11% of the portfolio by valuation, so the REIT is still very diversified outside of Japan. By contrast the benefits to the REIT are that this acquisition is DPU accretive, and provides a clear path for future growth. Weighing the pros and cons, I would say that on balance, the benefits outweigh the costs for unitholders. Of course. if MGCCT expands to the point where Japan forms half of its portfolio by valuation, we may need to reevaluate this thesis.

However, it would be many years before they hit such a point, and I suspect there will be many opportunities to exit this investment in the meantime if one is not comfortable with Japan.

Cheers