After the past week, a lot of you asked if the stock market has bottomed out.

And I must admit, I was actually pretty surprised by the Astrea 7 Balloting Results (which was frankly abysmal).

When I was calling for stocks to drop back in Dec/Jan, few agreed with me then.

It was the hard decision, but also the right one.

Fast forward to mid 2022, and suddenly everyone is a bear.

Everyone “agrees” that stocks are going to drop more as 2022 plays out.

And this makes me very, very nervous about my call.

Investor sentiment in Singapore is poor

Let’s survey the landscape.

Astrea 7 Balloting Results were dismal. It looks even worse than Astrea IV, despite having a much higher yield.

The recent Lendlease REIT rights issue paints a similar story. Despite being priced at an attractive discount, the take up rate was very poor.

Retail investors seem reluctant to part with their cash.

If you just look around at the investor Facebook groups and chats, you’ll find very similar sentiments.

Bill Ackman is crying again…

This horse is old enough to remember 2 years ago when Bill Ackman appeared on live TV and cried about a collapse in the stock market.

Exactly at the same time as he was covering his massive short (at the market bottom).

Basically, Bill is a contrarian indicator.

Just do the opposite of what he says and you’ll be fine.

Well… Bill is back.. and he’s crying again.

This should be worrying for bears.

George Soros

But George Soros probably takes the cake on bearish sentiment with this headline.

Bearish sentiment seems to be at a fever pitch

What I’m trying to say, is that suddenly everyone seems to be very bearish.

And when investors generally agree on something – you always want to question it.

Big money is seldom made by following the crowd.

Big money is made by doing what is uncomfortable.

So I decided to requestion all my fundamental assumptions about the market.

Is it possible that the stock market has already bottomed, and the path forward lies with recovery?

Are valuations more reasonable?

Let’s start by looking bottom up – with valuations.

SEA

The formerly “bigger than DBS” SEA stock has collapsed 80% from highs.

At current price, it trades at:

- 9 times sales

- EV/EBITDA of -23

And a P/E that is not meaningful because well… there are no profits in this company.

So… are you prepared to say that SEA is dirt cheap value at its 44 billion market cap?

And really, that’s a tricky question.

If we are indeed moving into a decade of higher inflation and higher rates volatility, then investors are going to value stocks on archaic metrics like P/E and P/Free Cash Flow (I know… what blasphemy).

The writing is on the wall too – because you see all these tech companies like SEA and Grab scrambling to pivot their business model to focus on profitability over growth.

Until they do though, nobody really knows the earnings potential for stocks like that.

Which makes it tough to call a bottom based on valuations.

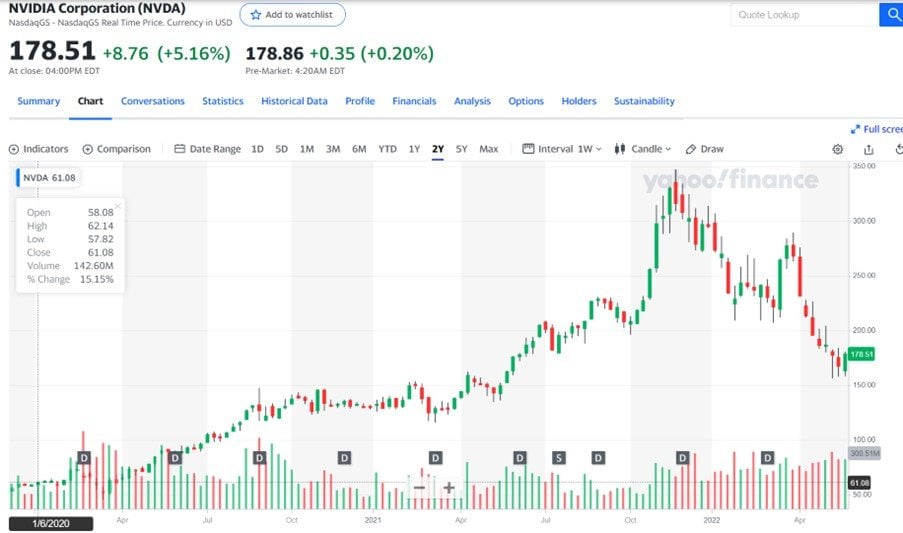

NVIDIA

Pretty much the same story for NVIDIA.

Despite a 50% plunge, it still trades at a whopping 15 times Price/Sales:

How much more do prices need to drop from here?

The thing about valuations is that they’re a blunt edged tool.

They tell you roughly where we are in the cycle, but are of little use in calling the exact inflection point to start buying.

That was when I chanced upon a beautiful piece from Zoltan Pozsar.

The famed market strategist had this to say:

At 4,000 [on the S&P500], the Fed does not seem content, and in the grand scheme of things, this is where the Fed would change its tune if it would still be writing a put.

At 3,500, we would have lost all of the post-pandemic gains in market wealth, but that level for stocks still feels like a put option, just with a lower strike price.

At 2,500, we would lose not only all of the post-pandemic gains, but would eat into some of the pre-pandemic gains too.

And if something indeed happened to the supply of labor post-pandemic (and some of that is wealth related), then to cool price pressures, maybe a pre-pandemic wealth level is appropriate indeed.

Beautiful.

What Zoltan is trying to say, is that – Since it was the COVID policy response that caused the inflation problem, the solution to inflation may be to reset to pre-COVID levels of wealth.

My own thinking is very similar.

The reason why I think 3500s is such a key level on the S&P500 (and may be a point to start buying) is because (1) it marks the pre-COVID top, while (2) also being close to a 30% decline from top.

But Zoltan goes beyond that.

He doesn’t think a return to pre-COVID levels is sufficient.

He thinks we go there, and then some more.

What if I am completely wrong? What if this is the market bottom?

The way I see it, there are 2 possibilities:

- Feds give up on fighting inflation because the pain is too much to bear – they stimulate into the recession

- Inflation subsides

Scenario 1 – Feds give up on fighting inflation (Currency Debasement)

Imagine that we are in Dec 2022.

The Fed Funds rate is at 2.5%.

By this point, the economy is already in recession (or at least a broad slowdown).

Risk assets are comfortably off their all time highs.

And yet – inflation refuses to go down.

Oil stays at $200, and global supply chains remain a total mess.

In this scenario – do the Feds (1) raise rates further, or (2) do they cut?

Does Powell (and Biden) have the stomach to persist with tight monetary policy despite a collapsing economy?

And the more I think about it, the more I think that they may cut in such a scenario.

The Feds become an Emerging Market Central Bank?

For the longtimers, there’s a touch of irony in this too.

Think back to the Asian Financial Crisis when the IMF forced Asian economies to hike interest rates despite a terrible recession, to prevent currency debasement and inflation.

Think about western economists crying blasphemy when Turkey cuts interest rates despite a plunging currency (to stimulate their economy).

Well… if the same thing ever happens to the US, I don’t think they’ll have the stomach for the pain.

They’ll just stimulate into the recession, subsidize oil and food prices, and let the rest of the world deal with the consequences.

What happens to stocks in this scenario?

This BTW – is a currency debasement scenario.

One where paper currency loses its value, relative to real goods.

Under this scenario – Stock prices will soar, but mainly because the value of paper money drops.

Strong nominal returns, but negative real returns (inflation adjusted).

Of course, under this scenario, we’re not at the bottom yet. Stocks will still need to decline further from here to trigger sufficient pain for a Fed pivot.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Just created a Discord server where I collate analyst reports and investing resources that I come across in my research. Hit us up here if you’re keen.

Scenario 2 – Inflation goes away

I know it seems ludicrous now when there’s shortage of everything from chickens to oil.

But with inflation a bit of forward thinking is required.

Supply crunch fades

Let’s say Russia-Ukraine agree on a ceasefire.

Russian oil reemerges on global markets, and oil prices plunge.

Because of base effects, inflation moderates significantly.

Markets price in a less aggressive Fed hiking cycle.

Stocks could really fly in that scenario, given the bearish positioning.

How likely is this to happen?

The problem though – how likely is this to happen?

And while this wouldn’t be my base case, I think you would be a fool to say that it’s impossible.

We live in unprecedented times, anything can happen.

Stay alive to risk, both to the upside and downside.

Demand fades

Inflation is a demand-supply problem.

If supply doesn’t ease, demand can fade.

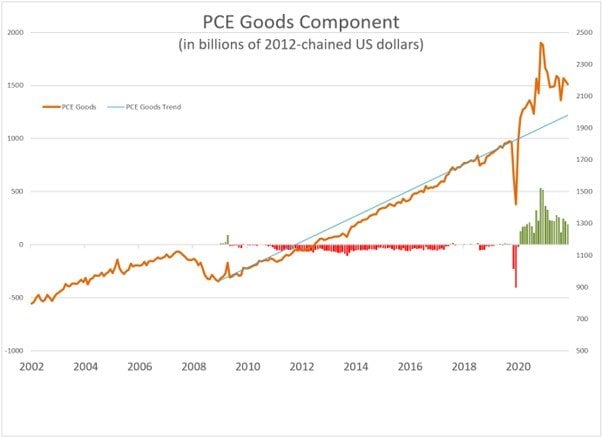

And to answer that question, I wanted to share a bunch of great charts.

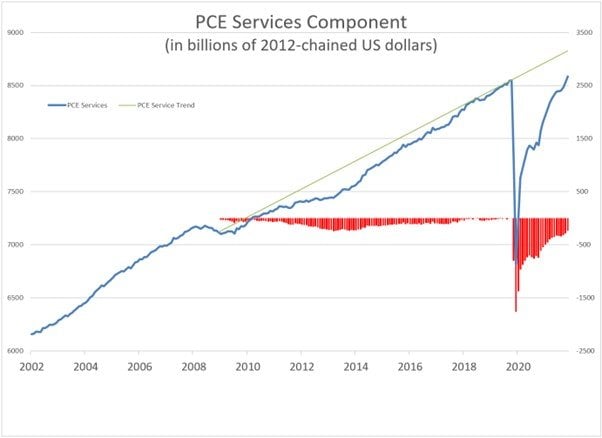

Here’s the demand for goods, vs the pre-COVID trend. Basically, demand for goods is well above pre-COVID trends.

While demand for services is well below pre-COVID trends.

Here’s the ratio of goods to services:

We need a rebalancing period

What the charts are saying, is that after COVID and all that stimulus, people had a lot of money to spend.

But they couldn’t go out right?

So all that excess money went into goods.

A new playstation, a new house, a new car.

Goods demand exploded globally.

Supply couldn’t keep up, hence inflation.

What the Feds are trying to engineer now, is a short period of rebalancing.

Demand of goods needs to go down, and more money spent on services.

And traditionally, a recession does wonders for that.

So FH… Is this the market bottom?

To sum up the discussion – valuations are of no help in calling a bottom.

Valuations have come down significantly, but it’s tough to point to that and say stocks have bottomed.

It’s too early to call for a Fed pivot, because we need more pain before that happens.

The biggest possibility, is for something to move on the inflation front. A Russia-Ukraine ceasefire could be a big black swan.

So… this is a bear market rally?

What I would say, is that if you are outright short the market, the risk-reward is less attractive than it was a few months ago.

Valuations have come down across the board, and a lot of speculative asset classes (eg. crypto) have deflated or are in the process of deflating.

There’s a good chance of a short term rally from here.

But if you are looking to go long (in a big way), I’m also not sure if this is the bottom.

Both the scenarios described above indicate that we probably need to see a bit more pain, before things get better.

Where does value lie?

That being said – I absolutely do not deny that pockets of value are starting to emerge in this market.

Long time readers know that I am a big fan of REITs, and I think REITs are getting very close to the point where I would be backing up the truck.

Big names like Mapletree Industrial Trust, Ascendas REIT, Mapletree Commercial Trust etc are trading at 5.5% yields.

I think for long term investors, that’s fantastic value.

Only reason I haven’t loaded up yet is because I’m being greedy and trying to wait for 6% yields.

But like I said – no denying that there is value in this market, if you know where to look.

US small caps have also sold off to the point where they are pricing in a very bearish outcome. There’s value there if you know where to look.

And commodity names – if you think this is going to be an inflationary decade, those guys are literally printing cash.

If you are keen, my full stock watch list (on stocks/REITs I am keen to buy) is on Patreon.

If you have deep pockets…

So that being said, and with the caveat that I personally don’t think we’ve bottomed for 2022, I think an argument could be made to start buying.

Buy small, average in, while saving enough dry powder for further declines.

This way if I am completely wrong on my macro call, at least I have positions at these prices.

If I am right, then I still have enough dry powder to average in further.

It’s risk management.

Timing the bottom is harder than you think

The reason why this helps, is that timing the bottom is a lot harder than you think.

It’s actually not the mental aspect that is hard, it’s the emotional aspect.

You know what I mean – in a bull market everyone wishes for a 10-20% pullback, so they can buy the dip in size.

And then we get a ~30% pullback in the NASDAQ, and suddenly nobody wants to buy, because “falling knife”.

Investing is funny like that.

When it’s not the time to buy, everybody wants to buy.

When it’s finally the time to buy, nobody will want to buy.

Mark my words on this.

So the benefit of averaging in now, is that if you’ve consistently bought into the market on the way down, psychologically it will not be as hard to deploy the capital when the time comes.

But of course, this requires deep pockets, and nerves of steel.

I’m not telling you to blow 80% of your dry powder on Monday’s open.

Closing Thoughts: FAANG stocks a buy?

Many of you have asked me for my views on the FAANG as a value stock.

What I will say, is that the end of every market regime is always marked by the collapse of the “former” leaders.

In the 1970s it was the nifty fifty, in the 2000s it was commodities/real estate, and so on.

And it’s clear that the defining trade of the 2010s, was tech.

And within tech, there’s nothing more emblematic than the FAANG.

The outperformance of FAANG versus the other 492 stocks in the S&P500 has fallen noticeably of late.

Will this continue going forward?

I mean I don’t know the answer to that, but this is not a trade I want to pile into at this point in the cycle.

As always, this article is written on 28 May 2022 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patreon.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 1 free Apple share (worth $230) you’re new to MooMoo and fund $2700.

Get a Free Apple stock (worth S$230) when you open a new account with Tiger Brokers and fund $2000.

Special account opening bonus for Saxo Brokers too (drop email to saxo@financialhorse.com for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

Hi, FH, great reading your sum up, what a weak of bear market rally !

I still remember the days of those young kiddos shouting SEA SEA SEA, “growth investing” during the days of covid in FB, and laughing at the ones buying singapore stocks, but guess what. it turns out SGX stocks and STI remains fairly resilent at this point of writing LOL. (Not saying it wont crash though. Those shouting growth investing (arkk names for eg.) is the best. well they have been very quiet for the past 7 or 8months.

Spore reits at current prices are attractive, and if you keep them long enough, their yields can afford inflation. ( Kep infra, Mapletree Industrial , Sasseur Reits and Capland China their yields are attractive agree ? )

Also just like your feedback what do you think of Vanguard VT index fund (60% US 40% rest of the world ) as a diversified/ passive way of investing ? DCA like monthly type of investing ? what are your thoughts ?

Well I think there are 2 ways of doing it (1) active investing, something like that is discussed in this article, and (2) passive investing, just DCA through rain and shine.

Both are perfectly acceptable, which is better will depend on the investor in question (level of knowledge, interest levels, willingness to spend time etc).

So yes – DCAing into a diversified index fund, while ignoring global macro, is perfectly acceptable if said investor decides to go with the passive route.

Nice catch on Bill Ackman, never noticed that.

I started putting in small amounts into US stocks last week, but about 25% is still in cash. If this turns out to be the bottom, I would be upset 🙂

Haha, appreciate the share!

Dear FH

Excellent analysis, completely agree on the potential scenarios and possibilities.

My observations:

1- Inflation will peak anytime now except if oil soars higher. The US driving season, China opening up and subsequent trade expansion as well as increased global mobility will keep oil high. The possibility of ceasefire is always to be factored in. If this happens, oil prices will pullback to under 90$

This will ensure the SPY is back at 4800 by year end

The fed will breathe a sigh of relief and their job is done

2- The war drags on, rest of reopening and China gets back- Oil will cross 150 and the Fed will hike and hike , the US midterm election will matter . Equities will pullback and 3400/3600 is very much on the cards

THere is no foolproof strategy to make money but discounting ceasefire and inflation peaking would mean missing out on great returns

I am buying progressively since March and will be buying both value and growth with a 2:1 ratio plus extra locally in SG. The SG banks as well as good quality REITS like ASC-R, AIMS APAC, MIT, FLCT offer value at current prices for long term investors. AT circa 5.7% or higher, these Reits offer 300 basis points higher than the prevailing 10 year SG bond yields

Positioning for both possibilities is a prudent way forward

Regards

Garudadri

Man after my own heart Garudadri! Frankly I agree with the points that you raised, and nothing further to add from me.

Please can you provide examples of value & growth?

Hi FH, there’s also scenario 3 where the Fed dosen’t move and lets inflation come down gradually, and in principle nominal growth trends around zero. Stocks could technically see a rebound as market prices in Fed rate decreases, but the market could also be volatile IF the Fed does not move for a period longer than expected. We shall see. I also agree it is too early to call a bottom, but with oil closing at 115 this week, goldilocks seems a long way from home.

True, that’s quite an interesting scenario. But agree it might be a bit too early to call how something like that would play out. I’m more inclined to the extremes – either the rising rates will break the economy, or they will not and Feds keep going.

Global market liquidity is so much higher post-Covid as compared to pre-Covid days. It may not be appropriate to use the suggested S&P 500 level if this is not adjusted for global market liquidity. Japan is still continuing with ultra-easy monetary policy, China is looking to stimulate its economy and US and Europe monetary conditions are currently far from being restrictive.

If one waits for S&P 500 level to reach a level that will eliminate post-pandemic gains in market wealth, it is likely that he/ she will greatly underestimate the strength of bullish market participants in current global market liquidity condition.

The number of high quality global stocks trading at reasonable valuations are limited and it does not take much for these stocks to start rising again in current global market liquidity condition. This is similar to Singapore property prices which continue to rise despite restrictive cooling measures and less than ideal economic conditions in an era where global market liquidity is high.