You might have missed it if you only look at the blue-chip REITs from CapitaLand, Mapletree and Frasers.

But under the surface, the smaller REITs are starting to break.

Here’s Prime REIT, down 42% from highs.

At this price, it trades at a 11.54% annualised yield, and price to book is 0.709x.

The last time Prime US REIT was this cheap?

It was March 2020, right in the depths of the COVID crisis (all time low was $0.50).

So… is Prime US REIT the buy of the year?

Or is it a value trap.

Property Portfolio of Prime US REIT

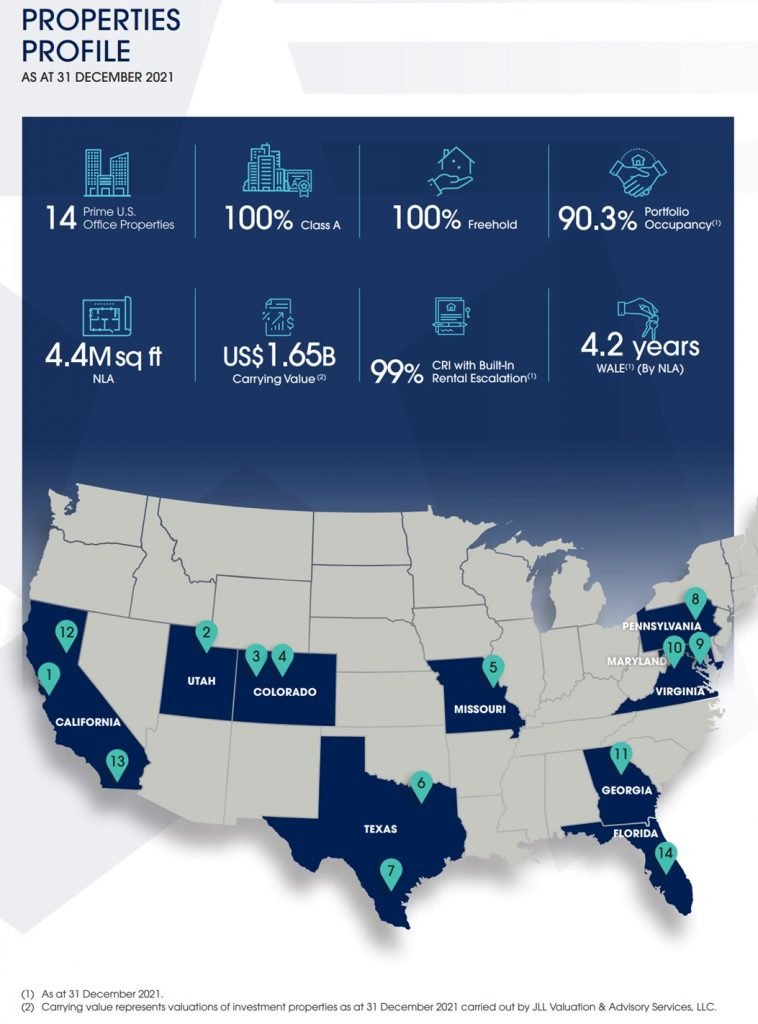

From the Annual Report: “PRIME has a portfolio comprising 14 high-quality Class A office buildings located in 13 key U.S. markets with an aggregate net lettable area (“NLA”) of 4.4 million sq ft as at 31 December 2021.”

For the record, I very rarely take long term positions in US real estate.

US real estate is a very deep and sophisticated market.

As a Singapore based investor, I don’t have the edge to compete effectively, which is why I usually don’t take long term positions.

Where I do buy REITs with US real estate (like Digital Core REIT and Keppel Pacific Oak REIT previously), I almost always just flip for capital gains when price recovers.

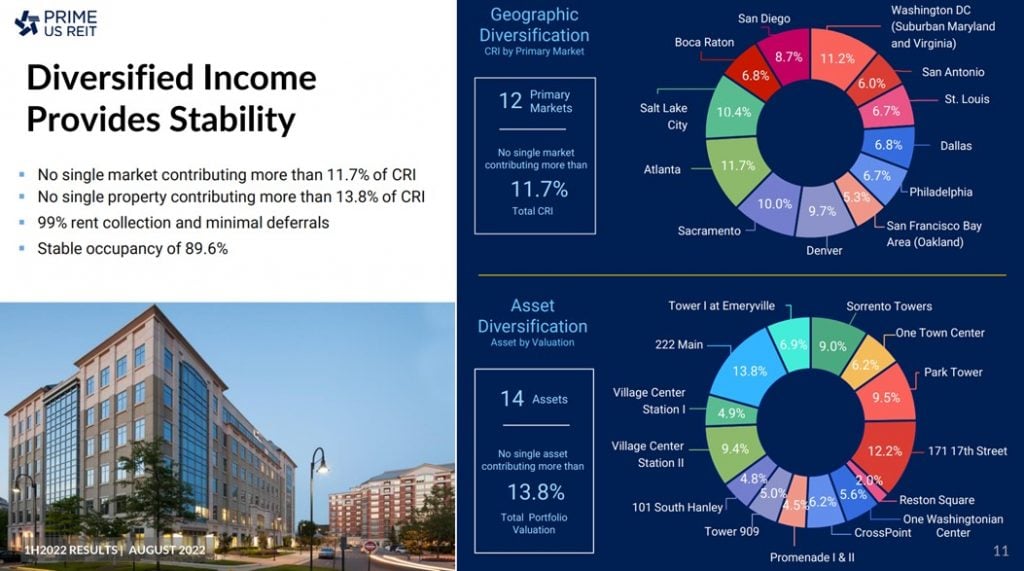

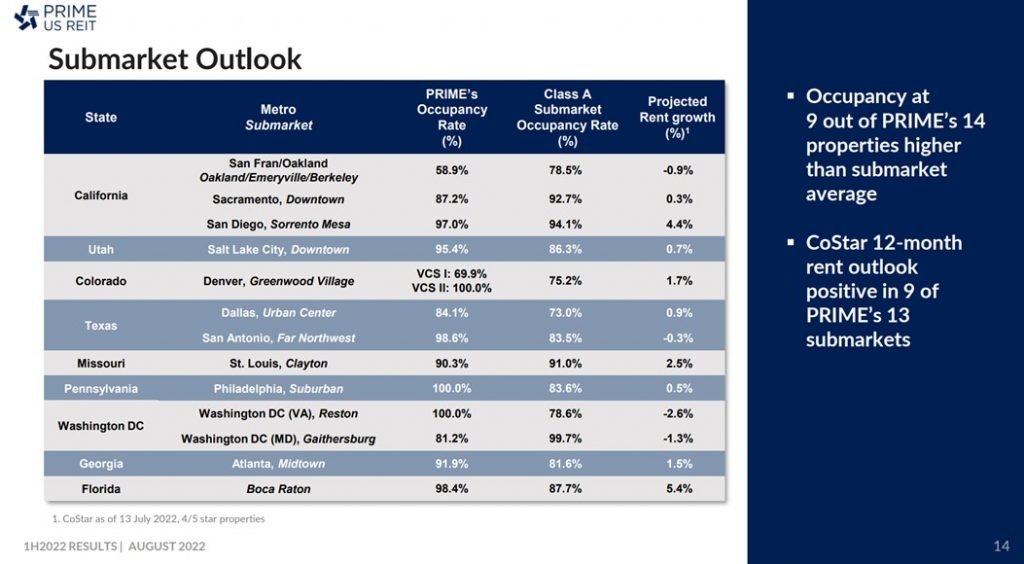

Prime US REIT’s real estate portfolio is diversified across a number of geographies, with no single market forming more than 11.7% of rental income:

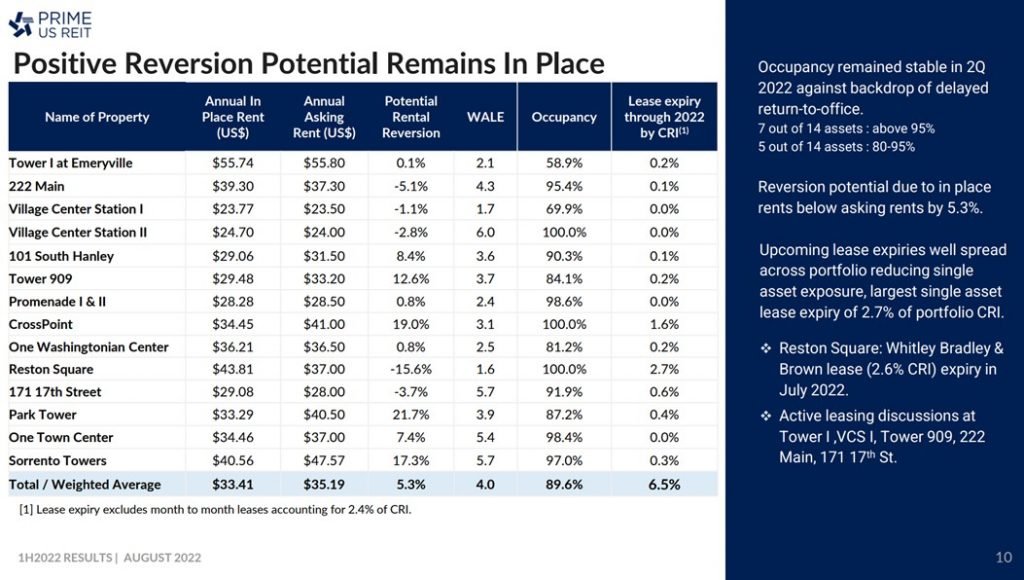

Tabletop analysis is positive, as rental reversions are doing well.

Occupancy rates for some submarkets are below market benchmarks though, indicating that these are not necessarily the best real estate around.

There’s a lot of talk about the death of the office, but so far at least, occupancy and rental reversions are holding up.

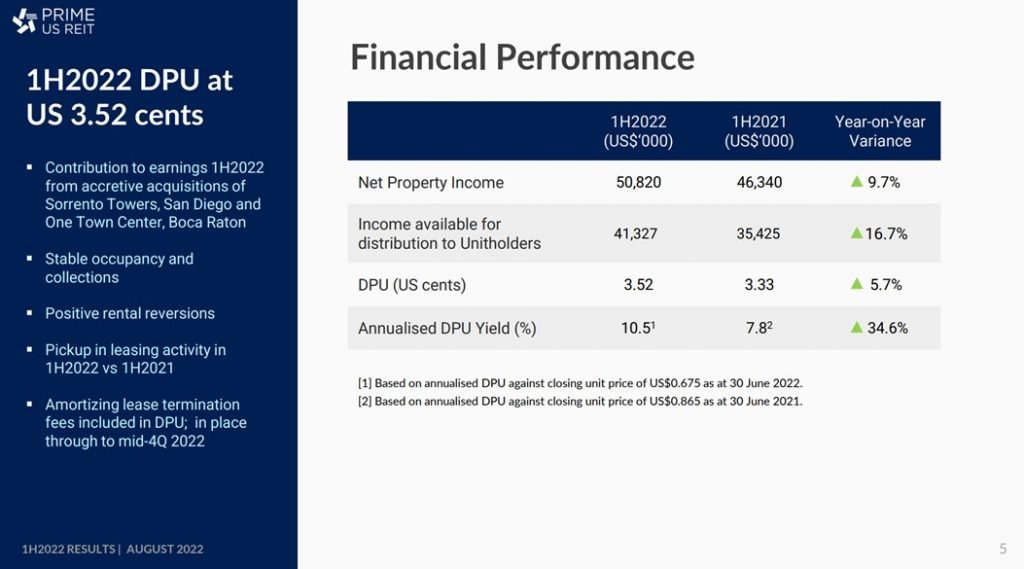

And you wouldn’t have realised it from the price, but DPU is actually up 5.7% from last year.

You can argue that’s down to inflation, but hey – growth is growth right?

Valuations of Prime US REIT

Annualised dividend yield of Prime US REIT is 11.54%

Price to Book is 0.709x.

So… the numbers look fantastic… what’s the catch?

US REITs are all trading at ridiculously cheap valuations

Now if you think this is a fantastic deal, you need to look at the other Singapore listed US REITs.

Manulife US REIT trades at a 10.6% yield, while Keppel Pacific Oak US REIT trades at a 9.6% yield.

Here’s Prime US REIT against Manulife (blue) and Keppel Pacific Oak US REIT (purple).

Prime US REIT is actually outperforming Manulife US REIT.

Why are US REITs so cheap now?

It’s never easy to answer these questions definitively.

But if you asked me, I’m going to point to the global macro condition.

US interest rates are going to be at 4% by end of the year (or early 2023).

REITs are leveraged real estate positions, and interest rates at 4% are going to crush them (from higher financing cost, higher real estate cap rates, and higher yields demanded by investors).

I wrote an article on Patreon to share deeper views on REIT valuations and at what prices I would start buying this cycle, so do check it out if you are keen.

Long story short – with the rapidly rising risk free rate, REITs need to drop quite a bit to catch up to valuations.

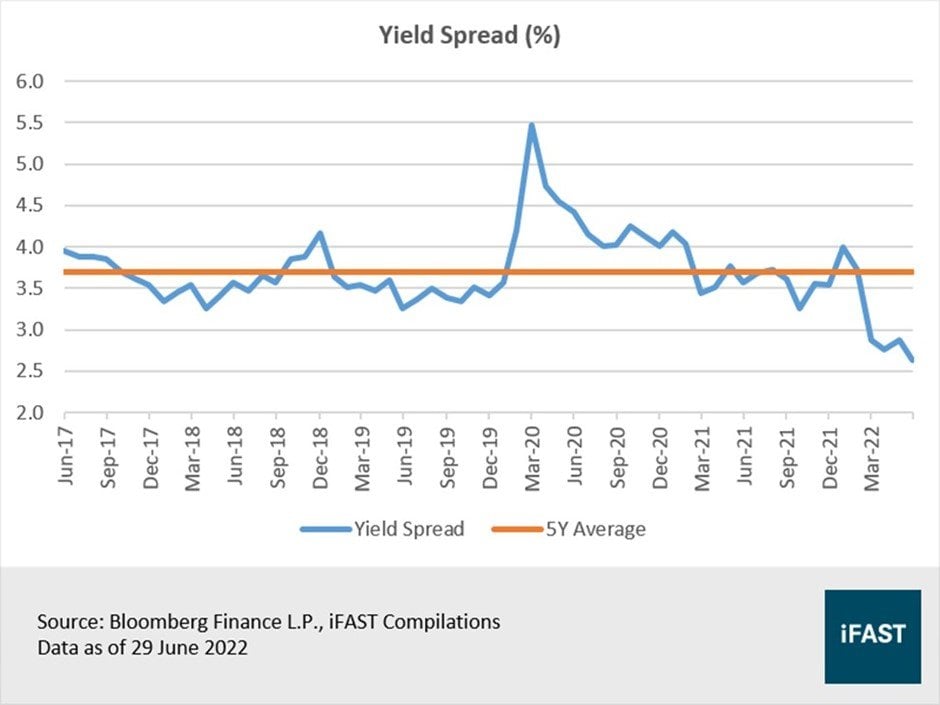

From a yield spread perspective, REITs are the most overvalued they’ve been in 5 years.

This collapse seems to have already happened for the US REITs, but *should* spread to the broader S-REIT universe in time.

But… why is Prime US REIT at an 11.5% dividend yield?

That said – the fact remains that at an 11.5% dividend yield, Prime US REIT is majorly underperforming its US REIT peers.

So you can’t just blame the macro.

Trying to answer this question led me down a very interesting rabbit hole.

And I narrowed it down to 3 reasons:

- Mapletree is selling down Prime REIT after purchase of SPH

- Track record of Sponsor is unproven

- Refinancing risk

Mapletree is selling down Prime REIT after purchase of SPH

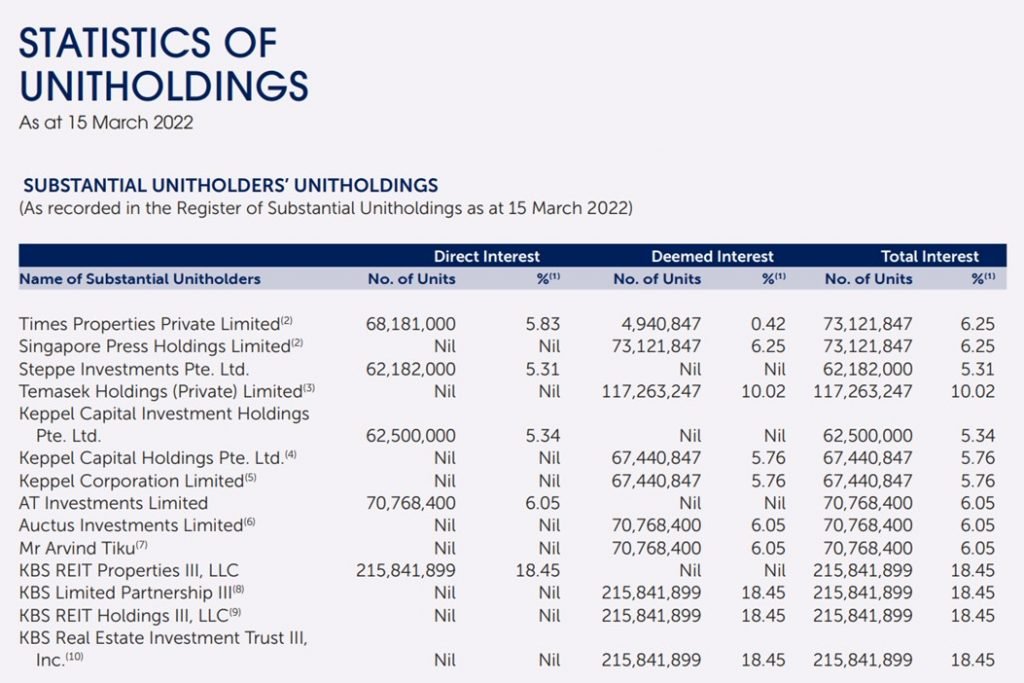

Guess who were the 3 big shareholders of Prime US REIT?

KBS (the sponsor), Keppel, and SPH.

SPH… which has now been acquired by Cuscaden Peak, a consortium made up of Hotel Properties Limited; Mapletree Investments Pte. Ltd., and CLA Real Estate Holdings Pte. Ltd

And – Mapletree has been selling.

Here’s the SGX disclosure, where Mapletree sold 3.23% of Prime US REIT in a married deal to an unnamed buyer.

![]()

Never looks good when a big unitholder is dumping their position.

For what it’s worth though, this mystery buyer bought Prime US REIT at $0.76, so hey – you can buy it much cheaper than them today.

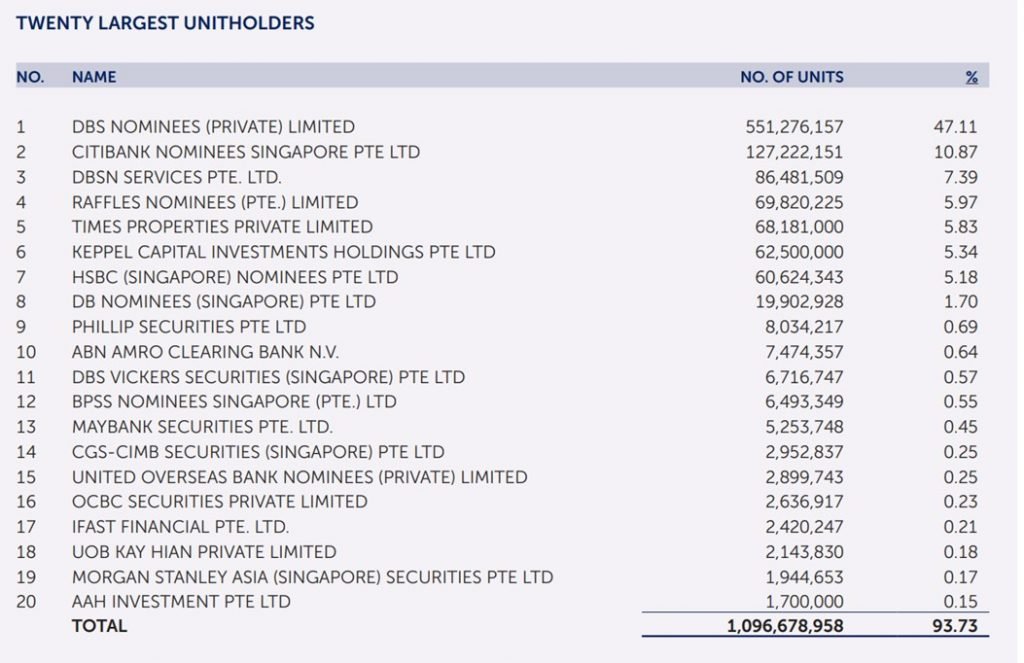

Full list of unitholders is below.

A significant portion of the REIT looks to be owned by private wealth, via the private banking arms of DBS/Citi etc.

This is usually not a good sign, because private wealth can be quite fickle.

Sometimes they also layer on leverage, so when unit price is sliding and financing costs are going up, there is a risk of them selling.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

We also share great nuggets of wisdom on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

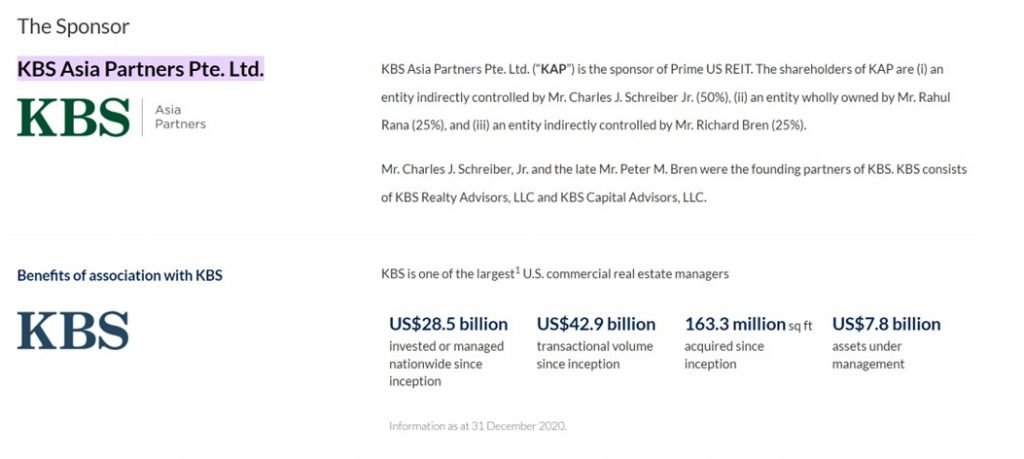

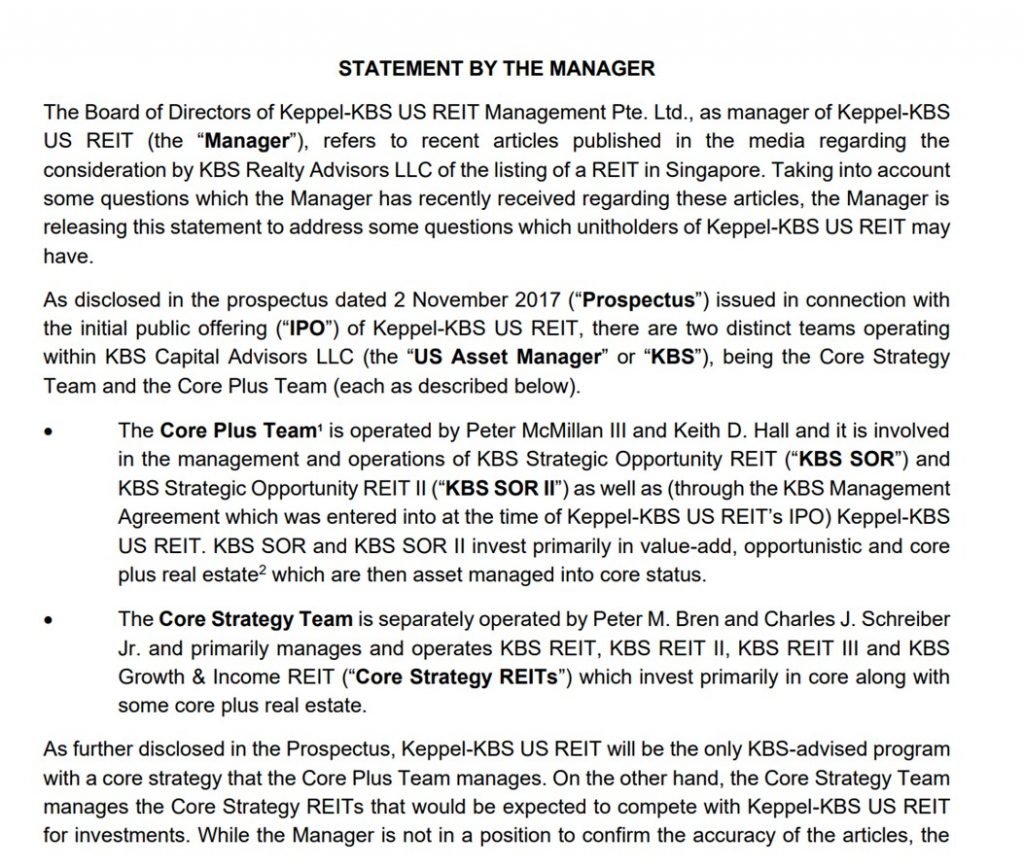

Track record of Sponsor is unproven

The Sponsor of Prime US REIT is KBS Asia Partners, which is one of the largest US commercial real estate managers.

They sponsor a number of other REITs such as KBS REIT I, II and III, but these are all unlisted US REITs.

Interestingly, KBS used to be asset manager for Keppel Pacific Oak US REIT – formerly known as Keppel KBS US REIT.

I dug around a bit on the historical SGX announcements, and it’s quite an interesting breakup in which the KBS team split into 2, and Keppel-KBS US REIT swapped to the new KBS team.

You can read the full SGX announcements here and here if you are keen.

Key takeaway for me at least – is that the track record of this sponsor is unproven.

Okay they’ve not necessarily done anything bad.

But because they dont have a very long track record in Singapore, it’s also hard to say they are of the same quality as a sponsor like CapitaLand or Mapletree.

Is there risk of insolvency for Prime US REIT?

Usually when you see a REIT trading at double digit dividend yields you’ll think there is insolvency risk.

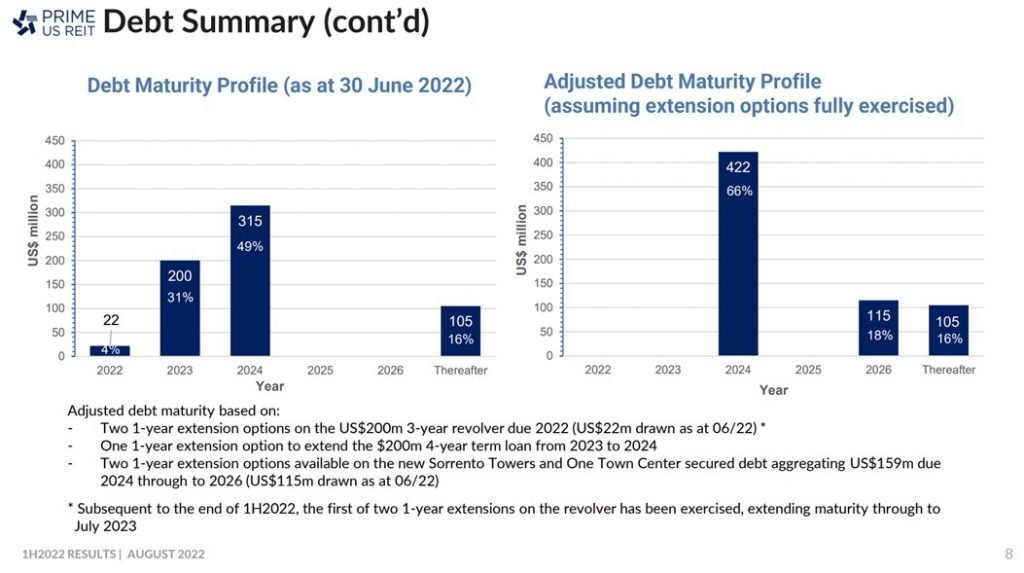

Prime US REIT’s debt maturity profile is below, and it does look slightly scary with up to 66% of debt up for refinancing by 2024.

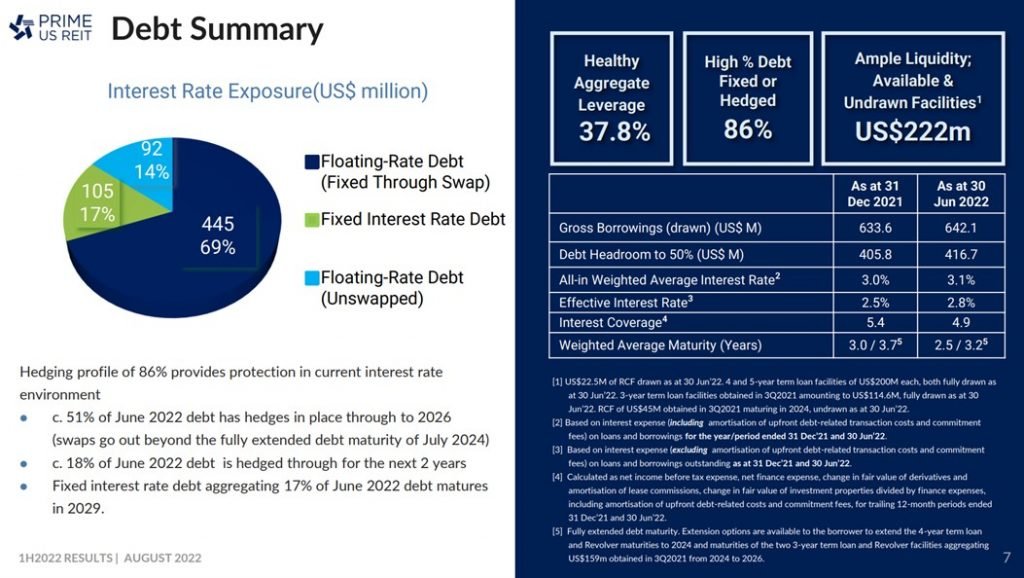

86% of their debt is fixed rate or hedged.

But as you can see from the chart above, they’re going to be refinancing almost 66% of their debt over the next 2 years, into very high interest rates.

So this is a red flag to note.

Worst case if they can’t refinance it could get ugly.

Best case if they can refinance the higher interest expense is going to weigh on DPU.

Prime US REIT pays 11.5% dividend yield – Will I buy this REIT at $0.61

Now you look at this chart of Prime US REIT, overlay it with US macro, and the 3 risk factors above.

And you tell me you can confidently call a bottom in this REIT.

If you really wanted to buy Prime US REIT, I suppose there are 2 ways to do it:

- Close your eyes and buy at a price when fundamental valuations are compelling

- Try to time it around a catalyst

Close your eyes and buy at a price when fundamental valuations are compelling

With this approach, you’re just going to buy and average in, and accept that the price may continue to slide.

But that’s okay, because you’re buying at a price that you *think* is good value.

Which begs the question – what is fair value for Prime US REIT?

If we assume a peak US 10 year rate of 4.5% this cycle (which is probably on the aggressive side).

At 11.5% dividend yield, that’s a whopping 7% yield spread against the risk-free.

You’re looking at almost junk bond levels of yield.

Is the risk here similar to or larger than that of a junk bond?

Debateable.

Try to time it around a catalyst

Alternatively, you can accept that while Prime US REIT is cheap, it can continue to get cheaper in the absence of a catalyst to drive unit price.

With this approach, you try to buy when there is an event driven catalyst to spark a recovery in price.

This could come in the form of a macro driven Fed pivot, or who knows, a sponsor driven unit buyback like what happened with Digital Core REIT.

But of course, sometimes the price just recovers because sellers stop selling, so with this approach you may miss out.

Will I buy Prime US REIT at $0.61

Right now? I don’t think so.

I’ve been saying since Jan 2022 that this is a year to respect the macro.

The time will come for fundamental stock picking. And while we are nearing it, we are not there yet.

Almost every central bank is now tightening monetary policy aggressively in response to inflation.

And with Russia cutting off European gas this week, it just looks like things may get worse in the short term.

In fact I think there is a real risk we’re moving into a sovereign debt crisis, and a possible Asian Financial Crisis 2.0.

The time will come to buy, but for interest rate sensitive plays like REITs, I still think it’s too early.

Sure, maybe $0.61 is the bottom for Prime US REIT this cycle.

And if so, I’m happy to miss that boat.

The way I see it, market is going to present more opportunities before this cycle is over, and I want to keep my capital intact for when it comes (the list of stocks / REITs I’m keen to pick up, and target prices, is available on Patreon.).

Closing Thoughts: What if Prime US REIT drops back to COVID lows of US$0.50?

At $0.50, Prime US REIT will pay a ridiculous 14% yield.

Even if you adjust for higher financing costs, it’s still a double digit yield.

Okay in that case barring any changes in the global macro, maybe I could be tempted.

But I don’t think Prime US REIT goes there without a significant deterioration in the global macro condition (or developments at the REIT level).

If that happens, other bargains are going to open up elsewhere in the market.

So it would be wise to weigh risk-reward against other options available.

In any case, you can see my list of stocks / REITs I’m keen to pick up, at what prices, on Patreon.

Love to hear what you think!

Refinancing tool

With rapidly rising interest rates – it might pay off to look into refinancing if your loan is coming due.

There’s a fantastic tool by Property Guru.

Do give it a try if you’re close to refinancing.

It’s completely free – you just input your mortgage details, and the tool lets you know whether you’ll save money by refinancing.

If the answer is yes, they’ll give you recommendations on what loan to take.

If the answer is no, you can set up a reminder for the tool to remind you when its time to refinance.

I did the same for my own mortgages and found it pretty useful.

Do give it a try here.

As always, this article is written on 10 Sep 2022 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon. You can access my full personal portfolio to check out how I am positioned for the coming downturn too.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 100 USD in Apple Shares with Webull, a zero commission broker.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

Hi FH, actually most reits (except parkway life or Frasers L&C) are about at least 30% lower of their peak high. If go for bargain buys, I will rather go for those with stronger backers, eg Keppel Pacific Reit.

My question is can we use reference to their private placement/ preferential offering prices issued in past 1 or 2 years to understand their valuations? For eg, MCT previously issued offering at 2.24/2.01 or Ascendas Reit at 2.96/2.63, or recent Ascott Trust’s 1.11. Prime’s last offering was 81 cents back in June 21, with current price about 25% lower.

Okay, might see if I can cover some of those you mentioned in other articles going forward.

My simple view is that they are useful as a reference point, but don’t read too much into it. These valuations were done in a very different macro climate, with very different interest rates / inflation situations. We look to be moving into a new paradigm of higher rates sticky inflation, so historical valuations may not be so useful in this climate.

Hi FH,

Your point on Reits being most over valued in 5 years based on yield spread is sobering. Would you consider simply selling off your existing Reits and buying back later?

Hi CMC,

No, the REIT positions that I was trading have all been sold by Jan 2022. Whatever I am still holding are core long term positions, that I do not intend to trade. But I will add when I find valuations sufficiently attractive.

Hi FH,

Some things about REITs that I find odd, hope u can enlighten me.

1. Why are Reit spreads so tight? Eg. Parkway Life yield is same as SGS bill. Investors are not pricing in equity risk.

2. Reit dividends during recessions – so they cut, by how much? In past 2 years alone, blue chip Reit dividends have fluctuated quite a bit.

3. Equity risk premium. After 2 years of observation, I still cannot tell whether Reits have market beta of 1 or benefit from flight to safety.

Hi Hungry Hippo,

Those are great questions, which I do not have ready answers to.

For what it’s worth, some personal thoughts from me:

1. Ultimately, price is driven by what a seller is willing to sell at vs what a buyer is willing to buy at. And sometimes, price doesn’t move because nobody is selling. Could be as simple as that sometimes. Of course, the question is whether that will change in time…

2. No easy answer to this – depends on the nature of the recession. COVID was quite a unique one and should not be used as a benchmark, because governments basically forced the economy to shutdown, and paid out monies to mitigate the effects. That said, the recession we are going to looks to be an inflationary recession, which again is quite different from what we saw the past few decades.

3. They most definitely do not benefit from flight to safety. Beta will depend on the REIT in question – CICT and Prime REIT have very different betas. Personally I find fixed income as the best proxy to understand how REIT prices will trade in the short term, although this will change in time with inflation.

Problem with US Reits is they are very volatile, both the share price and currency conversion. I have Manulife acquired at 0.55 which I tot it was a steal when it dropped from >0.6 within a month…but it went to as low as 0.48 in another month or so…that’s more than 10% dropped which cancelled out the annual div that I may have received….so I am not as comfortable in holding more versus local Reits…I guess the key word is diversification…for same budget….instead of 100% into Manulife…I will split my funds 50% Manulife and 50% Prime :p

Haha get what you mean. Personally I’m probably skipping this trade with the US REITs for now. Will wait for better opportunities to emerge. And if they don’t, happy to miss this boat. 😉

At a yield of 11%, and with 86% debt maturing in 2024, I can see how the market has priced this. They have either priced it on insolvency or signficant rental destruction. Insolvency would be unlikely – interest coverage ratio is roughly at 5 which is fairly healthy. I am not sure what are the circumstances where they default on their debt. However, I do think the management team, having so much experience must have that figured out.

Think the real fear is if there a recession. Commercial rental falls out of favour as cost cutting comes back to the forefront and companies instead cut unnecessary expenses like large office space. This deteriorates DPU and could be dangerous.

Admittedly, at a PB of 0.7, even if they were to sell everything at a 10-15% haircut to book value, investors would still come out on top.

Have to say that other American REITS like Eagle Hospitality have scarred me though.

Thanks, appreciate the sharing!

“But I don’t think Prime US REIT goes there without a significant deterioration in the global macro condition (or developments at the REIT level).”

Are you sufficiently tempted yet at 15-16%pa

To be very honest – not really. I just dont know enough about the property portfolio and sponsor quality to pull the trigger on a large investment.

Would rather put my money on investments that I am more familiar with – especially give the number of opportunities out there at the moment.