The recent Budget 2018 was a momentous one for REIT ETFs, as it accorded tax transparency status for REIT ETFs from 1 July 2018.

Before this change, REIT ETFs receiving distributions from a Singapore listed REIT with Singapore properties would be subject to a 17% income tax. This meant that an average dividend yield of about 5.8% was reduced to 4+ %, basically destroying the ETF as an effective investment vehicle.

Given that this major regulatory hurdle has been removed, are REIT ETFs now a viable option to invest in S-REITs?

[Note: 05 March 2018] This article was amended on 5 March 2018 pursuant to feedback from Nikko AM in relation to the method by which their ETF handles rights issues.

Basics: REIT ETF

A REIT ETF tracks a REIT Index by buying a basket of REITs, packaging it into an open ended fund structure, and listing it on the SGX. An open-end fund allows the fund manager to sell additional units if required, and allows investors to redeem their units directly with the fund.

There are currently 3 REIT ETFs in Singapore:

- Phillip SGX APAC Dividend Leaders REIT ETF

- LION-PHILLIP S-REIT ETF (Lion REIT ETF)

- NikkoAM-StraitsTrading Asia ex Japan REIT ETF (Nikko REIT ETF)

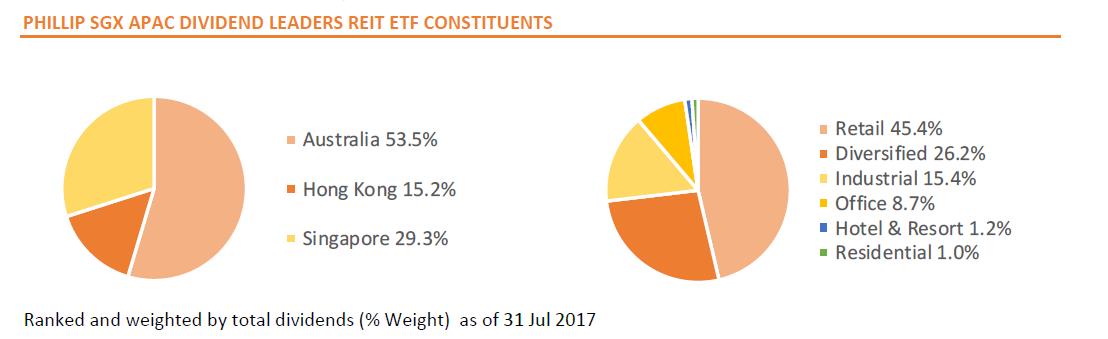

The Phillip SGX APAC Dividend Leaders REIT ETF has a combined 68% allocation to Australian and Hong Kong properties, to the point where Singapore is an afterthought. When picking a S-REIT ETF, I prefer that a larger portion of its assets are Singapore based. Accordingly, in this article, I will focus on Lion REIT ETF and Nikko REIT ETF.

Source: Phillips SGX APAC Dividend Leaders REIT ETF Fact Sheet

- Historical Performance

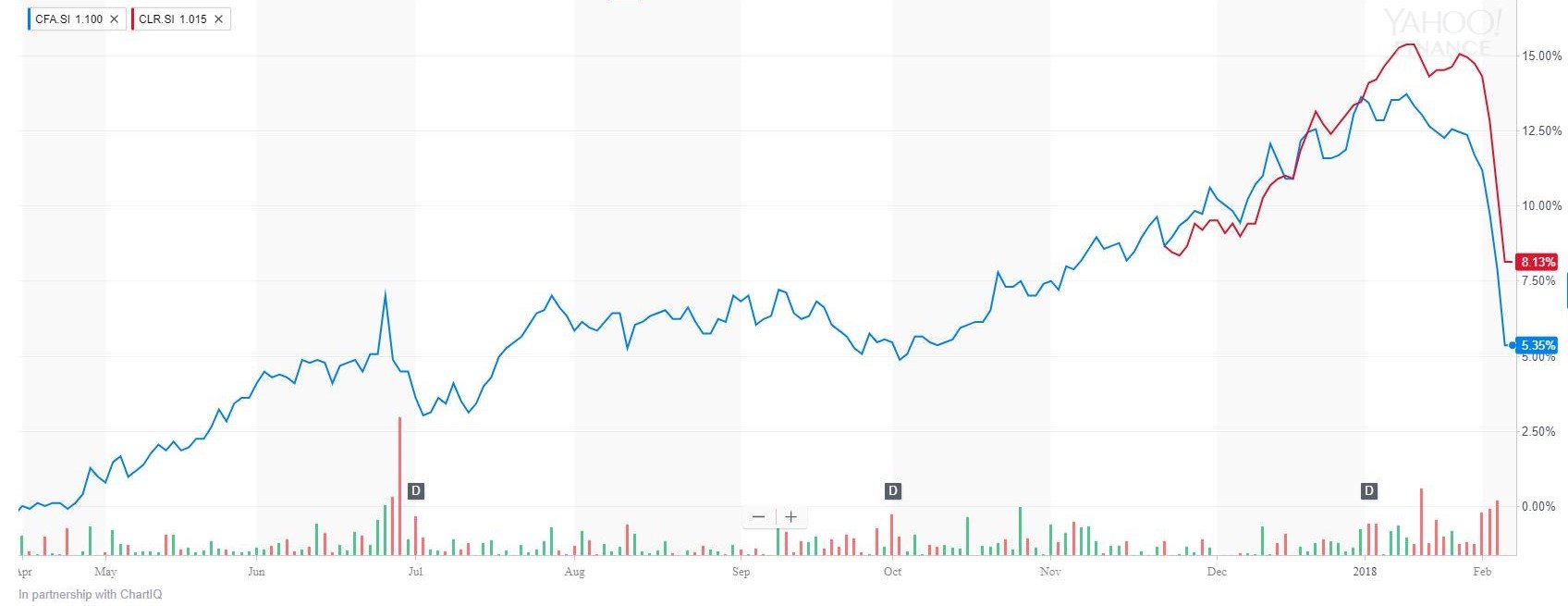

The historical performance of the Nikko REIT ETF and Lion REIT ETF are plotted below. Both were listed only last year, so there isn’t much of a track record to look at. The market is also a correction mode for REITs, given the fears over inflation and rising interest rates. Putting all these aside, as at 25 February 2018, Nikko REIT ETF’s 1 year performance is approximately 6.1% (capital gains), and an approximately 4 – 4.5% gain from distributions. This works out to a cumulative gain of more than 10%, not too shabby indeed!

Source: Yahoo Finance (Blue is Nikko REIT ETF, Red is Lion REIT ETF)

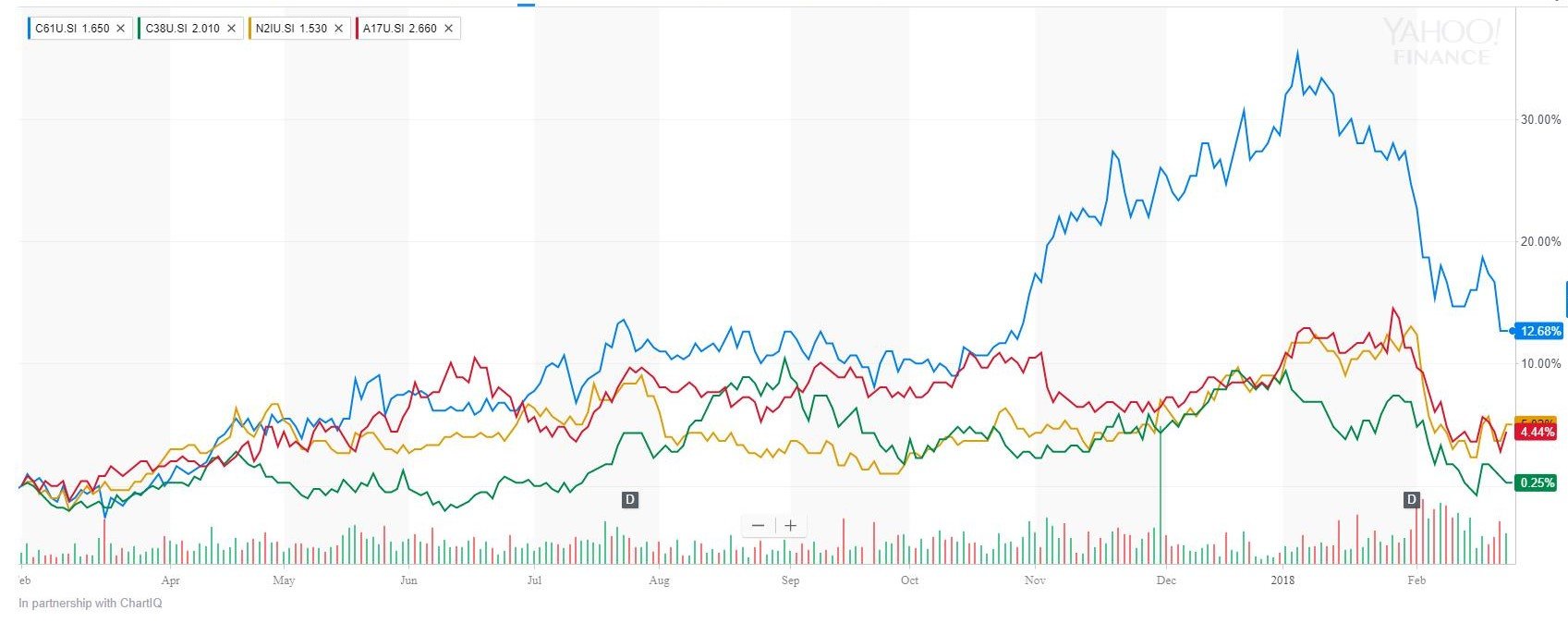

By contrast, had one done a broad, DIY REIT portfolio with equal weighting of CapitaLand Commercial Trust (CCT), CapitaLand Mall Trust (CMT), Mapletree Commercial Trust (MCT) and Ascendas REIT, the capital gain would have been an approximate 5.4%, with a yield of about 5.8%. This works out to an approximately 11% yield, which actually matches the performance of Nikko REIT ETF quite closely. This really surprised me, given that the Nikko REIT ETF pays an additional 17% corporate tax on their distributions. Perhaps the smaller REITs in Nikko REIT ETF’s portfolio boasted the overall performance of the ETF.

Source: Yahoo Finance (Blue is CCT, Orange is MCT, Red is Ascendas REIT, Green is CMT)

- Diversification

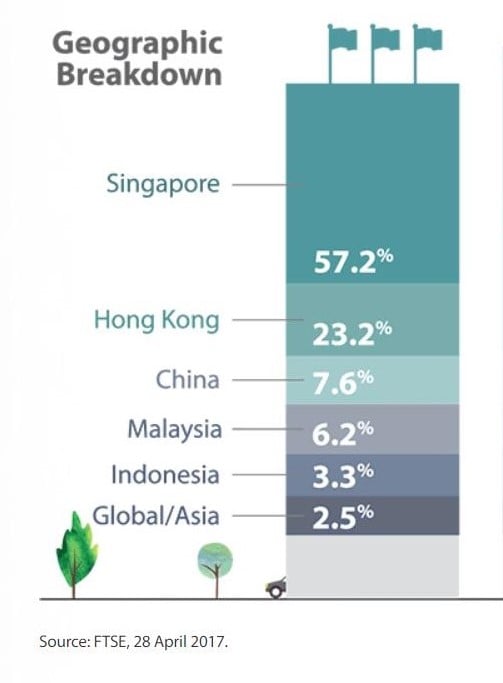

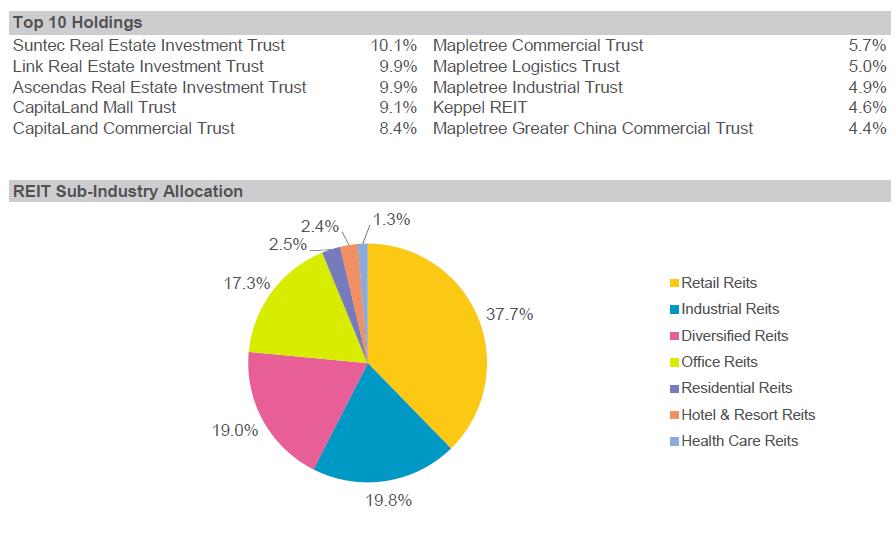

Nikko AM tracks the FTSE EPRA/NAREIT Asia ex Japan Net Total Return REIT Index. Its geographic breakdown is decent with more than 50% of its assets located in Singapore (to be expected if I am buying a S-REIT ETF), yet small enough to provide some diversification. Although there is a slight bent towards retail industry, the top 10 holdings and industry allocation are both decently diversified, and broadly track what I would do were I to create a REIT portfolio for myself. I am not a huge fan of the fact that the number 1 and number 2 REITs are Suntec REIT and Link REIT respectively, but this is not a deal-breaker for me.

Source: Nikko REIT ETF’s website

Source: Nikko REIT ETF Fact Sheet

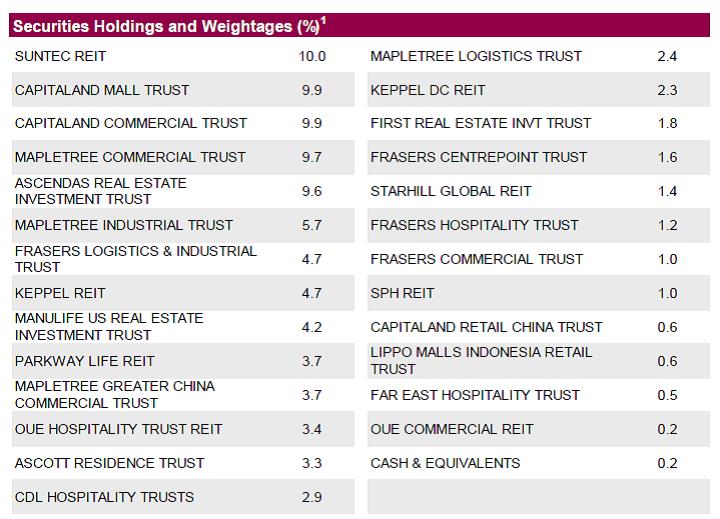

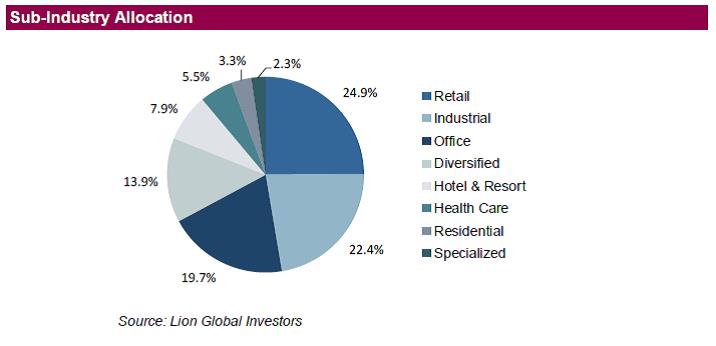

Lion REIT ETF tracks the Morningstar® Singapore REIT Yield Focus Index, which only includes REITs listed on the SGX (ie. S-REITs only). I personally like the allocation of Lion REIT ETF more than Nikko REIT ETF, as the industry allocation is well diversified, and it excludes HK listed REITs such as Link REIT.

Source: Lion REIT ETF Fact Sheet

With both REIT ETFs, assuming tax transparency status (which kicks in after 1 July), you are looking at about 5.5 – 6% trailing 12 month yield, before deducting management fees.

- Management Fees

You can take a look at the whole slew of charges levied on the ETF below, which works out to be approximately 0.60% per annum annualised, for both ETFs. This is really high for me, for a passive ETF that tracks an index and does semi-annual rebalancing. By contrast, the 2 most popular S&P500 indexes, the SPDR S&P 500 ETF (SPY) charges an expense ratio of 0.1%, while Vanguard’s S&P 500 ETF charges an even lower 0.05%.

Payable by the Fund from invested proceeds

The Fund will have to pay the following fees and charges to the Manager, Trustee and other parties:

Management Fee Current: 0.50% per annum of the Deposited Property; Maximum: 0.70% per annum of the Deposited Property.

Trustee Fee Current: up to 0.04% per annum of the Deposited Property; Maximum: 0.05% per annum of the Deposited Property. Subject to a minimum fee of S$15,000 per annum.

Custodian fee The custodian fee payable is subject to agreement between the Manager and the Custodian and may amount to or exceed 0.10% per annum depending on, amongst others, the size of the Fund and the number of transactions carried out.

Administration fee Current: 0.04% per annum of the Deposited Property; Maximum: 0.05% per annum of the Deposited Property. Subject to a minimum fee of S$15,000 per annum.

Other Fees and Charges Other fees and charges, including inter alia registrar fees may each amount to or exceed 0.10% per annum, depending on the proportion that each fee or charge bears to the Deposited Property.

The Manager intends to cap the total expense ratio of the Fund at 0.60% per annum of the Deposited Property. Any fees and expenses that are payable by the Fund and are in excess of 0.60% per annum of the Deposited Property will be borne by the Manager and not the Fund.

(Source: Nikko REIT ETF Product Highlight Sheet )

0.60% per annum works out to S$600 dollars a year on a S$100,000 investment. Given a rough yield of about 5.8%, that reduces your yearly S$5,800 distribution to S$5,200. On a 10 year timeline, this is S$6,000 alone before accounting for compounding effects. This may be justified if the fund manager were involved in active management by trading position in REITs to outperform the index. But given that the ETF invests broadly in a basket of REITs with semi-annual rebalancing and the occasional subscription for a rights issue, I find it hard to justify paying such a high fee.

Bear in mind that these fees are in addition to the fees charged by the REIT Manager. By investing in a REIT ETF, you not only have to pay fees to the REIT Manager, Property Manager and trustee at the REIT level, but also to the fund manager and the trustee again at the ETF level. This seems unnecessary to me.

- Rights Issue

As any seasoned REIT investor will know, rights issues and preferential offerings are a key part of long term REIT investing. REITs have to pay out more than 90% of their distributable income, leaving them with little to no cash on their balance sheet. Coupled with their statutory 45% gearing limit, REITs will typically need to draw on funds from their unitholders to acquire a new asset. The rights issues/preferential offerings are usually priced at a discount to market price, and it is crucial as a REIT investor to subscribe for your allotted units to prevent dilution, and apply for excess units if possible to further reduce your cost base.

There is a lot of misinformation online about how the ETF will handle a rights issue. To resolve this, I emailed the hotline on this issue, and here is their response reproduced in verbatim:

“Dear Sir

Thank you for your interest in our ETF, NikkoAM-StraitsTrading Asia ex Japan REIT ETF.

In the event of a rights issue by any of the component stock, the ETF will subscribe to the rights issue so as to align the weight of the affected component stock to that of the Index. The ETF will not subscribe for any excess rights shares.”

Which of course, is a fantastic position. The next question then, is where does the ETF get their funds to subscribe for the rights issue? I emailed them to this effect, but unfortunately it has been radio silence since.

Reasoning from first principles, the fund does not have much cash on their balance sheet, given that it distributes all the distributions received from the underlying REITs. There are 2 possible ways to fund this subscription:

1. The ETF uses the cash that it has received from distribution, to subscribe for a rights issue. This however, would affect the distribution that you receive from the ETF for the quarter.

2. The fund manager injects their own capital, in exchange for units, to subscribe for the rights issue. However, this seems awfully generous of the fund manager. Depending on the method of valuation however, it could potentially lead to abuse by the fund manager, to the detriment of unitholders (I assume also that further charges would be levied).

Another problem is that all of this is ultimately discretionary by the fund manager. Despite this clear response from their hotline, I trawled through their prospectus, website and other legal documents, but there is no mention of this policy anywhere. As a result, the fund manager is technically not legally bound to comply with this policy, although it seems that they will strive to do so.

One potential problem I can see is in a repeat of the 2008 style financial crisis, many REIT prices would have plunged and face trouble refinancing, and many will require capital injection through rights issues/preferential offering to stay solvent. In such a situation, where a majority of the REITs in the ETF are doing equity fundraising simultaneously, the fund manager may lack sufficient funds, and decline to subscribe. Depending on the discount rate priced into the offerings, this could result in massive dilution for unitholders. Of course, the flip side of this argument is that if investors are to hold the REITs individually, they may not have sufficient cash on hand to subscribe for all the rights issue too. However, even in such a scenario, I would prefer to have that decision left to me, as it allows me to decide on which REIT to allocate my limited funds to.

For this reason, I am slightly wary of REIT ETFs as a long term, multi decade investments where black swan events such as a financial crisis are an absolute certainty.

[EDIT (05 March 2018)]

NikkoAM has reached out to me with the following response, reproduced in verbatim:

“The portfolio manager of the ETF will adjust the portfolio of the ETF accordingly to raise the necessary cash and subscribe to the rights to achieve a final outcome that matches as closely to the prevailing weightages of the underlying index constituents.

Once an index constituent does a rights issue, its weight in the benchmark will increase as its market cap rises with more shares. Hence, the weightages of the other index constituents will fall and the portfolio manager will have to sell these other index constituents to align their weights accordingly. The proceeds will then be used to subscribe to the rights issue.”

This means that when there is a rights issue, the ETF will continue to track the index, which for Nikko REIT ETF is the FTSE EPRA/NAREIT Asia ex Japan Net Total Return REIT Index (part of the FTSE EPRA/NAREIT Global Real Estate Index Series). I took a look at how the index, which is administered by FTSE Russell, handles rights issues (available here and here) – which are actually pretty arcane.

Essentially, the FTSE index will always try to subscribe to a rights issue where it is priced at a discount to market price, with special rules if an issue is particularly dilutive for a constituent REIT. However, the rules are not conclusive, and FTSE Russell retains the discretion to deviate from the rules that are set.

This is troubling in a different way from the 2 options highlighted above, as it hints at a pseudo active management. This would work fine in normal trading conditions, but could be problematic in a financial crisis style situation where REITs are on firesale.

Assume for example, a repeat of the 2008 Lehman crisis. REIT A is unable to refinance and does a rights issue at a 30% discount to market price. The fund manager would have to sell its stake in other REITs, which could well be trading at a 50% discount to book value, in order to subscribe for the rights issue. The difficulty in deciding which REIT to sell, and which rights issue to take up, is compounded by the number of REITs held by the ETF. Given the comparatively low fees charged by the ETF (when compared with actively managed funds), the fund manager will simply track the rules set by FTSE Russell, and it is not exactly clear as to how FTSE Russell will apply these rules. Given the prevalence of rights issues/preferential offerings by REITs, this is a very real problem when financial conditions tighten.

Given these problems, an investment in a REIT ETF would require an implicit faith in the index administrator to make the right decisions or apply the rules in a prudent manner with respect to portfolio rebalancing. For me personally, I continue to favour and advocate owing the underlying REITs directly, such that an investor retains the flexibility to make the decision himself, based on his financial condition and goals. I would prefer to have more time to observe the performance of the REIT ETF in various financial conditions, before committing capital to it.

- Trading Liquidity

The assets under management (AUM) for Nikko REIT ETF and Lion REIT ETF is about S$100 million and S$122 million respectively. The average daily trading volume is about 250,000 units and 350,000 units respectively. As comparison, CapitaLand Mall Trust has a S$7 billion market cap, with average daily trading volume of 13.2 million units, while CapitaLand Commercial Trust has a S$6.1 billion market cap, and average daily trading volume of 13.6 million units.

The point is clear, trading liquidity for the REIT ETFs is not good, especially when compared to a direct investment in one of the underlying blue chip REITs. In a crisis style situation where investors are rushing for the exit, you may not be able to sell your units at a good price. This is especially pertinent if you are looking to trade REITs through an ETF.

You can always look to the fund manager to redeem your units, subject to a minimum of 50,000 units. The fund manager will instruct the trustee to sell an amount of the underlying REITs to redeem your units at NAV, with all expenses in relation to the selling of such units will be deducted from your amount. Unfortunately, the calculation of NAV for redemption purposes is:

“based on forward pricing which means that the Redemption Value of the Units shall not be ascertainable at the time of application to redeem Units”.

(Source: Lion REIT ETF Prospectus)

This results in a small timing risk, as you will not know the final NAV at the point when you submit your redemption request. This will be based on the NAV after close of trading (if you submitted your request on time), or if you did not submit it before 12 noon (for Nikko REIT ETF), the NAV after close of trading on the next business day. Going back to the 2008 style financial crisis, assume that you submit a redemption request at 1pm on 2 January, when the markets are in panic and freefall. On 3 January, the market gaps down, and by close of trading, the market price and NAV of the ETF could already be 20% below the point when you submitted your redemption request. Hence you lost 20% on your redemption price simply due to this timing risk. Accordingly, I do foresee problems exercising the redemption application when financial markets are in distress, due to this uncertainty over redemption price, which is precisely the time I would need to exercise it. As the recent VIX ETF unwinding has illustrated, these are very real risks (https://www.barrons.com/articles/a-violent-unwinding-volatility-spikes-kills-one-etn-1517931789).

Your best bet to exit the ETF in such distressed situations is to sell on the open market, which may be hard due to lack of liquidity.

Alternatives

What then, are the alternatives to a REIT ETF? Simply put, it is to create your own DIY REIT ETF, diversified across industries, and picking only blue chip REITs. I have a separate article on this here, but broadly, one can just buy portfolio consisting of (equal weighting):

| REIT | Industry Allocation |

| CapitaLand Commercial Trust

|

Commercial |

| CapitaLand Mall Trust

|

Retail |

| Mapletree Commercial Trust

|

Retail / Commercial |

| Ascendas REIT

|

Industrial |

| Ascott REIT

|

Hospitality |

This would actually provide a good amount of diversification across industries, while sticking only to blue chip REITs sponsored REITs that are implicitly backed by the Singapore government (Temasek links). This should have less volatility than a REIT ETF given the larger liquidity for the REITs selected and the preference for blue chips, as well as a healthy distribution yield of approximately 5.5 – 6% (using current figures).

Closing thoughts

With the granting of tax transparency to REIT ETFs, I can now see a place for them in the portfolio of an investor who has no interest in monitoring his portfolio or keeping track of rights issues, and who wants to leave the management to someone else. You get great diversification, a very decent distribution, and exposure to the real estate asset class, in exchange for a relatively handsome management fee.

For enterprising investors who know what they are doing and however, I do not see the REIT ETF as very attractive. The management fee rate is preposterous when it can be easily replicated through a bit of hard work, and the handling of rights issues/preferential offerings is potentially problematic, especially when coupled with the lack of liquidity. For these reasons, I do not see myself investing in a REIT ETF in the near future, unless of course (1) AUM and trading liquidity improves drastically and (2) the fund manager definitively addresses and commits themselves to a position regarding rights issues/preferential offerings.

You can consider a direct investment in the REITs instead. Financial Horse is a great fan of Mapletree Commercial Trust, read more here.

[Afternote]

Following this article, I have spoken to a number of industry players who have also highlighted that REIT ETFs are highly relevant for REIT professionals such as lawyers and accountants who are unable to purchase stakes in the underlying REITs due to the possession (or presumption) of inside information.

This is a very real problem for many people out there, and I do agree that the REIT ETFs will be a godsend for such professionals, as it opens up a new avenue to invest in a high yielding asset class.

Enjoyed this article? Like our Facebook Page for more great articles!

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. I share this with all my email subscribers at absolutely no cost. Sign up for the newsletter now!

[mc4wp_form id=”173″]

Following this article, I have spoken to a number of industry players who have also highlighted that REIT ETFs are highly relevant for REIT professionals such as lawyers and accountants who are unable to purchase stakes in the underlying REITs due to the possession (or presumption) of inside information.

This is a very real problem for many people out there, and for them I do agree that the REIT ETFs will be a godsend, as it opens up a new avenue to invest in an alternative, high yielding asset class.

The general worry in the article for REIT ETFs regarding the right issue or a financial crisis/bear market is irrelevant if you have a long term investment horizon which should be the case if you are planning to invest in such product.

Also, in case of a sell-off due to a right issue and/or market condition it is not the time to sell but to buy.

Finally, REIT ETFS provide better diversification than investing directly in one REIT.

My two cents.

I think it depends on what the alternative is. If like you mentioned, the alternative is to invest in one REIT, then definitely do an ETF. But it is quite straightforward to assemble a portfolio of 5 REITs diversified across asset classes, that provides fantastic diversification, better control over the securities, and far less expense costs.

Thanks for sharing your thoughts 🙂

This may be irrelevant but what are your thoughts on Vanguard REIT ETF? I feel that it’s a fantastic exposure to the US REIT markets

I don’t like them because of the 30% withholding tax on dividends, which to me would effectively kill the effective returns. Better to buy the REITs listed on the SGX directly, for a more tax efficient structure.

Although that said if you are truly keen on getting broad US REIT exposure, it’s probably the cheapest way.

Cheers!

[…] REIT ETFs: 5 Reasons I am still not a fan after Budget 2018. Financial Horse – February 25, 2018. https://financialhorse.com/reit-etf/. […]

Any idea how is right issues handled for REITS RSP?

For RSP you will still need to decide whether to take up the additional units as a unitholder. 🙂

[…] believe that financialhorse has previously covered this topic pretty well in this article. The gist, if I may summarise from the reply he has gotten from Nikko AM REIT ETF is that the […]