Quite a few of you have reached out to ask for my views on REITs, and whether I would start buying.

At the same time, those with access to my personal portfolio (the $40 tier) will know that I started to take profits in my DBS and UOB positions last week.

So I wanted to use this article to share my thoughts.

Let’s start with REITs.

REITs at 6% yields – Will I start buying?

Blue Chip REITs are approaching 6% yields

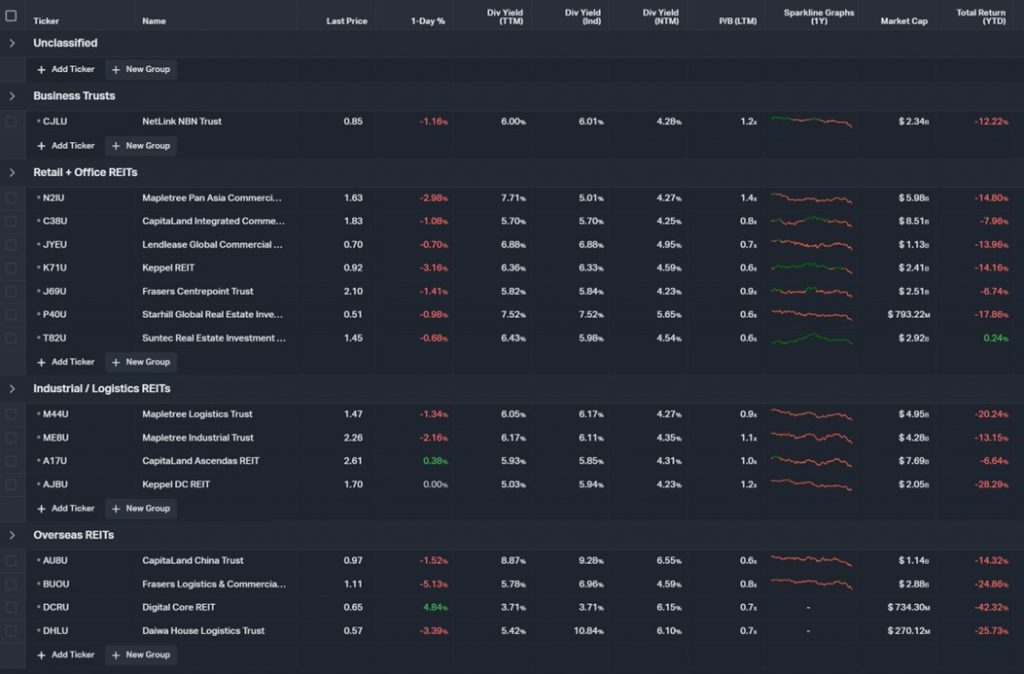

You can see the main REITs that I track below (with trailing twelve-month dividend yields).

A couple of big names are rapidly approaching the 6% dividend yield mark, including:

- Mapletree Industrial Trust

- Mapletree Logistics Trust

- Ascendas REIT

- CapitaLand Integrated Commercial Trust

- Netlink Trust

As shared previously, I would consider buying REITs if one of two things happen:

- REITs are cheap on a valuations basis

- Macro has bottomed (Fed Pivot)

Are REITs cheap on a valuations basis?

My previous fair value for Ascendas

A month or two back, I ran a simple exercise to determine fair value for the blue-chip REITs.

I specifically used Ascendas REIT as an example (because unlike MCT or CICT it hasn’t done any big merger the past 10 years that would skew the historical valuation).

My conclusion then was that:

- I would consider buying at 6% yields

- But I think fair value is 6.6% – 6.85% (approx. $2.2 – $2.35).

The assumptions I used back then were:

- 4.0% peak Fed Funds Rate

- 3.5% Peak 10 year Treasury

It is now clear that the previous assumptions I used were too conservative.

Realistically, we are looking at peak interest rates this cycle of:

- 4.5% – 5.5% peak Fed Funds Rate

- 4.0 – 4.5% peak 10 year treasury

That’s almost a 0.5 – 1.0% revision upwards in the risk free rate, which has huge implications for REIT prices.

Updated fair value for Ascendas

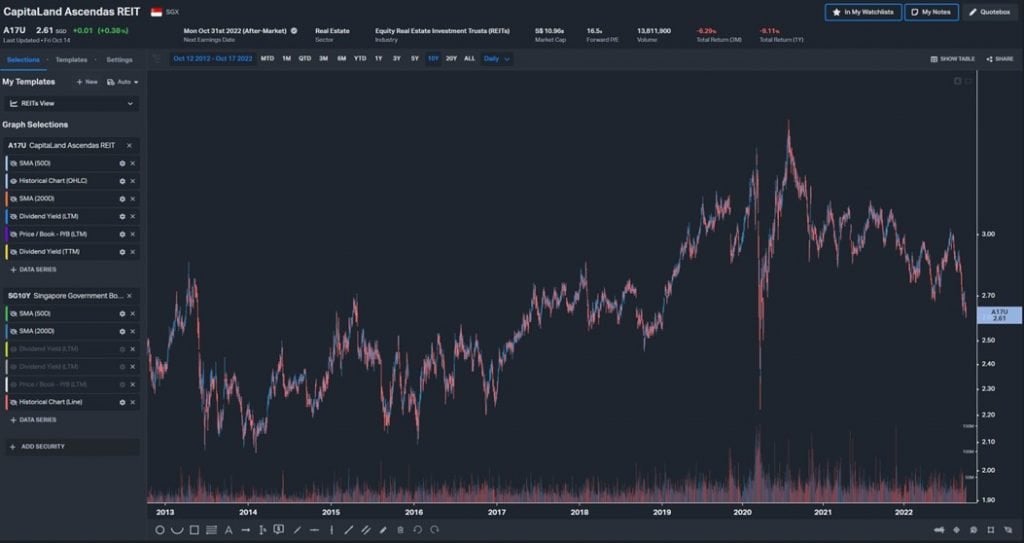

With that in mind, I wanted to refresh my fair value for Ascendas REIT using the latest assumptions.

I’ve set out the 10 year charts for Ascendas REIT’s dividend yield (yellow) and 10 year SGS (red) above.

The 10 year average for Ascendas REIT’s dividend yield is 5.63%.

The 10 year average for the 10 year SGS is 2.03%.

This means that the 10 year yield spread (dividend yield – risk free rate) for Ascendas REIT is 3.6%.

With the 10 year SGS at 3.5% today, that implies a fair value dividend yield of 7.1% for Ascendas REIT.

But this rate hiking cycle is not over, and I think we may see the 10 year SGS go anywhere from 3.5% – 4.5% before all this is over.

Going by these revised numbers, fair value for Ascendas REIT is about 7.0% – 8.0% dividend yields.

That means a unit price of about $1.93 – $2.2, which is still another 15-25% drop from here (A-REIT trades at $2.61, which is a 5.93% dividend yield).

Is it fair to use historical valuations?

Now some of you may say that it is not fair to use 10-year numbers, because Ascendas REIT has changed substantially since then.

It’s a fair point, and worth discussing in further detail.

There’s no denying Ascendas REIT today is a much bigger REIT than it was 10 years ago, simply because it has grown through acquisitions.

A bigger size means better stability and bargaining power, which deserves a valuation premium.

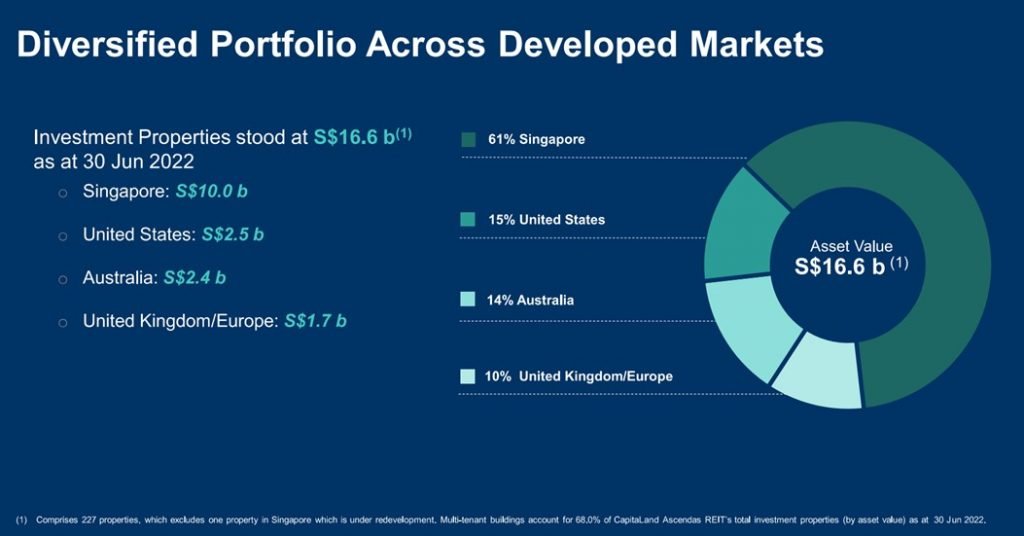

On the flip side, as Ascendas REIT grew, it diversified beyond Singapore real estate.

Today only 61% of the REIT is Singapore assets (rest is US, Australia and UK/Europe).

Generally speaking, I think overseas real estate will deserve a valuation discount in times like this, given record macro uncertainty.

Putting them together, I think the size and diversification points cancel each other out, to the extent that I would be comfortable relying on my valuation numbers above.

It’s crazy, but after the big decline in REITs prices, they are still not cheap

For what it’s worth, I understand your disbelief.

After the big plunge in REIT prices the past few months, from a valuations perspective they are still nowhere near cheap.

But hey – I’m not the one making the rules here.

As an investor, you always have the option to cash out and put your money into risk-free T-Bills yielding 3.77%.

When the risk free rate goes up, the valuations for assets across the board need to reprice, otherwise they just look less attractive.

And that’s just the first order effects

Now don’t forget the numbers above only adjusted for the first order effects of rising interest rates.

Don’t forget rising interest rates have a lot of knock on effects as well, including:

- Rental price growth (broadly linked to economic growth, inflation and real estate demand-supply dynamics as well)

- Impact on real estate valuations (same as above)

- Interest Expense

It is not easy to model the impact of (1) and (2), for the reasons discussed above.

The answer will differ from REIT to REIT, depending on the exact real estate mix.

Much will also depend on the global liquidity conditions, and how serious the coming recession will be.

(3) on the other hand, is very easy to model.

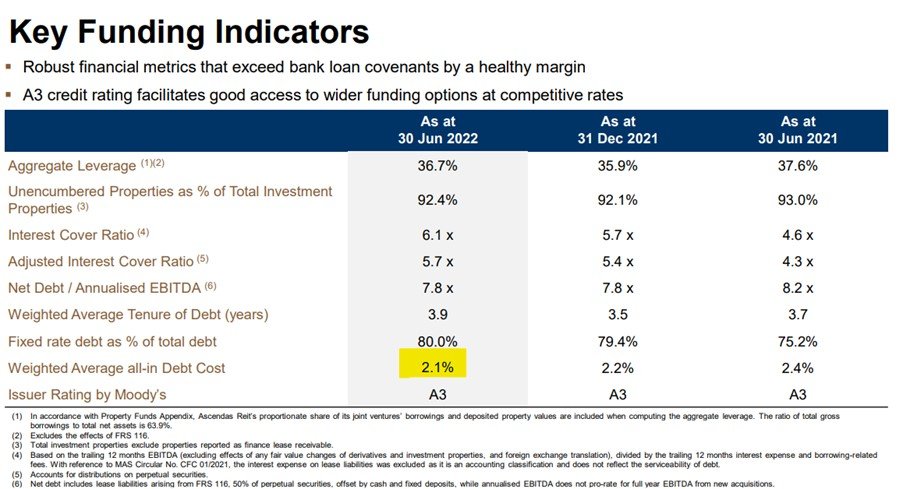

Ascendas REIT currently has an all-in cost of debt of 2.1%.

Let’s assume that cost of debt doubles to 4.2%, which is not too crazy in this new interest rate climate.

Running the numbers, that’s a 20% drop in distribution yield.

Which means what you previously thought was a 7% yield, is now 5.6%.

And again, that doesn’t even account for the impact of rising interest rates on real estate prices and on economic growth (which will affect rental).

There’s a reason why rising interest rates are so deadly for real estate.

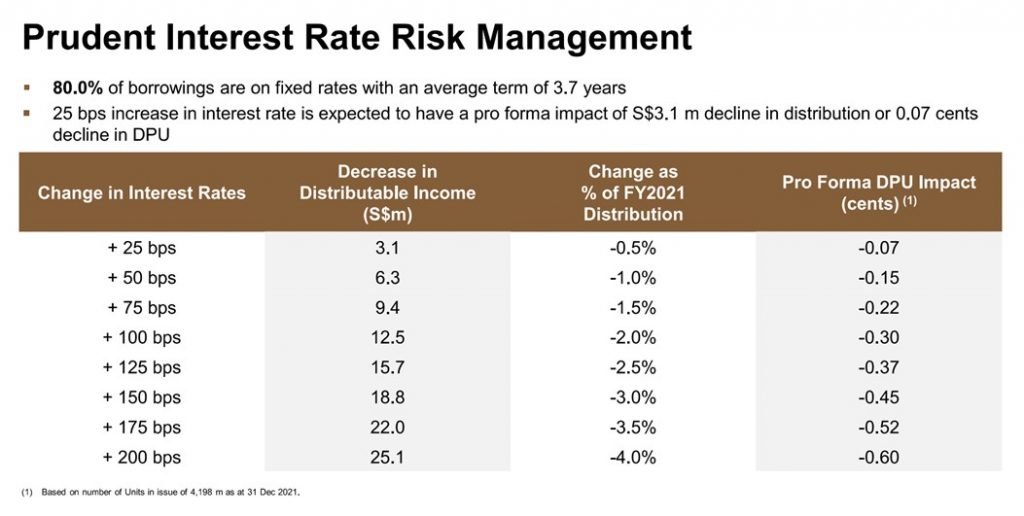

For the record – Ascendas REIT’s borrowings are hedged

Now for the record, 80% of Ascendas REIT’s borrowings are hedged, with an average term of 3.7 years.

So the rising interest rates will not impact Ascendas REIT’s interest expense ratio so quickly.

But I still leave the numbers above so you can better appreciate how badly REITs may get impacted if higher interest rates are here to stay, if inflation stays sticky.

So… Valuations are not cheap, what about the macro?

It’s clear that from a fundamental, valuations basis, REITs are nowhere near cheap yet.

They have not adjusted to the rapid rise in interest rates.

Which leaves macro.

If the Feds are going to pivot and drop interest rates to zero by early 2023, then of course everything changes.

Macro has not bottomed yet

Now I’ve talked about macro to death in the other posts, so I wont belabour the point.

Latest macro views are that:

- While leading inflation indicators are starting to roll over, labour inflation is still very hot – driving the services component of US CPI

- This means the chance of a Fed pivot in 2022 are very low

- Any Fed pivot is probably more of a 2023 story, and the exact timing will depend on (a) when markets break, or (b) when inflation starts to roll over

And this is not a situation where I want to frontrun the Feds.

I don’t see a need to buy the bottom here, and risk getting the call wrong.

I’m prioritising capital preservation, over capital growth.

I’ll just wait until the Feds announce their decision to stop hiking (or cut rates), and then I would start buying (unless of course valuations are dirt cheap – but they are a long way from there).

Sell DBS?

Earlier this year, I wrote a piece on trying to market time the local bank stocks.

My conclusion, was that:

DBS tends to top out about 4 – 8 months before the peak in US interest rates

Going by this thesis, if you assume a Fed pivot in mid-2023, then working backwards you want to sell DBS roughly in Q4 2022 – Q1 2023.

Now this is using 20 year data, over 3 rate hike cycles, so frankly it’s quite a small sample size.

All of the 3 prior crashes were deflationary style crashes, and not inflationary crises as I think the current one will be.

So I do suggest you take the conclusion above with a large pinch of salt.

Frankly don’t know where DBS trades going forward

That said, frankly I don’t know where DBS will trade the next 12 months.

Rising interest rates will translate into much higher net interest margins (NIM) for DBS, so the NIM will explode (in a good way).

The big question – is loan defaults.

How bad will the coming recession be, and how high a level of loan defaults will we see?

If things get really bad, will the government step in with stimulus and loan payment waivers like we saw in 2020?

Like I said, I don’t know the answers to these questions, and I don’t know where DBS will go the next 12 months.

Risk-Reward is asymmetric

What I do know, is that with DBS trading at 1.5x book value, the risk-reward looks asymmetric.

Especially given the risks piling up in the macro world.

Let’s say everything goes smoothly, the economy avoids a recession, there are no loan defaults.

Maybe DBS goes back to all time high of 37. Plus a 4% dividend, that’s about a 16% return if all goes well.

What if things go wrong?

If we get a hard landing, how high is the downside?

Will we get a liquidity crisis this cycle?

DBS book value is about 22, which is a 33% drop from here if it goes back to book value.

Can I deploy the capital more effectively elsewhere in the next 12 months?

I also think that with the rapidly rising interest rates, some part of the market is going to break sooner or later.

We already see that with the UK Gilts and pension funds, and with the BOJ.

More will come.

So if DBS never declines and stays in the 30s for the next 12 months, I still think I can deploy the cash elsewhere in the market to achieve a higher return.

I’ve sold slightly over half of my DBS and UOB positions to date (mostly accumulated in 2020).

If DBS drops in 2023/2024, I’m happy to buy it back.

If DBS doesn’t drop significantly, I will redeploy the cash elsewhere.

In the meantime, cash is earning close to a 4% yield these days, which significantly reduces the opportunity cost.

Food for Thought – Do you still buy the Fed pivot?

Now I’ve been saying all year that I will wait for the Fed pivot, then I would start buying.

But I was rereading Ray Dalio’s Big Debt Crises over the weekend, and it got me thinking (it’s a must read if you’re serious about macro investing btw).

Traditionally speaking, there are 2 kinds of economic crises.

The (1) inflationary kind, and the (2) deflationary kind.

The inflationary kind is the kind that results in currency depreciation and high domestic inflation. Think Weimar Germany, think Asian Financial Crisis etc.

In an inflationary crisis, the time to buy, is when the currency depreciates a lot, and when it bottoms (usually after a 30% drop). This usually coincides with the peak in short term interest rates (ie. the central bank pivot).

So I’ve always assumed this coming crises would be an inflationary one, where the next phase is currency depreciation and a higher level of structural inflation.

And therefore the time to buy is when central banks pivot, and after the big currency depreciation.

What if this is a deflationary crisis instead?

Now what if this is a deflationary crisis instead?

In a deflationary crisis, deflationary forces like debt default and restructuring dominate.

Think 2008 GFC, and 1930s Great Depression. Or China right now with their real estate crisis.

Now in a deflationary crisis, the central bank pivot is just the start.

After central banks pivot, the deleveraging and market collapse continues, and stocks only bottom later (12 months after the pivot on average).

More specifically, stocks bottom around the point where the deleveraging is offset by sufficient money printing.

What does this mean?

Long story short – I’ve always assumed the coming crisis will be an inflationary one.

But if I’m wrong and it turns out to be a deflationary one, then you need to wait until the massive stimulus comes (via big rate cuts and QE) before you start buying.

How do you know whether you are in an inflationary crisis or a deflationary crisis?

It’s never easy to tell when it’s playing out.

My suggestion is to be flexible.

Don’t be too stubborn and dogmatic in your view – and don’t be afraid to change your mind.

Let the macro play out, and watch the events play out carefully.

Watch how central banks and governments react to the unfolding crisis, and decide whether they are prioritising (a) fighting inflation, or (b) trying to stimulate growth.

You only start buying when the forces favour stimulating growth over fighting inflation.

In any case, I will continue to share macro views here as the crisis plays out.