I recently received this question from a reader:

Hi FH

It’s my first time having to make a decision on a rights issue.

Are you able to share your thoughts on the rights issue for Keppel kbs reit?

For example, what are the possible thought process that an investor has to go through to make a decision for the rights issue of this reit? What is the possible rationale for the reit manager to issue the new shares at such a discount?

Thank you!

Absolutely fantastic question! Rights issues are a core part of REIT investing, and every REIT investor will need to address this question at some point in his investing career.

I will use Keppel KBS REIT as a case study here. Tam Ging Wien over at Probutterfly recently penned an article on the Keppel-KBS REIT rights issue, and I thought it was very well done. I’ve shared it in full here with his permission, and I’ll share my thoughts on the decision making process below.

On the 24-Sep-2018, Keppel-KBS REIT announced its maiden acquisition of Seattle assets known as the Westpark Portfolio in Redmond, Washington for US$169.4mil.

The assets are valued at US$178.0mil and US$181.4mil by valuers Cushman and JLL respectively. The agreed acquisition price is therefore 4.8% and 6.6% discount to both the independent valuations.

According to the announcement, the acquisition is expected to be yield accretive based on pro forma figures with the following assumptions:

- Portfolio has an occupancy rate of 97.7%

- Partially funded with a rights issue of US$0.59 per unit to raise US$102.3mil

- Resulting theoretical ex-rights price of US$0.7854

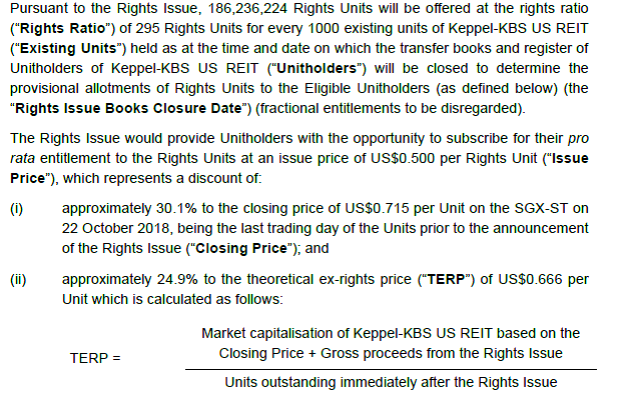

In a surprising twist, Keppel-KBS REIT announcement late Monday on the 23-Oct-2018 for a 295-for-1000 rights issue priced at only US$0.50 per unit, 15% lower than its initial assumption. This larger than expected rights would result in the theoretical ex-rights price of US$0.666 instead.

Keppel-KBS REIT also announced its latest results as of 30-Sep-2018 on 17-Oct-2018

Due to a set of disparate announcements and differing assumptions, it is difficult for many unitholders to make sense of the overall deal and what it means to them.

Here in this article, we examine the details of this rights issue and acquisition and put them together so that unitholders can better understand how it affects them.

Details of the Proposed Acquisition

The Westpark Portfolio is a business campus comprising 21 buildings in Redmond, Washington with good connectivity to key commercial hubs in Redmond and the Seattle-Bellevue area.

Source: http://www.kepkbsusreit.com/en/news_item.aspx?sid=7381&aid=8001

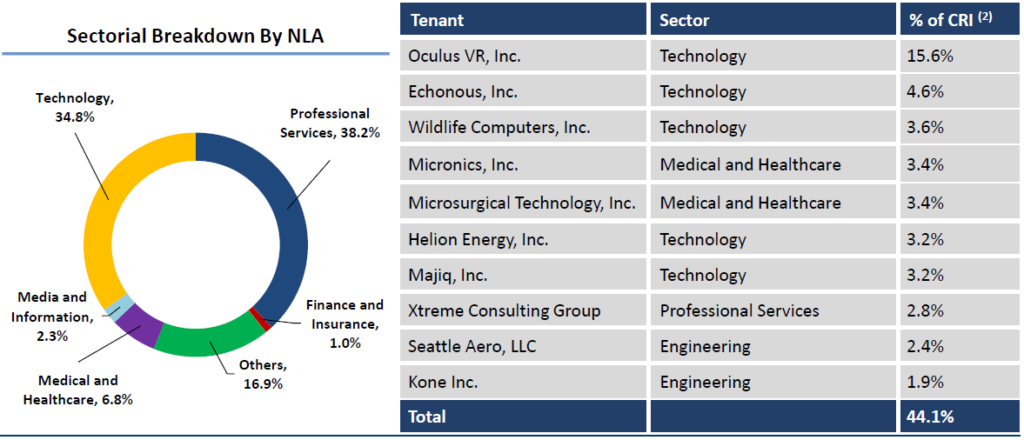

The Westpark portfolio is a freehold asset and is currently 97.7% occupied with an average portfolio WALE of 4.3 years.

About 34.8% of portfolio tenants are from the high growth technology sector and another 38.2% of the tenants are in the professional services, the bulk of them which provides support services to these technology tenants.

Source: http://www.kepkbsusreit.com/en/news_item.aspx?sid=7381&aid=8001

Management provided the following rationale for the propose acquisition:

- Deepen Presence in High Growth Seattle Market

- Accretive Acquisition Positioned for Long Term Growth

- Portfolio Diversification that Enhances Income Resilience

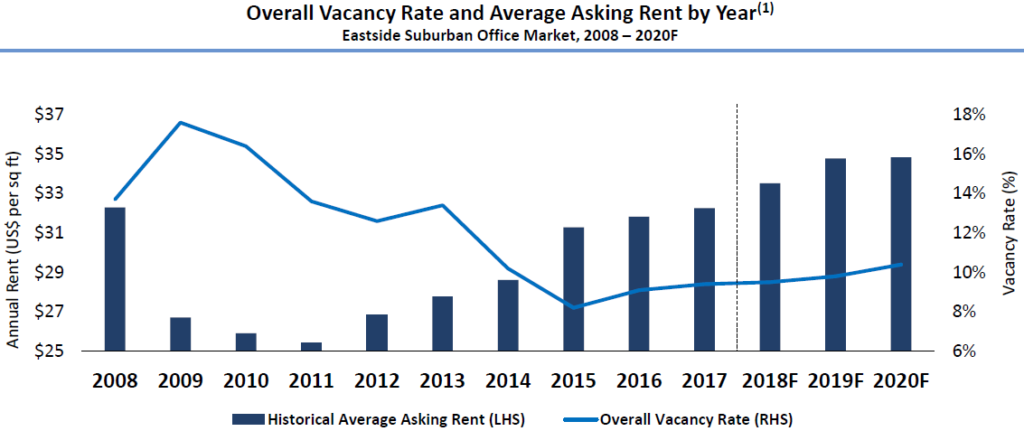

The location and portfolio appeals to tenants in the technology section due to close proximity to Microsoft World HQ and the key commercial hubs in Bellevue and Seattle.

Source: http://www.kepkbsusreit.com/en/news_item.aspx?sid=7381&aid=8001

The annual rent in the vicinity has been growing over the years and is expected to continue to through 2018 and 2019.

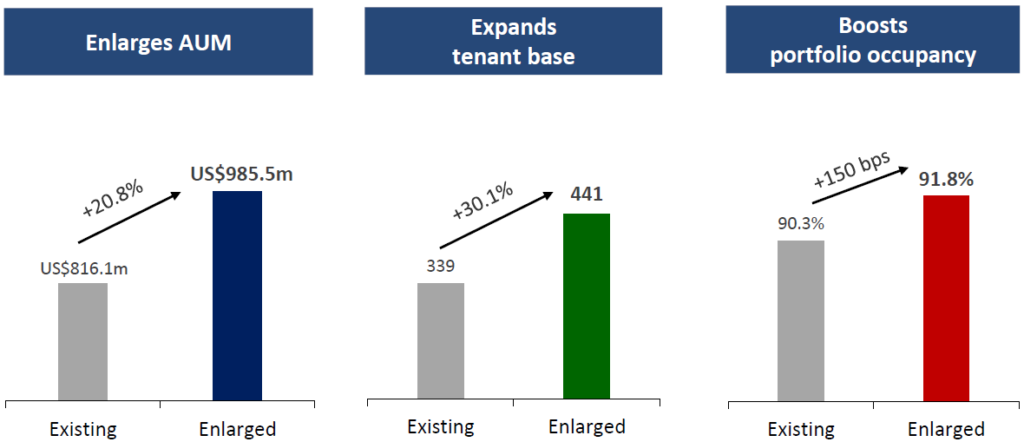

The acquisition of Westpark portfolio is also expected to increase diversification through the enlargement of the AUM, tenant base and increase in overall portfolio occupancy.

Source: http://www.kepkbsusreit.com/en/news_item.aspx?sid=7381&aid=8001

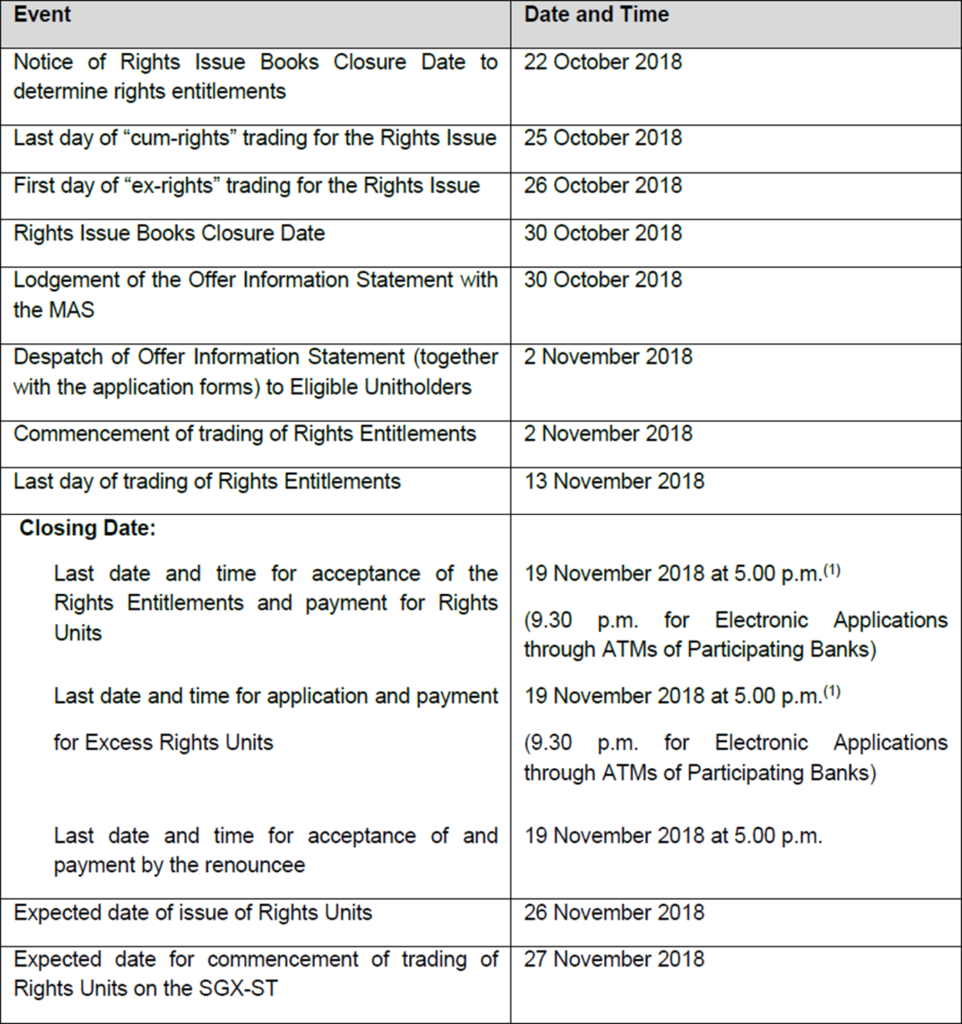

Details of the Rights Issue

To finance the proposed Westpark portfolio acquisition, the management proposes to undertake a 295-for-1000 renounceable rights issue priced at US$0.50 per unit and issue 186,236,224 new units to raise gross proceeds of approximately US$93.1mil.

Keppel-KBS REIT closed the week at US$0.69 per unit the week prior to the announcement. This means that the rights issue price of US$0.50 per unit represents a discount of 27.5% to the previous week closing price and 24.9% discount to the theoretical ex-rights price of US$0.666.

Out of the US$93.1mil expected to be raised, approximately US$89.7mil will be used to partially fund the acquisition of Westpark Portfolio while the remaining are used to pay the fees and expenses incurred in the fund raising.

The indicative timetable of the rights issue is provided below:

Source: http://www.kepkbsusreit.com/en/news_item.aspx?sid=7381&aid=8177

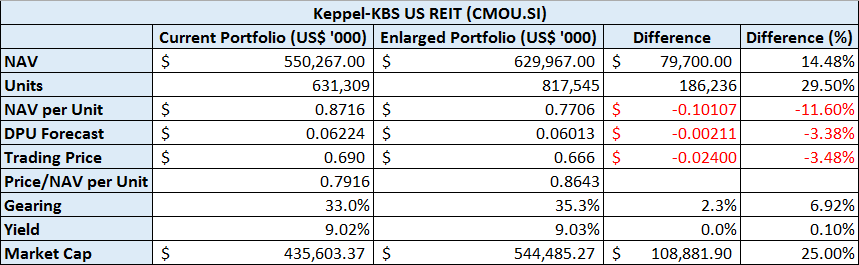

Putting the Acquisition and Rights Issue Together

Using information from Keppel-KBS REIT’s latest financial results, details of the acquisitionas well as details of the rights issue, we can now start to stitch together a holistic picture of what this deal would mean to unitholders.

Source: REITScreener Research, ProButterfly Research

The increase in NAV is estimated by adding the difference between the valuation of the Westpark Portfolio and the total debts incurred in the acquisition. This results in an increase of approximately 14.5%.

The units are increase assuming all the rights are taken up according to the 295-for-1000 ratio – in other words, the total unit base will increase by 29.5%.

The DPU forecasted are based on annualisation of its financial period since listing on the 09-Nov-2017 until its latest reported results on 30-Sep-2018. The DPU forecast of the enlarged portfolio was estimated based on the pro forma DPU figures provided in the acquisition announcement. DPU is expected to fall 3.38%.

Gearing is also expected to increase from 33.0% to 35.3%.

There is no significant change in the yield based on the theoretical ex-rights price of US$0.666.

What We Think of the Deal

Based on the closing price of US$0.54 at the time of writing, the yield is forecasted to be 11.14%. Certainly with such a steep fall in price from US$0.69, the market is viewing this deal negatively.

If viewed from its IPO price of US$0.88, the fall represents a 38.6% capital loss. We have previously covered the IPO of Keppel-KBS REIT <https://www.probutterfly.com/blog/analysis-of-keppel-kbs-us-reit-ipo> and it may serve unitholders to review the assumptions made at that point of time.

As a result of this deal, NAV per Unit is dilutive owing to the fact that the base units are increased by 29.5%, much more than the NAV gain of 14.5%. From a DPU perspective, the deal is also dilutive on a per unit basis, falling from a forecast of US$0.06224 to a US$0.06013 – a fall of approximately 3.38%.

Gearing will also increase by 2.3% to 35.3%. This will also likely result in higher interest cost.

Based on our analysis and assumptions above, we certainly concur on the negative view of the market in the short term.

The deal while not as severe an impact to unitholders compared to the recent acquisition and rights issue proposal made by OUE Commercial REIT’s acquisition of OUE Downtown, it not beneficial to unitholders in the short term.

In the longer term, perhaps the high growth tech sector will help to grow Keppel-KBS REIT’s portfolio returns organically contributing to higher DPU and higher NAV per Unit. That’s assuming that the manager doesn’t make another net dilutive rights issue and acquisition before the portfolio has time to fully revert to its current DPU.

All eyes will be on the REIT manager going forward on how it manages its future acquisition pipeline.

To sum up Tam Ging Wien’s analysis, this transaction and rights issue is dilutive for unitholders, both in terms of DPU (distribution per unit) and book value (NAV per unit). However, if you don’t subscribe for the rights issue as a unitholder, you’re still going to get diluted anyway, but because you didn’t average in through the rights issue, the dilution to you is significantly higher than other unitholders who took up their rights.

To illustrate this very simply – Imagine you hold S$1000 units of a REIT at 1 dollar each. The DPU is S$0.06 (ie. 6% yield), so you get 60 dollars a year.

The REIT now does a 300 to 1000 rights issue at a 30% discount.

If you take up the rights issue, you will own 1300 units at a cost of S$1210. If the DPU stays the same at S$0.06, that’s S$78 distribution a year, which works out to a 6.44% yield.

If you don’t take up the rights issue, you will own 1000 units at a cost of S$1000. The DPU stays the same at S$0.06, totalling 60 dollars a year, which works out to a 6% yield.

It’s a very simplistic analysis, but you get the point. Because of the massive discount of the rights, subscribing for them is basically a way of dollar cost averaging into the investment, to reduce your average price per unit. If everything else stays the same, in almost every case (there are a few exceptions), subscribing for the rights issue is better than not subscribing for the rights issue.

And the two notable exceptions to this are:

- If the current market price of the units is below the price of the rights. This almost never happens. If this happens, the market is signalling a total loss of confidence in the REIT, or you’re having a severe liquidity crunch in a financial crisis style situation. If this happens, it is pointless to take up the rights, you’re better off just buying the units at a cheaper price on the open market to average down.

- You don’t have the cash lying around. If you have S$100,000 in Keppel-KBS REIT, a rights issue like this would cost you upward of S$20,000 to subscribe. That’s not spare change. A lot of investors just may not have that kind of liquidity lying around to take up a rights issue. If so, you need to make a value judgment for yourself. How big a discount are the new rights, as compared to your buy in price. If the discount is big, the opportunity cost of not taking up the rights is very high, and you should be trying to find to find a way to get the cash. If the discount is small (this is rare), the opportunity cost is lower, and you can consider sitting it out and being diluted.

I’ve set out Keppel-KBS REIT’s pricing for the rights issue below, and you can see it’s priced at a massive 30% discount to the price before the rights issue was announced. If you’re an existing unitholder, you’re already sitting on a huge capital loss, and your best bet is to average in.

Source: SGX Announcement (All Keppel-KBS REIT announcements here)

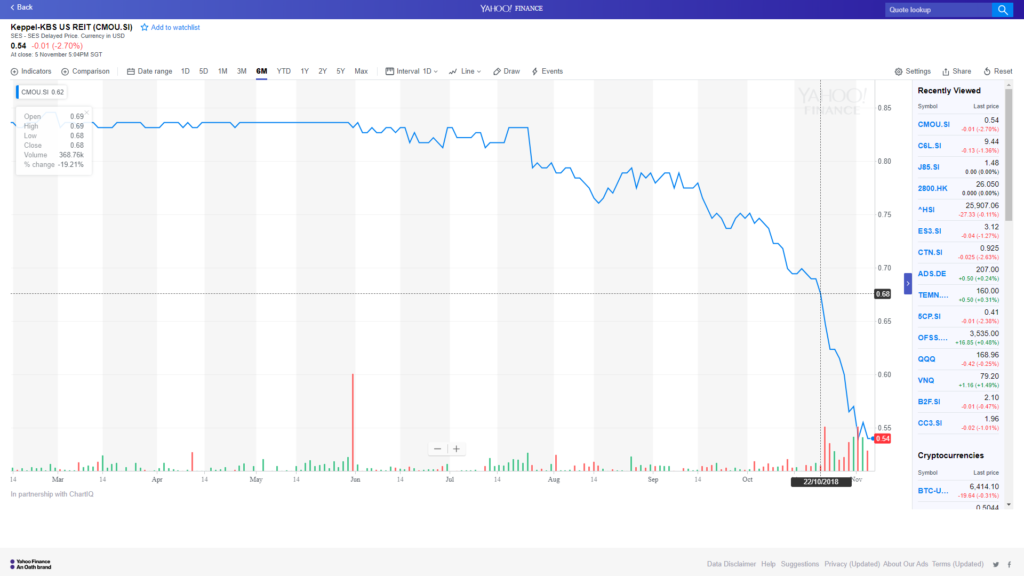

What if you after this horrible rights issue, you absolutely hate the REIT and want to exit your investment entirely? That depends a lot on the current market price of the REIT. Keppel-KBS’s chart is set out below (marked out when the rights issue was announced). As you can see, the unit price has fallen almost 20% since the rights issue was announced. You can still sell it now, but it really doesn’t make sense. Personally, if I were in such a situation, I would take up the rights issue, hold the REIT, and wait for a better price to exit in the next 6 to 12 months.

My approach to REIT investing and rights issue is this. I only buy REITs from big reputable sponsors, to reduce the chance of a situation where the manager does a massively dilutive rights issue to screw unitholders over. Such sponsors will include CapitaLand, Mapletree and Frasers. Secondly, I only buy REITs where I like and believe in the growth story. If you had bought into Keppel-KBS US REIT, presumably you were bullish on US commercial real estate. This acquisition is exactly in line with that strategy. Sure, the method of financing is questionable, but if you truly believed in their growth story, you’ll take up all your rights, and use this temporary dip to add to your position in the REIT.

For me, whenever there’s a rights issue for a REIT I own, I’m taking up all my rights, and applying for all the extra rights I can get to further reduce my cost of investment. I can do this because I believe in management’s strategy and vision for the future. As retail investors, we don’t have much say over such what acquisitions are done, or how they are financed. So it’s important to pick a REIT that you believe in, and are comfortable holding for the long term. If at some point you no longer believe in the story, you should look to exit, but even then it still pays to be patient. Take up the rights, and wait for a better exit opportunity. One will usually present itself.

Till next time, Financial Horse, signing out!

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. Enter your email below to receive a copy in your inbox!

[mc4wp_form id=”173″]

Enjoyed this article? Like our Facebook Page for more great articles, or join the Facebook Group to continue the discussion!