Dear Sasseur REIT,

I had such great hopes when I first read about you. The first outlet mall REIT to be listed in Singapore, with assets located in China, and a forecast 7.5% annualised FY 2018 yield? Were you to be the China REIT to dispel investor doubts about China REITs? The S-REIT to allow Singaporean investors to regain their faith in China listings?

But alas, the reality is a lot more complicated. Your Entrusted Management Agreement is a complicated web of obligations that effectively amounts to a 2 year income support in exchange for a 10 year master lease that limits DPU upside. Your outlet malls are ultimately dependent on Sponsor support to be successful. And at a 7.5% forecast yield and a 3% premium to book, you definitely are not cheap. Is this why you kept the public offering at a miniscule 11 million SGD, to reduce underwriting risk?

Basics: Sasseur REIT

Sasseur REIT is Singapore’s first outlet mall REIT, with assets located in Tier 2 cities in China. From its own Prospectus, it professes to be:

“Sasseur REIT is the first outlet mall REIT to be listed in Asia with an Initial Portfolio comprising outlet malls located in the PRC. Unlike traditional retailing formats such as department stores and shopping malls, sales through outlet malls in the PRC are experiencing strong growth. Because of the strong growth momentum, the PRC’s outlet sector is expected to become the world’s largest outlet market by 2030.”.

Of course, the reality is a lot more complicated.

Source: Sasseur REIT Prospectus

- Entrusted Management Agreement (EMA)

The key to understanding Sasseur REIT lies in its Entrusted Management Agreement. Clearly the lawyers (and possibly the SGX) felt the same way, because references to the EMA are littered throughout the entire prospectus. Now I have to confess, Financial Horse used to be a corporate lawyer who drafted prospectuses for a living, and it took me more than an hour to work through the mechanics of the EMA (you can take a look at my scribbling below as proof).

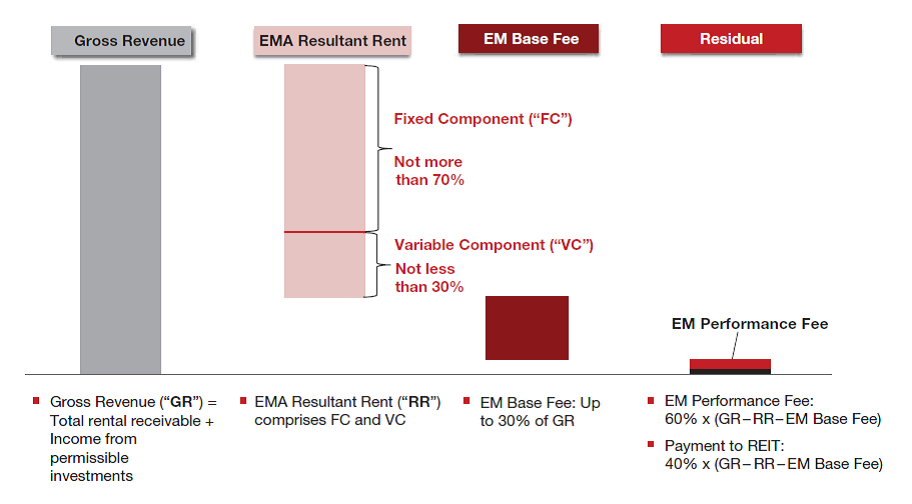

In summary, the EMA is a master lease agreement with a built in income support. To simplify it massively, let’s assume that the REIT receives S$100 gross revenue from rent.

REIT Component – The REIT will keep S$60, which we shall call the REIT component for discussion’s sake. The REIT component comprises 2 parts, a fixed component and a variable component. The fixed component is a fixed sum that is determined prior to IPO and willl step up at 3.0% a year, but will always form less than 70% of the REIT component. The rate of the variable component is determined prior to IPO as well, and is a percentage of each outlet mall’s respective total sales.

Sponsor Fee – The REIT will then take S$36 (of the remaining S$40) to pay its Sponsor for managing the properties. Let’s call this the Sponsor Fee. The Sponsor Fee is again split into 2 parts, being a fixed and variable component.

The fixed component is the lower of (1) 30% of gross revenue or (2) Gross revenue minus the REIT component. Based off our example, (1) will work out to be S$30, and (2) will be S$40, so the fixed component will be S$30 (the lower of the two).

The variable component is determined by the formula: 60% (Gross Revenue – REIT Component – Fixed Component of Sponsor Fee). Using our example, this will be 60% (100 – 60 – 30) = S$6.

REIT Upside – After payment of the Sponsor Fee, we are left with S$4 for the REIT, which we shall call the REIT upside.

What the REIT gets – The REIT gets the REIT Component and the REIT Upside, which is S$64 dollars (while the Sponsor gets S$36). The REIT will take this S$64 dollars to pay its REIT management fees, trustee management fees, and other expenses. After deduction of expenses, the remainder will be paid out to unitholders via distributions.

Source: Sasseur REIT Prospectus

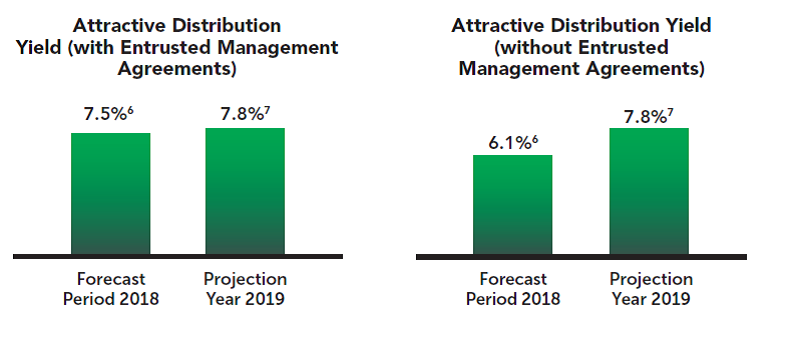

Income Support – If you thought the above was complicated, it gets even better. In exchange for the Sponsor Fee, the Sponsor will provide a psuedo income support for the REIT. The Sponsor will guarantee that the REIT Component will never fall below a certain amount, which we will call the Minimum Yield. This Minimim Yield is fixed at IPO, and works out to be 7.5% annualised yield for FY2018, and 7.8% yield for FY2019. The amount does not change from 2020 onwards, and will stay at 7.8%.

It gets even trickier. If the REIT Component is greater than the Minimum Yield for 2 consecutive years, then this income support falls away, and unitholders will be left holding the risk of the asset underperforming. Given the way this has been structured, I can only assume that the Sponsor is highly confident that it will be able to meet the Minimum Yield for the first 2 years. Even if it doesn’t, the Minimum Yield does not step up from 2019 to 2020 onwards, so it will most likely be achieved in the third year. Do note also that the EMA lasts for a period of 10 years (and is renewable for another 10 years), so there will be a situation where the income support falls off, but the Sponsor still enjoys its management fee.

Source: Sasseur REIT Prospectus

It is certainly controversial, which is why Sasssuer REIT felt it fit to appoint KPMG Corporate Finance Pte Ltd as an independent financial adviser to provide an opinion to the Independent Directors and the Trustee as to whether the Entrusted Management Agreements are on normal commercial terms and not prejudicial to the interests of Sasseur REIT and its minority Unitholders (their view is yes btw).

Sasseur REIT justifies this arrangement on the basis that:

due to the specialised nature of outlet mall operations as well as the fact that the bulk of the revenue generated from the Properties are predominantly sales-driven, the management of outlet malls would be resource-intensive and have significant manpower requirements which Sasseur REIT as a REIT would not be able to undertake on its own. As an experienced outlet mall operator, the Entrusted Manager would be able to commit experienced staff and manpower who have already been managing the Properties since their inception to continue managing the Properties on behalf of Sasseur REIT so as to maintain operational continuity and effectiveness;

the Entrusted Manager is familiar with the specialised retail outlet mall business model and it has a strong operating track record and distinct management capabilities in operating and managing retail outlet malls (including those owned by third parties); and

the Entrusted Manager, in its role as the entrusted manager of the Properties, shall be exercising full control over the running, operation and performance of the Properties, subject to the oversight of the Manager.

My own take on this is that the EMA is effectively a master lease to the Sponsor, where the Sponsor is paid a significant chunk of revenue, in exchange for managing the properties. Given that outlet malls are highly management intensive (they don’t get fixed rents, but rather a percentage of turnover), this may not necessarily be a bad thing. However, it does limit the upside in a way, because even if the outlets perform well, a huge chunk of the upside is going to the Sponsor as fees.

At the same time, the downside is protected for 2 years due to the income support. In the third year, chances are good that it will fall away, and unitholders will be left assuming the risk of the assets underperforming. It’s a very interesting proposition, and kudos to the bankers and lawyers who thought it up.

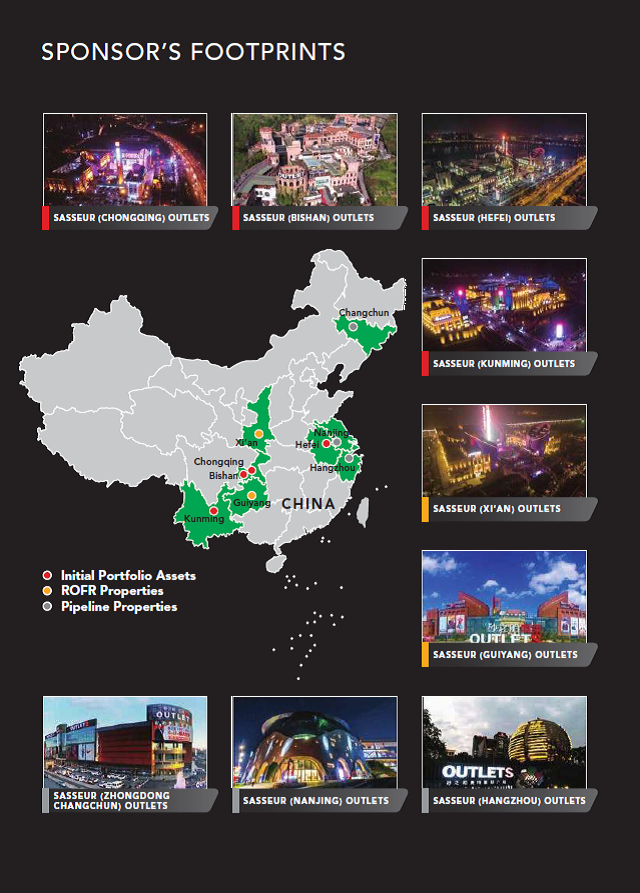

- Assets (Location and quality)

The initial portfolio comprises 4 retail outlets and 2 ROFR properties, all in Tier 2 cities in China. I have never been to any of the outlet malls in this portfolio, so I really can’t comment on how amazing an asset they are. Based off the prospectus, they are touted as one stop destination shops (the closest equivalent in Singapore would probably be the Tampines Ikea, but on a much larger scale).

Source: Sasseur REIT Prospectus

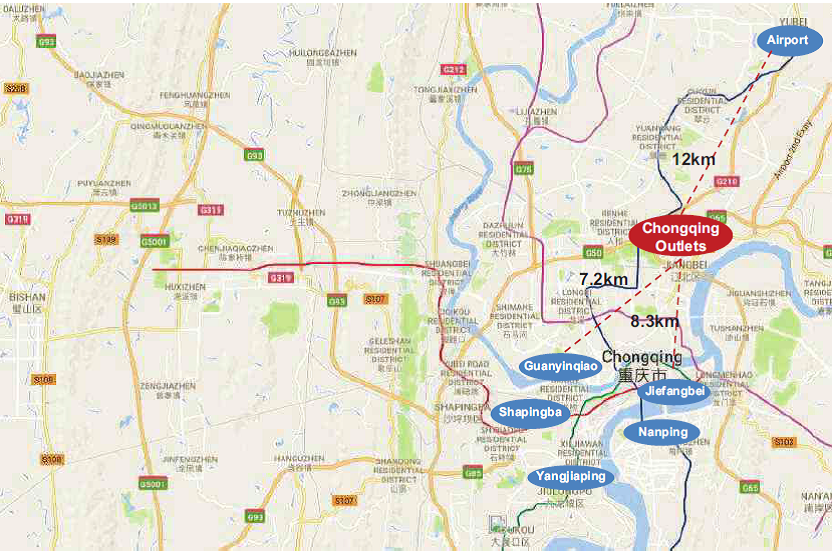

Given that these outlet malls are located slightly outside of population centers (which is typical of an outlet mall), there is unlikely to be much inherent value in the land itself. It is vital that the Sponsor continues to value add, to market and promote these outlet malls to attract footfall, which is probably why the Sponsor enjoys such a huge chunk of revenue under the EMA.

Source: Sasseur REIT Prospectus

This is further compounded by the rental structure in place. Unlike typical rental contracts, outlet malls collect almost exclusively gross turnover rent, where tenants pay rent based off their sales. This would mean that a fall in tenant sales will really impact the REIT, with a direct and immediate impact on the financials. By contrast, leases at a more traditional mall (such as those by CapitaLand Mall Trust or Frasers Centerpoint Trust) will have a large fixed rent component, that helps to smooth out the lumpiness in earnings, and are less directly exposed to tenant sales volume. This means that a fall in competitiveness of the outlet mall, perhaps due to a competitor or changing consumer tastes, is really going to bring a world of pain for the REIT.

The Independent Market Research Report touts outlet malls as a fast growing area in China. I can’t really comment on this, but given the prevalence of Taobao and e-commerce in China, and the fickleness of modern consumers, I remain a sceptical “I will believe it when I see it” in relation to outlet malls.

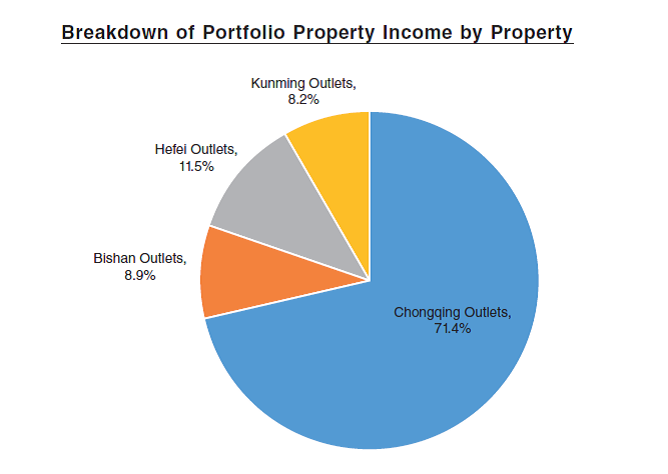

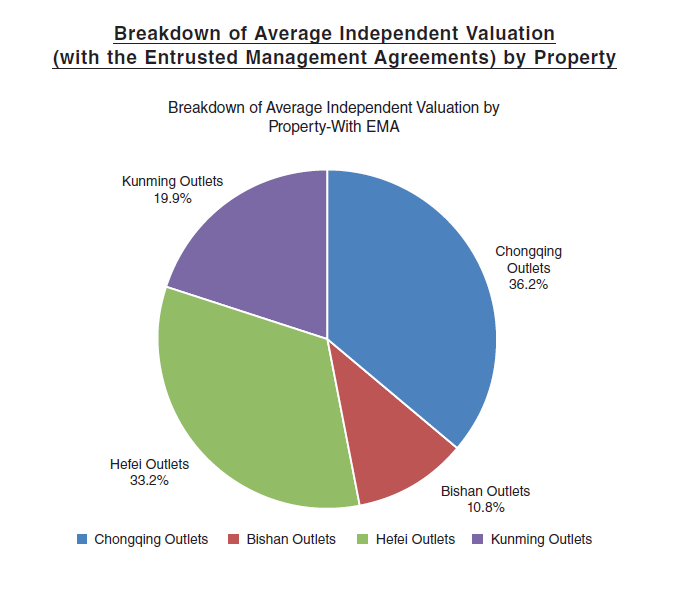

The initial property income is also highly lumpy, being concentrated mostly in the Chongqing outlet (it contributes 71.4% of income while forming only 36.2% of the portfolio valuation). The rationale given is that the other outlets are less mature assets, and need some time to ramp up sales. Admittedly, this is less of a problem, given that there is income support for the first 2 years. However it would be interesting to see whether the other 3 outlets are able to ramp up sales as quickly as the REIT is projecting. If possible, then China outlet malls may truly be a revelation and this REIT may be the best thing to hit SGX in a while.

Source: Sasseur REIT Prospectus

- Sponsor

The prospectus sums up the Sponsor, Sassuer, quite well:

The Sponsor Group has ample experience in the development of outlet malls. As at the Latest Practicable Date, the Sponsor has designed and implemented the development of six outlet malls, which comprise the four Properties in the Initial Portfolio, as well as the two ROFR Properties (namely Xi’an Outlets which commenced operations on 30 September 2017, and Guiyang Outlets which commenced operations on 9 December 2017). The Sponsor Group also has extensive experience in the management and operation of outlet malls. It managed and operated the four Properties in the Initial Portfolio, and currently manages and operates the two ROFR Properties and the three Pipeline Properties. As at 30 September 2017, the four Properties, one ROFR Property (namely, Xi’an Outlets) and the three Pipeline Properties that were in operation had an average occupancy rate of approximately 90.1%.

The Sponsor’s substantial size is also evidenced by its profitability and balance sheet strength, with the Sponsor reporting a total net profit of approximately RMB 2.0 billion for the year ended 31 December 2016 (equivalent to approximately S$0.4 billion) and total assets of RMB 11.9 billion (equivalent to approximately S$2.5 billion) and total shareholders’ equity of RMB 5.5 billion (equivalent to approximately S$1.1 billion) as at 31 December 2016.

From the above, it seems like the Sponsor is not a juggernaut like a Dalian Wanda or even a CapitaLand. As a rough gauge, the Sponsor’s net profits of S$0.4 billion and assets of S$2.5 billion doesn’t compare too favourably to Wanda’s S$50 billion revenue, or even homegrown CapitaLand’s S$1.84 billion profits. Don’t buy this REIT thinking that its backed by a major Chinese SOE or conglomerate, because its not. It’s more of a niche play, with a focus on outlet malls.

On the plus side, there is a very strong alignment of interests, as the Sponsor holds about 58% after listing (assuming no over-allotment option exercised), and is also entitled to significant profits under the EMA.

- Valuation (P/B and Yield)

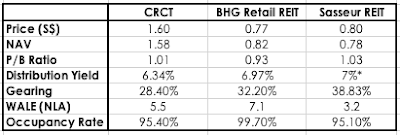

SleepyDevil did an amazing table that compares the valuations of Sassuer REIT against its peers. Admittedly, CRCT and BHG REIT are not true peers, since they are retail malls in Tier 1 cities. But it is useful as a rough gauge, and as expected, investors will get a significantly higher yield from Sassuer as a risk premium, given that Tier 2 outlet malls are inherently riskier. The 3% premium to book comes as a surprise, since this is even higher than CRCT.

Based off these numbers, Sassuer does not look cheap by any means. To buy into this REIT, you have to believe the aggressive financial projections that are being forecasted, to justify the handsome valuation.

Source: SleepyDevil

Honorable Mention: IPO pop on Day 1

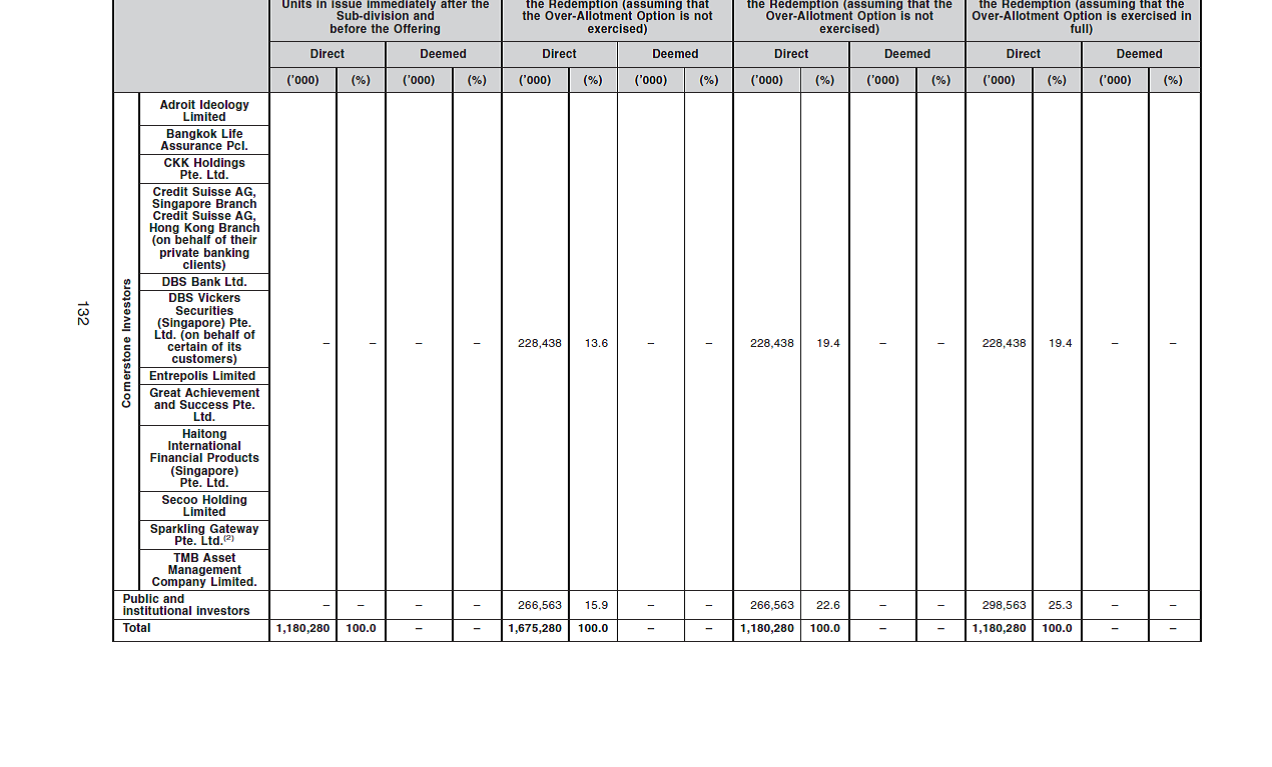

To be honest, the success of this REIT is already guaranteed, given that most of the units have been already been placed to cornerstone investors. The public tranche is only S$11 million, so even if the retail take up is poor, the underwriters will just mop up the remaining units, which at S$11 million is small change.

Source: Sasseur REIT Prospectus

More interestingly, the fact that the public tranche is so small raises the possibility that prices may pop on IPO day due to lack of liquidity. However, upon closer examination, it seems that not all the cornerstones are subject to a lock-up arrangement. I therefore cannot rule out the possibility that one of these big boys will sell on day one. Considering also the current market volatility the past 2 days, I will not be trying to punt this IPO.

Closing Thoughts

I have mixed feelings on this REIT. Essentially I am getting a guaranteed annualised 7.5% yield for the first year, and 7.8% on the second. In the third year, most likely the income support falls away, so I take on the risk of the asset underperforming. And if it performs well, my upside is limited, due to the pseudo master lease in place to the sponsor.

At the end of the day, these are outlet malls in a tier 2 city in China that I have never seen with my own eyes. These are also young assets that need some time to ramp up sales. There is always a tail risk that Chinese consumers decide to go to another mall, after which the asset is worthless. If outlet malls in China are really as attractive as they say, why are other big competitors not flooding into this area (or if they are, how will Sasseur hold up?).

You can consider buying if you are familiar with the assets / outlet malls in China, and have a strong belief that the assets will perform well after year 3. If the underlying assets grow according to the financial projections, you could well make a ton of money.

It’s a bit too many unknowns for me for a 7+% yield at a 1.03 times book value. I can easily buy a safer REIT at a 6+% yield and sleep easy. I will probably give this REIT a miss.

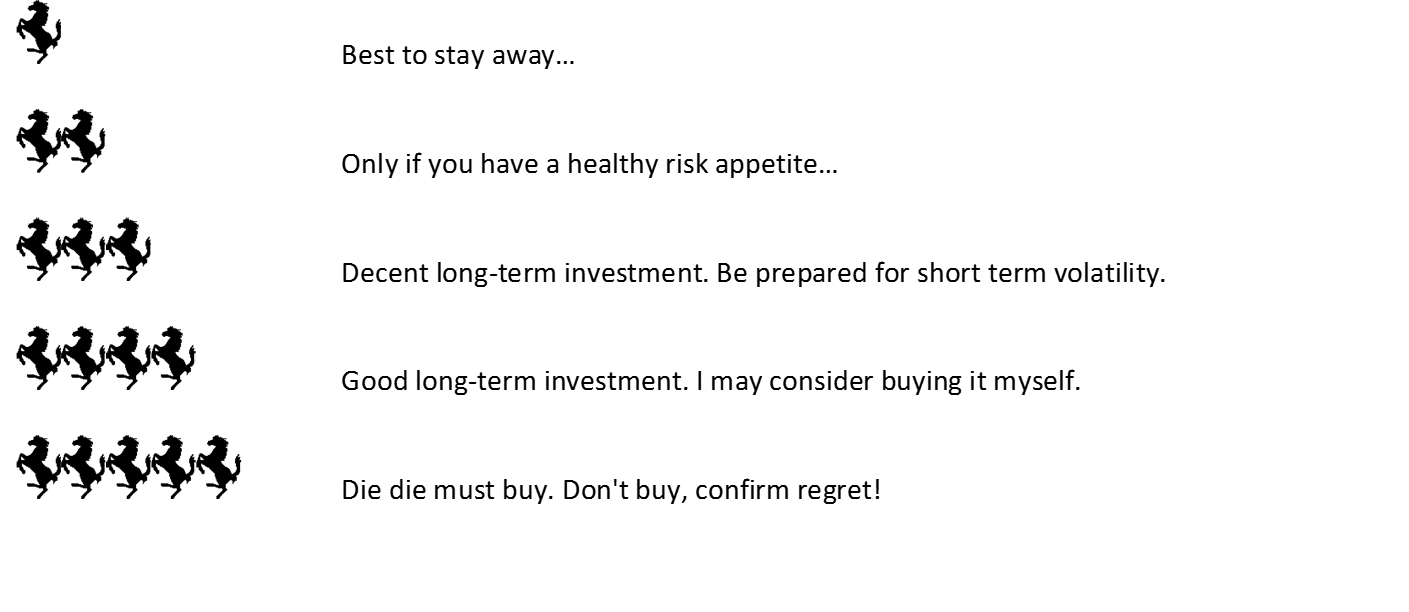

I will give Sasseur REIT a 2 Financial Horse rating, simply because of the guaranteed yield in the first 2 years, and the strong cornerstones and small public tranche. I also like the niche play that this REIT entails, as it could have a lot of upside if the underlying assets perform well.

Thinking of investing in S-REITs for income yield? Find out more about how Financial Horse selects S-REITs for long term investments here.

Sasseur REIT – Financial Horse Rating:

Financial Horse Rating Scale:

Enjoyed this article? Like our Facebook Page for more great articles!

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. I share this with all my email subscribers at absolutely no cost. Sign up for the newsletter now!

[mc4wp_form id=”173″]

[…] Besides ProButterfly, our friends at Financial Horse had also covered this REIT in their article entitled Why I am so disappointed by this 7.5% yielding China REIT. […]

[…] Besides ProButterfly, our friends at Financial Horse had also covered this REIT in their article entitled Why I am so disappointed by this 7.5% yielding China REIT. […]