Channel News Asia ran an article this week on how “Singapore’s Sea is world’s best performing stock. And it can do better”.

A lot of readers have also asked that we do a piece on Sea Limited, and it’s easy to see why given the one year chart below.

This stock has gone from $50 in March to $169 as at today, an unbelievable increase.

In fact, its market cap today of US$80 billion is double that of DBS, and triple that of Singtel. Crazy stuff right?

What is SEA? – Garena, Shopee and SeaMoney

Some of the older gamer will know of SEA by its previous name, Garena.

Sea operates three key businesses:

- Garena (gaming),

- Shopee (eCommerce), and

- SeaMoney (Fintech).

There’s a great description of each arm from their Annual Report:

- Our digital entertainment business, Garena, is a global game developer and publisher with a significant presence in Southeast Asia, Taiwan and Latin America and a global footprint. It was number one in market share in our region by revenue in the combined PC and mobile game market in 2019, as estimated by Newzoo and Niko Partners. Garena provides access to popular and engaging mobile and PC online games that we develop, curate and localize for each market. Free Fire, our first self-developed mobile game, was the most downloaded mobile game globally for the full year of 2019 across the Google Play and iOS App Stores combined, according to App Annie. Garena also exclusively licenses and publishes games developed by third parties. In addition, Garena provides access to other entertainment content, such as livestreaming of online gameplay, as well as social features, such as user chat and online forums. We believe we are the leader in esports in Southeast Asia, Taiwan and Brazil, which strengthens our game ecosystem and increases user engagement.

- Our Shopee e-commerce platform was the largest e-commerce platform in our region in 2019 by GMV and total orders, according to Frost & Sullivan. Since its inception, Shopee has adopted a mobile-first approach and is a highly scalable marketplace platform that connects buyers and sellers. Shopee provides users with a convenient, safe and trusted shopping environment that is supported by integrated payment, logistics, fulfillment, and other value-added services. Our users enjoy the social nature of Shopee’s platform, where users can follow, rate, play micro-games with one another and easily browse for discovery to enhance their retail experience. We also empower sellers with various tools and support such as livestreaming and other value added services for them to better engage with their buyers. We monetize Shopee mainly by offering sellers paid advertising services, charging transaction based-fees, and charging sellers for certain value-added services. We also purchase products from manufacturers and third parties and sell them directly to buyers on our Shopee platform.

- Our SeaMoney business is a leading digital financial services provider in our region in 2019, according to the International Data Corporation. SeaMoney currently offers e-wallet services, payment processing, credit related digital financial offerings, and other financial products. These services and products are offered in various markets in Southeast Asia under AirPay, ShopeePay, ShopeePayLater, and other digital financial services brands.

We began our digital entertainment business at our inception in May 2009, and by 2019, we had expanded our local game operations to cover Indonesia, Taiwan, Vietnam, Thailand, the Philippines, Malaysia, Singapore and Latin America. Our self-developed game Free Fire is also currently available in more than 130 markets globally.

We launched our e-commerce platform, Shopee, in Indonesia, Taiwan, Vietnam, Thailand, the Philippines, Malaysia and Singapore in June and early July 2015, and in Brazil in the fourth quarter of 2019.

We launched our digital financial services platform in Vietnam in April 2014 and in Thailand in June 2014. In the fourth quarter of 2019, we introduced SeaMoney as the overall brand for our digital financial services business.

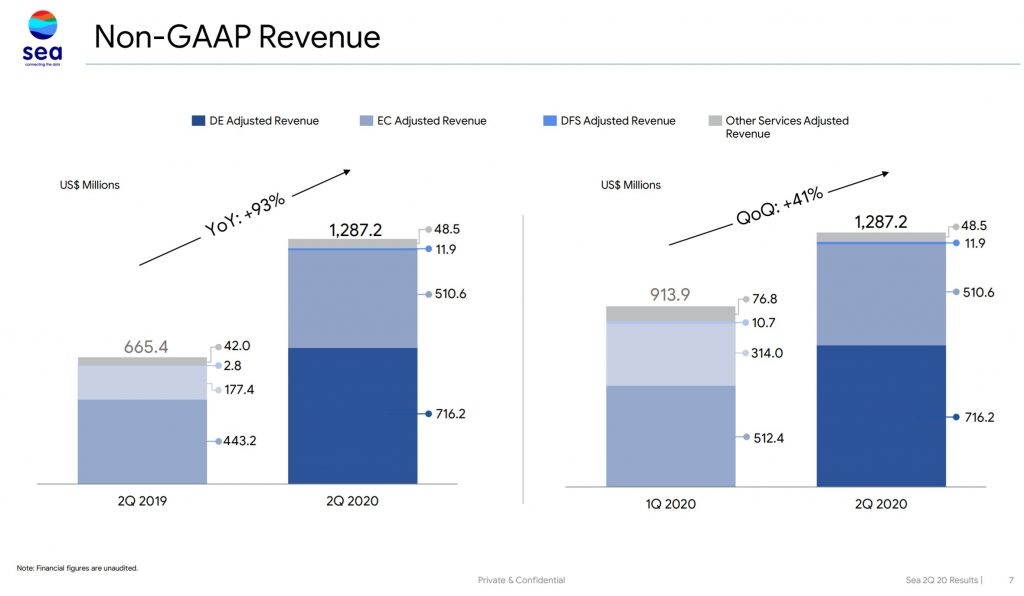

Revenue breakdown of Sea

Revenue charts are set out below, and the biggest revenue generator is Garena, followed by Shopee. The Fintech arm is still very small for now, but it does hold a lot of promise.

Sea doesn’t break down profit numbers by segment, but based on their prior statements:

- Garena is by far the main profit generator, and within Garena most of the profits comes from a few top games like Garena Free Fire (a Battle Royale like PUBG for the gamers).

- Shopee is still in the money burning stage, so it doesn’t make profits. Rather, it burns a ton of cash.

In short, Sea is today, is a gaming and ecommerce business, with the former generating the bulk of the profits. There is also a fintech arm they plan to grow strongly in the coming years.

Bull Case for Sea

With growth / tech companies like this, it’s less important to look at historical earnings, and more important to look at where they will be in the future, when growth stabilizes.

The bull case is easy to see. South East Asia is one of the fastest growing regions in terms of economic growth.

At the same time, Sea is exposed to gaming, eCommerce and fintech, in a region where the digital (and physical) infrastructure so far has been very undeveloped, and where competition isn’t crazy intense like US or China.

In some ways, it feels like China in early 2010s, before the Tencent and Alibaba became who they are today.

If Sea executes well, it’s possible that they could grow into the Tencent and Alibaba of this region. And so far, they’ve executed very well on their gaming and eCommerce strategies, to the point where even this skeptical horse is impressed.

FYI we’ll share commentary on the 2020 crisis every weekend going forward, so for those of you who haven’t signed up for our mailing list, please do – its absolutely free.

It’s a weekly newsletter that goes out at noon every Sunday, and rounds up the week’s posts so you never miss anything.

[mailmunch-form id=”928667″]

Valuations

Let’s run some simple valuations to answer – how much is Sea worth if they become Alibaba / Tencent for South East Asia?

GDP Numbers

Sea has both a gaming and eCommerce arm, so the closest comparison will be Tencent for gaming, and Alibaba for eCommerce.

Some rough numbers:

- Alibaba has a US$800b market cap

- Tencent has a US$660b market cap

At the same time, China’s GDP is $13.6 trillion, while South-east Asia’s GDP is around $2.8 trillion.

So if we assume that Sea grows to one day become as dominant as Alibaba / Tencent, then on a GDP basis, it’s valuation should be ( 2.8 / 13.6 ) * 800 or 660, which means

- If it becomes Alibaba, its fair valuation will be $165 billion

- If it becomes Tencent, its fair valuation will be $135 billion

Sea’s market cap today is $82 billion, so this simplistic analysis shows there’s a fair bit of upside if Sea can execute well.

What does this mean?

So what does the valuation tell us?

It tells us, that if we assume Sea can one day become as dominant as Alibaba / Tencent in South East Asia, it’s valuation can probably double from here.

But that’s a big if, because South East Asia is a very different market from China. Namely:

- South East Asia is disparate – China is a coherent bloc, with a single political system, a single language, and generally similar consumer tastes. Sea is split into many different countries, with very different political climates, regulations, and consumer behaviour.

- eCommerce penetration in China is way higher – China’s eCommerce penetration is about 15% of retail sales, while that for Singapore is 5%. More room for growth, but also real problems to solve along the way.

- Alibaba / Tencent are more dominant – Alibaba / Tencent are juggernauts in their country. Alibaba not only owns the largest eCommerce market share at 56%, it also owns 33% in Alipay, a very strong Cloud business, and stakes in China tech unicorns. Tencent on the other hand, not only has a very profitable gaming business, it also owns WeChat pay (which is second only to Alipay), and it also owns WeChat, and a ton of stakes in China tech unicorns (including Sea). But of course, with Sea they hold both eCommerce and gaming stakes, so it balances it out a bit.

So this indicates that the Alibaba / Tencent comparison may not be fully fair. Let’s say we take 30% off the valuations, that gets us $115b and $94b respectively, so still a fair bit of upside, but not as big as before.

What are the risks with Sea?

What are the risks associated with an investment in Sea? Let’s cover each of the 3 businesses.

Garena (Gaming)

2 big risks:

Gaming drives the bulk of the profits for now, driven by a few games

In other words, concentration risk. Much of the profits comes from a few games, as disclosed by Sea themselves:

In 2017, 2018 and 2019, our digital entertainment business contributed 88.2%, 55.9% and 52.2% of our total revenue, respectively. In addition, our gross profit in 2017, 2018 and 2019 was primarily attributable to the positive impact of our digital entertainment business. Although our other businesses are growing and may contribute more to our total revenue in the future, we expect that our digital entertainment business will continue to contribute significantly to our revenue and gross profit.

…

In 2019, our top five games, which included Free Fire, contributed 94.5% of our digital entertainment revenue.

Gaming is a fickle business. So a game may lose popularity over time, and then you’ll need to find new games.

Some of the best games are not owned by them but Tencent

At the same time, Sea doesn’t own many of the most popular games, other than Garena Free Fire. They simply own the distribution rights. So for now, they’re pretty beholden to Tencent. Fortunately, Tencent is a big shareholder, so they probably won’t want to screw Sea over, but you never know.

For example, some of our most popular games, including League of Legends, Arena of Valor, and Speed Drifters are owned by Tencent Holdings Limited and its affiliates, or Tencent, one of our major shareholders. In November 2018, we obtained a right of first refusal from Tencent to publish its mobile and PC games in certain of our core markets, subject to certain terms and conditions.

Shopee (Ecommerce)

This one is simple – competition.

The biggest competitors in South East Asia will be Lazada, Tokopedia (for Indo) and Qoo10/Carousell (for Singapore).

The table below sets out monthly active users, which shows that in most key markets, Shopee is the number 2 player behind Lazada.

I did a check myself on page views and Google Play store, and this is what I found:

- Lazada – 8.2m views monthly, 100m+ app downloads (Google Play Store)

- Shopee – 11.6m views monthly, 100m+ downloads (Google Play Store)

- Qoo10 – 5.4m views monthly, 1m+ downloads (Google Play Store)

Interestingly, page views seem to say that Shopee is more popular than Lazada, which is a different story from what the App MAUs are saying. Perhaps more people use Shopee’s website, while more people use Lazada’s app?

Whatever the case, I think the conclusion is clear – as at right now, Shopee is a dominant player in eCommerce, definitely one of the frontrunners.

But this contest is by no means over just yet. Lots of time for things to change in the years ahead.

Lazada, Qoo10, and Tokopedia are all very strong contenders, with Lazada particular challenging given their Alibaba financial backing and expertise. And don’t forget the dark horse Amazon as well. They’ve established a small presence here, and who knows if they might suddenly decide to join the competition in a big way.

SeaMoney (Fintech)

The Fintech arm is really small now, so there’s not much to talk about.

Shopee is applying for a digital bank licence in Singapore, and I do think they have a good chance of getting it. With their strong track record of execution, I’m pretty excited to see what they do with it.

That said, the competition will likely be very intense. Not only do you have the established banking sector to contend with (DBS, OCBC, UOB), you also need to fight the fintech players (Grab, Bytedance etc).

Personally, I don’t think SeaMMoney will grow to achieve the kind of dominance that Alipay / WeChat pay achieved in China. China was unique where they didn’t have the existing Visa/Mastercard infrastructure, and they had a period where the banks were content to sit back and let Alibaba / Tencent fight it out.

Don’t see the same circumstances playing out here, which would make it tough to achieve such a dominant lead.

We’ll see though.

Shareholders of Sea

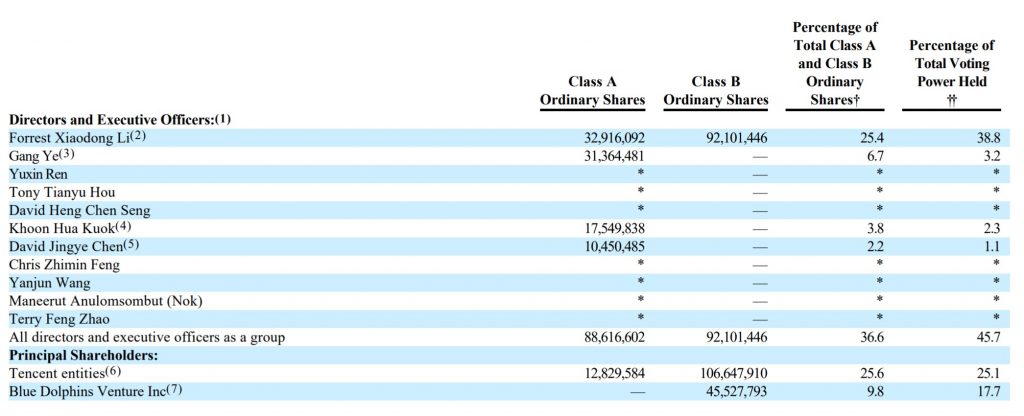

2 big shareholders: (1) the founder, Forrest Li, and (2) Tencent.

Forrest Li holds 38% of voting rights because he has a different class of shares, while Tencent holds 25%.

It’s not necessarily a bad thing – in fact I really like this part. I like it when the founder has a big stake and is actively involved in the day to day, I think that’s crucial to the success of any company.

I also really like the Tencent backing, because that opens a lot of doors, and a lot of games, for Sea.

It does put them up against solid competition from the Alibaba backed Lazada though.

Putting everything together

The way I see it, I really like the space Sea is in – South East Asia, eCommerce, Gaming, Fintech.

All areas with lots of growth in the coming decade.

I also really like Sea’s execution, I think they’ve executed unbelievably well in eCommerce and gaming. And I’m excited to see what they can do with a digital banking licence.

But at the same time, South East Asia is not China. The people are less affluent, and it’s a very disparate bloc, with differing consumer tastes and regulations. It’s also why Shopee decided to split their app and have different teams and tailored strategies for each country.

The problem with this though, is that it may mean Sea may never achieve the kind of margins that Tencent / Alibaba can in China, because costs will never be as competitive. In China you can have 1 team to set up a feature that applies for 1.4 billion people. In South East Asia you need to tailor it for each country.

And realistically, there’s also a lot of competition, in each of the verticals Sea is in. Gaming is the big money spinner now but that can change quickly, and neither Garena nor Shopee has the kind of dominance of Wechat or Taobao just yet.

Would I buy Sea?

At the end of the day, after all the analysis, we have to make a decision.

I do like Sea. The secular tailwinds for this space are massive, so it ultimately comes down to a matter of execution. And so far, they’ve been delivering, very well in fact.

But at the same time, the stock has gone on a 200%+ increase the past 6 months. That’s a lot of growth priced in, and the slightest misstep at this level can trigger a sell-off.

Lockdowns were a great tailwind for eCommerce and Gaming, but as South East Asia starts to reopen again, some of the growth might start to slow.

My personal view here is that some of the price increase might have gotten ahead of itself, at least short term. There could be a possibility of a near term correction.

But long term wise, I do still like the prospects of this company.

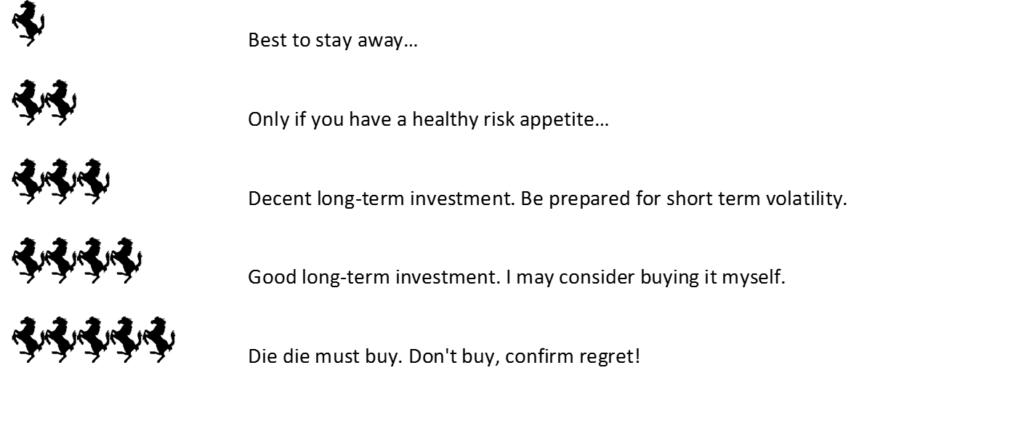

I’ll give Sea a 3.5 horse rating. I like the stock, and I like the execution. But this isn’t Alibaba or Tencent just yet, and some of the recent price gains have been really aggressive. A correction to let some of the air out could actually be good for the longer term prospects of the stock.

As always, this article is written on 9 Oct 2020 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Would love to hear what you think about Sea. Would you buy it at $169?

Share your comments below!

Sea Limited – Financial Horse Rating

![]()

Financial Horse Rating Scale

Support the site as a Patron and get access to my personal stock watch list, as well as my personal portfolio allocation.

Do like and follow our Facebook Page, or join the Telegram Channel. Never miss another post from Financial Horse!

Join our Facebook Group to continue the discussion, everyone is welcome!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

Interesting article. Shopee and sea money are just making them bleed, that’s true.

I’d argue having most of their revenue come from garena free fire is a strength, considering recent developments 😉

Interesting, why do you see that as a strength? Would have thought that’s risky unless that can keep coming up with hit products.

I think if market think they are worth so much, u will never get the price u want. Just follow the trend, mkt dictate the price, not how we value it. Look at most tech stock , they are very high, but they keep going higher. I bought in May. Tech stock and high growth stock are super high in valuation and PE.

Yeah I get where you’re coming from. Under this strategy, how would you decide the right time or price to sell the stock? Curious to hear the thought process.

I honestly feel waiting for pullbacks will only make the investors miss out some big potential gains and I learnt it the hard way for growth tech companies listed in US. Just buy in and DCA across time if you truly believe in it. Just look at big techs like the FAANGs, Microsoft, Nvidia, AMD, Adobe, Square, TheTradeDesk, Mercadolibre – waiting for pullback of big scales rarely occur

Yeah I get where you’re coming from. My concern is that the past decade has trained investors to think this way. And going forward, such strategies may no longer lead to outperformance, especially if we start moving into a more inflationary scenario where value starts to make a comeback. We’ll see though, only time will tell. For now at least, this BTFD strategy has been paying off in spades. 🙂

Don’t wait for pullback- just DCA slowly. There’s never a good entry point for those big growth tech companies listed in US

Hi F H, thanks again for a great article. I am not the most well-read but I do read a fair bit and amongst all the gurus and analysts using hindsight to their “advantage” (definitely not saying you are one!) to up-sell the stock, I have yet to see any of them try to put much (but still simply understood) science to valuing SE in the future as you have just done. Yes, tech stocks or any start-up for that matter is hard to value so well done! Unfortunately, in a bull market, there are many punters and some will get lucky and some of them will even self-professed to become gurus after that :p

Thanks! Glad you liked this article.

Yeah it’s really easy to make money in a bull market, and anyone buying FAANG the past decade would have made a ton of money, regardless of whether or not their thesis was right. I do have my concerns over how the next few years are going to play out though – I think passive / heavy tech strategies are not going to perform as well in this new regime. We’ll see though. 🙂