Okay, clickbaity title aside, this was a real problem that I encountered in January 2019. One of the main trends I highlighted in the Q1 2019 Financial Horse Outlook (you can get it for 2 bucks a month and help support this site ;)) was the crazy run-up in REIT prices.

Indeed this risk rally continued through much of January, to the point where REIT prices are looking quite richly valued. It’s always hard to know when to sell – there’s always a fear it may go up further after you sell it, so I wanted to pen this article to document my thought process.

Note: I’ve used MCT in this article for discussion’s sake, but you can apply this framework to any other S-REIT, and the considerations will be largely similar.

Basics: What happened the past 12 months?

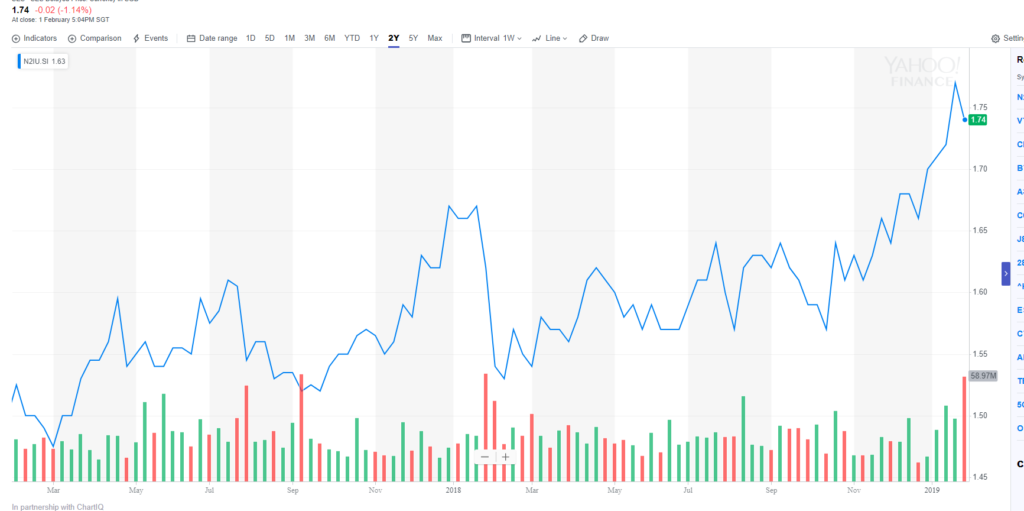

I’ve set out the 2 year chart for Mapletree Commercial Trust below, but you can pull up any S-REIT and the chart will look largely similar.

Here’s my view of what happened since 2017. As you can imagine it’s only my perspective, so take it with a pinch of salt (Big tip for the newer readers, nobody actually “knows” with absolute certainty what truly drives price movements in the market. Those who profess to “know”, are usually just guessing, or kidding themselves.).

- 2017 – 2017 was a great year for just about every risk asset out here. Trump’s election, the wave of fiscal stimulus, and a dovish Fed unleashed a global rally in stock prices.

- January 2018 – After Trump’s tax cuts, the market believed that 2018 would be an amazing year for stocks, and the narrative was all about a “synchronised global expansion”, and January 2018 saw a crazy runup in prices.

- February 2018 – Volatility exploded in February 2018 with a one day jump in the VIX that blew up many short VIX ETFs. This was the start of the tumultuous trading year. It was around this time that the narrative switched from “goldilocks economy” to concerns over an increasingly hawish Federal Reserve projecting 4 rate hikes in 2018. REIT prices fell sharply in this period.

- December 2018 – In December 2018 the narrative switched to a story of slowing global economic growth, and consequently a more dovish Fed. Lower interest rate are supposed to be good for REIT (because REITs are basically highly geared property investments), so REITs benefitted from this.

- January 2019 – Jerome Powell absolutely capitulated, and confirmed the market’s belief that the Federal Reserve would be more dovish going forward. However, this led to questions of: “What is the Fed is worried about?” What do they know that we don’t? If they have turned dovish, is this a negative sign for the global outlook?

Which brings us to where we are today. Understanding the past is always a heck of a lot easier than trying to understand what will happen in the future, which is inherently uncertain.

I’ve set out the pros and cons of exiting a REIT investment now.

Yes, Exit Now

Rise in price not rational

The most commonly accepted reason for the runup in REIT prices is the slowing global economy. If that sounds absolutely ridiculous, that’s because it is.

The popular narrative is that because the global economy is slowing, central banks around the world will ease financial conditions (through interest rates or quantitative easing). This will benefit REITs because they are:

- Highly geared, so a drop in interest rates will reduce interest rate expenses

- Highly exposed to real estate, and looser financial conditions will supercharge real estate like it did after 2009

I’m not so sure if I buy into this argument. Market sentiment can flip overnight. A slowing global economy can easily translate into lower rental reversions and crashing commercial real estate prices, none of which bode well for REITs.

Historical Valuations

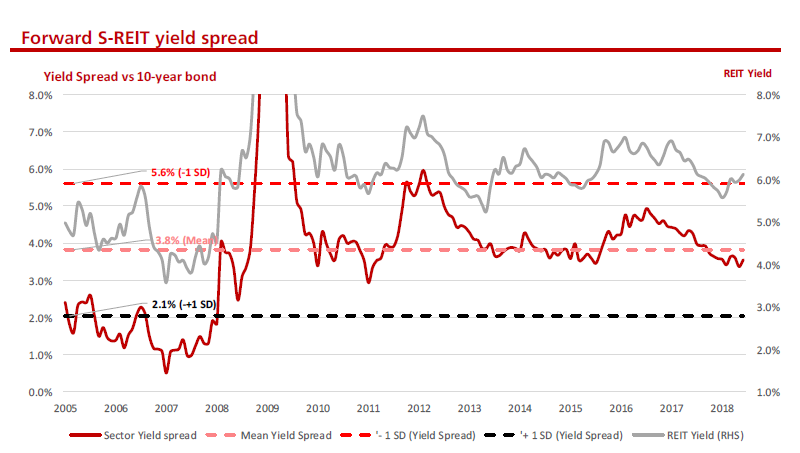

Mapletree Commercial Trust has an annualised DPU of 9.32 cents and a NAV of S$1.49. At its current market price of S$1.74, this works out to about a 5.35% yield, and a 16.8% premium to book. With a 10 year Singapore Savings Bond yielding 2.15%, MCT is trading at a 3.2% spread against the 10 year risk free rate.

The historical average for S-REITs is a 3.8% spread, so we’re definitely on the expensive side here, but it’s nowhere near the bubble valuation territories of 2007.

Lock in gains

During the market freak out over interest rates in 2018, I absolutely loaded up on REITs. My average buy in price for MCT is about 1.55, which works out to a 6% forward yield. One option is to sell all my MCT at the current price of 1.74, lock in a 12% gain (18% counting distributions), and move them entirely to Singapore Savings Bonds to earn 1.95% gain a year risk free. The forward opportunity cost is about 4.05% a year (the distributions that I give up less the risk free rate), but with a 12% capital gains, that works out to 3 years worth of distributions.

Long story short, if I sell all my MCT now, I can move all the money into risk free SSBs, and I have a 3 year window to watch the market. If the price drops below its current price anytime in the next 3 years, I can buy back all my MCT, and I would pocket the gain.

Of course if the price keeps going up for the next 3 years, I’m out of luck. So the million dollar question here is: What is the global macro outlook like over the next 3 years?

Global Macro

And that’s what really worries me. The data out of China these days looks like they’re into the deleveraging phase. With the PBOC easing and manufacturing data crashing, China is in a bad place, and likely to remain that way for 2019.

A trade-war resolution will bring temporary respite, but the fact of the matter remains that China is trying to deleverage their economy, and they’re not going to change their mind simply because of a trade agreement. At the same time, Europe is not in a great place (Italy is in a technical recession) and Australia is in the worst housing crisis in 30 years. The US is a big question mark, recent economic data looks strong, but inflation remains weak, and business sentiment is low, and Powell’s Federal Reserve seems to be worried about something. Emerging markets are actually having a good time because of the weaker USD, so there’s a bit of a bright spot there.

Long story short, the outlook over the next 12 to 24 months suddenly looks a lot murkier than where it was just 12 months ago. Locking in a 12% gain (counting distributions, it’s a 18% gain for 1 year holding period) and moving entirely to risk free bonds is starting quite attractive at this time.

Everybody is recommending REITs

The other thing that really worries me, is how popular REITs have become. Over the past week, I’ve seen REITs being recommended at popular investment events, by financial bloggers, and by big banks.

By contrast, when I loaded up on REITs early last year, I remember how absolutely everyone was saying that REITs were a horrible investment because of the rising interest rate environment.

The fact that the popular sentiment has flipped 180 degrees in a short span of time worries me greatly. I’m definitely no Warren Buffett here, but there’s a lot of truth in the saying that “what wise men do in the beginning, fools do at the end”.

No, Keep Holding

Buy and Hold beats market timing

On the flip side, there is the argument that a buy and hold investor outperforms active market timing, over longer period of time. I absolutely get this, because if I get my call on the global macro wrong, and it turns out to be an amazing 2019, I’m actually sitting out on the capital gains and distribution gains.

It’s definitely possible to outperform or underperform the market through active market timing, it all depends on whether you’re right. Some investors like George Soros are able to do it consistently, others don’t. I’m not so sure which camp I fall into.

Timing matters

Timing matters as well. I could be absolutely right on my macro call on a 12 month horizon, but that doesn’t mean that MCT is not going to go up to S$2 by March.

A lot of guys use technical analysis to predict short term movements in price, but I always thought it was absolute rubbish. It doesn’t matter what chart pattern you have on a puny counter on the SGX, if the PBOC lowers interest rates, everything goes up anyway.

Short term price movements are incredibly hard to predict, but my gut feel on this, is that there may be a couple more weeks (months?) left of price appreciation here. I could be absolutely wrong though.

MCT is a buy and hold forever investment

I kind of get the irony in this. In one of my first ever articles on Financial Horse, I professed my love for MCT and why I loved it as an investment. All the points there remain valid of course. But in investing, identifying a good investment is not enough. You also need to get a good price for it. S$1.55 is a great price for MCT, and if you offer it to me again at that price, I would probably buy more. At it’s current price though, it’s looking a lot less attractive with all that is going on in the world.

I definitely wouldn’t buy it at it’s current price, but whether I would sell it, is a more interesting question.

Closing Thoughts

After this entire article, I’m not so sure if I’m anywhere closer to answering the question of whether to sell MCT, or the rest of my REITs. But that doesn’t matter, because I don’t want anyone to follow my decision.

Any decision I make is unique to my financial situation, and if you take a look at my personal portfolio (available on Patreon), I have a large portion of my assets in risk free SSBs, bonds, CPF etc. So even if I lose the entirety of my equity portfolio, I could probably still go on living (but with a very bruised ego).

Any decision you make, has to be unique to your financial situation as well. If you popped 10k on MCT a year ago thinking that you want to make some quick money, you should seriously consider exiting now. If you’re a retiree who just wants a safe investment for income, and you don’t want to monitor the financial markets regularly, you’re better off just holding.

Till next time, Financial Horse, signing out! Here’s wishing all readers a very happy Lunar New Year!

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. Enter your email below to receive a copy!

[mc4wp_form id=”173″]

Enjoyed this article? Do consider supporting us and receiving additional exclusive content!

Like our Facebook Page for more great articles, or join the Facebook Group to continue the discussion!

A quote from Howard Marks about Wiseman. Absolutely right.

I think it is a good idea to take some cash off the table, it is tricky risk environment now.

Thanks for the comments! Yes, I’m inclined to agree with you.

Not sure whether u guys are happy to receive feedback through email?

Absolutely. Drop me a note at [email protected]

Using an asset class based investment portfolio approach, we could increase or decrease REITs holdings, in relative to the weightage of the other asset classes such as non-REIT equities and bonds.

That’s a good point. Although from a purist angle, that would entail selling REITs and moving to equities. In the current market, I’m more inclined to sell and move to risk free assets like SSBs.

I agree with you.

I too am into this worry. It is not just REITs but the whole market.

Well, over the next 12 months, we will see how this plays out!

MCT is 1 of my best performing REITs and I like vivocity.

I agree with your comments with regards to the sudden overwhelming recommendations to buy REITs. Was thinking of deleveraging as well.

In any case MCT dpu may be impacted for the next few months as dairy farm move out and ntuc move in.

MCT is also one of my best performing REITs. I’m thinking of lowering exposure to all my REITs, the macro environment has become a lot more tricky.

Cheers.

Why not locked in a portion of your MCT holdings instead, assuming the divested amount is large enough to justify the trading commissions. 12% gain is still significant and the probabilty of MCT to hold 1.74 when the economy slowdown is not high.

Yep that’s definitely an option as well. Unit price is now 1.82, which does increase the gains by a bit.

Yeah well, after sending my money back home to Europe for the past 3 years, your old MCT article I read in December finally made me want to invest locally (“Listen up y’all, I’m thinking about buying Vivo City”).

So I went down to the CDP office and proudly created by account (took them 4 weeks to confirm), waited another 10 days for DBS to open my trading account. And now that thing went up from 1,64 to 1,81 in the meantime 🙂

Lesson learned: I bookmarked your site so I wouldn’t waste time in the future 🙂

Hi there!

Thanks for this great comment, truly made my day! Yes, MCT is trading really high right now, I’d give it some time before looking to open a position ;).

Glad to have you on board, and welcome to Financial Horse!

Interesting thoughts about REITs although I’m always wondering what’s the big deal about a small change in the price of a reit when it’s not capital gain or loss that I’m after when it’s the passive income that I receive. I’ve also noticed that the yield varies inversely with the price. If price goes up, the yield goes down and vice versa. If that’s true, it’s akin to hedging, doesn’t it? At the end, I think the yield from interest rates or SSB is still paltry compared to REITs. Can you tell me if there’s a flaw in my thinking? Thanks.

Yes that’s absolutely right. If you’re intended to hold long term and have no plans to sell, your attitude is perfectly fine (in fact, it may even be recommended). Short term trading is usually a fool’s errand to maximise gains.

Hi, Thank you for your articles, they are very interesting

.

I am a new investor and I do own some shares of Mapletree NAC too.

Same as you, I have been wondering if I should sell them after the current rally (~+10%).

There are 2 points that stops me, and I would value your insight about them:

1-Since I am quite new about REITS I was wondering what would be the impact of such a high value for the management team. Do they get more leverage to ensure the futur of their operations ?

2-I bought Mappletree with the idea to build a dividend portfolio. So instead of selling it, wouldn’t be right to consider that I got a good stock at a bargain price, thus I should keep it? Moreover the PV act as a insurance against market volatility and down time ?

Thank you

Hi there, welcome to Financial Horse!

My replies below:

1. Yes, a strong management team matters a lot for a REIT. There are many ways to improve a REIT performance, from proper asset management to good financial management. More importantly though, it’s really about the strategic direction set by the sponsor, and Mapletree is a pretty good sponsor (in my books).

2. Yes, absolutely. If you got it on the cheap, you can absolutely hold it long term. The purpose of this article was to discuss the possibility of flipping the stock for short term profit and buying it back later. In the end though, I never sold my Mapletree REITs. 🙂