Note: This article is a premium article that first appeared on Patron. This was written in 2020, but the underlying industry structure remains very relevant today.

If you enjoy articles like this, do consider supporting Financial Horse and getting access to premium articles, my personal stock watch list, as well as my personal portfolio allocation.

A couple of Patrons have asked me to share some thoughts on how I view the entire semiconductor space, and why I selected TSMC, AMD and Micron for the FH Stock Watch.

So here goes today’s article.

There’s no denying that this is a very technical topic, so while I’ll tried to keep it as simple as I could, there still is a minimum level of technical detail required.

If you need any clarification, or if there’s any area I left out / am incorrect, just leave a comment below!

Basics: Semiconductors are today’s infrastructure

The semiconductor industry today is what the construction industry used to be 20 to 30 years ago.

Back in the 20th century, if you wanted to invest in infrastructure, you’ll go for something like Caterpillar, because when countries build roads or highways, they need bulldozers right?

In the 21st century however, most of the “infrastructure” has now gone digital. When governments inject fiscal stimulus, it’s no longer just roads we’re talking about, it’s a digital transformation. It’s investing in cloud infrastructure, data centers, 5G networks – all ultimately powered by semiconductors.

Now in the 1980s to 1990s, the semiconductor space was highly fragmented. It was a low margin industry, high pace of change with multiple players. It was a dog eat dog world.

Over time, the low margins and high capex added up, resulting in a survival of the fittest situations. The weaker players went bankrupt or were bought over by the stronger ones.

And today, the industry has consolidated into one or two major players per sector.

The main sectors here, are:

- Foundry

- Processor (Desktop)

- Processor (Mobile)

- GPU

- Memory

- Specialised parts (eg. controllers, wireless modem etc)

We’ll run through each individually.

Don’t forget to join our Telegram Channel and Instagram!

[mailmunch-form id=”928667″]

Fabrication Facility (Foundry)

Before we really go into the details, we need to talk about Foundries.

These are basically factories that build semiconductors.

Moore’s law is the observation that the number of transistors in a semiconductor doubles about every two years. This doubling is basically what has driven the entire IT revolution.

But to keep up with Moore’s law, manufacturing techniques have to be continually improved. To squeeze double the amount of transistors into a semiconductor every 2 years, the manufacturing process needs to get smaller and smaller.

So manufacturing techniques a decade ago could have been on the 100nm node (manufacturing size), but the cutting edge techniques these days rely on the 7nm node.

And because the capex requirements associated with transiting to a new node are so high (estimated cost for a 7nm manufacturing facility is around $3 to 5 billion), it has created a winner takes all industry.

The winner who can advance to a new manufacturing node ahead of the others will get the lion’s share of profits, which it can then use towards R&D for the next node, creating a snowball advantage over time.

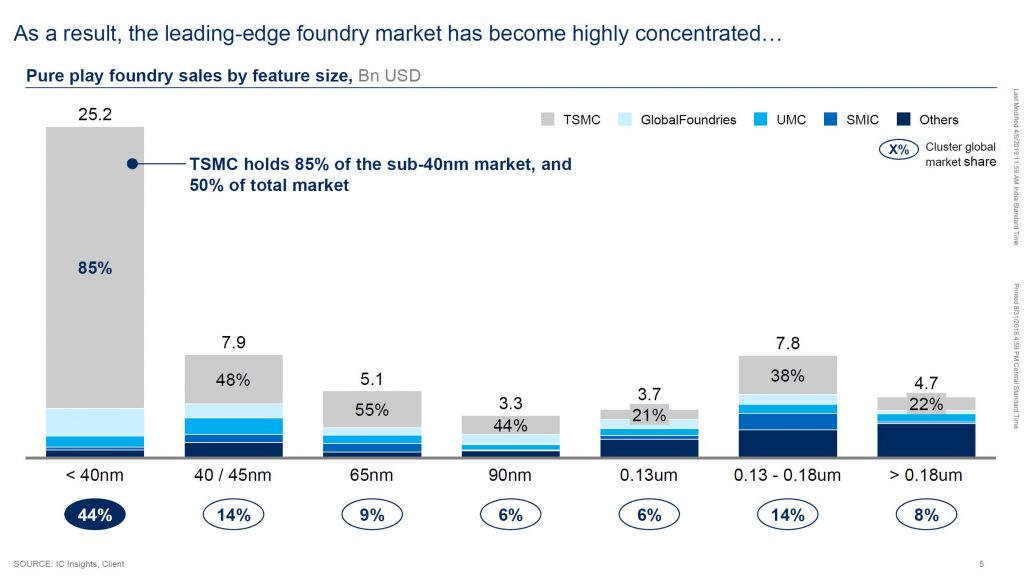

Over time this effect compounded, resulting in the industry below.

Basically, only 1 player (TSMC) controls 85% of the leading edge, sub-40nm market.

And in the cutting edge, 7nm market, there is really only 1 player that can build those chips, TSMC.

A couple of you have asked me about Intel’s plunge in share price the past week.

For those who missed it – Intel has been on the 10nm node for a few years, and they’ve been trying to catch up to 7nm. The past week, they announced that there’s been a slip in production schedule, and they’re probably not hitting the 7nm node until 2022 – 2023. This sparked a 16% plunge in their share price on Friday.

This illustrates:

- The difficulty in node transitions at the cutting edge – Even a behemoth like Intel with a massive R&D budge ran into production issues, let alone smaller players. Cutting edge node transitions are tough.

- The dominance of TSMC in the short term – TSMC themselves cannot increase production massively in the short term, because each Foundry has a fixed capacity, and a new Foundry takes years to build. This actually creates a shortage in production capacity, as most of the leading players have to rely on TSMC for 7nm production. This gives them pricing power, which leads to bigger margins for TSMC, and smaller margins for everyone who relies on TSMC for manufacturing.

In recent years, Samsung has been investing heavily in cutting edge nodes as well, with a goal to becoming a no. 2 foundry.

For now though, much of Samsung’s production capacity is reserved for their own Samsung line of processors. Many competitors are reluctant to use Samsung’s foundries because Samsung is a competitor in the consumer market.

For example – Apple used to subcontract to Samsung to manufacture their processors, but switched to TSMC when Samsung smart phones started emerging as a major competitor to Apple. Even though the Foundries are technically china-walled, competitors were still afraid of trade secrets being lost to Samsung.

This was another factor that contributed to the rise of TSMC.

Processor (Desktop)

These are the CPUs that go into your laptop, or desktop.

There are 2 main players: Intel, and AMD.

Intel is the massive, established player with large institutional support. AMD almost went bankrupt a couple years back, but they’ve recovered very strongly since with a new line of chips.

Intel’s traditional strength is manufacturing their own chips inhouse. This has allowed them to enjoy 50%+ margins, which are unbelievable in this industry.

AMD by contrast, sold their Foundries many years back, and has outsourced all manufacturing to TSMC.

As mentioned above, Intel has been stuck on the 10nm node for a while now, while AMD being on the 7nm node via TSMC, and design improvements made the past few years, has caught up with Intel on performance the past few years.

And in this industry, performance is everything. Clients may stick with you short term due to existing relationships, and hassle of changing tech. But longer term, if the performance is sub-par, nobody will stay with you.

So Intel’s delay to the 7nm node is highly troubling. If short term, they’re going to lose the performance lead to AMD (they already have in power efficiency metrics because 7nm is more energy efficient), they may concede significant market share to AMD, which would be disastrous for Intel’s share price.

Intel has promised performance upgrades while remaining on the 10nm node though, but it remains to be seen if they can deliver.

Processor (Mobile)

Then we have mobile processors, that go into smartphones or Tablets.

The main players are: Apple (they design their own A series processors), Qualcomm, Mediatek, Hisilicon (Huawei), Samsung.

Of these, Apple, Qualcomm, Mediatek and Hisilicon use TSMC Foundries for manufacturing, while Samsung manufactures inhouse.

Designs are based on the open source ARM architecture (anyone can use it).

So because everyone uses ARM architecture, and TSMC manufactures the chips, it has resulted in an industry where performance between players is not fundamentally different.

There are minor differences between players (eg. Apple will optimize their processors for iOS etc), but neither company necessarily has a commanding lead over the other.

Graphics Processing Unit (GPU)

GPU are the graphics cards that go into your computer to power games and graphics designs.

In recent years, GPUs have been used heavily for machine learning purposes, creating an explosion in demand.

There are 2 main players: Nvidia, and AMD.

Nvidia is basically the intel of the GPU space. Big, established, lots of institutional support.

AMD again, almost went bankrupt a couple years back, but their recent GPUs are looking decent competitors to Nvidia at the mid range.

For now, the top end GPUs are dominated by Nvidia, but we may see that change with AMD’s new Big Navi line of GPUs (that will power the PS5 and Xbox – and are rumoured to be significant upgrades in power).

The new series of PS5 and Xbox will also create big demand for AMD GPUs and Memory (that we’ll discuss below), because they use cutting edge specifications. The bigger the demand for game consoles, the more bullish I am for this space.

Memory (DRAM and NAND Flash)

Memory is split into 2 big markets. DRAM and NAND Flash. We leave out mechanical hard disks because that’s a sunset industry that will eventually be replaced by NAND Flash.

DRAM is the short term memory that goes into phones, computers, servers etc. All devices will require RAM to run.

NAND Flash is the solid state storage that goes into phones, computers, servers etc. It is used for longer term storage, and it’s significantly faster than mechanical hard disks.

So when your new phone says 8 + 128, the 8 refers to 8GB or DRAM, while the 128 refers to 128 GB of NAND Flash.

The industry is broadly dominated by 3 players. 2 Korean players in Samsung and SK Hynix, and US based Micron.

Memory is a very commoditized product, because memory from Samsung is interchangeable with memory from Micron.

There is very little to differentiate Micron from SK Hynix or Samsung.

So like any commoditized product, it is very cyclical, with big boom bust cycles.

So with memory players like Micron, you want to really watch the memory cycle closely. You buy when there is oversupply and prices plunge, and you sell when there is undersupply and prices soar.

No different from how we play oil or real estate.

Specialised parts (eg. FPGA, Communications etc)

Finally, we have specialized parts like FPGA, controllers, wireless modems etc.

These are basically specialized parts that are designed to perform specific tasks. Big players will be guys like Xlinx.

The chart below gives you a broad overview of the entire spectrum of Semiconductor players and where they sit relative to each other.

Investing in Semiconductors

It’s been a really long article, so I’ll share more about why I picked TSMC, AMD and Micron in Part II of this article. I’ll also touch more on the difficulty of China in catching up on Semiconductors.

For now, I wanted to comment generally on the semiconductor industry.

Because it’s such a technical area with a high pace of change, it isn’t so suitable to buy and hold strategies (unlike an industry like real estate where you can buy and hold REITs).

As Intel’s announcement last week illustrated, any performance decline or loss of market leadership can result in disastrous results. With semiconductors, it is best to keep up to date with latest developments in the particular sector you’re investing in.

One way out of course, is to go with ETF investing (via SOXX), as a way to gain broad exposure to the industry. But the performance might not be the same.

Longer term though, I am incredibly bullish on this sector. Semiconductors run the world in the 21st century, and are the backbone of the entire cloud / digital infrastructure. Investments into data centers, cloud, digital transformation are all bullish for Semiconductor stocks. And as we’ve seen, the industry is relatively consolidated, which makes it easy to buy 1 or 2 players to get exposure to this space.

The biggest tail risk though, is the rise of China manufacturers in the Semiconductor space. If China can built the same part at a fraction of the cost, that’s big margin loss for the existing players.

We’ll save this for Part II of the article.

Note: This article is a premium article that first appeared on Patron. If you enjoy articles like this, do consider supporting Financial Horse and getting access to premium articles, my personal stock watch list, as well as my personal portfolio allocation.

Also good to keep an eye on those selling the picks & shovels to those rushing into this semicon gold rush e.g. Amat, Lrcx, Klac. You know the cliche story about who got rich from the California gold rush … yeah Levi’s.

To hedge against non-systematic risk, perhaps a portion into etf like Soxx or Smh, the specific % depending on individuals’ characteristics.

Yeah really good points. Thanks for raising this Sinkie.

Been following your blog for awhile, feel that this article should have been written like last year when semi cons, was very obvious beneficiary of the lock downs…. Own some local semi cons since last year and they did very well for me, would wish to expand to US market semi cons this year, How would your rate SMH ( ETF which has abit of everything in it ) Would really like to hear from your views on Semi cons ETF too. And in which region should we be looking at ? China, ASIA or the United states ? Thank you so much.

Thanks for the support!

Yes – this article was indeed written last year. But it was released exclusively to Patrons back then, do sign up for the exclusive content if you’re keen: https://www.patreon.com/financialhorse

Semicon ETFs are perfectly fine. I think it’s just a massive growing sector the next 5 to 10 years, China, Asia, US are all fine.

For now though, most of the big IP names are US (Nvidia, AMD, Micron), and the big fabs are Asian based (Samsung, TSMC). How China will fit into the picture isn’t so clear right now yet.

Just to add – it’s back to the classic ETF vs Stock picking debate. If you pick well, stock picking outperforms. Otherwise, ETF gives you an average return, which is not too bad either. Goes back to risk-reward + who you are as an investor!