Quite a few readers have asked that I do a piece on SIA. And it’s a really interesting topic, so I was happy to oblige.

A reader also helpfully sent across the following questions, which we’ll use as the framework for discussion today:

1) Some interpretation about the complex structure Rights + MCB

2) The valuation of SIA after the rights/MCB?

3) Your recommendations to FH followers on SIA – whether we should subscribe to entitlement or even excess rights?

FYI we’ll share commentary on the 2020 crisis every weekend going forward, so for those of you who haven’t signed up for our mailing list, please do – its absolutely free.

It’s a weekly newsletter that goes out at noon every Sunday, and rounds up the week’s posts so you never miss anything. Sign up below (you get a free guide when you sign up):

1) Breaking down the Rights Issue and MCBs

All of the relevant documents are available here: https://www.singaporeair.com/en_UK/sg/about-us/information-for-investors/rights-issue/.

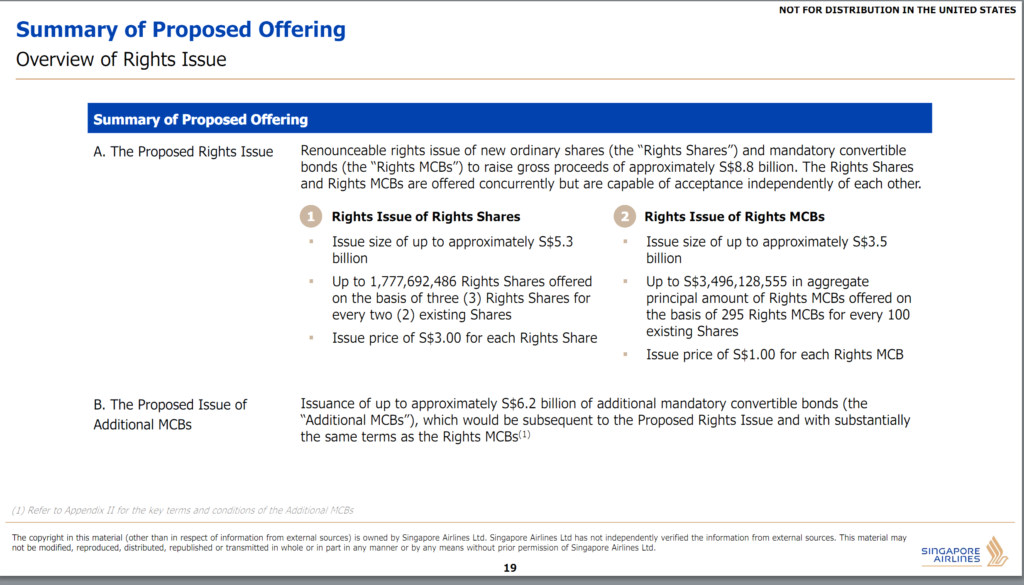

Very simply, SIA’s “bailout” is split into 3 parts:

- Rights issue of Rights Shares

- Rights Issue of Rights Mandatory Convertible Bonds (MCB)

- A proposed further issuance of Additional MCBs

Parts 1 and 2 are happening right now, whereas Part 3 may happen later depend on how much cash SIA needs down the road.

Part 1 – Rights issue of Rights Shares (raising $5.3 billion)

Plain vanilla rights issue. For every 2 shares in SIA you own, you get3 rights at $3.00 each.

You can either choose to (1) exercise the rights to get a share in SIA – in which case you need to pay $3.00 per right, or you can (2) sell the rights on the open market – in which case you take the price of the rights on the open market, which is about $3.8 as of today.

This will raise a total of $5.3 billion for SIA

Part 2 – Rights Issue of Rights Mandatory Convertible Bonds (MCB) (raising $3.5 billion)

The MCBs are more unique. I don’t think I’ve seen these ever being offered to retail investors, at least not in this debt cycle.

The MCBs are pretty technical, so we’ll skip all the mumbo jumbo and go right into what it means.

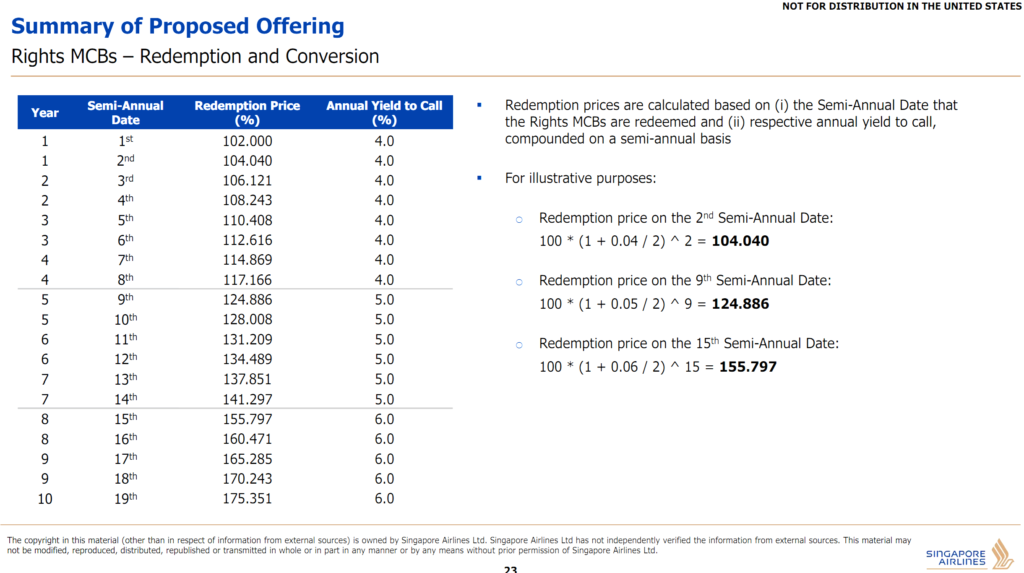

Imagine that you own $1000 of MCBs.

These are zero coupon, so you’ll not get paid any interest (or coupon) each year.

But these MCBs can be redeemed by SIA any time within 10 years.

And on redemption date, they will pay you $1000 (being the principal) + an extra amount equivalent to the interest that would have been due on the bonds for the duration that you held it.

And the interest is 4% for the first 4 years, 5% for year 5 to year 7, and 6% for year 8 to year 10.

So basically, if SIA redeemed the bonds in year 4, you will get no interest payments for the first 4 years, but on redemption date you get a lump sum payment equivalent to $1117.166, which is the $1000 you put in originally, and $117.166 which is equivalent to the 4 years interest at 4% a year.

If redeemed in Year 5 – then SIA basically pays 5% a year to you, but as a lump sum at the end. Full numbers are set out in the table below.

So no interest is payable by SIA every year, which is great because nobody knows when COVID19 goes away. This gives SIA lots of flexibility to repay the MCBs only when cash flow has recovered to a point where they are comfortable paying these off.

What if SIA doesn’t have the cashflow to redeem the MCBs? Then in year 10, you still get paid a lump sum of $1,806.11, which is the $1000 principal and 10 years’ worth of 6.0% coupons. Only difference is that instead of being paid in cash, you’ll be paid in SIA shares.

So you will get the number of shares equivalent to $1,806.11 dollar value – based on S$4.84 per Share (subject to adjustments). This works out to roughly 373 Shares per 1000 MCBs.

For every 100 shares in SIA you hold, you will get 295 Rights MCBs.

The MCBs will raise $3.5 billion.

Part III – A proposed further issuance of Additional MCBs (up to $6.2 billion)

Part III is basically just an option to issue even more MCBs down the road, up to $6.2 billion more.

So if 3 months (or 1 year) later SIA is still not doing well, then they can tap the additional MCBs to raise up to another $6.2 billion.

Same mechanic as how they work in Part II.

Summing it up

So to sum it up – for every 100 shares in SIA you hold, you get 150 rights shares at $3 each, and 295 rights MCB at $1 each.

Assuming a pre-rights but post-COVID price of about $6 per SIA share, this means that for every $600 in SIA shares you hold, you’re being called on for $450 in rights, and $295 in MCBs, totaling $745.

That’s quite a big capital call from shareholders now that I think about it.

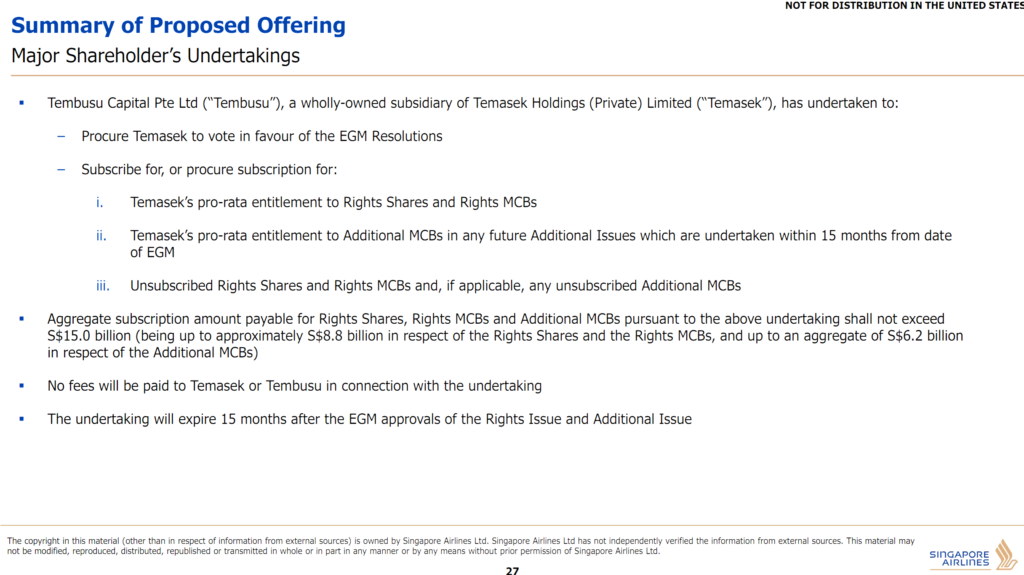

Undertaking from Temasek

In any case, Temasek is backstopping the entire offering.

So if you don’t want the rights or MCBs, Temasek will buy the remainder.

The total amount being raised is $8.8 billion Part I and II, and up to another $6.2 billion in Part III.

To put things in contrast, SIA’s current market cap is about $11 billion, so that’s a big bailout package.

2) The valuation of SIA after the rights/MCB?

This was what I wrote for Patrons back in March:

“The key thing about this bailout is that it is massively dilutive.

Some back of the envelope calculations – assuming an original share price of $9 pre-COVID19, after the dilutive rights, the final price of the shares will be about $5.4, give or take.

So assuming SIA recovers to its pre-COVID19 earnings and valuations, the share price for SIA should be around the $5+ range (really rough calculations).

Which means the current post-rights effective share price of SIA of $4.4 isn’t looking so attractive (assumes you buy now and subscribe for the rights in full).

I haven’t taken a look at SIA so closely yet because I think it’s way too early to be touching airlines, but ballpark number to get me interested will probably be in the $2 to $3 range.

It may never get to that price, in which case I just skip the stock entirely. Too many other bargains out there, with bigger upside and less risk.

If I did want to play SIA though, I think the right time to start looking is probably when the rights entitlement start to trade.”

Traditionally, the best time to get into a stock is when the rights entitlement start to trade. Applying that here, it would mean now is the perfect time to open a position in SIA if one is so inclined. But of course, I do have my doubts on whether that rule will hold true here.

Valuations

I am a big fan of the rubbish in rubbish out theory.

This is the simple idea that any model you build, is only as good as its inputs. And to build a valuation model of SIA, what is the most important input that I would need right now?

If you guessed earnings, you’re absolutely right. If you can tell me what SIA’s earnings will be like for 2021, and 2022, and 2023, I can give you a valuation for SIA.

So let’s go back to basic principles. What do I need to forecast SIA’s earnings? I need to know revenue – and for this I need to know what international airtravel will be like in 2021 and out (because Singapore doesn’t have domestic air travel).

So I basically need to know what the COVID19 situation will be like, what kind of measures global governments are taking to combat the spread, and just much of a pain in the ass it will be to take an international flight. Because if I need to do a swab test and mandatory quarantine each time I cross international borders, I’m probably just not going to travel internationally for a while.

The CEO of AirBnb came out with a bold prediction what going forward, travel for business will drop drastically (replaced by Zoom calls), and people will travel more for leisure. Didn’t make sense at first, but the more I think about it, the more I appreciate the genius of this comment. Nobody wants to put up with all that hassle for a business trip, but a leisurely trip to Japan for some Sashimi? Hell yeah.

But coming back, I think the simple answer here is that no one has any clue what international travel will be like 3 months out, 6 months out, or 12 months out.

So valuation of SIA? I have no clue.

Ballpark numbers

Okay but let’s run some rough, ballpark numbers to give ourselves a gauge.

Taking SIA’s pre-COVID price of about $9 per share, and adjusting for 3 for 2 rights are $3 per share, we have an adjusted price of about $5.4. So if everything recovers and we go back to Dec 2019 flight numbers and valuations, SIA will go to about $5.4, which is about a 40% upside from here.

Investing is about risk reward, so the question is how likely is that 40% upside, and how much are you risking for that 40% upside.

And genuinely – your guess is as good as mine.

3) Your recommendations to FH followers on SIA – whether we should subscribe to entitlement or even excess rights?

Okay first things first – I don’t do recommendations.

Investing is a very personal decision, and you need to decide based on your risk appetite, and your goals. I can’t make that decision for you. It’s your money, and yours alone.

All I can do it share my thought process, and hopefully it will be helpful for you in making your decision.

What would I do?

There are 2 kinds of people in this world. Those who think that air travel will recover over the next 2 to 3 years. And those who think that there is no way of knowing for sure.

Which now that I think about it, is kinda like how religion works.

Anyway, I belong in the second camp – the agnostic camp. This camp includes guys like Warren Buffet, who some would say has lost his edge in his old days.

Whatever the case, my position is that it’s impossible to know for certain how air travel will play out the next 2 to 3 years. Maybe COVID19 goes away, and everything goes back to normal. Maybe the virus mutates into a more deadly strain, and it’s the end of the world. Maybe we are just stuck in this status quo where you need a 2 week quarantine when you cross borders.

The way I see it, all of them are possible futures, and because this isn’t a financial problem, I don’t see how I can assign probabilities to each of the possible futures.

So if I buy now, I’m just making a blind bet that everything will get better, and to convince me to do that, I need a big upside, and a big margin of safety.

If I were a shareholder?

I think if I were a shareholder (and I’m not), I probably would have sold all of my shares in April when it was at the $6 range. I just have no clue what air travel will be like for the next few years, and at $6, the price was too good to not exit.

If I somehow missed the boat then, and held on till now, then I think I have no choice but to take up the rights, because otherwise I would get diluted out (in any case the rights are cheaper than the market price of the shares, so it’s a no brainer). History shows that the time when rights are selling are usually a poor time to exit your investment, so I would take up the rights and hope for a small bounce after this goes away.

This also gives me time to watch COVID play out. If everything clears up quicker than expected, SIA could just turn out to be a great investment.

If I were not a shareholder?

As a non-shareholder, I think there are 2 potential ways to play this:

Short term flip

One way is to buy SIA now at the $3.8 range. Short term there is the possibility of a bounce into $4+, and if it does, I exit the investment completely.

But the question really is how much am I risking for this return.

This is essentially a trading-style strategy, which I am not good in, so I’ll leave it to the traders out there.

Long term investment

A lot of readers have asked me for my view on SATS. And the views are very similar to SIA.

The simple answer is that I don’t know that the recovery will look like. If I buy into airtravel now, I’m basically taking a position that airtravel will eventually recover in some form.

So then the question is one of pricing. With all the uncertainty, at what price would I be tempted in?

I think for SIA, I will stick to the ballpark I threw up in my original Patron post back in March: the $2 to $3 range (between $2.00 and $3.00). Subject of course, to no material deterioration in the COVID19 situation.

That said, I genuinely don’t think SIA will ever drop that low, so I’ll probably never end up buying this stock. But that’s fine too, because there are lots of other great buys out there.

MCBs look really good though

I really like the MCBs though.

I think the best way to play SIA could be via the debt, rather than the equity.

With debt you’re taking on credit risk rather than P&L risk, which looks a lot more attractive.

The Rights MCBs will be listed on the SGX in due course, so it will be interesting to watch the pricing and liquidity there.

Closing Thoughts: View on Temasek Bailout

A blogger had a great post back in March on SIA’s cashflow issues:

What this means from a cashflow point of view is that should the situation prevails, the company is burning approximately $1,461m in cash every quarter, or $487m every month.

The company’s balance sheet is in precarious condition by having only $1.5b in cash while having a borrowings that is almost 4 times the amount.

Out of those borrowings, $3.75b belongs to the bond issuance which they did over the years while the rest of the $2.35 belongs to bank borrowings.

What is more worrying at this point is that the company have a $500m bond that is maturing in Jul 2020 this year, which is simply just 3 months away from today. The next call will mature in Apr 2021, amounting to a smaller amount of $200m.

There’s a fair bit of assumptions going in, but the core message is there – without a bailout, SIA was in real danger of running out of cash.

So the way I see it, this bailout is one that absolutely needs to be done.

Every country is bailing out their airlines.

Singapore would be foolish not to do the same. SIA is our national carrier, and the pride of our nation. It would be a shame to undo all that hardwork because of some squabbles over how to bail them out.

So as investors, we can criticize how the deal was done, and maybe we can even come up with a better idea, but we must recognize that it had to be done, and done fast. It’s easy to criticize when sitting in the comfort of our homes, but when you’re in the midst of things, scrambling to put together a $15 billion bailout package and satisfying all stakeholders, it’s a lot harder than you imagine. So I would be slow to criticize how the bailout package was put together.

What do you think? Share your comments below!

Support the site as a Patron and get market and stock watch updates.

Do like and follow our Facebook Page. We share great links and infographics there.

Join our Facebook Group to continue the discussion, we have a great community of investors who want to help each other become better investors. Everyone is welcome!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

Hi Financial Horse,

Why do you say the MCB is very good? The first day trade from 0.001 to 0.019. Second day 0.003-0.002. Now 0.001-0.002. Seems like going zero? Also post 21 May: I got these few questions.

1. What about SHORTist of MCB who has not covered back but no more trading?

2. How can Temasek exercise a right that belongs to me even if I did not exercise it?

Hi Greg,

Those are not the MCBs though, those are the rights to exercise an MCB. Even if you buy them you still need to cough up (no pun intended) the cash to subscribe for the MCBs at $1. So technically speaking, as long as they are positive it’s still alright.

That said – we probably won’t have true price discovery until the MCBs are actually listed and there is some semblence of liquidity.

I like the MCBs because on a risk-reward basis, I think they offer a more attractive risk reward. If SIA can’t redeem these things within 10 years, then the equity price is dead anyway, and so is much of international travel as we know it. That said, I don’t like them so much at their issue price of $1, but if they drop post listing as COVID19 plays out, they could become interesting.

Not sure why SIA is investing in new planes at this current time and climate.

With their track record of fuel hedging losses also

Not really confidence inspiring imo

Most of these were ordered before COVID19 if I recall. Not new orders. I suppose you could argue that they should just cite force majeure and refuse to take delivery, but what would also impact reputation going forward. Kinda catch 22 here.

Indeed the bailout is critical, but SQ needs to watch out for cost, esp staff cost. Many redundancies in its staff cost. Paying bonuses to its staff is ridiculously a bad idea instead if preserving cash. It’s time for SQ to look after the investor who supported them all these years.

Were they paying bonuses recently? Couldn’t find anything on it.

I guess it’s really about managing stakeholders. Cutting staff is the easy move, and many other countries have done it. But what if you’re one of the staff who’s been cut. What happens next?

Hi FH,

So the MCB Rs by your logic is worthless or max 0.001?

Also what should technically happen is that the right to buy the MCB expires and ceases to exist. However, Temasek can somehow exercise a Right that they do not have or a right that ceases to exist.

What if I shorted 10 million Rs on the last day of trading?

Yeah so it seems that nobody is really selling (or buying) the MCB Rs, which may look bullish, but we won’t have true price discovery until they list and there is decent liquidity.

If you’re holding the rights on expiry, then you need to subscribe for the rights at $1 each. Temasek will mop up all excess rights.

Good question on the short, can you even short these things? Assuming you can – reasoning from base principles, then you need to borrow the rights to short them. And you’ll need to return them prior to exercise unless there is a separate deal with the lender, so technically you cannot be short going into exercise.

HI FH,

I subscribed for your REIT Masterclass and want to say a big thanks fore creating it. Would like to check though, how long is the validity of the course? or is it permanent?

Thanks! Glad you’re finding it helpful. Yes you get lifetime access, so you can watch and rewatch, including updates to the course down the road. 🙂

Hi you said it looks bullish but it seems to be unloading by the funds at 0.002 and 0.001. Do you think it may go up next week? Or u think capped at 0.002 and towards the end 0.001?

Yeah after thinking about it a bit more I realised it may be hard to gauge market reaction based on the price action of the MCB rights. If it sells for a high price it’s clearly bullish, but the current price action – might actually be more bearish than bullish.

Not a bad thing though – if the MCBs fall big time post listing, could be an attractive pickup.

Hi

In the past 2 months I made a few short posts on SIA. In a more recent one I tried to do a simple extrapolation of what it’s revenue for this qtr to 30 Jun will be – at 4% utilisation of its fleet I came up with an estimate of $200 million. This compares to an average of ~$4 billion per qtr for the year ended on 31 Mar 20, which included the already depressed 4th qtr

I had expected the 4Q to record a loss of at least $1.5b including provisions for losses on its forward contracts for fuel hedges. In actuality it reported a <$1b loss seems to be largely because only those fuel hedges contracts expiring up to 31 Mar (ie those that SIA had technically or physically taken deliveries of) were marked to market, or more like impairing inventories. (From this qtr on SIA will have an additional item of expenditure – fuel storage expense!)

I too am expecting its share price to drop below $3 perhaps sometime after its 1HFY21 results are known. In my mind, another unknown breeding from the one about travelling habits is how airlines will be reacting in anticipation of this. Will it affect SG air hub position?

But back to SIA itself, I was asking a FB friend if he were a fund manager holding shares in SIA bought before the crisis will he take up the rights and thus increase the number of units to 2.5 times at a time when the industry is just beginning to enter the worst time the industry has ever faced? I would sell everything!!!

Thanks! That’s really interesting. So the numbers are not as bad because of how they accounted for the fuel. If so you’re absolutely right that eventually they’ll run into storage issues, so the 1H could be tricky since this oil glut isn’t going to clear up so fast.

I actually think air travel will eventually recover. The only question is how long, and how? I wouldn’t rule out massive consolidation within the global industry.

They’re apparently giving 1/2 mth bonus. I guess it’s mostly to help staff who are dependent on the bonus given the 20% paycut.

Got it, thanks for the clarification!

Also, most of their staff cost are in pilots and cabin crew. You cant get rid of pilots and it’s foolish to do so given the grave global shortage. If you do so now, you’ll suffer a year later when aviation recovers. As per cabin crew, most of their salary comes from variable component. Their fixed component is miniscule. Finally, when the govt is footing 75% of the wagebill up to 4.6k, I think there’s less incentive to cut manpower

The place they should be looking to review is how they conduct hedging. They’ve only reaped hedging benefits maybe 2-3 times this decade…

Hahaha.. good point on the fuel hedges.

Hey, I’m a little confused about the MCB. The way you phrased it, if SIA calls it after 10 years, they pay you in shares. What if they call it after 5 years, are you still paid in shares or in cash instead? Thanks!

Yep you’re broadly right. If SIA calls it, they pay in cash. If SIA doesn’t call it, it will automatically convert after 10 years, and the automatic conversion is in shares. 🙂

April’ Passenger-KM Load Utilisation

Only 9.1% of the 3.7% Fleet Utilisation

Cargo load factor was better

75.6% of the 35.3% Fleet Utilisation

May not achieve even $200m in revenue in 1QFY21?

https://links.sgx.com/FileOpen/opstats-apr20.ashx?App=Announcement&FileID=611115

There was a commen somewhere about mark to market fuel hedges. Would that explain revenue? I havent done a deep dive into their accounting policy.

But financial engineering aside, I do think the current quarter will look really bad, from a common sense point of view – nobody is flying.

Yes they are paying 1 month bonus to all staff.

Thanks!

Was NOL our national carrier? National pride? We know what happen in the aftermath.

NOL was commercial cargo though. Wouldn’t exactly call it a national pride. 😉

Hi, if SIA doesn’t call it, it will automatically convert into Shares after 10 years, and then conversion price is $4.84. So if the Sia Shares price is $3 in that time, does it mean the MCB holders will suffer a lost?

The 4.84 price is before adjustments (to account for share splits/consolidation, dividends etc), so the final price will differ slightly. But yes – the concept is sound. If the conversion price is above the prevailing market price, MCB holders will suffer a loss on conversion.

Can I ask, how is the price of rights 3.80? The price of SIA is about 3.90 now, and with the rights you can buy SIA shares at 3 bucks. Then wouldnt the price of rights be around 90cent?

Sorry I added in the $3 price of exercise to the rights for easy comparison against the price of the shares. You are right – the price of the rights alone is about 80 cents now (excluded the $3 for exercise).

they need to seriously relook/revamp/whatever-you it their fuel hedging team!

thats the biggest hole in the ship.

🙂

I am SIA shareholder, I will definitely subscribe for the right share. However, will I loose out if I don’t subscribe for the MCB?

That’s a good question. Really tough one too. If I were a shareholder I would probably take up both, but its also hard to say that you would “lose out” if you don’t take up the MCBs. I would say that they go well together – occupy different parts of the capital structure to give a broader investment into SIA.

Hi, can I sell or redeem my MCB before the 10th year? If so, would I get any interest earned on it or would I even get my cost back?

You can sell them on the SGX after they are listed. You will have to accept the price on the open market though – and there is uncertainty as to what that price would be. If the market thinks SIA will redeem soon, the price will go up. If not, price may drop.

This is an excellent piece of analysis. Many thanks!

Glad its helpful!

Good writeup for my understanding & conclusion to subscribe to the rights issue but not the MCB mainly because the MCB is not liquid & works v much like a ELN which may result in a substantial loss of capital.

Yeah I’m really curious to see how the MCBs trade on the open market – and what the take up rate is like vs rights.

Does anyone believe the oversubscribing for the right MCB would be an option? Furthemore if i buy 10.000 Rights MCB do i then have to use them all?

My issues is that i have an minimum order on Saxobank, thus have to buy 39.000 at 0,01 despite not planning to us them all.

That’s a really good question, I actually don’t know the answer to this one. Will need to check the offer docs.

I bought a thousand shares on 13 May (ex-rights pricing), may i know if my shares will be diluted after the rights shares are introduced?

Well the number of shares you hold stays the same. But the total number of SIA shares will go up. So yes technically – you will get diluted.

not fully understand MCB being good investment? suppose SIA doesn’t redeem in the entire 10yr period that is due to poor operating income, which could mean its share price doesn’t recover to $4 or $5. wouldn’t that be worse-off for MCB holders to have the bonds exchanged into shares at $4.84 imagine share price still stuck at ~$3?

I think the key to the MCBs is getting them at the right price. At $1 risk-reward may not be amazing, but if they trade below par post-listing, they could be good risk-reward at the right price. 🙂

But yes, there are real risks with the MCBs as well, as you have rightly pointed out.

Hi Greg, your analysis are indeed very sensible. I have just a concern. What if 10 years later the price of SIA is below $4.80, say $3. For simplicity sake. No dividends issued for 10 years. No adjustment of price is required. Isn’t this as good as I’m using $4. to get something that’s worth only $3. After 10 years. Forgo opportunity cost…. etc…

Yes, that is the tail risk with the MCBs. And there may not be sufficient liquidity on the open market to exit an investment in them without a big bid-ask spread. But in that scenario – imagine how badly SIA and the entire world would be hit, if SIA can’t redeemd the MCBs in 10 years.

Anyway, back to the issue at hand, the question then is at what price will the MCBs have attractive risk-reward. If not at $1, what about $0.8? Or $0.6?

Sorry. It’s meant for Financial House. Not Greg

Currently, if you subscribe to MCB, it has no leverage. It’s hard cash. After trading, it may not have leverage too. We don’t know. So, my view is, it is high chance it will be below par upon listing. I believe most shareholders who entitled to it will just

1. sell, if enough to cover brokerage.

2. just subscribe and keep (small amount after all).

3. Do nothing. So Temasek take up all.

I’m concerned with what will SIA do after 10 years when the price is still below the subscription price. If no adjustment. Then I’ll be a big loser again.

Well, 10 years is a long time – a lot of things will change in that 10 years.

One way to see it is that if SIA cannot redeem these MCBs within 10 years, and needs to resort to mandatory conversion, what does the rest of the world look like? I think in that scenario, a lot of other investments (including the equity in SIA), are going to perform very poorly. Is your portfolio prepared for such a scenario?

The have made provision charge of $2.6B in reserves. This is their accounting treatment since the past. Be it profit or loss. Now that the price of fuel has increased. I believe some of the losses will be write back.

Thanks for the heads up!

I’m new to Financial House. I find the articles and discussions very good. Especially your analysis and views and comments. Are you able to share on SATS and ST Engineering? Thanks

Hi. I’m new to Financial House. I find your views, comments are very good and broad. Most importantly not Bias. I don’t know where to post my questions/request on SATS and ST Engineering.Are you able to do a review on these counters? whether it’s time to get in now? Or, At what price is a good entry point? Thanks

Hi Wellytjia,

Welcome to Financial Horse! Glad you find it helpful.

I’ve actually done simple reviews on them on Patron, you can check them out next time if you’re keen: https://www.patreon.com/financialhorse

I’ll recap some views simply here for your benefit:

SATS – pretty similar to SIA. Could go up, could go down, key is how COVID19 plays out. Buying now requires taking a leap of faith that COVID19 will go away sooner rather than later, so the key question is what kind of margin of safety is required.

ST Eng – Pretty big exposure to aerospace. I like it, but I don’t see it as a compelling buy right now because there will be real earnings headwinds. Was a buy for me back in March when it was at the 2.8x range though.

Hi! I am a bit confused and new to this.

Rights issue- $3.

1) Does it mean I’m buying sia shares at $3 below market value of $3.80?

2) What happens if i “do nothing”? Does it get sold? If it gets sold, how much do I get? Or do I need to go somewhere to sell it?

3) if I exercise my rights. Subscribe to it- I need to pay $4.5k and i will get 1500 shares on TOP of my 1000 shares.

Mcb- what happens if I do nothing? Or do I need to enter my trading platform/ Internet banking to sell it?

Questions derived as I saw them credit the mcb and rights issue to my cdp

Sure, my thoughts below:

1) Yes

2) If you do nothing, nothing happens. Your options are (1) to take up the rights, (2) sell the rights on the open market, or (3) do nothing.

3) Yep, pretty much.

4) If you don’t take them up, nothing happens for you. Temasek will sweep up the excess MCBs.

Hope this helps! 🙂

Hi. Isn’t it the case though that as long as the actual share price is above SGD 1 at the time of MCB conversion in Yr 10, technically MCB holders do not lose money per se? That is, because we only paid SGD 1 for MCB and we get 373 shares and hypothetically the share price is SGD 3 at the time, we still gain = (SGD 3 – SGD 1) x 373 from the MCB?

You get 373 Shares per 1000 MCB, so as long as the share price is 2.68 you get the principal back. Everything beyond that will be gain, and everything below will be losses. 🙂