As many of you may have known by now, this week saw the closing of not one but two US banks.

The first was crypto bank Silvergate.

The shut down of Silvergate Bank has been talked about for a while now, so it doesn’t come as that big of a surprise.

Most of the impacts will likely be contained to crypto itself, and the case of FTX showed that you can have contagion in crypto without it spreading to broader financial markets.

But the second, far more important bank – is Silicon Valley bank.

Most of the silicon valley startups bank with Silicon Valley Bank, which makes this a much bigger story.

I’m seeing a lot of alarmist takes out there on how this is Lehman 2.0, and how contagion is going to spread next week.

As always – the truth is much more nuanced than that.

So I wanted to spend some time discussing Silicon Valley Bank’s bankruptcy.

This is a premium Patreon post. I am making it available to all readers in the hopes that this might help you make sense of what is going on.

If you find this useful, do support Financial Horse as a Patreon. You can get regular premium updates just like this, together with my full REIT and stock watchlist.

Sign up here.

What happened with Silicon Valley Bank?

If you are interested, there are great articles from Bloomberg and Financial Times that cover this in greater detail.

I’ll try to summarise in simple English here.

Problem starts in 2021…

In 2021, venture capital backed startups were flooded with cash.

Easy money from the Feds and rock bottom interest rates meant that venture capital money was everywhere, and these startups had a lot of cash.

They deposited most of this cash with their main banking partner – Silicon Valley Bank.

What a normal bank would do, is to take those deposits, and lend it out to a third party for a profit.

The problem with Silicon Valley Bank, is that most of their clients are startups.

And remember this is 2021 where liquidity was everywhere – and none of the startups needed to do something as old fashioned as “taking a loan” from a brick and mortar bank.

So what did Silicon Valley Bank do with all that cash deposits on their hand?

They lent it to the US government.

Or more specifically, they put it into US Treasuries (and mortgage bonds).

A whopping $91 billion of it.

Fast forward to 2022…

Fast forward to 2022, and the Feds are on a crusade to stamp out inflation.

We see the fastest pace of interest rate increases in 25 years.

When interest rates go up, bond prices go down.

So the $91 billion pile of US Treasuries and mortgage bonds held by Silicon Valley Bank drop in value.

If they were sold at market price, there would be a $15 billion loss.

Note – this is a mark to market loss

Just to be absolutely clear, this is a mark to market loss.

In other words, Silicon Valley Bank was technically not insolvent at this point in time.

It was merely a liability mismatch.

Had they held all the US Treasuries to maturity, they would have gotten back every single penny they put in at the start.

Unfortunately… 2023 is a tough year for startups…

The problem of course, is that the majority of Silicon Valley Bank’s clients are startups.

And 2022/2023’s rising interest rates have not been kind on startups.

Many of these startups went from being flooded with cash in 2021, to being unable to raise any new financing in 2022.

So they started to draw down on their bank accounts – at Silicon Valley Bank.

And you start to understand the problem.

Because to meet all those withdrawals, Silicon Valley Bank needed to sell their US Treasuries.

And if they sell their US Treasuries at today’s prices, they would recognise a loss on their balance sheet.

A loss that could potentially drive them into bankruptcy.

The catalyst

As is classic in capital markets though.

When it rains, it pours.

Bloomberg covers what happens next well, which I extract below:

In a meeting late last week, Moody’s Investors Service had bad news for SVB: the bank’s unrealized losses meant it was at serious risk of a credit downgrade, potentially of more than one level, according to a person familiar with the matter.

That put SVB in a tough spot. To shore up its balance sheet, it would need to offload a large portion of its bond investments at a loss to increase its liquidity — potentially spooking depositors. But standing pat and getting hit with a multi-notch downgrade could trigger a similar exodus.

SVB, along with its adviser, Goldman Sachs Group Inc., ultimately decided to sell the portfolio and announce a $2.25 billion equity deal, said the person, who requested anonymity to discuss internal deliberations. It was downgraded by Moody’s on Wednesday anyway.

At the time, large mutual funds and hedge funds indicated interest in taking sizable positions in the shares, the person said.

That is, until they realized how quickly the bank was hemorrhaging deposits, which only got worse on Thursday after a number of prominent venture capital firms, including Peter Thiel’s Founders Fund, were advising portfolio companies to pull money as a precaution.

“Stay Calm”

Around that same time, on Thursday afternoon, SVB was reaching out to its biggest clients, stressing that it was well-capitalized, had a high-quality balance sheet and “ample liquidity and flexibility,” according to a memo viewed by Bloomberg. Becker had a conference call in which he urged people to “stay calm.”

But they were already too late.

SVB “should have paid attention to the basics of banking: that similar depositors will walk in similar ways all at the same time,” said Daniel Cohen, former chairman of The Bancorp. “Bankers always overestimate the loyalty of their customers.”

A vice president, in one call with a public company client, seemed to stick to a script and gave no new information, according to a person on the call.

That client decided to move a portion of their cash to JPMorgan to diversify assets Thursday; the transaction took two hours to navigate on SVB’s website and is still marked as “processing.”

The same client tried to move a larger amount on Friday morning, but no attempts to wire the money worked, the person said.

Quick Collapse

The collapse on Friday happened in the span of hours. SVB abandoned the planned equity raise after shares tumbled more than 60% on Thursday. By that point, US regulators had descended upon the bank’s California offices.

SVB “didn’t have nearly as much capital as an institution that risky should have had,” William Isaac, the former chairman of the FDIC from 1981 to 1985, said in a telephone interview Friday. “Once it started, there was no stopping it. And that’s why they just had to shut it down.”

Before noon in New York, the California Department of Financial Protection and Innovation closed SVB and appointed the FDIC as receiver. It said the main office and all branches would reopen on Monday.

Breaking it down in simple English…

Basically, to meet liquidity needs (ie. Client withdrawals), Silicon Valley decided to do 2 things:

- They would sell a portion of their US Treasuries and recognise the mark to market loss

- At the same time, they would do a big equity fundraise from investors to cover the loss

But once the market realised the bank was in trouble, they rushed to pull funds out.

And this being Silicon Valley, all the VCs that were eager to “value add” started advising their portfolio companies to pull funds.

And as all the FTX bros have realised (myself included as I had deposits in FTX), whenever a bank starts using buzzwords like “ample liquidity and flexibility”, you want to get your funds out of there pronto.

Once the pace of withdrawals became clear, the equity fundraise itself collapsed as potential investors balked and started to walk.

This only made the rush to withdraw funds worse.

This is a classic bank run

At this point it just becomes a classic bank run.

No bank in the world is immune to a bank run – it’s the very business model itself.

For every $100 the bank receives in deposits, it will keep $15 and loan out the rest.

If enough depositors come and withdraw $20 tomorrow, the bank is in trouble.

What happens next for Silicon Valley Bank?

Bank Deposits in the US are only insured up to $250,000.

Per regulatory filings, more than 97% of the deposits at Silicon Valley Bank crossed this threshold.

So if the bank is allowed to fail, it could get pretty messy for all those startups that banked with Silicon Valley Bank.

It would take weeks, even months for them to get any cash deposits above $250,000 back (assuming they can even get it back).

In the meantime, you still have payrolls to meet, suppliers to pay, landlords to pay, and so on.

Not to mention counterparty risk for other banks that dealt with Silicon Valley Bank.

It gets messy.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Will a buyout happen?

But if history is any guide, the FDIC and Treasury are likely working around the clock right now.

The most typical course of action in a case like this is to get a bigger bank to buy out Silicon Valley Bank for cents on the dollar.

And if they’re kind enough, the Treasury may even grant a federal guarantee to the buyer to sweeten the deal.

This of course, is the ideal outcome, as it would mean that depositors are made whole again.

Bondholders or equity holders are unlikely to be so lucky though.

At the very least they would be looking at hefty losses.

Is this Lehman 2.0?

But I do want to put things in perspective here.

Silicon Valley Bank is NOT a JP Morgan.

The list of depositors are much more limited in scope.

Not to mention that 2008 was different in 2 key ways:

- Banks were way more leveraged back then

In 2008 banks held about $3 capital for every $100 deposits.

This time around the number is closer to $12 – $15.

That’s a monumental change in terms of strength of bank balance sheets.

The ability of banks to absorb stress this cycle is much higher than in 2008.

- There was an underlying asset class (subprime mortgage) that almost all banks were exposed to and where credit quality was significantly impaired

Or to put it simply, in 2008 banks were exposed to subprime mortgage which turned out to be a toxic pile of trash (worth close to zero).

This time around, the asset class in question that did Silicon Valley Bank under was US Treasuries.

Where the default risk is basically zero.

Had they held the US Treasuries to maturity, they would have gotten back every single cent.

So the real mistake made by Silicon Valley Bank is a duration liability mismatch.

It is a bank who loaded up too much on long duration Treasuries, such that they were unable to meet liquidity needs without realising market to market losses.

In simply English – they mismanaged their interest rate risk.

How many other “Silicon Valley Banks” are there out there?

The logical next question – is how many other cases of this are there out there.

Are we going to discover another 100 regional banks going under next week due to a “run on the bank” caused by “liability mismatch”?

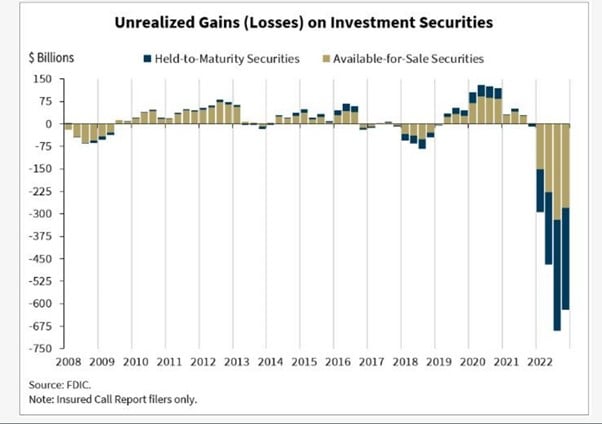

There’s a chart below making the rounds, that shows the amount of unrealized losses held by banks out there.

It’s not small.

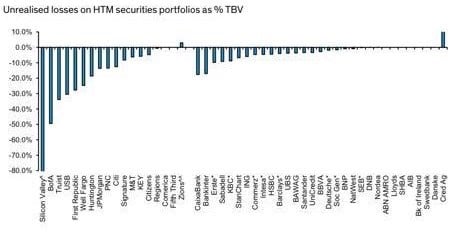

Here’s another chart that breaks it down by bank.

Silicon Valley Bank was definitely the biggest culprit, but there are a couple of others on the list that look worrying too.

Can this spread to the G-SIBs (Global systemically important banks)?

Personal view though – As of now, I don’t see broader contagion arising out of Silicon Valley Bank.

A lot of the factors that drove Silicon Valley Bank are unique to a bank that had a very concentrated client base (startups) and had very poor interest rate risk management policies.

The likes of Bank of America and JP Morgan, they have a much more diversified client base.

They also have a much more diversified asset base, to meet short term liquidity needs.

Not to mention better interest rate risk management practices (one hopes).

They do have a problem in that their deposit rates are waaay too low compared to T-Bills, which is driving an outflow of cash (to be fair DBS is guilty of this too).

But there is an easy fix there in raising interest rates paid on deposits, if push really comes to shove.

But the smaller, regional banks?

Coming back to Silicon Valley Bank – chances are that some kind of deal will likely be reached for the assets or the bank, or some kind of continuity plan put in place.

But for the other regional banks that have poor risk management practices, will we see more of them go under this cycle?

Sure, definitely possible.

Every rate hike cycle will see bank defaults, this is not unusual.

But in the 1980s during the Savings and Loans crisis you saw 32% of savings and loans associations (thrifts) in the US go bankrupt, without a significant recession (until years later).

So the regional banks can fail, without causing broader contagion if properly managed.

For now at least, I don’t see this spreading to the likes of Bank of America or JP Morgan yet.

Can this become Lehman 2.0?

That being said, I am NOT saying that this cannot evolve into something bigger.

It is possible of course.

But quite a few steps need to happen from here until the point of broader contagion.

What’s the bigger story here behind Silicon Valley Bank?

The bigger story here in my view, is this.

We’ve had an extended period of zero interest rates, where investors were lulled into a false sense of security

They made bets on the assumption that interest rates would stay low forever.

Now interest rates are going up rapidly, and that is causing all manners of pain throughout the economy.

It’s not easy to anticipate what exactly will break in the months ahead.

Last year we saw the crypto complex blow up (Luna and then FTX).

Then we saw the bubble in loss making tech burst.

Then we saw the UK Pension Funds blow up from their poorly managed bet on Gilts.

Now we see the same with Silicon Valley Bank.

And that to me is the takeaway here.

The longer interest rates stay at these levels, the more you’ll see things start to break.

Silicon Valley Bank is the next to fall, but it likely won’t be the last.

This unwind will need time to play out, until we get something big enough that forces the Feds to pivot.

Personally I don’t see Silicon Valley Bank itself triggering broader contagion.

But hey – let’s see.

Afternote: Will the failure of Silicon Valley Bank cause the Feds step down to a 0.25% rate hike?

Following up on the piece on Silicon Valley Bank, I received a great question that warranted further discussion:

This event seemed to have sent yields on US treasuries of all tenors down. Is this due to a short term flight to safety, or do you think the market has fundamentally reassessed the extent/duration of rate hikes after this event?

If you look at the futures curve, you’ll find that:

1. Right after Jerome Powell’s testimony, the market priced in a 78% chance of a 50bps rate hike

2. After Silicon Valley Bank failed, this fell as low as 40%

3. As of today, the market is back to pricing in a 68% probability

So to answer that question – the immediate reaction of the market was a combination of both.

The immediate reaction of the market was both (1) a flight to the safety of US Treasuries, and (2) sending the chances of a 0.50% rate hike down.

But was this justified?

The better question though – is that was this justified?

Is Silicon Valley Bank enough to cause the Feds to step down from a 0.50% rate hike, after just having called for a 0.50% rate hike to combat reaccelerating inflation.

My personal view is no – unless this bank failure is not properly contained and allowed to spiral further.

The Feds are concerned about their credibility here.

It is why they always want to give the market as much advance warning as they can of what moves they are going to make.

The Feds of today like to choreograph their moves well in advance, and are not in the business of shocking markets.

To step up to a 0.50% hike, and then to step down to a 0.25% hike in the same week, simply due to a failure of a regional bank, would cast doubt over the Feds credibility.

The market seems to agree with this view, as the pricing of a 0.50% hike has gone back up to 68% probability.

Make no mistake though, if the Feds keep going, something will break…

Just to be clear though.

While I don’t think Silicon Valley Bank’s failure is big enough to cause a Fed pivot.

If we keep going down this path, eventually something big enough will break that forces the Feds to pivot.

Stars are aligning for a period of economic weakness in 2H2023

With recent developments (most notably a sharp pickup in Fed terminal rates and market pricing this in), the stars are lining up for a period of economic weakness in 2H2023.

And the difference this time around, is that if the Feds succeed in taming inflation, then value stocks will not be an effective hedge as it was in 2022.

Remember in 2022 economic growth slowed, but because inflation stayed high, earnings growth for value stocks was strong (because of price increases).

To put it simply – underlying volume was weak, but price increases were strong, driving good revenue/profit growth. This made value stocks look good despite weak underlying volume. This is a pure monetary illusion due to price increases, and is common during inflationary phases.

If the Feds succeed in controlling inflation, this will no longer hold true, and weak volume will translate into weak revenue / profit.

So I would be more cautious on value stocks heading into 2H2023.

Positioning wise, I’m still heavy cash here.

If interest rates are going to 5.75% (possibly 6.00%), equity risk just look underpriced here.

It’s not easy to forecast what exactly will break in the months ahead, so staying in heavy cash and watching the opportunities play themselves out is just the best risk-reward trade (when you’re getting 4% risk free). No need to commit to equities too early and get chopped up in the short term volatility.

This is a premium Patreon post. I am making it available to all readers in the hopes that this might help you make sense of what is going on.

If you find this useful, do support Financial Horse as a Patreon. You can get regular premium updates just like this, together with my full REIT and stock watchlist.

Sign up here.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

WeBull Account – Get up to USD 500 worth of fractional shares

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares.

You just need to:

- Sign up here and fund any amount

- Maintain for 30 days

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Dear FH

Excellent analysis and enjoyable read although worrying for all

The fed might not hike by 50 if the Inflation data coming out this week shows further fall in pace of inflation

Whereas it might be tempting to think that the fed wants to inflict pain , a bigger credit event than this might certainly have a domino effect

Credit Suisse is vulnerable as of now and add in a few of the smaller regional banks in US. If more cracks appear and inflation is stable or lower, the fed will stick to 25 base points and might even pause in April and decide again

The fed will not only be data driven but also influenced by more credit risk situations

By this time next month, the Q1 earnings reporting season will begin and the short term market course will be led by this as well

For me, this is a risky but good chance to nibble at the 6 major US banks with strict portion sizing and also add the local banks as they fall in sympathy

Not much to do

– either go for fixed income and lose to inflation ( real return of minus 2-3% in SG)

– take equity risk and add the dividend paying SG blue chips, keeping faith long term

I will do the latter and am buying local blue chips plus banks gradually and will buy more without much hesitation

The opportunity cost of staying in liquid cash has to be factored in with a 6-8% straight loss plus potential dividend opportunity loss per year or pro-rata otherwise

Time will tell whether my strategy will work this time

Regards

Garudadri

Fair enough Garudadri. Great comment as always.

If we do indeed get a more dovish Fed as a result of this, one struggles to imagine what would happen to inflation expectations!

I myself do retain exposure to REITs / Stocks as a result of this, primarily from long term positions that I do not want to market time with.

Let’s see how this plays out.

2023 is shaping up to be even more eventful than 2022.

Hi FH, thanks for the insights! Just curious, why do you think the US government didn’t step in to bail them out?

Well moral hazard for one. If you can take a lot of risk with your bank and keep all the upside if it goes well, and then if things head south the government bails you out – that’s real moral hazard right there. A lot of people were upset with this after 2008 when shareholders / bondholders were made whole using taxpayer money.

And second it’s also a tricky political issue after 2008, to use taxpayer funds to bail out private parties. Doesn’t look good after 2008.

If you look at the solution eventually settled upon, they were very keen to stress that this is not a bailout by taxpayers, and that private sector would have to absorb some losses: https://financialhorse.com/silicon-valley-bank-the-bailout-is-here-is-contagion-averted-time-to-sell-dbs-bank-and-astrea-bonds-13-march-2023/

Hi, could i get the source for the “Unrealised losses on HTM securities portfolios as % TBV” chart please? Thanks!

It was one of the Fed reports from bank stress testing, dont have the link with me right now unfortunately.