I’ve been getting a couple of questions on Singapore Savings Bonds and whether it still makes sense to buy (or hold on to) them today.

Or whether you just put the money into T-Bills or Fixed Deposit instead.

So I wanted to address these questions quickly, and share what I am doing with my own Singapore Savings Bonds.

3 key questions:

- Does it make sense to buy Singapore Savings Bonds today? Why I am buying T-Bills and Fixed Deposit instead?

- Will Singapore Savings Bonds interest rates ever go up again?

- Should you still hold onto Singapore Savings Bonds today?

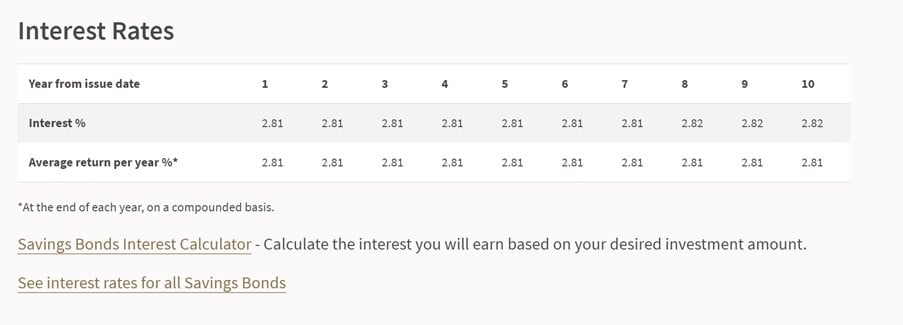

Latest Singapore Savings Bonds yield 2.81%

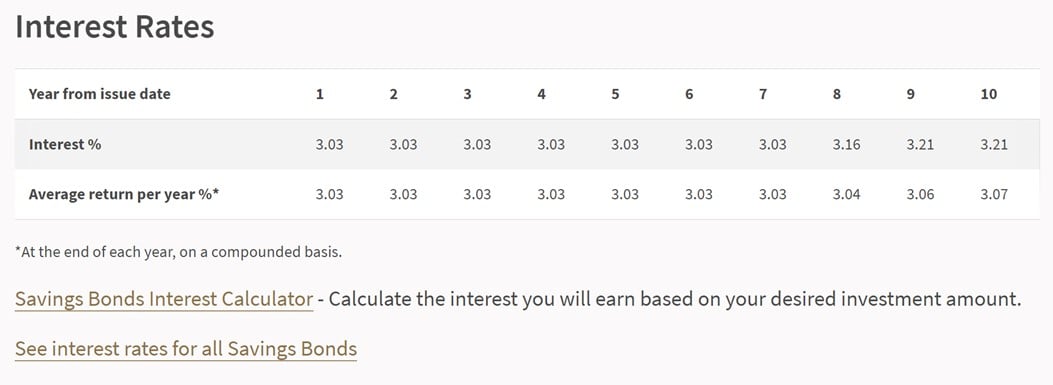

First off – here are the interest rates for the latest Singapore Savings Bonds.

You’re looking at 2.81% for the first year.

Which stays flat for 10 years – 2.81% all the way up to 10 years.

Singapore Savings Bonds artificially smooth out the yield curve

For those who are wondering why the yields look like this.

It is because Singapore Savings Bonds smooth out the yield curve – so that the 1 year interest rate will never be higher than the 10 year interest rate.

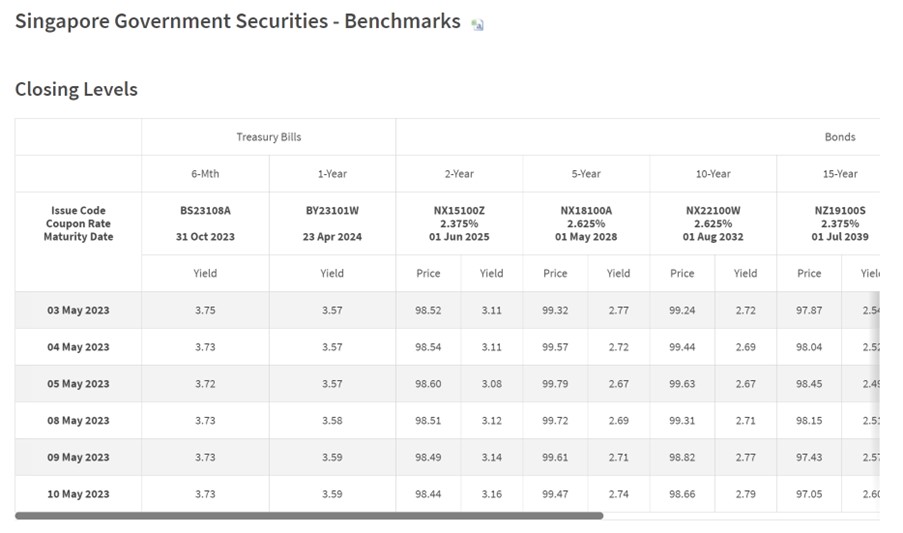

This is a big problem right now where the yield curve is inverted all the way up to 10 years.

You can see how the 1 year interest rate (3.59%) is below the 10 year interest rate (2.79%).

This is also quite a potent recession signal, but that’s a topic for another day.

So for Singapore Saivngs Bonds, the yield gets artificially smoothed out, resulting in the very flat yield that you see above.

Does it make sense to buy Singapore Savings Bonds today?

The main advantage of Singapore Savings Bonds is the dual flexibility to (1) lock in interest rates up to 10 years, and (2) redeem the money any time with accrued interest and no principal loss.

But no denying that at today’s yield’s – you are taking a below market yield on the 1 year interest rate for that flexibility.

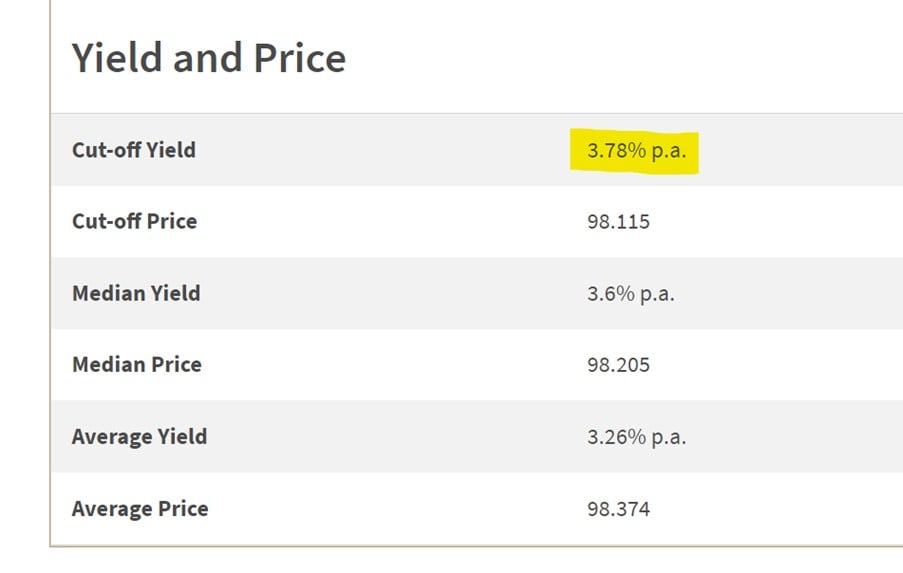

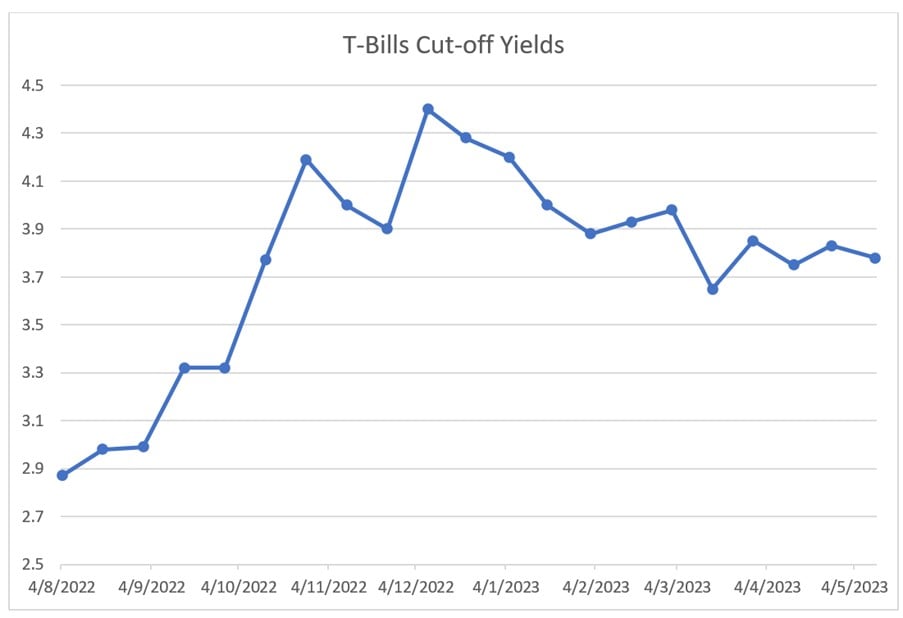

If you wanted to go with another instruments, you’re looking at 3.78% on the latest 6 month T-Bill.

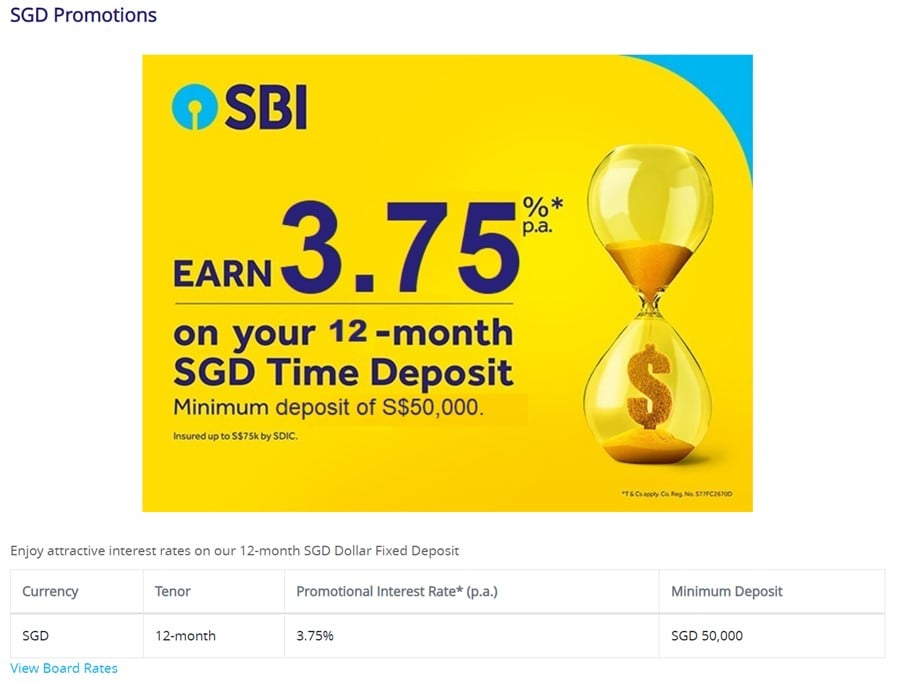

And 3.75% on for a 12 month Fixed Deposit with State Bank of India.

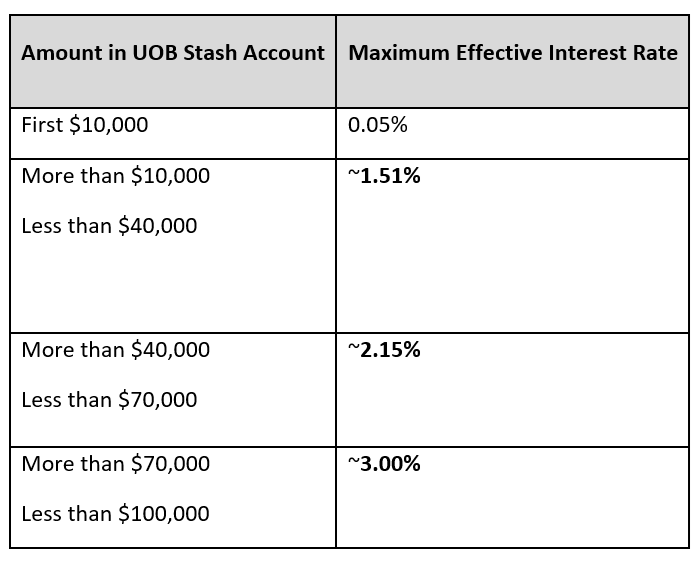

Heck, even if you wanted something with full flexibility to withdraw any time, you even use the UOB Stash Account which pays an effective interest rate of 3% on $100,000.

This is a savings account – you can withdraw any time.

Why I am buying T-Bills and Fixed Deposit instead

Personally – I’m no longer buying the Singapore Savings Bonds.

Firstly for the very simple reason that I am already close to maxxed out on my individual $200,000 allocation of Singapore Savings Bonds.

I can’t buy much more even if I want to.

Even if I could buy more though, I don’t really see myself doing so at these prices.

~$200,000 is enough liquidity for me, I’m happy to put the rest into higher yielding instruments – namely T-Bills and Fixed Deposit today.

Personal Views – Singapore Savings Bonds worth buying?

That being said, it’s ultimately a personal decision.

If you look at all the other options above, you’ll find that you can easily get:

- Equivalent liquidity at a higher yield via UOB Stash Account – 3% on $100,000, can withdraw any time, or

- Higher yield at the expense of liquidity – via T-Bills or Fixed Deposit

The only thing that you cannot easily replicate though, is locking in interest rates up to 10 years on a cash like product.

Sure, you can buy a 10 year Singapore Government Bond, but you can’t get money back before maturity unless you sell it on the open market – which means capital losses if interest rates go up.

So investors who value this aspect of the Singapore Savings Bonds can still consider buying.

But man – last month’s Singapore Savings Bonds were better in every way in terms of interest rates.

And saw full allotments.

And I even wrote an article saying this might be the last chance to get Singapore Savings Bonds above 3.0% yields.

If you’ve been a regular reader of Financial Horse, you really should have filled up on your Singapore Savings Bonds allotment this cycle and locked in much better interest rates.

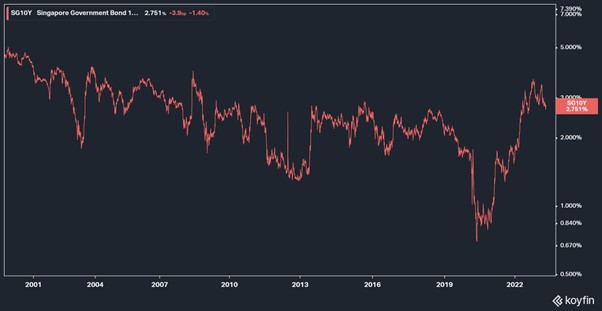

Will Singapore Savings Bonds interest rates go up again?

Will we get a second change?

Will Singapore Savings Bonds interest rate ever go up again, beyond this cycle’s highs?

Singapore Savings Bonds effectively track the average Singapore 10 year interest rates for the previous month.

So this question is effectively whether Singapore 10 year interest rates will go back up again.

You can see the 20 year chart of the 10 year yield below.

The highs this cycle brought us back to 2007 levels – the highest in 15 years.

Based on what we know today, it is fairly clear that we are at the later end of the current rate hike cycle.

So it does seem unlikely the 10 year yield will surpass this cycle’s highs.

You *probably* need to wait for the next rate hike cycle.

But never say never.

If it does, I would be sure to redeem some of my older Singapore Savings Bonds to buy the new ones.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Will I redeem my existing Singapore Savings Bonds?

My Singapore Savings Bonds are scattered across a mix of issuances.

But generally speaking the yields will look something like this.

In today’s market, I agree that 3.03% is probably not amazing.

When I can get 3.78% on a 6 month T-Bills.

But for me I do think it goes back to asset allocation.

I don’t mind parking aside close to $200,000 at these yields – for the flexibility to hold up to 10 years, and yet the flexibility to take it out any time with accrued interest.

As shared previously, I think there is a good chance of a hard landing in the next 12 – 24 months, and I might need the liquidity when it comes.

If it doesn’t I always have the option to take the money out any time and flip it into other instruments too.

That’s the kind of optionality cash brings in today’s markets, which I think is invaluable.

But ~$200,000 is probably where I draw the line.

The rest I’ll put into other higher yielding assets like T-Bills or Fixed Deposit.

But as always – this needs to be a personal decision.

I’m sharing my own practices in the hopes that this might help you guys in your thought process, I’m not saying to copy me exactly.

Every investor is different.

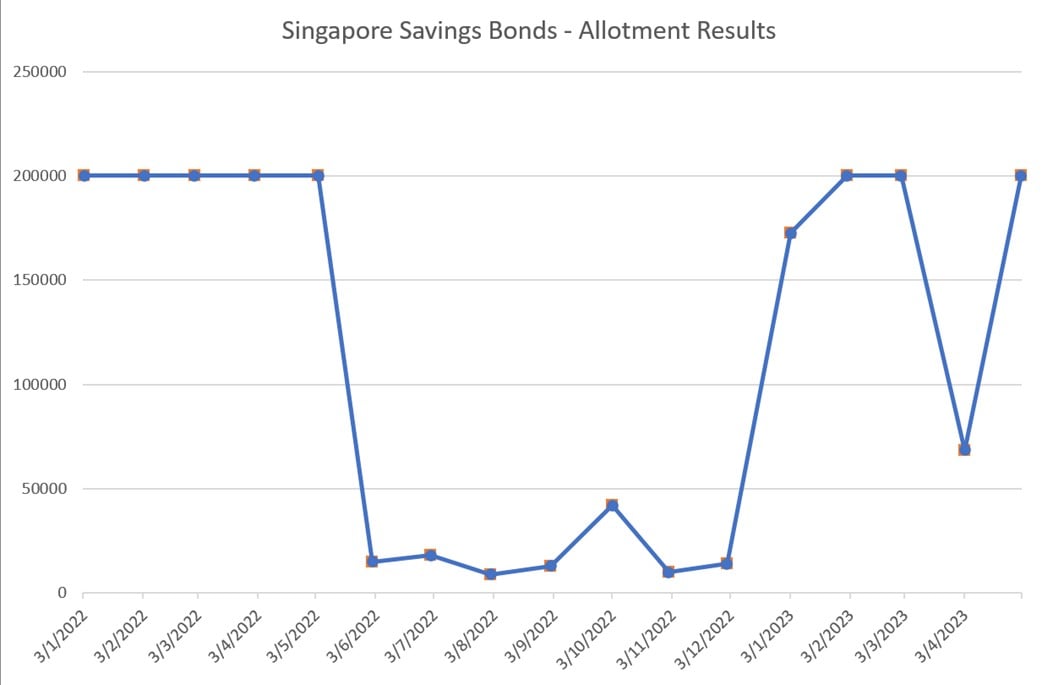

Singapore Savings Bonds – Allotment Results

The allotment results for the Singapore Savings Bonds are set out below.

You’re looking at full $200,000 for the previous Singapore Savings Bonds, which had yields much better than this round.

So I do think you’ll see full allotments for Singapore Savings Bonds this time around as well.

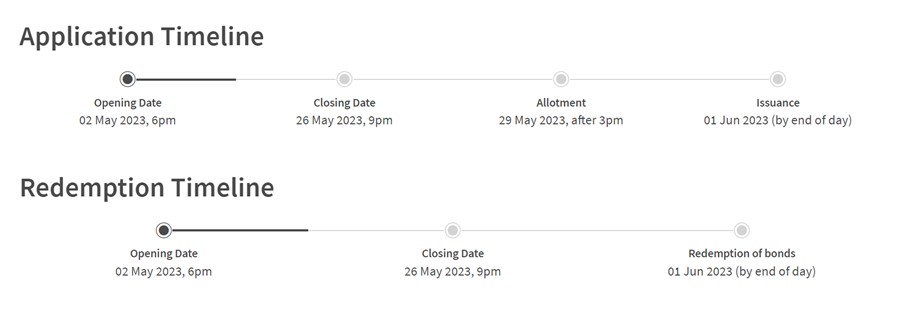

Singapore Savings Bonds – Application / Redemption Timeline

If you’re interested, here’s the application timeline.

Last day to apply for both buying / redemption of Singapore Saving Bonds is 9pm, 26 May 2023.

This article is written on 12 May 2023 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon, together with weekly premium macro updates like this one. You can access my full personal portfolio to check out how I am positioned as well.

WeBull Account – Get up to USD 500 worth of fractional shares + chance to win USD888 / Tesla Model 3 (expires 30 May)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares, and a chance to win USD 888 or a Tesla 3.

You just need to:

- Sign up here and fund any amount

- Maintain for 30 days

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Looking for the best investment books to improve as an investor in 2023?

Check out my personal recommendations for a reading list here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!