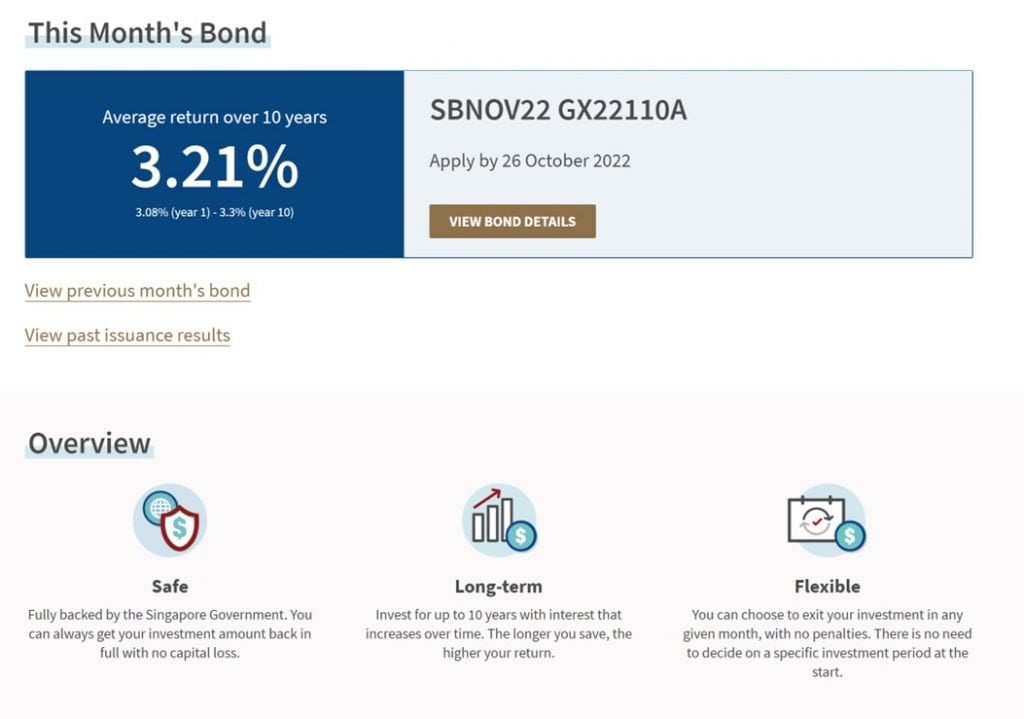

The latest interest rates on the Singapore Savings Bonds are out, and they are really attractive.

- Starting at 3.08% for Year 1

- Going up to 3.30% for Year 10

With an average return of 3.21% if held for 10 years.

This is better than the interest rates on CPF-OA by quite a bit.

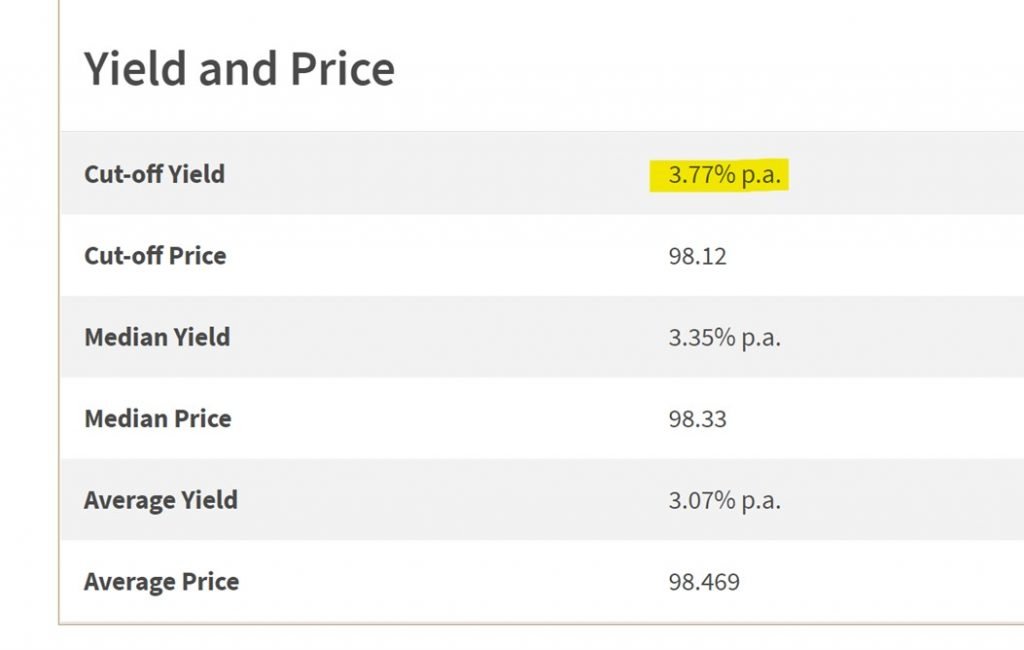

That said, the latest 6-month T-Bills pay 3.77% interest rates – and quite a few of you have asked whether it’s better to just buy T-Bills instead.

So I wanted to share my views in this article.

Basics: November Singapore Savings Bonds pay 3.21% interest rates

To recap the key features of Singapore Savings Bonds, they are:

Risk Free – Fully backed by the Singapore Government.

Can be redeemed any time with accrued interest – You will get the money back at the start of the following month, per timeline below:

Can hold up to 10 years – Singapore Savings Bonds can be held for up to 10 years, and the interest changes every year:

Each person can apply for a maximum of $200,000 worth of Singapore Savings bonds – You need to be 18 or older to apply, so you cannot use your kid’s name to get around the limits.

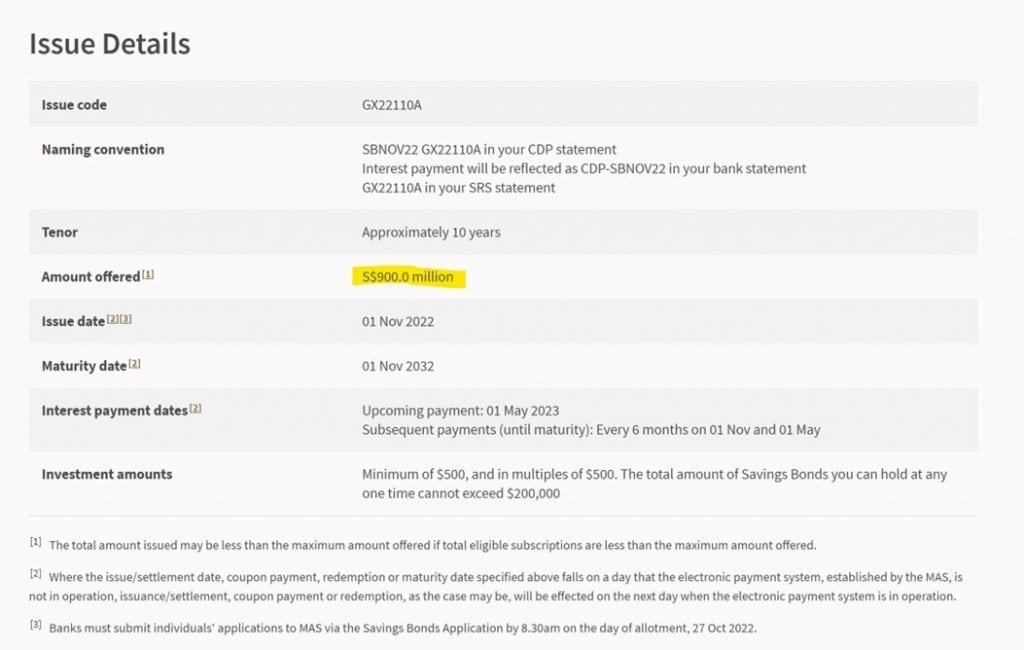

Issue size for the November Singapore Savings Bonds is $900 million, same as that for the previous October Singapore Savings Bonds.

2 Big Questions on Singapore Savings Bonds

The 2 big questions I’ve been getting on Singapore Savings Bonds are:

- Should you buy Singapore Savings Bonds now or wait for higher interest rates?

- Should you buy T-Bills (3.77%) instead of Singapore Savings Bonds (or Fixed Deposit)?

Should you buy Singapore Savings Bonds now or wait for higher interest rates?

To answer this question, we need to have some understanding of how high interest rates can go.

How high can interest rates go for Singapore Savings Bonds?

Now Singapore interest rates generally track US interest rates (because of the Impossible Trinity – google it if you’re interested).

Futures markets are pricing in a peak of 4.5% – 5.0% on the US Federal Funds Rate (US short term interest rates).

Now if inflation stays sticky we might get an overshoot to 5.5% on the Fed Funds Rate.

But let’s be conservative and assume a 4.5% – 5.0% peak on the Fed Funds Rate.

This means realistically, you’re looking at 4.0% – 4.5% peak on the US 10 Year Treasury.

Again, I get that if there is a liquidity crisis we may overshoot on the US 10 Year, but let’s be conservative for now.

Singapore Dollar strength means that Singapore interest rates may not go as high as the US.

Singapore Savings Bonds also track average interest rates for the previous month, which smooths out short term volatility.

So working backwards, I think you might be looking at peak interest rate for the 10 year Singapore Savings Bond this cycle of 3.5% – 4.25%.

Now for obvious reasons, these are just projections, so do take this with a pinch of salt.

But if my numbers are right, it means that with Singapore Savings Bonds at 3.21% now, they could go a fair bit higher before the end of this cycle.

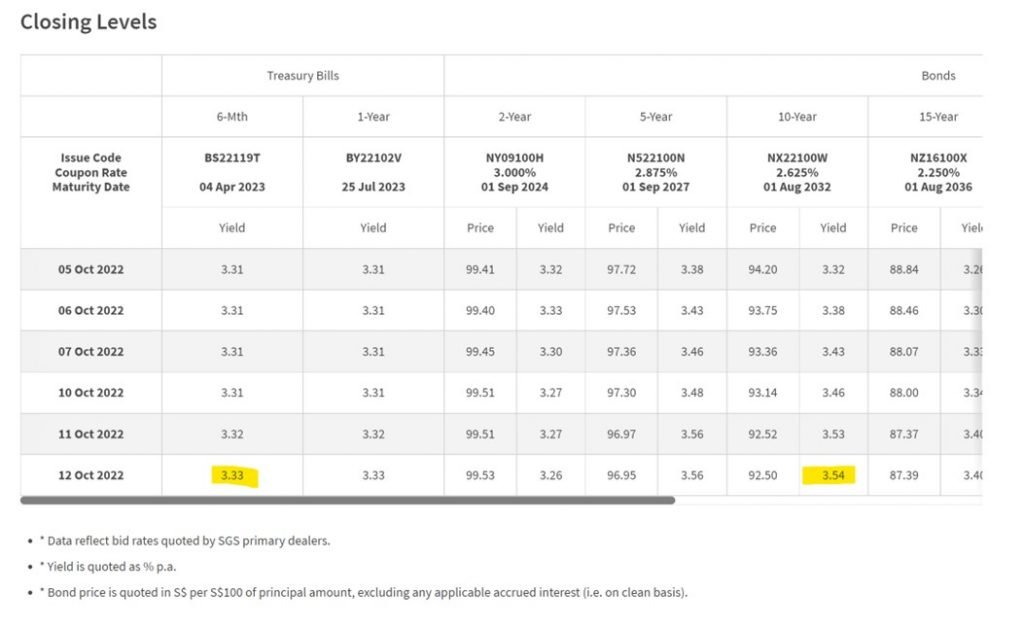

December Singapore Savings Bonds are likely to yield even higher interest rates

As it stands, the latest Singapore Government Securities are yielding 3.54% for 10 years.

While the latest 6-month T-Bill is yielding 3.77%:

If things stay this way, the December Singapore Savings Bonds are going to be even more attractive.

Should you buy Singapore Savings Bonds now… or wait?

That said, whether it makes sense to apply for Singapore Savings Bonds now or wait will depend on 2 things:

- What you do with the cash in the interim (if not buying Singapore Savings Bonds)

- How much Singapore Savings Bonds you are allocated (when you eventually apply)

What you do with the cash in the interim (if not buying Singapore Savings Bonds)?

Think about opportunity cost.

If the cash is going to be sitting in a savings account earning 0.25% interest.

Then frankly it doesn’t make sense to fret over whether you’re getting 3.08% or 3.77%.

Singapore Savings Bonds can be redeemed any time, so even if you change your mind down the road, it’s pretty easy to get your money back.

Low Allocations is a real problem

A big drawback with Singapore Savings Bonds is the low allocation size.

I’ve set out the allocation size per person for the last 3 Singapore Savings Bonds below:

- August – $9,000

- September – $13,500

- October – $42,500

At this rate, if you’re trying to put two hundred thousand cash into Singapore Savings Bonds, it could take quite a few months.

And every month that goes by, you’re losing the interest on your cash.

So… don’t be penny wise pound foolish.

I encourage you to look at the big picture.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

We also share great nuggets of wisdom on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Should you buy T-Bills at 3.77% yield instead of Singapore Savings Bonds?

With the auction that closed on 13 October 2022, the latest 6 month T-Bills pay 3.77%:

That’s an unbelievably high yield, that’s only set to go even higher.

Using my numbers above, you could see 6 month T-Bills go to 4.0% – 4.5% before all this is over.

Advantages of T-Bills over Singapore Savings Bonds

The main advantage of T-Bills over Singapore Savings Bonds, are:

- Higher short term interest rates

- No allocation limits

Higher short term interest rates (3.77% vs 3.08%)

The 1 year interest rate on Singapore Savings Bonds is 3.08%, while the 6 month interest rate on T-Bills is 3.77%.

T-Bills for now, give you much higher interest rates.

The exact reason why is a bit technical, and has to do with how Singapore Savings Bonds yields are calculated (takes the average yields for the previous month), and also how SSB yields are smoothed out so that the yield will only step up.

But the fact remains – if you want higher short term interest rates, T-Bills are probably the place to be.

No allocation limits for T-Bills

Singapore Savings Bonds have a maximum allocation of $200,000 per person, and you only get $10,000 – $40,000 a month (if you’re lucky).

For investors looking to invest hundreds of thousands or more in cash, the Singapore Savings Bonds limits are too low.

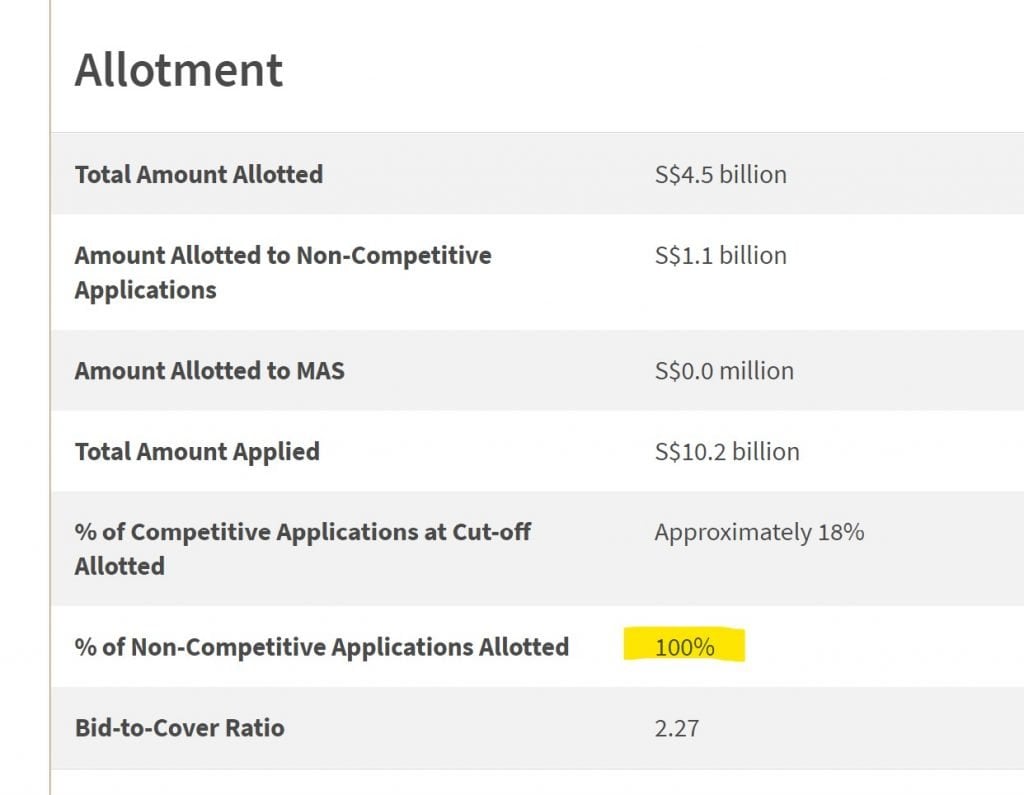

T-Bills have no limits on the amount you can hold, and non-competitive applications see 100% allotment (for now).

You can literally apply for $1 million in T-Bills and get full allocation.

Can’t say the same of Singapore Savings Bonds.

Limitations of T-Bills

That said, there are notable limitations with T-Bills.

The biggest one – is liquidity.

As a retail investor, it will not be easy to sell your T-Bills prior to maturity.

If you’re a high net worth individual selling large amounts, your private banker could probably make something happen.

But if you’re a mom and pop investor – you should probably count on holding your T-Bills to the full 6 or 12 month maturity.

And because T-Bills are short term instruments, after you get the cash back, you need to reinvest them at market interest rates (which may have gone up or down).

Is Fixed Deposit a better buy than Singapore Savings Bonds (or T-Bills)?

Now I know that a lot of you like Fixed Deposit.

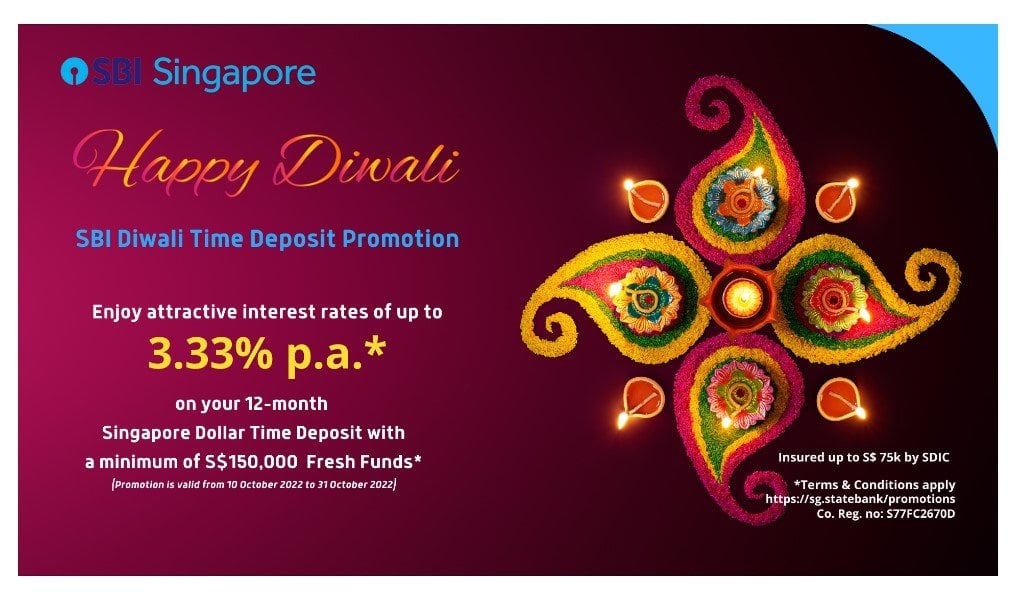

Fixed Deposit can have pretty attractive interest rates as well, with State Bank of India offering 3.33% for a 12 month fixed deposit for $150,000.

But as you can see, Fixed Deposit rates are usually not as attractive as T-Bills, because it takes some time for the banks to catch up in such a rapidly rising interest rate climate.

On the plus side though, with Fixed Deposit, if you really need the cash, you can get it back before maturity by paying a small penalty to the bank (usually in the form of lower interest).

Limitations of Fixed Deposit

The limitation with Fixed Deposit is that it is only SDIC insured up to $75,000.

And just like with T-Bills, after you get your money back in 12 months, you are subject to wherever interest rates are at that point in time.

Singapore Savings Bonds vs T-Bills vs Fixed Deposit?

I’ve summarised the pros and cons of each instrument below.

|

|

Singapore Savings Bonds |

T-Bills |

Fixed Deposit |

|

Interest Rates

|

Average |

High |

Average – High |

|

Risk Free |

Yes |

Yes |

Up to $75,000 SDIC insured

|

|

Allocation Limit

|

Poor |

Good |

Good |

|

Liquidity (ability to exit before maturity)

|

Good |

Poor |

Average |

|

Ability to lock in interest rates long term

|

Good |

Poor |

Average |

What am I buying – Singapore Savings Bonds vs T-Bills vs Fixed Deposit?

I shared my general approach to cash management in a recent article:

Personally for me in this climate – I would prioritise liquidity.

I would optimise my cash positions for liquidity first, and yield second.

I think in this climate, the chances of a liquidity event in the next 12 – 18 months is quite high, and I want to have immediate cash on hand to buy if that happens.

So the priority for me is:

- Minimum amount of cash in savings account

- Max out Singapore Savings Bond allocation each month

- X amount in T-Bills / Fixed Deposit

- Rest in savings account (depending on liquidity needs)

General Thought Process

I hold a minimum amount of cash in savings accounts, so they can be accessed at a moment’s notice.

This will be accounts like DBS Multiplier, Trust Bank (check out my Trust Bank review here – it’s worth signing up in my view) or Singlife.

The yield at 1-2% is definitely lower than T-Bills or Singapore Savings Bonds, but that’s the price I pay for the liquidity.

After that I will max out my monthly Singapore Savings Bond allocations.

Yields are lower than the market yields, but I think that’s an acceptable trade-off for the liquidity, and the option to lock in yields for up to 10 years.

Of the remainder, I am happy to keep X amount in T-Bills or Fixed Deposit for the higher yields.

T-Bills I would need to hold to maturity, and Fixed Deposit I can break early if I really want to (but there is a bit of hassle that comes with it).

And the rest I keep in a Savings Account, again for the liquidity.

But the exact proportion of each – only you can figure out for yourself. It will have to depend on your age, income status, and risk appetite.

I am buying the November Singapore Savings Bonds

I am currently maxxed out on my $200,000 Singapore Savings Bonds allocation.

Some of my Singapore Savings Bonds are from 2019, which pay 1.71% even in the 4th year.

So it’s a no brainer for me to redeem the 2019 Singapore Savings Bonds and buy the latest Singapore Savings Bonds.

As shared above, I value liquidity very highly in this climate, so I do not want to be caught with all my cash in T-Bills despite the higher yields.

What will allocation numbers for Singapore Savings Bonds be like?

It seems that with the soaring T-Bills interest rates, a lot of retail money has moved over into T-Bills instead.

T-Bill issuance sizes go for about $4 billion a pop, with multiple issuances a month – so there is more than enough supply to meet whatever demand there is.

That and comparatively lower Singapore Savings Bonds rates, mean that allocation sizes have been going up the past few months:

- August – $9,000

- September – $13,500

- October – $42,500

Hopefully that stays the way for November, as I have quite a bit of 2018 and 2019 Singapore Savings Bonds that I want to redeem.

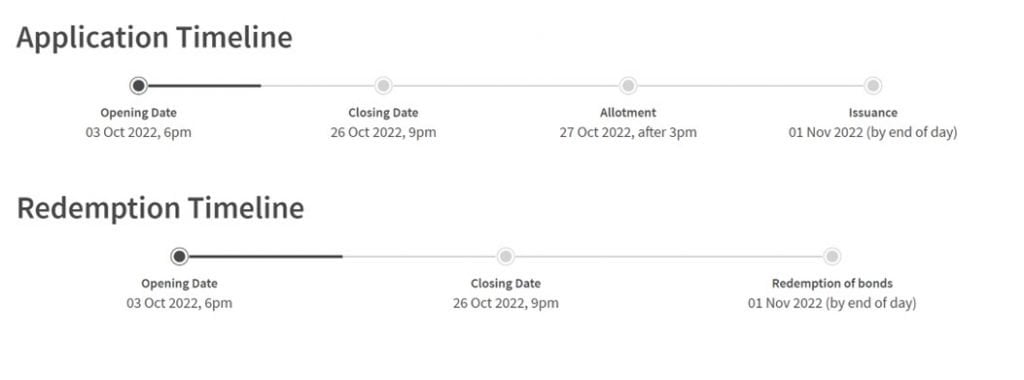

Application Timeline for the October Singapore Savings Bonds

Application timelines are set out below.

Don’t forget to apply before 9pm on Wednesday, 26 October 2022 if you’re keen.

Application method is via the internet banking website or ATM of any of the 3 local banks (DBS, UOB, OCBC).

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- Whole bunch of freebies – A free packet of rice (1kg), a free Kopitiam Kaya Toast set, a $1.99 Double Mushroom Swiss at Burger King, and 50% off KFC Zinger Set just to name a few.

- 1.0% base interest on your first $50,000 (up to 1.4%)

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

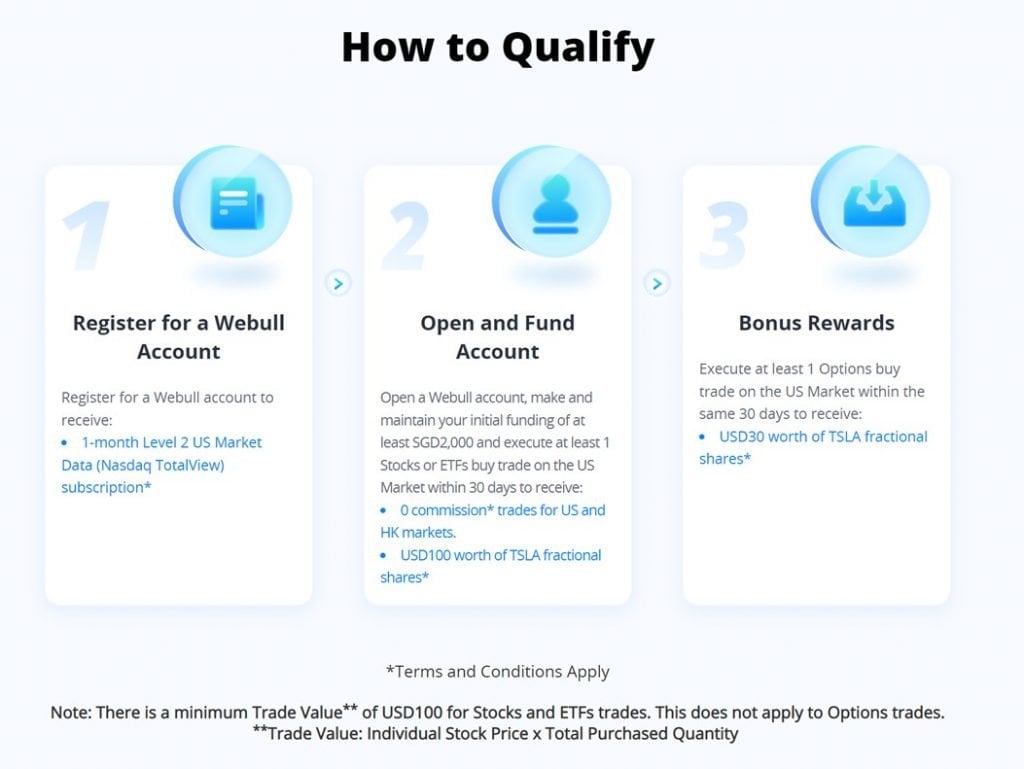

WeBull Account – Free US Stock, Options and ETF trading (Free USD130 (S$185) in Tesla shares)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

To get the USD130 (S$185) in Tesla shares, you just need to:

- Sign up here and fund S$2000

- Make 1 US Stock or ETF trade (you get USD100 in Tesla Shares)

- Make 1 Options trade (you get USD30 in Tesla Shares)

If you find this article helpful for you, please do consider signing up for the Patreon subscription. Most of the regular macro updates and changes to my portfolio positioning have moved there.

At S$15 a month you get the premium weekly market updates.

At $25 a month you get my full stock and REIT watchlist, and at $40 a month you get updates on changes to my portfolio positioning.

Don’t be penny wise pound foolish.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 100 USD in Apple Shares with Webull, a zero commission broker.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

Hi FH, sorry if this comment doesn’t exactly pertain to the subject at hand. To give context, I’m quite young and only just recently got access to brokerage services. I invested into crypto at the peak and used leverage so suffice to say I’ve paid quite a bit in “tuition fees”. Recently, I’ve been quite interested in US equities domiciled in Singapore such as KORE and Digikore REIT given their attractive yield spreads. However, I’m concerned about the recent rate hikes, recession and possibility of high FX risk given the fact that USD/SGD is so high right now. Do you think such REITs would be good to scoop up around 2023 Q1 -Q2 when things settle down? Or do you think the macro condition will further detoriate longer? Thank you so much for your blogs, look forward to reading them everyday!

Hm will see if I can share some views on this, perhaps in next week’s article.

For now you can see my latest macro views in this piece: https://financialhorse.com/how-i-will-invest-1-million-in-2023s-market-crash-as-a-singapore-investor/

Good one FH ! On penny wise, pound foolish, looking at the big picture and prioritizing based on individual situation.

Seems many want to have their cake and also eat it. And lazy to go MAS website to read and think. Every day someone will ask what’s the yield, when close, how to apply, etc.

Every instrument has pros and cons. And I agree with you there’s no need to freak over the 0.1 or 0.5% difference in rates unless one is going for 6 or 7 digits amount. Even that the difference is not significant.

When the situation reverse as it will, the short sighted will ask why again. Lol. My view is the current rate is not sustainable in the mid to long term hence my bond ladder is designed to smoothen that out.

Someone asked why invest half of my networth in bonds a few years ago. Ha, I’m still overall positive, are you? It shielded me from this rout in equities with a sustainable passive income in my retirement. Everyone should think and execute based on their unique situation. My way may not be the best for everyone. You prefer liquidity, i prefer sustainable income over long term. You want your cake and also eat it? Teach me how? Just my personal opinion from personal experience.

Agreed! Each instrument has their own pros and cons, there is no free lunch in this world.

While I prioritise liquidity, I dont expect every investor to be the same as me.

It’s well worth taking the time out to understand each instrument, and figure out what (and what proportion) works for each individual – as you yourself have done well!

I hope the last part of your reply is heed by the readers. From all the questions asked in various blogs and GC I get the impression that more than 50% don’t bother to read MAS website to understand those 3 classes of instruments. Some are like “speculating”; trying to predict amd capture that extra 0.1, 0.2% interest in the short term in T Bills. There are better things to do in life than freak over a $5, $10 more in interest a year. You can see that the 6M TB is overwhelming popular but not the 1Y TB. The SGS has even fewer retail takers except maybe the HNWIs I think. Lol. What this means is most people just want to speculate (short term) instead of invest (mid to long term). As a bond investor, I think this is unhealthy. Bond is an asset class that is a component of a portfolio to to earn stable income and also mitigate the volatility of a portfolio. That’s my approach. It’s ok if anyone don’t agree.

I assuming you hold the bonds to maturity with hardly any intention to trade?

Yes. Collect 5 figure interest every year for expenses.

I once tried to lock in a $9K profit in 2018. Queue for a few months and gave up.

HI FH, instead of SSB vs T-bills, how abt applying T-bills using CPF OA (provided one does not have interest in investing using CPF OA or other purposes, housing loan etc). Would be great to hear from you.

Yes been meaning to write on this. Will get an article out next week. 🙂

Great and comprehensive analysis of SGS . Thank you for the kind effort in putting up this .

Thanks ????yau

Thanks! Hope it helps!

Thanks for article and comments/advice. One question – does your bank allow you to apply for a new SSB if you don’t yet have the liquidity to pay for the new issue (while waiting for the redemption proceeds which are going to be received only on November 1 (but the deadline to apply for the new bond is October 26)? Thank you.

The cash is deducted from your account when you apply for SSBs. As long as you can find a way to cough up the cash when you apply, the bank does not care where the money comes from.

Prudent investment.

Hi FH. If i already hit the 200k limit of SSB, would it be possible if I sell some today eg. 50K, and apply for 50K today? Thanks for any advice.

My understanding from the bond docs is that yes this is possible.

Funnily enough I just did the exact same thing as you, put in my orders yesterday.

I will find out tomorrow if this is indeed possible. 😉

Tested and proven. But dint get the extra 500 units.

Was gonna reply you the same as well. I managed to get it too, but only the $10,000. Bummer.