If you haven’t been keeping track of interest rates for a while, you’ll be pretty amazed by the yield on Singapore Savings Bonds these days.

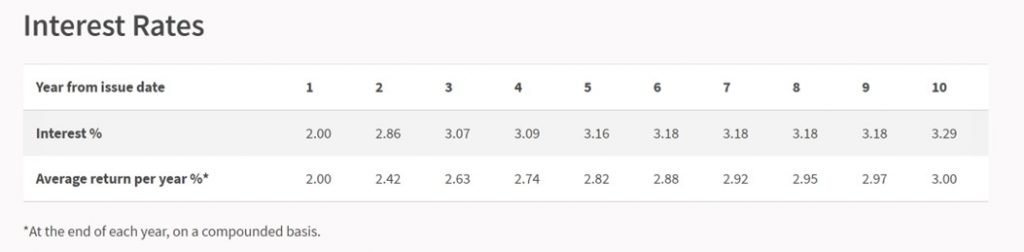

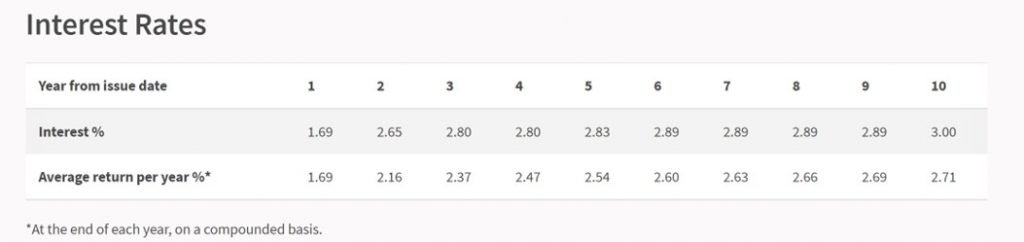

The July 2022 Singapore Savings Bond yields are below, and they’re one of the most attractive yields in a while.

Starting at 2.0% for the first year, and going as high as 3.29% in the 10th year, these bonds are even better than those at the peak of the 2018 rate hike cycle.

And with interest rates continuing their march up the next few months, the Singapore Savings Bonds might get even more attractive going forward.

I’m a buyer of the July Singapore Savings Bonds, and I will likely be applying every month going forward.

A lot of you have been asking for my views on the Singapore Savings Bonds and where to park excess cash, so I wanted to share some views in this article.

This was originally a Patreon article, but am sharing it in the hopes it would help all readers. Do support FH as a Patron for more content like this.

Basics: How do Singapore Savings Bonds work?

To recap the key features of the Singapore Savings Bonds, they are:

- Risk Free

- Can redeem any time with accrued interest

- Maximum of $200,000 (in multiples of $500)

1. Risk Free

Singapore Savings Bonds are fully backed by the Singapore Government.

Enough said.

This is as close to risk-free as it gets.

2. Can redeem any time with accrued interest

Singapore Savings Bonds can be redeemed at any time, and you will get back your principal in full together with any accrued interest.

One point to note is that you don’t get the cash back immediately.

The redemption moneys are only credited to you at 2nd business day of the following month.

So you may need to wait potentially up to 1 month to get the money back (if you apply at the start of the month).

This is crucial to note for liquidity requirements.

You can see the example redemption timeline for July below:

3. Maximum of $200,000 (in multiples of $500)

Each person can apply for up to $200,000 worth of Singapore Savings Bonds, in multiples of $500.

If you’ve busted your limit, you can use your spouse’s or children’s names to apply as well.

FAQs about Singapore Savings Bonds

Now I’ve been getting a lot of questions about Singapore Savings Bonds, so I wanted to address the big ones below.

Will interest rates on SSBs go up further?

This seems like a simple question, but man… accurately answering it requires a deep understanding of financial markets and politics.

Singapore Savings Bonds interest rates track the Singapore Government Security yields. Which in turn are heavily influenced by US interest rates.

So this is basically a question on where the US interest rate curve will move over the next few months.

The short answer is that – no one has any clue.

The long answer is that – yes it is most likely to go up given the Fed’s path of aggressive interest rates.

But the rate hikes are more likely to hit the short end of the curve (1-3 year interest rates).

Whether the long end of the curve will go up significantly is still not very clear for now.

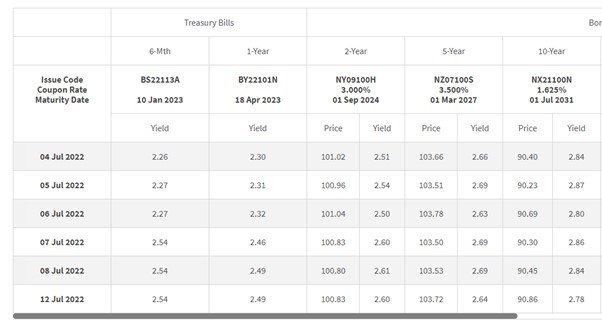

Here are the latest SGS yields, and you can see that:

- The front end (1 year) has moved up to 2.49% (vs 2.0% for the July SSB)

- The long end (10 year) has dropped to 2.78% (vs 3.0% for the July SSB)

So the August SSBs are likely to have a higher short term interest rates, but lower long term interest rates.

My personal view on US Interest Rates?

My personal view, is that the short end and long end will probably both go higher before the end of this cycle.

Which means the Singapore Savings Bonds are going to get even more attractive in the months ahead.

But I could be wrong.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great nuggets of wisdom on Twitter.

Don’t forget to sign up fr our free weekly newsletter too!

[mc4wp_form id=”173″]

Should you apply for the July Singapore Savings Bonds or wait for higher interest rates?

A lot of you have been asking me whether it makes sense to apply for the July SSBs, or wait for higher interest rates.

My view as shared above, is that I think interest rates both at the short end and at the long end will go up over the next few months.

Ie. The Singapore Savings Bonds will get more attractive over the next few months.

But I definitely could be wrong on this.

And another point to note, is that these Singapore Savings Bonds are likely to be very hot.

Which means allocations might be quite tight.

How much are you likely to get?

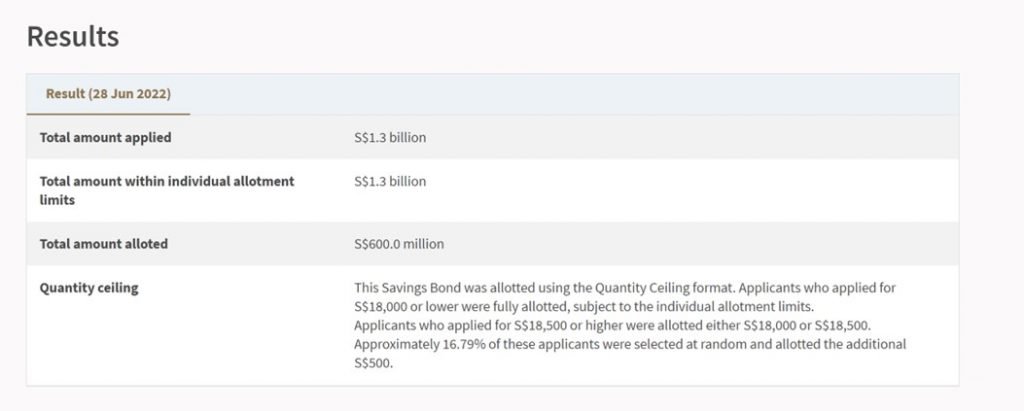

For the June Singapore Savings Bonds – the allocation was only $18,000 per person.

Okay to be fair the June SSB offer size was slightly smaller at $600 million (this month is $700 million).

But the yields last month were also a lot lower than this month’s:

Given how hot the Singapore Savings Bonds are, if I were to venture a guess I would say you’re going to get even lower than $18,000 this month.

Should you apply for the July Singapore Savings Bonds or wait for higher interest rates?

So to answer the question – it depends on how much you’re applying for, and whether you’ve already hit the $200,000 cap.

And how much cash you have lying around.

For example if you’re very far from the $200,000 cap, and you have a lot of spare cash lying around, you might as well apply and lock in the yields.

Because even if you wait for the “perfect” SSBs and apply for $100,000 a few months from now, you may not necessarily get the full allocation when the time comes.

If interest rates do go up, you can just redeem and swap out for the newer SSBs (although there is a bit of cash management because you will need to redeem the bonds and wait for the cash to come back then use the cash to apply for the following month’s bonds).

Whereas if you’re very near the $200,000 cap, then there’s a bit of opportunity cost.

Because you might redeem $100,000 of the older bonds, but only get $15,000 this month, which leaves $85,000 cash with no home.

So you do need to adapt the decision making based on your own circumstances.

What if you’re already maxxed out at $200,000?

If you’ve already maxxed out $200,000, you need to make an educated guess as to how much you are likely to get each month moving forward.

So if you think that you will get $20,000 allocation next month, you should be redeeming $20,000 each month, and applying for that amount (and top up a bit as a buffer).

And you apply on the last day of application, so you minimise the liquidity cost of your cash.

And then when the allocations are out – you recalibrate future months based on the latest allocations.

How am I subscribing for the Singapore Savings Bonds?

Personally for me, most of my Singapore Savings Bonds are from the 2018 – 2019 cycle.

The lowest yield bonds that I own are paying 1.7% in the third year, which makes it a no brainer to redeem and buy the newest Singapore Savings Bonds with higher yield.

The problem for me is that while I think yields are going up in the near term, it looks like the allocation will be a problem.

So I’m not going to wait for the perfect Singapore Savings Bonds to come around.

I’ll probably just be applying for every month’s Singapore Savings Bonds from now until the end of the year.

And if my allocations are filled, I’ll start redeeming some of the earlier Singapore Savings Bonds to recycle the cash into these newer bonds.

But that’s just me, you’ll need to decide if the same makes sense for you.

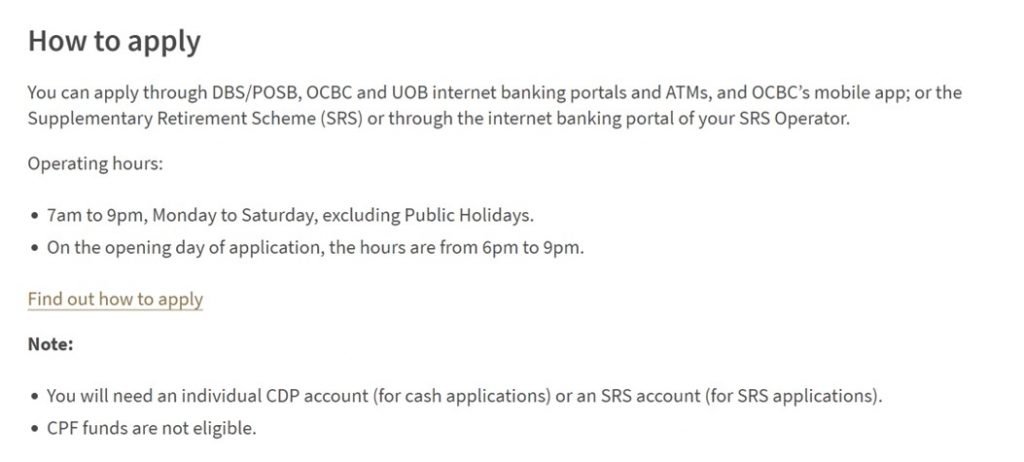

How to apply for Singapore Savings Bonds?

Application for the Singapore Savings Bonds are via any of the 3 local bank, pretty similar to how you would apply for an IPO.

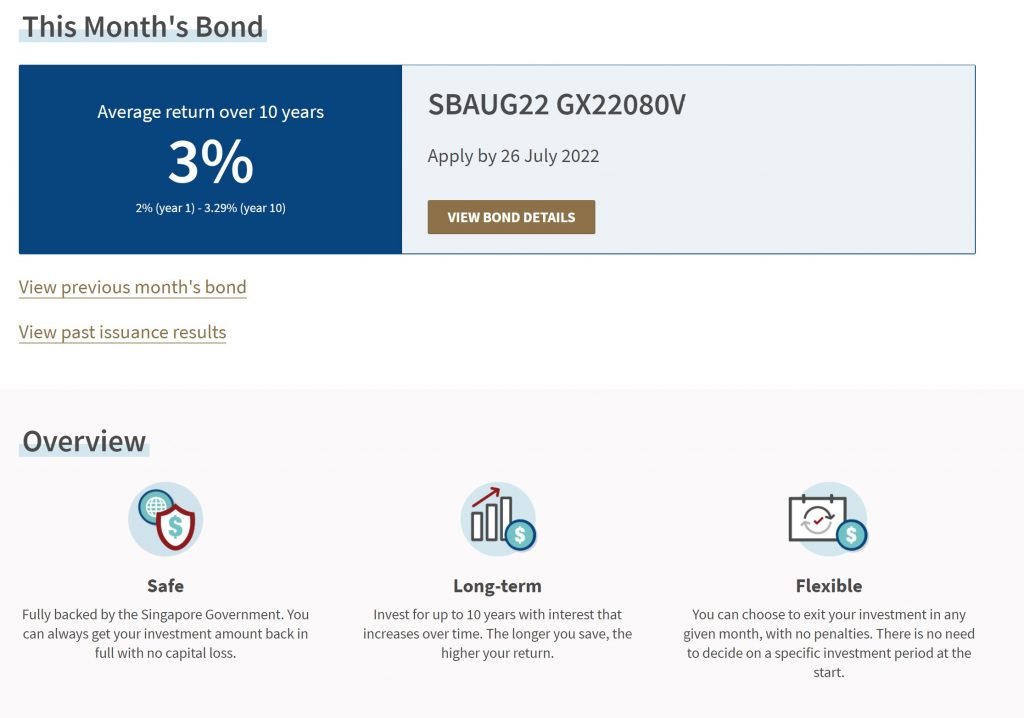

Last day to subscribe is 9pm on 26 July 2022, so do mark that date on your calendars if you are keen!

Refinancing your mortgage

With rapidly rising interest rates – it might pay off to look into refinancing if your loan is coming due.

I know a lot of you have been writing in for my views on fixed vs floating loans, and I plan to write a full article for this.

But in this market – I think you’re pretty much forced into taking floating. The banks themselves know interest rates are going up quick, so the fixed rate loans are priced in such a way that they aren’t sufficiently attractive (in my view).

In the meantime, there’s a fantastic tool by Property Guru.

Do give it a try if you’re close to refinancing.

It’s completely free – you just input your mortgage details, and the tool lets you know whether you’ll save money by refinancing.

If the answer is yes, they’ll give you recommendations on what loan to take.

If the answer is no, you can set up a reminder for the tool to remind you when its time to refinance.

I set up the reminders for my own properties just this week and it’s pretty neat.

Do give it a try here.

As always, this article is written on 15 July 2022 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon. You can access my full personal portfolio to check out how I am positioned for the coming downturn too.

Looking for a low cost broker to buy US, China or Singapore stocks?

My recommendations on Stock Brokers here.

Get 120 USD in Microsoft Shares with Webull, a zero commission broker.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to saxo@financialhorse.com for full steps).

Or Interactive Brokers for competitive FX and commissions.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

Dear Financial horse,

Great article as always.

Just like to bring a small pointer to your attention. To buy Singapore saving bond for your SG children, i believe your children need to be at least 18 years old.