Singtel is one of those quintessential Singaporean stock that every Singaporean knows (and may even own).

Back in 1993 when Singtel IPO-ed, there was a scheme known as Singtel Discounted Shares (SDS), which allowed Singaporean CPF members to purchase Singtel shares at a discounted price.

This led to broad ownership of Singtel among retail investors of a certain age, making this a very followed stock.

Unfortunately, this is what the 5-year chart looks like, which is not pretty.

Note: The research for this article, and most of the charts here, are sourced from ShareInvestor Webpro. It’s a great way to quickly perform research on Singapore stocks, far more comprehensive and flexible than other options like Yahoo Finance.

You can learn more in my review on ShareInvestor Webpro here.

Basics: What is Singtel?

Singtel is a telecommunications company – it provides phone and mobile data services.

Singapore and Australia (Optus) are the core operations. Singtel also has significant operations via ownerships of telco players in India, Thailand, Indonesia, and Phillipines.

We did an article on Singtel 2 years back, so do check it out for more background. Otherwise we’ll jump straight into the juicy stuff.

What happened to Singtel’s earnings?

It’s not immediately obvious when you think about it – but COVID19 has decimated Singtel’s core business.

It’s funny because you would have thought that lockdowns would actually boost demand for phone services / mobile internet.

Unfortunately, what actually happened was that because everyone stayed home and stopped travelling around, reliance on mobile data or roaming dropped drastically – and those were the high margin earners for Singtel.

Instead, because people stayed home, they accessed the internet via home wi-fi, which is a fixed payment plan regardless of how much they use.

So Singtel lost the high margin mobile data earnings, and couldn’t earn from the higher home data usage. Bad for Singtel, but good for consumers.

Throw in the continued transition to SIM only plans, and competition in pricing plans, and that led to a poor business showing for Singtel.

I’ve extracted their explanation below, it’s well worth the read if you want a bit more colour (well written too).

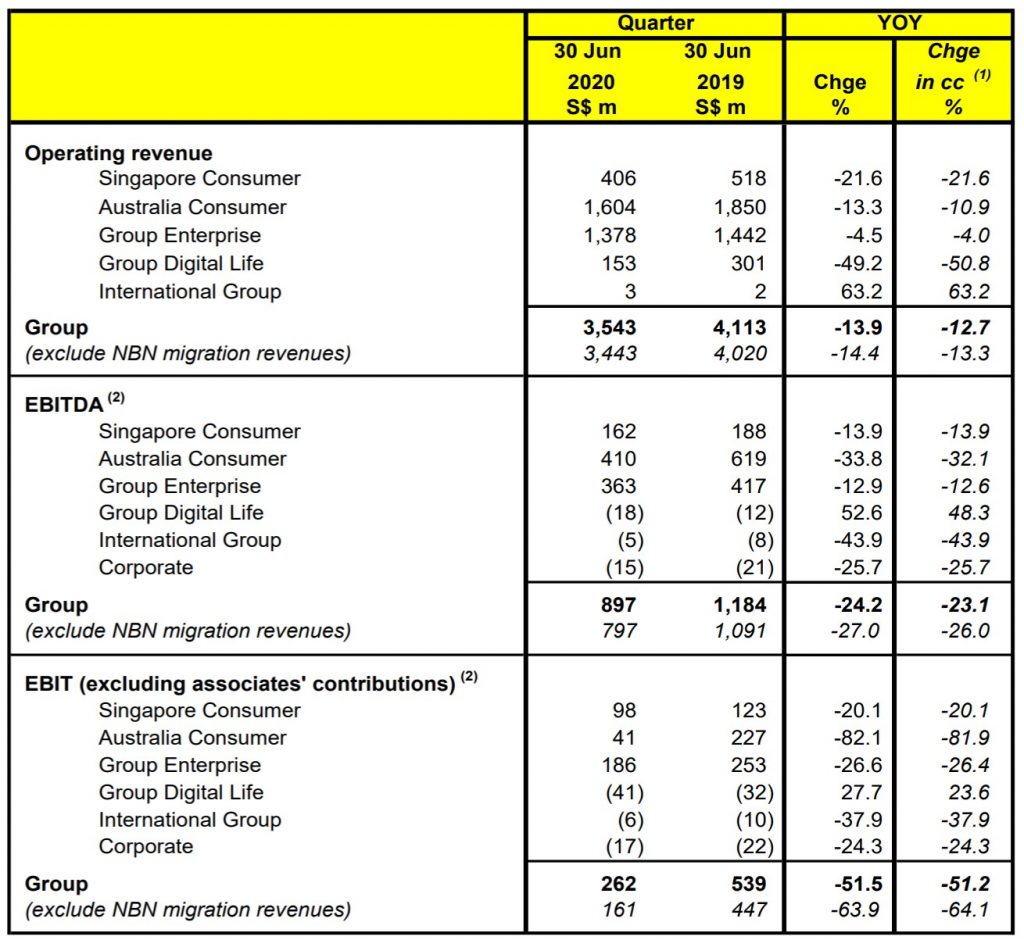

For the first quarter ended 30 June 2020, the Group faced challenging market conditions as COVID-19 caused shutdowns across Singapore and Australia. Travel and movement restrictions and lower footfall in retail stores severely impacted roaming and prepaid mobile revenues and equipment sales, while the global economic slowdown dampened both consumer and business spend. Some ICT projects were deferred or delayed, resulting in increased project costs and slower billings. The above factors, together with intense price competition across markets and declines in carriage revenues, resulted in operating revenue and EBITDA for the quarter declining by 14% and 24% respectively. EBIT fell 52% mainly reflecting the lower EBITDA.

In Singapore Consumer, operating revenue fell 22% with the government’s mandated COVID-19 ‘circuit breaker’ measures in April and May. Mobile service revenue declined due to a sharp fall in roaming as well as lower prepaid usage as customers relied on wifi as they stayed indoors, and the number of tourists and foreign workers fell significantly with border closures. Movement restrictions during the period also affected equipment sales. EBITDA fell 14% after including S$17 million of Jobs Support Scheme credits.

Operating revenue in Australia Consumer decreased 11% mainly from Mobile revenues. Mobile service revenue declined due to lower roaming, late payment fee waivers and credits to frontline healthcare workers, as well as higher SIM-only customer mix and continuing data price competition. Equipment sales also declined given lower retail footfall, flow on impact of lengthening handset replacement cycles and cessation of subsidies. EBITDA fell 32% with lower operating revenue, fixed margin erosion and operating expenses related to COVID-19 such as onshore care agents and debt provisions from financial hardship relief. Retail fixed margins were impacted by the migration of customers from Optus’ proprietary networks to NBN which resulted in a much higher mix of NBN broadband customers at low resale margins.

The enterprise business was similarly impacted by the pandemic. Group Enterprise’s operating revenue fell 4.5% due mainly to continued declines in carriage services and weak business sentiment. Mobile service revenue was lower with steep declines in roaming and voice. Equipment sales also declined from lower mobile connections with reduced customer engagements. ICT revenue growth was affected by project delays and deferments as customers scaled back their operations as a result of a drop in business activities. However, data centre revenue increased with new wins. With the lower operating revenue and higher ICT mix, EBITDA fell 13% after including S$43 million of Jobs Support Scheme credits.

What I don’t like about Singtel

In my original review on Singtel back in 2018, I shared that I did not like Singtel for 3 main reasons:

- Poor industry dynamics

- Expansion into new sectors may not bear fruit

- Lack of near-term catalysts

Let’s see if anything has changed for each of them – 2 years on, and a 30% price drop later.

(1) Poor industry dynamics

In my view, this is the main problem with Singtel – Industry dynamics continue to be incredibly poor.

These days, Telcos have become no more than “dumb pipes”. All the value in this value chain has migrated upstream to the software providers, or the hardware providers (silicon side).

All Telcos do in this value chain is to connect the players to each other. And there’s not a lot of value you can squeeze out of that.

There are only 2 saving graces to this business: (1) if you can build a monopoly, and (2) very strong cash flow generation.

Building a monopoly

If you can build a monopoly, then the problem goes away because you can price in a way that protects your profits.

Unfortunately, governments are also aware of this, so consolidation into a monopoly status has been tough in almost every market. All across Asia – from China to Australia to Singapore to India, we don’t see one telco dominating the market.

There’s always some competition in each market, that prevents one player from becoming the monopoly required to secure good profits long term.

So while this sounds good on paper, practically it is tough to accomplish. The reality for now, is that this is a business that requires big upfront Capex, but doesn’t give you the monopoly required to protect profits.

Where it does though (like Netlink Trust), those players become good investments.

Cash Flow Generation

The other saving grace about this business, is that is generates a ton of cash flow.

You’re basically collecting bucketloads of cash every month from users who pay for phone plans. This cash flow is incredibly steady.

What then do you do with the cash?

You can either use it to (1) pay a dividend, or (2) invest in new businesses.

Guys like Softbank and Reliance Jio, they went down Route 2, and invested not in the Telco business but in the real value providers – the software and cloud players. So they basically used the Telco business as a cash cow, and used that cash to invest in other stuff.

The problem with Singtel, is that they took the cash and went to buy other Telcos. This failed to diversify the business beyond pure Telco, because it only diversified them geographically, but not in terms of business lines.

And over time, the poor industry dynamics started to show in declining earnings, so Singtel had to start going down Route 1 to appease shareholders, paying out greater and greater dividends.

So if Singtel had tried to become a player like Reliance / Softbank, and used that money to invest in Alibaba / Tencent / the other Unicorns in their heydays, we could be looking at a very different Singtel today.

Unfortunately, it is what it is, and we have a Singtel that owns large stakes of other Telcos instead, all of which face the same underlying issue.

(2) Expansion into new sectors may not bear fruit

To be fair, Singtel did take steps to try to move up the value chain. They tried to launch Hooq (a Singaporean video on demand streaming service), and they bought adtech firm Amobee.

My concern back in 2018 was that while the idea was good, much of the success would hinge on the execution of the strategy.

In this space you’re competing with the real behemoths like Google and Facebook, and I wasn’t so sure whether Singtel with all their old-world processes could execute well enough to make inroads into the industry. It’s the same problem that SingPost had when they tried to expand into US eCommerce.

It was still a bit of a surprise earlier this year when Singtel announced that Hooq would be shut down for good. The official reason was that “it could not receive new funds from new or existing investors”, but given how hot Netflix is, I suspect what this really means is that the performance of Hooq was so poor that it was hard to raise funds from investors, and Singtel couldn’t justify throwing in new funds to turn it around.

There’s still adtech firm Amobee, but again, I’m not super optimistic for the reasons described above.

Accordingly to Singtel: Amobee’s revenue fell due to a significant cut back in advertising spend by customers as a result of COVID-19 and a reduction in TV revenue following the licensing of its technology platform to ITV plc from July 2019. In addition, technology licensing fee income received from ITV plc recognised in the last corresponding quarter did not recur this quarter.

(3) Lack of near-term catalysts

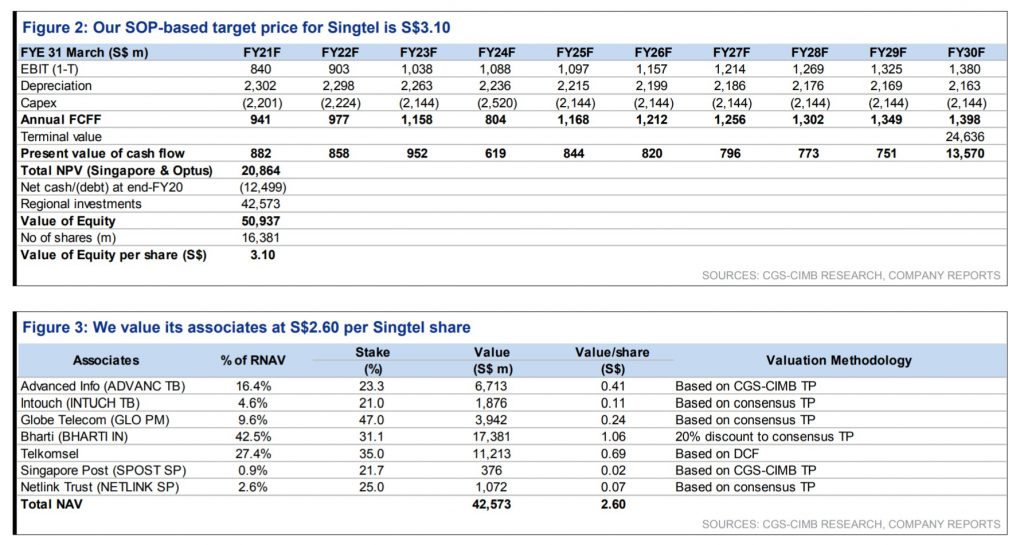

Singtel has always been cheap on the sum of the parts (SOTP) analysis.

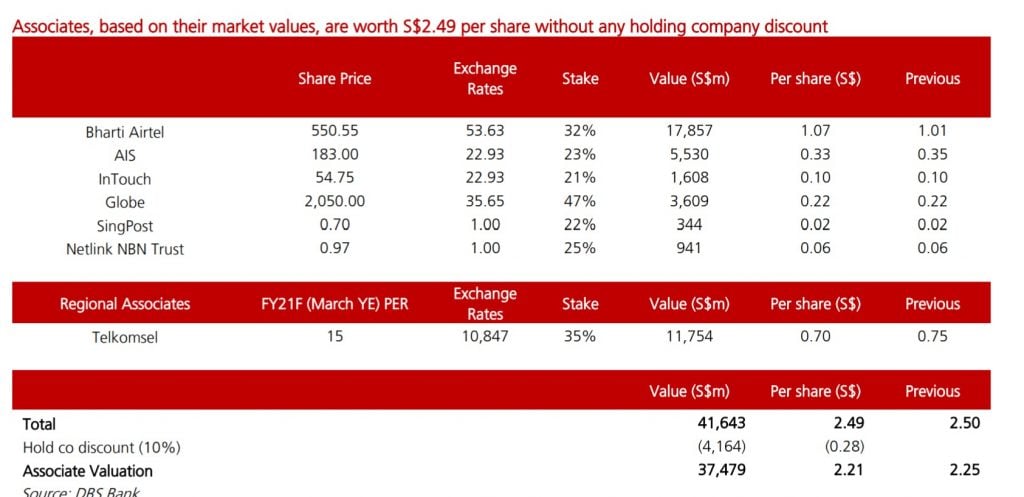

When I wrote the original article, DBS had a $3.7 SOTP valuation for Singtel.

SOTP valuation today, is about $3 ($2.49 for the associates, and $0.48 for the core business).

The problem with SOTP analysis, is that you need a catalyst to unlock value, otherwise it can trade at a discount for extended periods.

There wasn’t any catalyst back in 2018, but it seems today Singtel is considering the sale of its cell towers in Australia:

Singtel has engaged advisors for a potential Optus tower sale. While still in the preparation stage, we believe a tender may be called in the next few months. The Australian Financial Review reported in Mar 2020 that the towers may be worth at least A$2bn (S$2bn). Singtel said potential proceeds may be used to fund 5G capex and pare down debt, though we think a small special DPS (2-4 Scts, if we assume 20-30% of S$2bn) is also possible. The IPO of Amobee and Trustwave are still being considered but may not happen in 2020-21F, as earnings are still not at optimal levels.

Maybe if a sale is announced, there could be a near term boost to share price.

But longer term, I don’t see how the sale would solve the problem with the industry dynamics highlighted above, especially if the proceeds are going to be used to fund Capex and pay down debt or pay a bigger dividend.

In fact, the Optus cell towers are exactly the kind of business I want to own instead (because of monopoly status), rather than Singtel itself.

FYI we’ll share commentary on the 2020 crisis every weekend going forward, so for those of you who haven’t signed up for our mailing list, please do – its absolutely free.

It’s a weekly newsletter that goes out at noon every Sunday, and rounds up the week’s posts so you never miss anything.

[mailmunch-form id=”928667″]

Valuation of Singtel

Both DBS and CIMB have a sum of the parts valuation of Singtel at about $3.

For once, I don’t disagree with them here. I do agree fair valuation for Singtel is probably anywhere from $2.50 to $3.00.

The only problem is what would it take to realise that fair valuation.

Downside is limited – Like Keppel?

In some ways, Singtel feels to be in the same situation as Keppel, in that at this price, the downside is probably limited because it’s already so oversold, and so cheap on a valuations basis.

The problem is that there’s just very little growth in the business, so the upside is also limited.

Best case if COVID goes away, Singtel’s earnings will recover, but probably to a level below where they were pre-COVID.

Shareholders of Singtel

A couple more points to touch on, then I’ll round up my views.

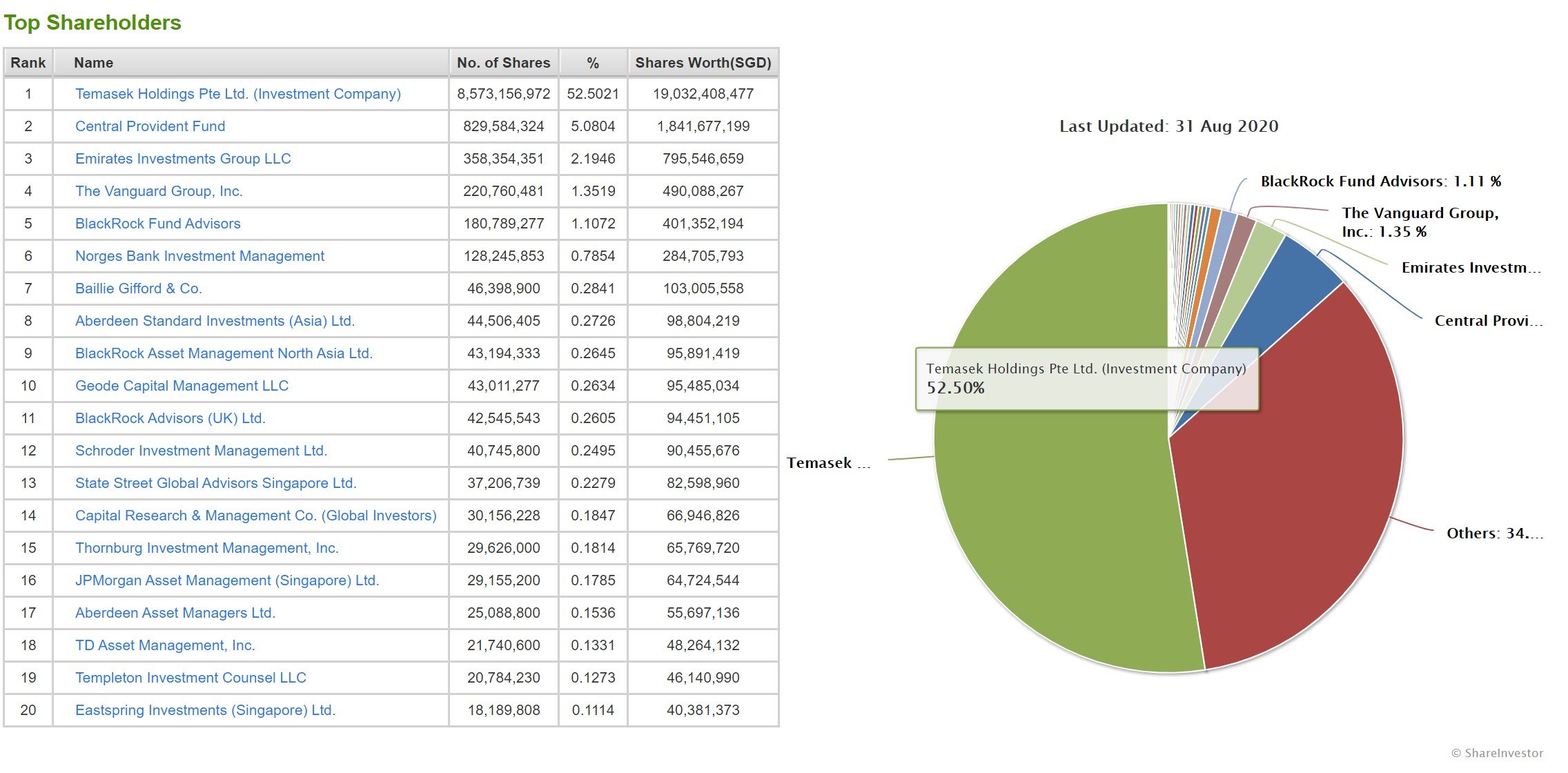

Temasek is the single largest shareholder, coming in at 52%. Next largest is CPF at 5%, because of the Singtel Discounted Shares back in 1993. The investors from back then are still holding on.

Institutional investors don’t feature strongly in their holdings of Singtel.

With a majority stake by Temasek, I don’t think there’s any solvency or liquidity related risk here. I also don’t see much chance of any corporate action from Temasek because Singtel isn’t doing as badly as some of the other portfolio companies like SIA, Sembcorp, Keppel.

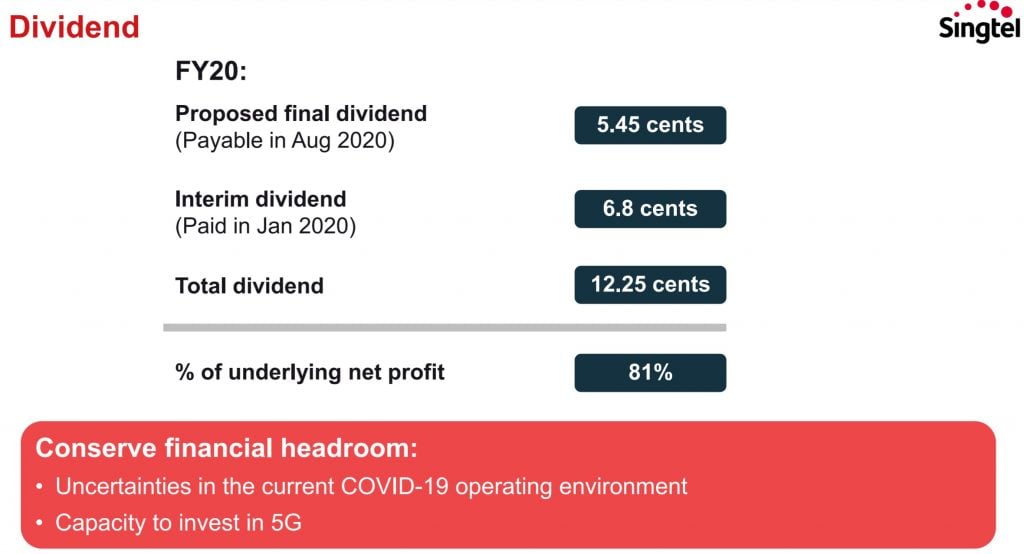

Singtel’s Dividend (5.5% after cut)

Payout ratio is dangerously high.

It stayed at about 80% for many years, then spiked in the last 2 years because of deteriorating business fundamentals.

This led to a dividend cut this year to 12.25 cents (originally 17.5 cents), which is a 81% payout ratio. I think this is a good thing as it helps Singtel to conserve cash, and it was clear the previous dividend policy was not sustainable.

At current price of $2.2, that’s about a 5.5% yield.

One thing to note is that Singtel has approved a Scrip Dividend Scheme at the recent AGM. So going forward, shareholders may get their dividend in the form of Singtel shares rather than cash.

It’s annoying because of the odd lots, but it does help Singtel conserve cash that can be better used on the core business.

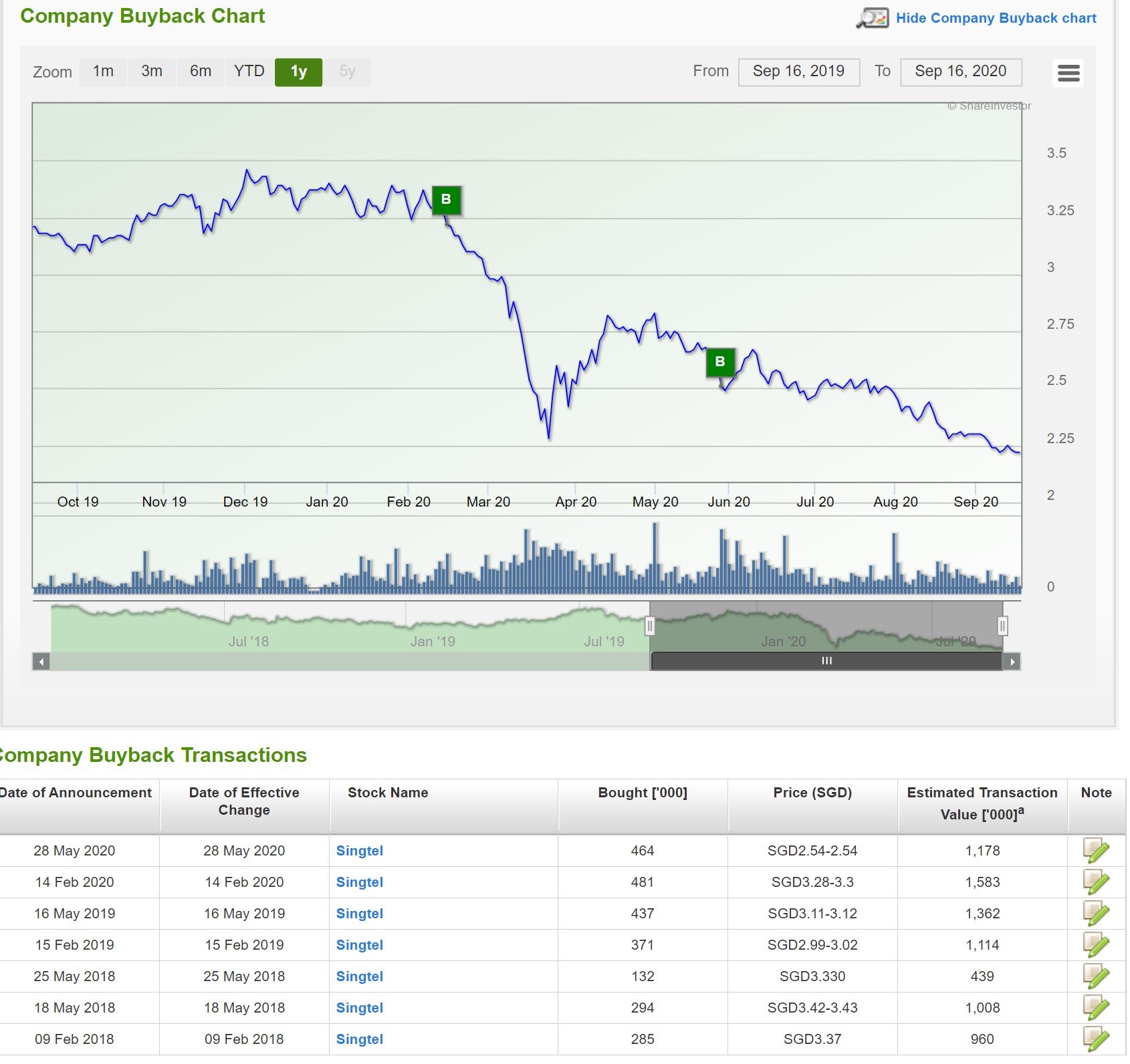

Share Buyback

Buyback is almost non-existent. This makes sense because all the cash is returned to shareholders via dividends and not buybacks.

Note: ShareInvestor WebPro is a great and very cost-effective way to do analysis like this – beats trawling through the SGX announcements one by one. If you do such analysis regularly, well worth checking it out. Our review on WebPro (and Promo Code) here.

So… I failed to take my own advice on Singtel

Here’s where it gets interesting.

I know that Singtel is a poor long-term investment. But in 2019, after a big sell-off in Singtel, I decided to buy some as a short-term trading position because it was so oversold.

You can see where I bought marked in the chart below.

The trade worked out well at first, and at one point I was sitting on a 20% – 30% gain.

But then I got greedy, and I failed to exit.

And of course, the rest is history, because COVID happened.

It’s a very small position to be fair, but it places me in a weird situation of what to do next.

Do I cut losses and exit to redeploy the cash elsewhere, or do I hold out for a short-term bounce and sell into strength?

It’s a similar conundrum to what a lot of you guys have written in about.

For now, I’ll probably hold on and hope for a short-term bounce, but I would love to hear what you think about this.

Closing Thoughts: Would I invest in Singtel?

I like Singtel’s price. I also like the Temasek backing and the dividend.

But I just cannot bring myself to like the industry that Singtel is operating in.

As the quote by Warren Buffet goes, “When a management with a reputation for brilliance tackles a business with a reputation for bad economics, it is the reputation of the business that remains intact.”

That’s Singtel.

You can bring in the best management team, and I fail to see what they can really do to change the industry dynamics. It’s a high capex industry, without monopoly protection, and where there’s very little value add to the consumer.

They best they can do to me, is to choose not to play in this industry. Go the way of Softbank and Reliance – take the cash flow from this business, and invest in another high value industry like software or cloud. Or heck, just go the way of Softbank and use it to buy call options on the NASDAQ. (But please no real estate, one SPH is enough).

Instead they’re going down the route of paying dividends, and selling off key infrastructure (Optus cell towers) to pay down debt and fund 5G capex.

If this is indicative of the future direction of Singtel, it’s a direction I do not want to be part of as investor. Netlink Trust is a better play to me as a core utilities play.

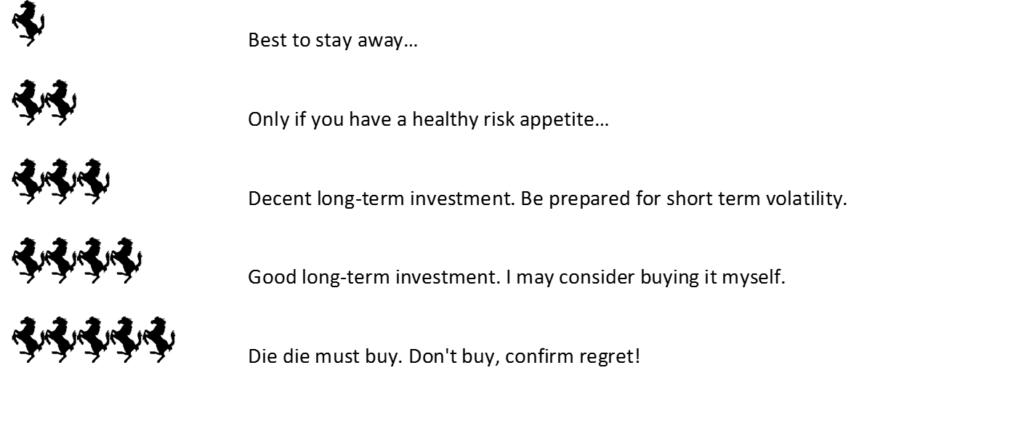

That said – just like Keppel, I do think the stock is oversold, and very cheap on a valuations basis. A near term bounce is possible if we get positive news on COVID. I’ll give Singtel a 2.5 horse rating.

As always, this article is written on 18 Sep 2020 and will not be updated going foward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Share your comments below!

Singtel – Financial Horse Rating

Financial Horse Rating Scale

Support the site as a Patron and get access to my personal stock watch list, as well as my personal portfolio allocation.

Do like and follow our Facebook Page, or join the Telegram Channel. Never miss another post from Financial Horse!

Join our Facebook Group to continue the discussion, everyone is welcome!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

I think Singtel is not managed well. Poor vision company. I have on my limited charting analysis, looking for 1.95. What would be dividend at 1.95?

It will be 6.4%, assuming no cut. 🙂

What if the FB, Amazon and Google type investors start to find value in the direct consumer access in emerging markets of India (Airtel), and lucrative market of SG and Australia? Shouldn’t Singtel aggressively look at that?

That’s a good point, and yes I agree it’s worth a shot for Singtel. For now, they don’t seem to be going down this route aggressively though.

Hi Financial Horse, thanks for your sharing. Do you mind sharing your views on the medical penny stock market which has been turbulent since the start of Covid, the recent situation (significant downward correction after initial surge) and performance of the key players (Top Glove, Riverstone, Medtecs etc.)?

Cheers!

That’s an interesting one. Let me think about it and see if I can do something on it.

With the Scrip Dividend Scheme approved, can you comment on whether you will accept the dividends in shares (odd lots) or cash? And the reasons why?

Also, what are your thoughts on scrip dividends in general? Many counters such as the banks are going in this dividend scheme as well.

Dank je!

Marc

My personal rule is to always take the cash, unless the scrip dividend is at a big discount to prevailing market price (which is rare).

This way, I get the cash, and I get to make the decision on where to deploy the funds. I can reinvest in that counter if I think it’s at a good value, but if it’s pricey, I can deploy it elsewhere. 🙂

Hi, I’ve entered Singtel some time ago like yourself and given the situation, it seems like Singtel is pretty much doomed unless a fancy deal comes along the way that will change Singtel’s strategy etc. What is your way forward on your money stuck at Singtel, as the price looks to continue dropping? Will you cut your losses and exit or will you continue to hold on? And why?

I’ll probably look to sell into strength if I can get a good rally in the stock. I dont like the longer term prospects of Singtel.

They go to the same school, study the same textbooks, sit for the same exam with the same A Star result, report to the same boss, what do you expect? Produce the same dismay result lor.????????????

yes TopGlove will be very interesting to look at.

the only business now which have order for the next 2-3 years with deposit paid. that is a lot of cash in the Bank.

also the price per 1,000 pieces keep increasing every month while production cost remain same.

Sure, I will have a closer look at the glovemakers. 🙂

Hi FH, Great sharing piece as always and very sound approach on this matter. Just one question to ask. What is your view on 5G, do you think that it will beef up SingTel’s earnings? It seems that studies have shown that the ARPU for 5G users are much higher as compared to 4G and will this turn things around for SingTel, Optus and their subsidiaries with better margins? What is your take? Thanks and best regards.

I agree that 5g will lead to higher ARPU. 5G also brings in significant capex requirements though, and with the current shape Singtel is in I’m not sure how they’re going to fund it (sale of Optus towers?).

Even if 5g does well, it still doesn’t solve the underlying problem which is the lack of value provided by the telco. Unless they can turn it into a monopoly, or they can find a way to invest the cash generated in a way that generates good returns, the same problem will eventually manifest itself again. It’s a tough situation.

But to answer your question, if 5G does well, there could be a tradeable short term jump in the stock. I agree that’s possible.

Would rolling out 5G boost Singtel market position? I know other telco like M1 and Starhub were awarded the 5G implementation plan as well. However, among all, Singtel has the deepest pocket; so they should be able to get a head start. Previous 4G implementation in 2012 saw Singtel shares rode on a bullish trend for a few years. Though market is different now, still it would account for some discounted gains, right?

I agree that 5g will lead to higher ARPU. 5G also brings in significant capex requirements though, and with the current shape Singtel is in I’m not sure how they’re going to fund it (sale of Optus towers?).

Even if 5g does well, it still doesn’t solve the underlying problem which is the lack of value provided by the telco. Unless they can turn it into a monopoly, or they can find a way to invest the cash generated in a way that generates good returns, the same problem will eventually manifest itself again. It’s a tough situation.

But to answer your question, if 5G does well, there could be a tradeable short term jump in the stock. I agree that’s possible.

I think your short term jump will come as and when they win the digital banking license with grab.

But I agree with you that in longer term unless they split out the utility portion and the risky portion of the business the value can not be unlocked

Aqgree with AG, Singtel Up coming catalyst would be the award of digital banking license with Grab. Another one is the launch of 5G phones which will attract more upgrades of data plan by their users 🙂

Yeah I don’t disagree with this. That could be one possibility. 🙂

Like the way you articulate and share your opinion.

On the same, can I have your opinion on a company which is a proxy to HK telecom, having exposure in digital banking with SCB in HK via its associate and good dividend paid out since 2018 – PCRD (P15.SG).

Thank you and looking forward to your view

To be honest I am not that familiar with the HK Telco market, but I suspect the same issues will apply there. I will try to have a closer look at this stock. 🙂

Weren’t you warned in school about monopolies? Stop rooting for them to appear, OK? Absolute power corrupts absolutely…When there’s zero competition, it is easy for a big company to tell you whatever it wants… Those data you rely on to do analysis can and have become fictitious at financial fraud committing companies like Enron in the USA, and Barclay’s, AIG, Royal Bank of Scotland, became in the 2008 meltdown.Don’t you see how corrupt the banking systems have become around the world?…

Haha I love this comment. Thanks for sharing, and keeping us grounded! 🙂