There was a time where I dumped all my excess cash into DBS Multiplier. It earned a good 2.3%, and was completely liquid. Boy, those were the good days.

Unfortunately, now that I’m based overseas, I’m in an unfortunate situation where I have some excess SGD that I want to generate interest on short term, and yet still be able to access at a moment’s notice.

Normally, I would go with the Singapore Savings Bonds for something like that, but the complete collapse of the Singapore Government Securities (SGS) yield curve has been a bit of a bother.

Basics: What are Singapore Savings Bonds

I’m sure most of you are familiar with how the Singapore Savings Bond (SSB) works, but I’ll just summarise it quickly for the newer investors.

The Singapore Savings Bond is basically a special bond created by MAS, that is a hybrid between a fixed deposit and a Singapore government security. So you put money in and you get paid x amount of interest twice a year. You can redeem them any time with up to 1 months’ notice, and you get back the complete principal and accrued interest. The maximum duration of the bond is 10 years.

Every Singaporean can apply up to $200,000 worth of Singapore Savings Bonds, and they are completely risk free (backed by the Singapore government).

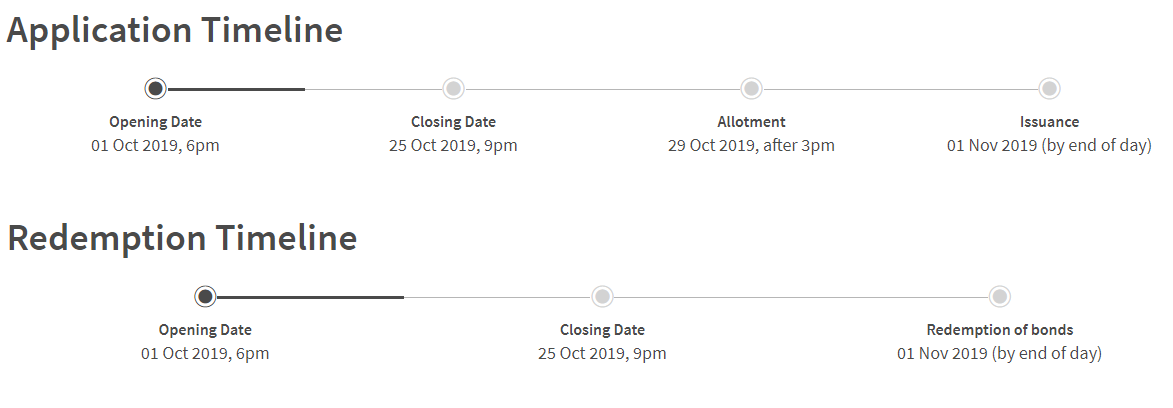

The rough application timeline is set out below, and you basically need to apply for next month’s Singapore Savings Bonds in the current month, and you can also submit a request to redeem any existing bonds in the current month, to receive the money at the start of the next month.

Current Interest Rate

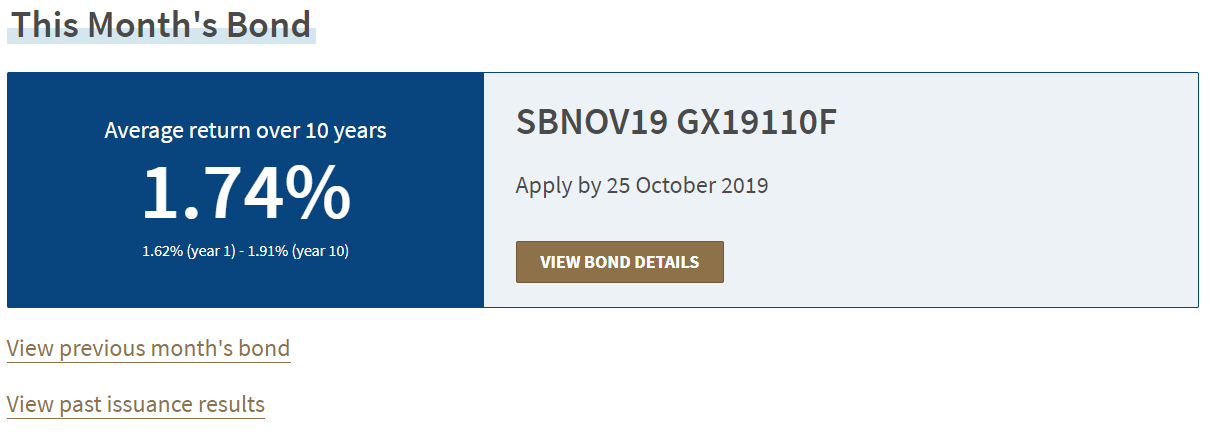

I’ve set out the interest rates for the November Singapore Savings Bond below.

| Year from issue date | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

| Interest % | 1.62 | 1.62 | 1.62 | 1.68 | 1.73 | 1.73 | 1.78 | 1.83 | 1.88 | 1.91 |

| Average return per year %* | 1.62 | 1.62 | 1.62 | 1.63 | 1.65 | 1.67 | 1.68 | 1.70 | 1.72 | 1.74 |

The interest rate is basically tied to the SGS yield curve (the interest rate that the Singapore government borrows at). One interesting quirk is that the SSB yield curve is designed to always slope upwards, so it can never have a situation where the first year interest rate is higher than the second year interest rate.

This almost never matters, except when it does.

And unfortunately, the current SGS yield curve is inverted, which is just a fancy way of saying that the short term interest rate is higher than the long term interest rate.

But the Singapore Savings Bond cannot allow that to happen, so the yields on the SSBs are artificially distorted to achieve an upward sloping yield curve.

This artificial distortion of the yield curve, has one big implication for the Singapore Savings Bond:

SSB is no longer efficient for shorter durations (~ 1 to 2 years)

In January 2019, the 1 year SSB was yielding 2.01%, while the SGS yielded about 2%. So the SSB was pretty competitive.

But this was back when the SGS yield curve was functioning normally, and sloping upward.

| YEAR FROM ISSUE DATE | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

| Interest,% | 2.01% | 2.14% | 2.25% | 2.35% | 2.45% | 2.53% | 2.62% | 2.70% | 2.79% | 2.90% |

| Average p.a. return, %** | 2.01% | 2.07% | 2.13% | 2.18% | 2.24% | 2.28% | 2.33% | 2.37% | 2.41% | 2.45% |

In November 2019, the 1 year SSB now yields it now yields 1.62%, while the 1 year SGS yields 1.84%. This actually means that when you own an SSB, you’re getting a below market interest rate, due to the whole yield curve fitting process.

It doesn’t really make a difference if you plan to hold it for the full 10 year duration, because your 10 year return still averages the 10 year SGS.

But for someone like me, who only plans to put the money in the SSB for about 1 year max, using an SSB is actually no longer as great.

The long end of the yield curve has collapsed

What I actually found more interesting though, was the complete collapse of the long end of the yield curve.

For the record, here is the SSB interest rate from 1 year ago. See that 10 year? It’s a whopping 2.48%. And the current 10 year on the latest Singapore Saving Bond? 1.73%.

| YEAR FROM ISSUE DATE | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

| Interest,% | 1.80% | 2.09% | 2.27% | 2.42% | 2.54% | 2.63% | 2.69% | 2.75% | 2.84% | 2.98% |

| Average p.a. return, %** | 1.80% | 1.94% | 2.05% | 2.14% | 2.22% | 2.28% | 2.34% | 2.38% | 2.43% | 2.48% |

That’s a complete collapse of 75 b.ps in the span of 12 months. Saying that’s a big move, is probably understating the magnitude of this.

Now this isn’t due to the MAS’s or Singapore Government’s fault, the longer end is simply pegged to the SGS yield curve, which trades based on investor demand. So the reason why the yield curve has fallen is simply because more people around the world have been buying bonds.

And there are only 2 reasons why global investors will go out and buy bonds in this magnitude, all across the world:

(1) They expect interest rates to go down further – This is basically a variant of the “greater fool” theory. Global investors basically know that at this point in time, bonds are going to be a poor investment if you hold them purely for the yield. But they’re betting that interest rates will continue to drop, causing bond prices to go up (they trade inversely), resulting in capital gains.

And the only reason why interest rates go down, is because central banks cut them. And the most plausible scenario where central banks cut rates drastically is where the economy slows drastically, and a recession is likely.

The net effect here, is that basically the entire world is now betting that the economy slows drastically.

(2) They are wrong – Of course, the other, scarier possibility, is that global investors are wrong. The economy avoids a massive slowdown, the Federal Reserve does 1 more rate cut and stops, and the economy starts picking up again. This scenario is going to trigger such a massive destruction in fixed income, that the Feds may even be forced to step in.

Anyway, who is ultimately correct is beyond the scope of this article. Personally, I think we are in a bond bubble and bonds are way overpriced, but this will stay the way for the next 1 to 2 years as the global economy slows further, but that’s a topic for another day.

Singapore Savings Bonds has no potential for capital gains

Now another interesting quirk about the Singapore Savings Bonds, is that unlike an SGS or a US Treasury, even if interest rate drops, you cannot sell the bond back to the government at a profit.

So I have a whole bunch of January 2019 Singapore Savings Bonds, with a 1 year yield of 2.01% and a 10 year of 2.5%, which looks fantastic in the current market. If they were actively traded, I’m probably sitting on an upwards of a 10% capital gain.

But because this is a Singapore Savings Bond, if I were to redeem them right now, all I get back is the face value of my bonds. There is just no way to make capital gains from a Singapore Savings Bond.

So back to the greater fool theory above, the Singapore Savings Bond cannot be used in this way. There is no greater fool you can sell your Singapore Savings Bond to, other than to the Singapore government.

So the only reason why you would buy a Singapore Savings Bond, is for the yield.

And just to show how savvy Singapore investors are, the application rate for the SSB peaked some time in March and April 2019 (when the 1 year was 1.95%), and has been on a massive decline ever since.

| ALLOTMENT RESULTS | ||||||||||

| ISSUE DATE | MATURITY DATE | MAX OFFERED($) | TOTAL APPLIED($) | TOTAL APPLIED WITHIN LIMITS($) | AMOUNT ISSUED($) | QUANTITY CEILING($) | % ADDITIONAL ALLOTMENT | |||

| 02/01/2019 | 01/01/2029 | 300,000,000 | 381,743,500 | 367,590,000 | 300,000,000 | 39,000 | 42 | |||

| 01/02/2019 | 01/02/2029 | 300,000,000 | 246,895,500 | 203,269,000 | 203,269,000 | 100,000 | 0 | |||

| 01/03/2019 | 01/03/2029 | 300,000,000 | 456,582,000 | 454,869,000 | 300,000,000 | 38,500 | 51 | |||

| 01/04/2019 | 01/04/2029 | 300,000,000 | 455,102,000 | 451,024,000 | 300,000,000 | 37,000 | 60 | |||

| 02/05/2019 | 01/05/2029 | 350,000,000 | 401,830,000 | 396,599,500 | 350,000,000 | 75,500 | 69 | |||

| 03/06/2019 | 01/06/2029 | 350,000,000 | 274,486,500 | 270,874,000 | 270,874,000 | 200,000 | 0 | |||

| 01/07/2019 | 01/07/2029 | 350,000,000 | 275,404,500 | 271,430,500 | 271,430,500 | 200,000 | 0 | |||

| 01/08/2019 | 01/08/2029 | 350,000,000 | 93,046,000 | 90,947,500 | 90,947,500 | 200,000 | 0 | |||

| 02/09/2019 | 01/09/2029 | 350,000,000 | 77,481,500 | 76,651,000 | 76,651,000 | 200,000 | 0 | |||

| 01/10/2019 | 01/10/2029 | 250,000,000 | 58,152,000 | 56,966,000 | 56,966,000 | 200,000 | 0 | |||

Alternatives

So what are the alternatives to the SSB? I’ve compiled some alternatives in the table below, but the short answer here is that there is no easy alternative to the SSB.

| Instrument | 1 year yield | 10 year yield |

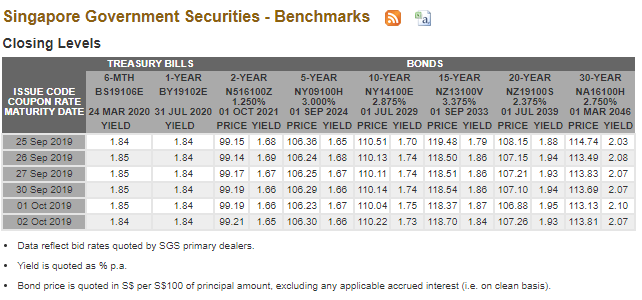

| Singapore Government Securities (SGS) | 1.84% | 1.73% |

| Fixed Deposit | 1.85 – 1.9% | NA – Continually roll over |

| Savings Accounts (eg. DBS Multiplier) | 2.3% | NA – Continually roll over |

| SSB | 1.62% | 1.74% |

Probably the closest replacement to the Singapore Savings Bond will be the SGS. The SGS has the added benefit of having the potential of capital gains, and having a 1 to 2 year yield that is higher than the Singapore Savings Bond.

Unfortunately though, there are a lot of problems with the SGS. The biggest problem is liquidity. The Singapore government only does issuances at certain times of the year, and the bonds come with specified durations. So perhaps there is an auction for a 10 year SGS next month. You can only buy the 10 year, and not a 1 year like you could with the SSB. And if you bought the 10 year and want to exit after 1 year, you’ll need to sell it on the SGX. You won’t know the price that the SGS will be trading at, and you won’t know for certain whether you’ll have sufficient liquidity to sell it quickly.

Fixed deposit on the other hand, typically has high minimum sums, and requires the money locked in for a certain period of time (eg. 12 month). If you try to exit earlier, you’re penalised by a lower interest rate on the money. And for fixed deposits, you can’t lock in a 10 year term, the max you can do is put it in a 2 year fixed deposit, and then come back again 2 years later to lock in whatever interest rate you can at the time (which could be lower).

High yield savings accounts like DBS Multiplier are probably the most attractive at the short end for now. Their 2.2% to 2.3% is very easily achievable for any working adult, and it’s a fair bit higher than everything else on the market right now. The problem of course, is that you must fulfil the requirements which can be a bit of an annoyance sometimes (eg. Salary credit, minimum spends on credit card etc), and you’re at the mercy of the rates changing at a moment’s notice.

Closing Thoughts

So the Singapore Savings Bond is a poor investment on the short end (because it’s below the market rate), and lacks the potential for capital gains even if interest rates continue to drop.

And what did I decide to do with the sum of money I had in the end? Yep, I decided to chuck it into Singapore Savings Bonds.

Because despite all it’s shortcomings, the Singapore Savings Bond does have some advantages. It is completely risk free, there is zero potential for loss of capital, I can get the money back with no more than 1 months’ notice, and it’s convenient as hell.

I didn’t like SGS because the capital gains goes both ways, and there is potential for capital loss of the rates go up, and it’s also just a big hassle to find the right bonds. I also didn’t like fixed deposit despite the higher rates because I needed to pop down to the bank to get it done, and I’m no longer able to fulfil the requirements for the high yield savings accounts now that I’m based overseas.

But the fact remains, the Singapore Savings Bond is no longer a no brainer place to dump your cash, like it was earlier this year. These days, you actually need to think about the duration you want to put your money in for, weigh the pros and cons against the competing instruments, and then decide which is most suitable for you.

In my case, the Singapore Savings Bond still made sense, but it may not for many of you out there. But then again, looking at the steady decline in the allotment numbers, I’m sure most of you already knew that 😉

Are SSBs still a good investment? Share your comments below!

Looking for a comprehensive guide to investing? Check out the FH Complete Guide to Investing for Singapore investors.

Support the site as a Patron and get market and stock watch updates. Big shoutout to all Patrons for their support!

Like the Financial Horse Facebook Page and join the Facebook Group (Singapore) or Facebook Group (China) to continue the discussion!

Great, informative article! Keep it up…

Cheers, glad you found it helpful!

I am using my SRS to buy SSB, to get higher interest

Why not use SRS to buy stocks instead? Since SRS funds are locked up long term anyway.

what stocks would you recommend to buy? I believe these have to be SGX listed stocks?

Well it’s always tough to recommend what stocks to buy without knowing your risk appetite and personal circumstances. If you want some stock ideas, you can take a look at some of my previous articles (https://financialhorse.com/top-5-singapore-stocks-2019/) or on Patron (https://www.patreon.com/financialhorse).

Cheers, hope this helps!

Since when did SSB ever reach 2.9% yield ?

Apologies, I meant that the 10th year SSB yields 2.9%. The 10 year SSB will yield an average 2.5% yield. Thanks for pointing this out, have corrected it. 🙂

Hi,

You can buy T-bills if which yields around 1.8% and have shorter duration.

You need to do more in-depth research on SGS.

SGS is not just limited to 10 years bond, maybe you want an apple to apple comparison however saving account does not have any maturity.

So well… ???

Thanks for the tip! My problem with SGS is that I may need to access the moment with short notice (1 month tops). With T-bills or SGS, not only does it take time to find the right bill that I need (right maturity), if I exit prematurely I’m also subject to liquidity and price constraints on the SGX. Hence my hesitation with SGS/Tbills.