It’s been a while since we’ve done a deep dive into a company.

So let’s remedy that today – with a classic Singaporean favourite: ST Engineering.

The manufacturer of our beloved SAR-21, Temasek linked, with a 3.8% dividend down to boot.

What more do you want in a stock?

Basics: What is ST Engineering?

ST Engineering’s business can be broken down into 4 big segments:

- Aerospace

- Electronics

- Land Systems

- Marine

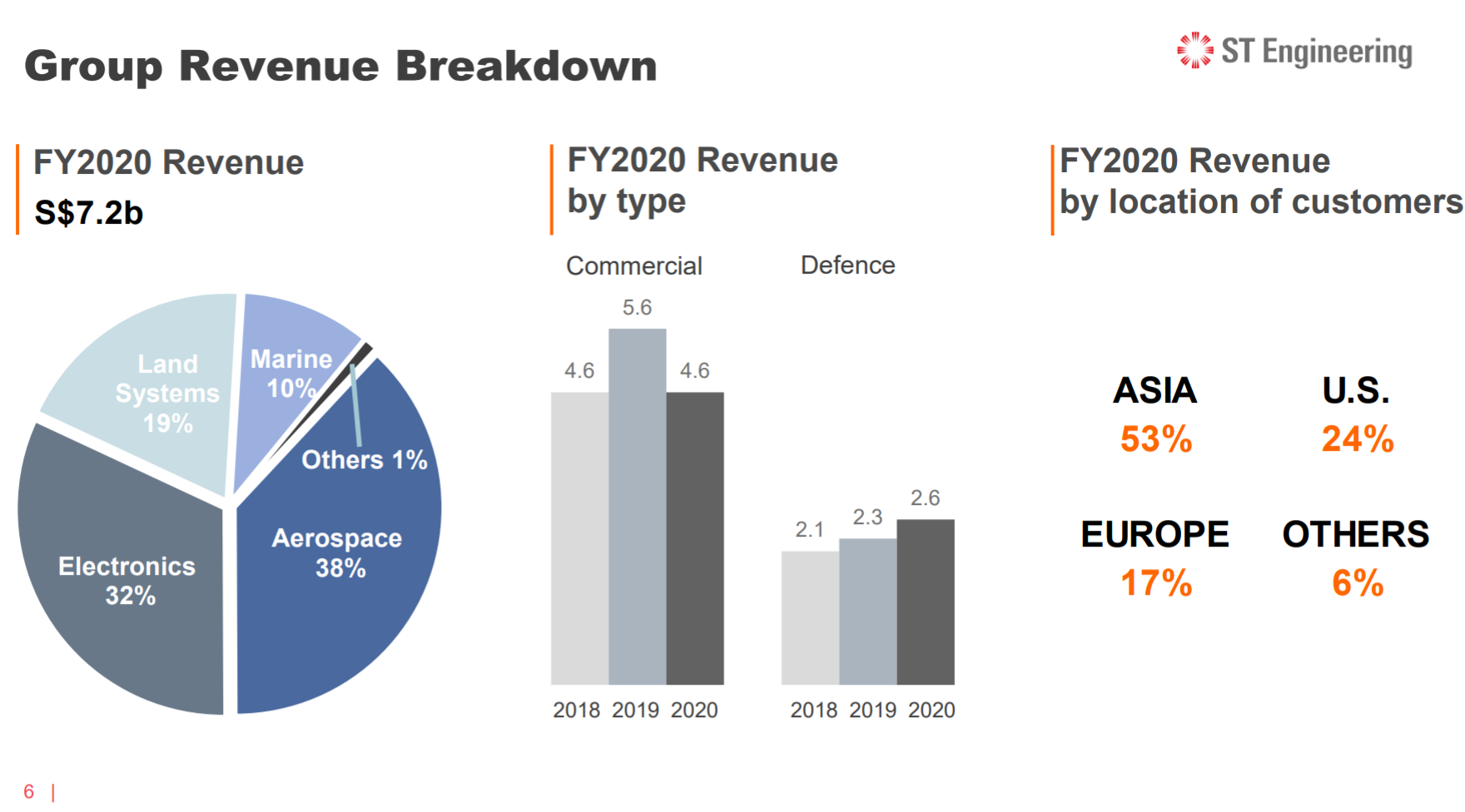

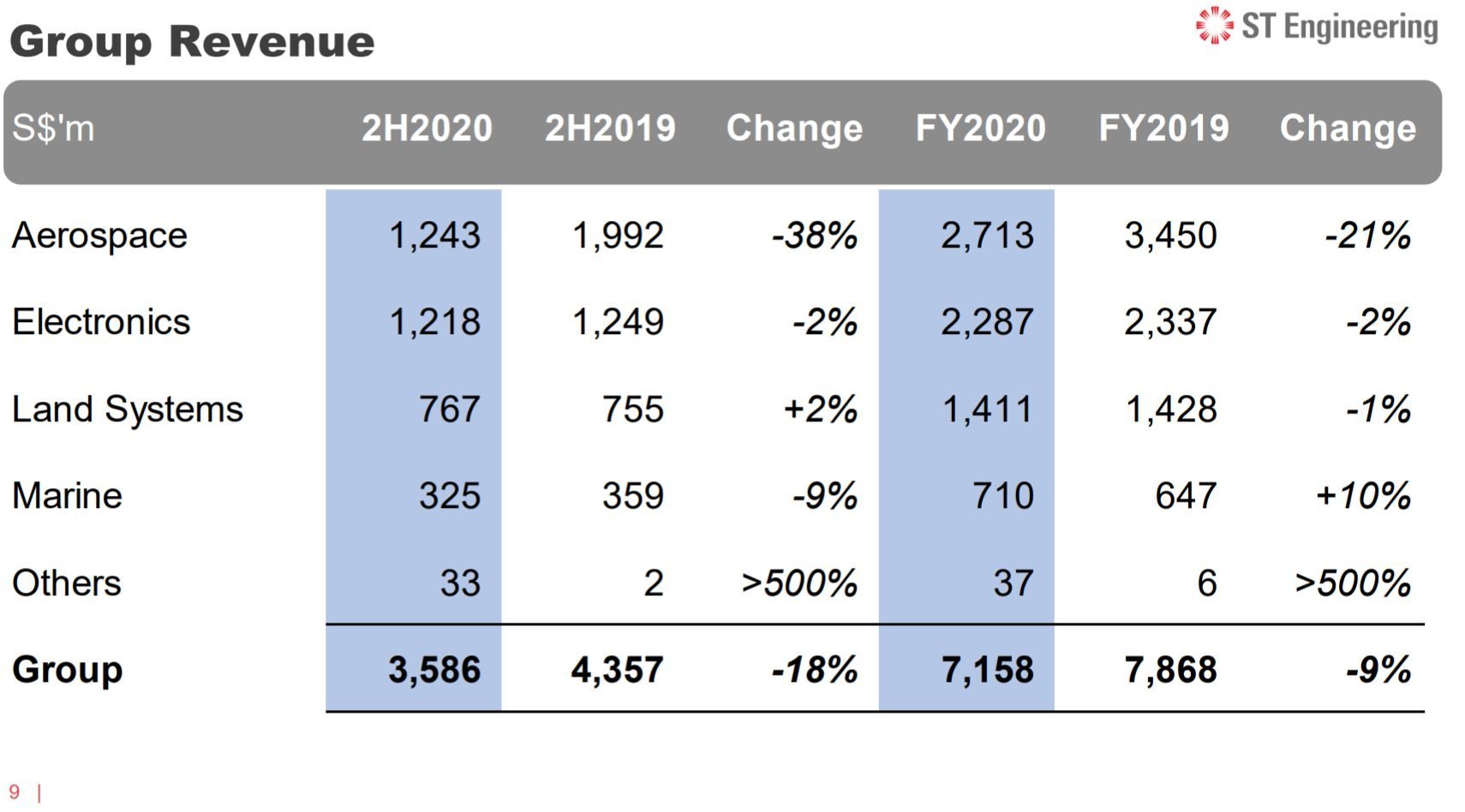

Aerospace is the largest contributor with 38% of FY 2020 revenue. This is the maintenance of aircraft, and sale of aircraft parts.

Electronics is the next largest contributor with 32%. They do project solutions – electrical projects like railways, Internet of Things, Smart City, Public Safety, Digital Health Platforms.

Land Systems is the defence element that every Singaporean male will know. SAR-21, armoured vehicles, most of the homemade weapons we use in the SAF are from ST Engineering. This contributes about 19% of revenue.

The lasts one is marine, which is shipbuilding, repair etc. It’s the smallest segment at 10% of revenue.

It’s also worth nothing that going forward, ST Engineering will no longer report using this structure.

Rather – the business will be reorganised into Commercial and Defence:

No strong views from me on this – I always like it when a company does pre-emptive restructuring. The world is changing very quickly, and businesses must change quickly to adapt.

Best to restructure early, than when profits are dropping.

BTW – we share commentary on financial markets every week, so do sign up for our mailing list, its absolutely free (goes out every Sunday).

Don’t forget to join our Telegram Channel and Instagram or (YouTube)!

[mc4wp_form id=”173″]

FY 2020 Results for ST Engineering

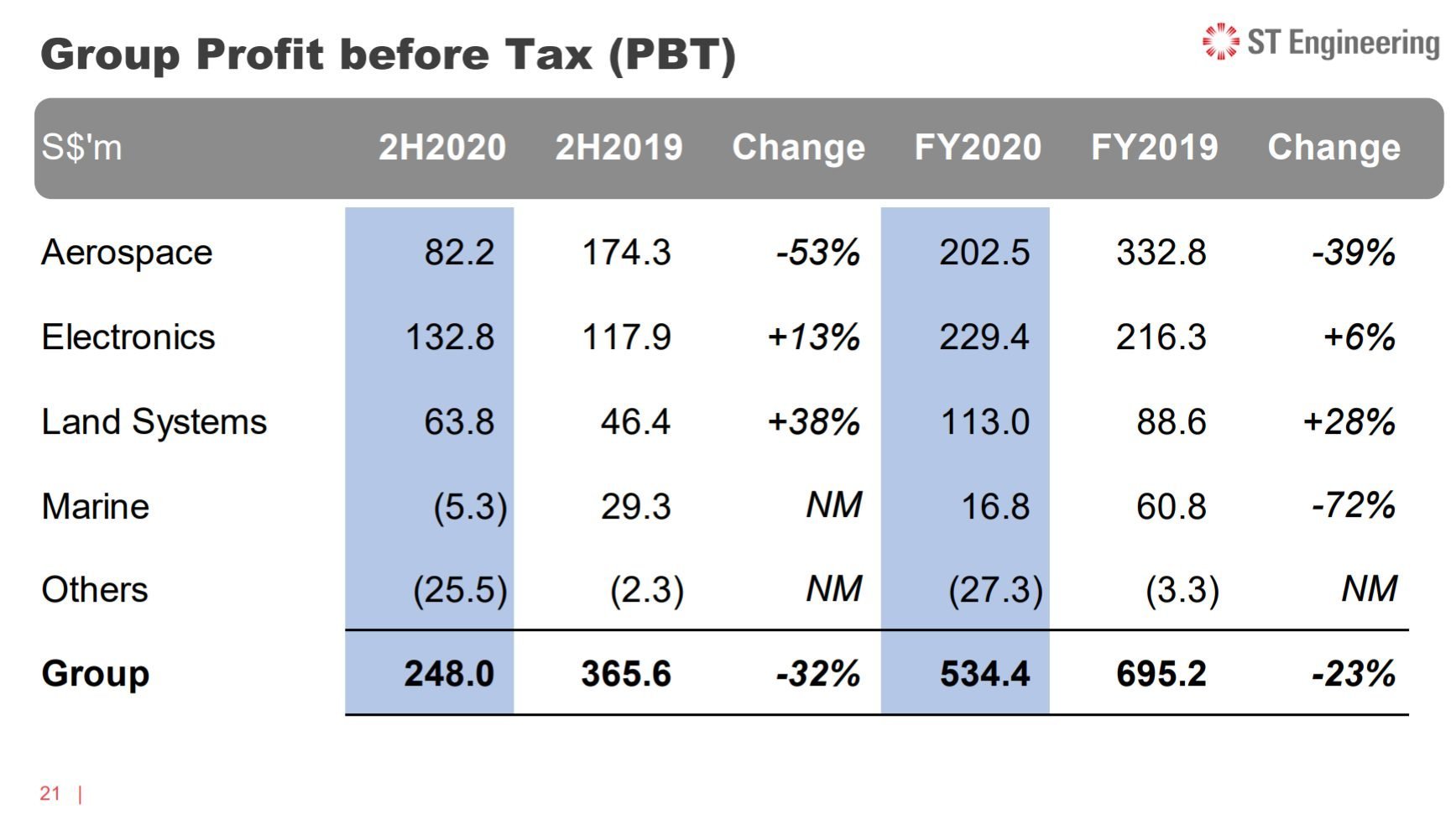

To sum it up in 1 sentence: Aerospace and Marine did poorly in 2020, while Electronics and Land (defence) proved very resilient.

That’s one of the benefits of having such a diverse business – when any one segment is not doing well, you usually can count on the other segments to save you.

And this was pretty much what happened in 2020, with Electronics and Land (Defence) saving the day.

Total revenue was down only 9% for FY2020, which all things considered, was a pretty good showing.

Most other companies would kill to go through COVID and take only a 9% hit to revenue.

Impact on each segment

There’s a very good writeup in the annual report that walks you through each business in 2020, so I’ve extracted it below.

The TLDR is:

- Aerospace was hit badly but the commercial aircraft business helped cushion the impact

- Electronics – Aviation and maritime were hit badly, but the defence, broadcast, and enterprise segments helped mitigate the impact to deliver overall strong results

- Land (Defence) was very resilient as you would expect. COVID barely had an impact on defence spending

In the Aerospace sector, the aviation industry was badly affected as travel restrictions were imposed around the world. Consequently, demand for aircraft maintenance, repair and overhaul (MRO) services dipped and engine nacelle manufacturing volume dropped. The silver lining was our passenger-tofreighter (PTF) conversion business. The grounding of passenger aircraft meant that their bellyhold cargo capacity was largely removed, while a spike in e-commerce created strong demand for all-cargo freighters. These factors, coupled with the availability of older passenger aircraft (many of which had been retired), meant that our PTF business received many enquiries as well as new orders.

At the Electronics sector, our Satellite Communications business in the aviation and maritime segments were similarly hit by COVID-19 as passenger aircraft and cruise ships ground to a halt, resulting in lower demand for our solutions. Nevertheless, having fully integrated our acquired businesses in Europe and the U.S., we added the defence, broadcast and enterprise broadband segments, which are more resilient, to our customer base and this diversity helped to mitigate the slowdown. The enlarged Satellite Communications group was also better positioned to capture opportunities emerging from new nongeosynchronous orbit satellite constellations including Low Earth Orbit (LEO) and Medium Earth Orbit (MEO) satellites. The pace of digitalisation hastened by the pandemic also led to higher demand for other business areas such as cybersecurity and secured digital solutions.

In contrast to the impact on our commercial business, our defence business provided much needed stability. Our Land Systems sector rolled out the production of the Hunter Armoured Fighting Vehicles, while our Marine business in the U.S. commenced design work on the Polar Security Cutter vessel. Meanwhile, our Singapore yard was focused on building Fast Patrol Boats for the Singapore Police Coast Guard.

Which is my favourite segment?

No prizes for guessing – I love the Defence business.

If ST Engineering spun off the Defence as a standalone listco, I would buy it in a heartbeat.

Defence is just good business. As we move away from a US centric world to a more multilateral world, I see defence as a great business to be in, with years of secular growth ahead of it.

The number of potential flashpoints around the world is growing (more Gazas, more South China Sea), and I expect more investments into defence going forward.

The problem though, is that ST Engineering comes with the aerospace, electronics, and marine business. Sidenote – the other big defence maker I really liked was Raytheon, but again it has merged with a civilian contractor and is no longer pure defence.

Other 3 segments – The electronics business is okay, it should pick up going forward as the cyclical recovery picks up pace.

Aerospace is not great, but the worst should be over for now. That said it will probably take until 2024 to fully recover to pre-COVID levels.

Marine is not a great business to be in, as we’ve seen from Sembcorp and Keppel. But it’s a small enough part of ST Engineering that it probably wouldn’t drag the business down.

Macro tailwinds – cyclical recovery + inflation

That said, there are some favourable macro tailwinds in play for the manufacturing business.

A lot of times as an investor, you just need to be in the right place at the right time, and get exposure to the right industry when there are secular tailwinds in play. It’s a rising tide lifts all boats scenario.

As shared in the mid-week post, I think we’re in the early to mid stages of this new economic cycle.

We’re starting on the tightening phase of this cycle, but there should still be years of economic growth that lie ahead.

This kind of early to mid stage cycle is very bullish for the engineering industry ST Engineering is in.

As the economic recovery picks up pace, more and more businesses will start investing in capex. If inflationary pressures make a comeback, cash flow heavy businesses like this could also potentially benefit.

So macro wise, there are some favourable tailwinds here.

Acquisition of Cubic Corporation

Interestingly, ST Engineering made a big buyout offer for US listed defence and transport technology firm Cubic Corporation.

If it had gone through, it would have been valued at about US$3 billion, almost 30% of ST Engineering’s current market cap.

The bid failed though, with Cubic accepting another proposal instead.

I’m personally not a big fan of big flashy M&A deals. I find that the buyer always overpays, and overpromises on “synergies”. In reality, that seldom comes to pass, and management is stuck with a business they overpaid for.

So I’m glad the takeover fell through, but it does indicate that ST Engineering has plenty of dry powder here, with ambitions to expand internationally.

Another big M&A deal is a real possibility going forwaard.

ST Engineering’s 3.8% Dividend… with 90% payout ratio!

Dividend is very strong at 3.8% yield.

By comparison, DBS has a 4% yield at today’s prices, while CapitaLand sits at 3.2%.

So ST Engineering’s dividend is almost at DBS’s level of yield, which is very high.

The problem though, is that payout ratio is very, very high at 90%.

This indicates that almost all of the profits being generated from the underlying business, is being used to fund the dividend.

90% payout ratio is nosebleed high, which puts the dividend at real risk of being cut if there’s some unexpected hit to the underlying business.

If you’re buying in for the dividend, it’s one to watch closely.

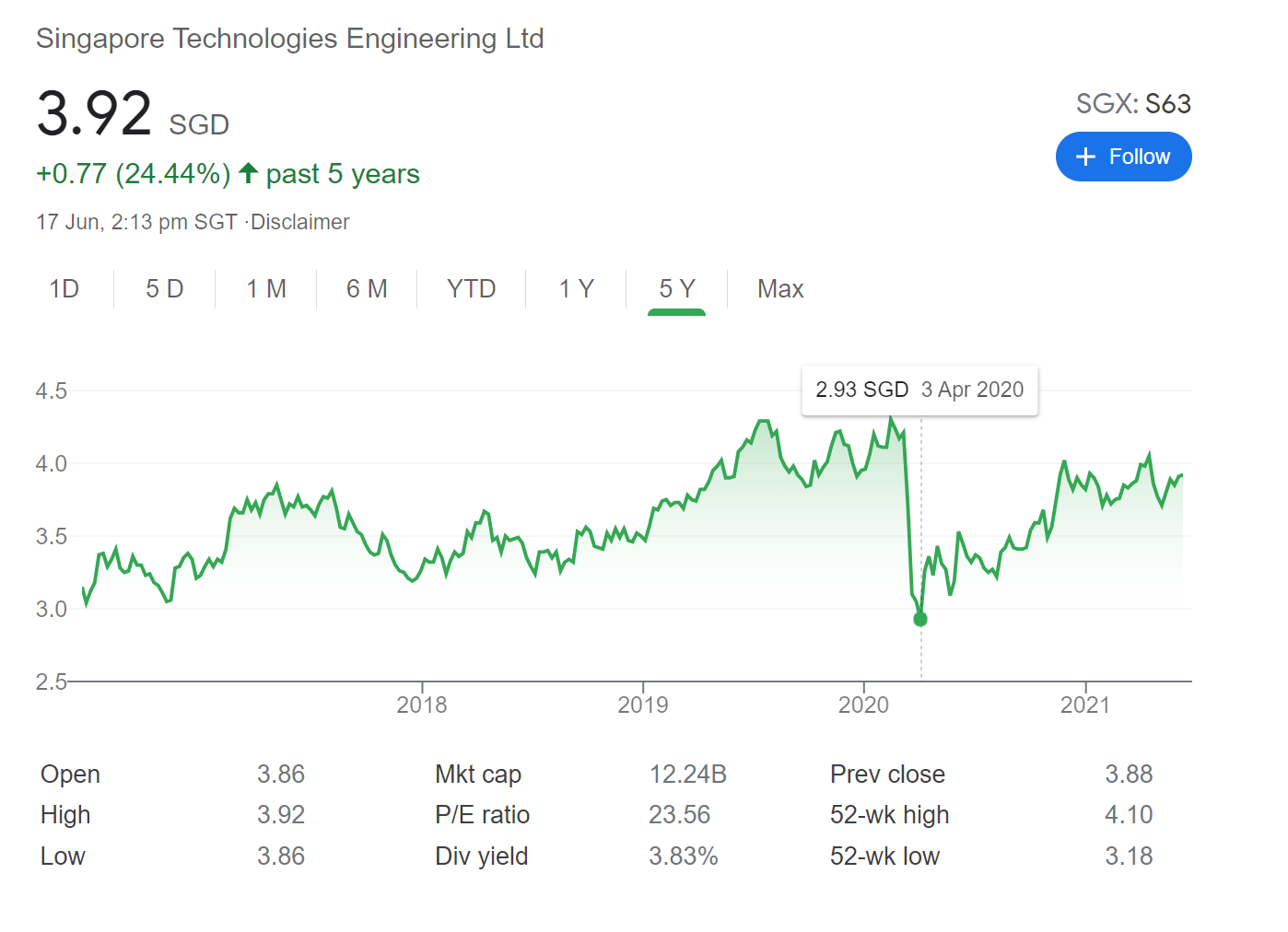

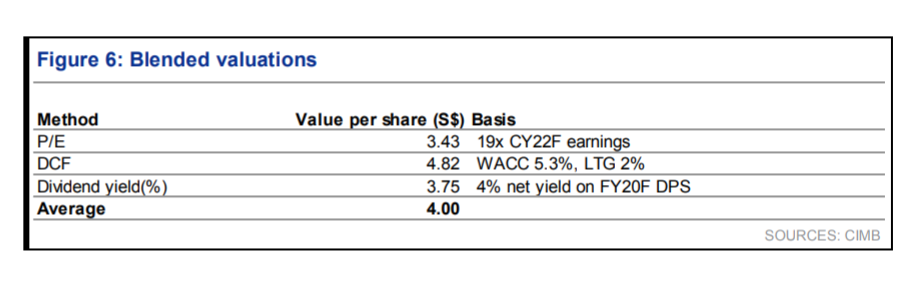

Valuations – ST Engineering

This is what DBS says about ST Engineering:

Maintain BUY with unchanged TP of S$4.20. We continue to like STE for its strong business diversity and continued resilience amid the pandemic, and strong balance sheet which will enable the group to capitalise on both organic and inorganic growth opportunities.

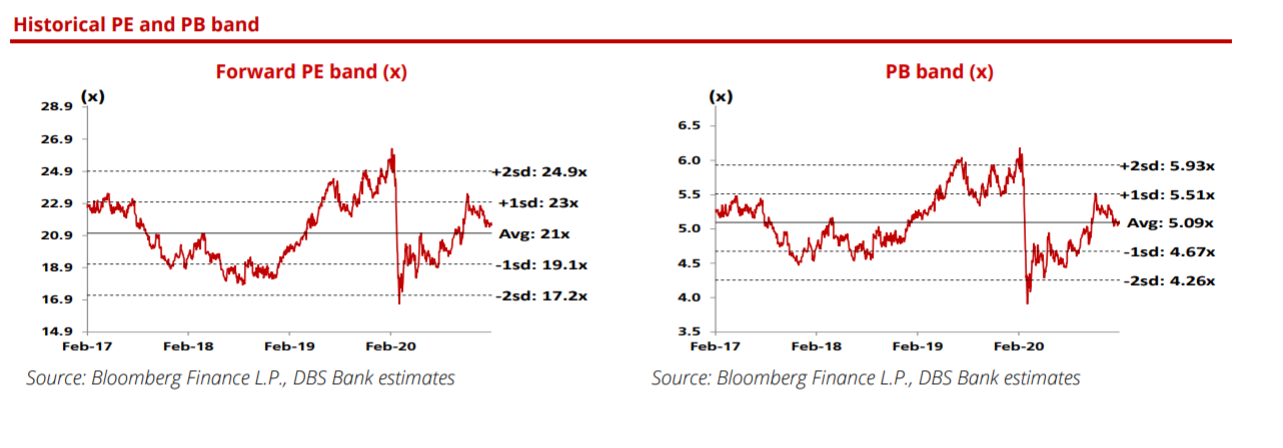

Current valuation of 21.7x (FY21F) P/E is consistent with mid-cycle valuations, but we believe STE should be priced at a higher multiple given that the group is entering the recovery phase of the cycle.

Furthermore, the stock also offers an attractive c.4.0% dividend yield, which is higher than most peers in the aerospace and defence sector.

UOB uses a mix of valuation methods to come up with a fair value of $4.00.

I’m generally with DBS on this one.

Current PE of about 23 seems fair to me, given we’re at the early to mid stages of this economic cycle.

Gun to my head, I think fair valuation should be about 21 – 23x FY21 PE.

This works out to a fair value of $3.62 – $3.97.

Today’s price of $3.92 puts it at the higher end of this range, but definitely well within fair value.

Shareholders of ST Engineering

As a GLC – Temasek is the largest shareholder of ST Engineering at 49%.

Would I buy ST Engineering?

I remember looking at ST Engineering very closely back in March 2020. I even remember when it dipped below $3, and I was deciding whether or not to buy.

In the end, the big aerospace exposure caused me worry, so I decided to go with the safer bank and REIT plays instead.

Probably should have loaded up in hindsight, but hey – hindsight is 20/20.

Frankly speaking, I think ST Engineering is quite a decent stock.

It’s definitely not a tech play with years of secular growth ahead of it, so don’t buy this expecting to 10x your money in the next decade.

They provide engineering services, with a profit margin of 7%. They repair planes, build electrical stuff, and build guns and boats.

That’s as old world as it gets.

What you do get though, is a very diversified engineering company, a solid 3.8% dividend yield, strong global cyclical recovery that lies ahead, and a potentially more inflationary world.

So for investors who are building a value/dividend barbell to supplement their growth barbell, I can really see ST Engineering as going into the value/dividend end.

Closing Thoughts

That said, I don’t have any immediate plans to buy ST Engineering.

I like the stock, but I see better uses for the money elsewhere now.

I still have a lot of money in the banks, REITs, and oil that forms the value end of my barbell.

If and when I start to take profit in those positions, I may consider allocating some money into ST Engineering.

But for now, I’m happy with how the value end of my barbell is performing, and I’m focussing more on the secular growth end of the barbell – with exposure to tech and China. You can check out my personal portfolio and stock watch on Patron.

That said, ST Engineering is definitely going to be on my watchlist. I don’t expect a dip because the underlying business is quite solid, but you never know sometimes.

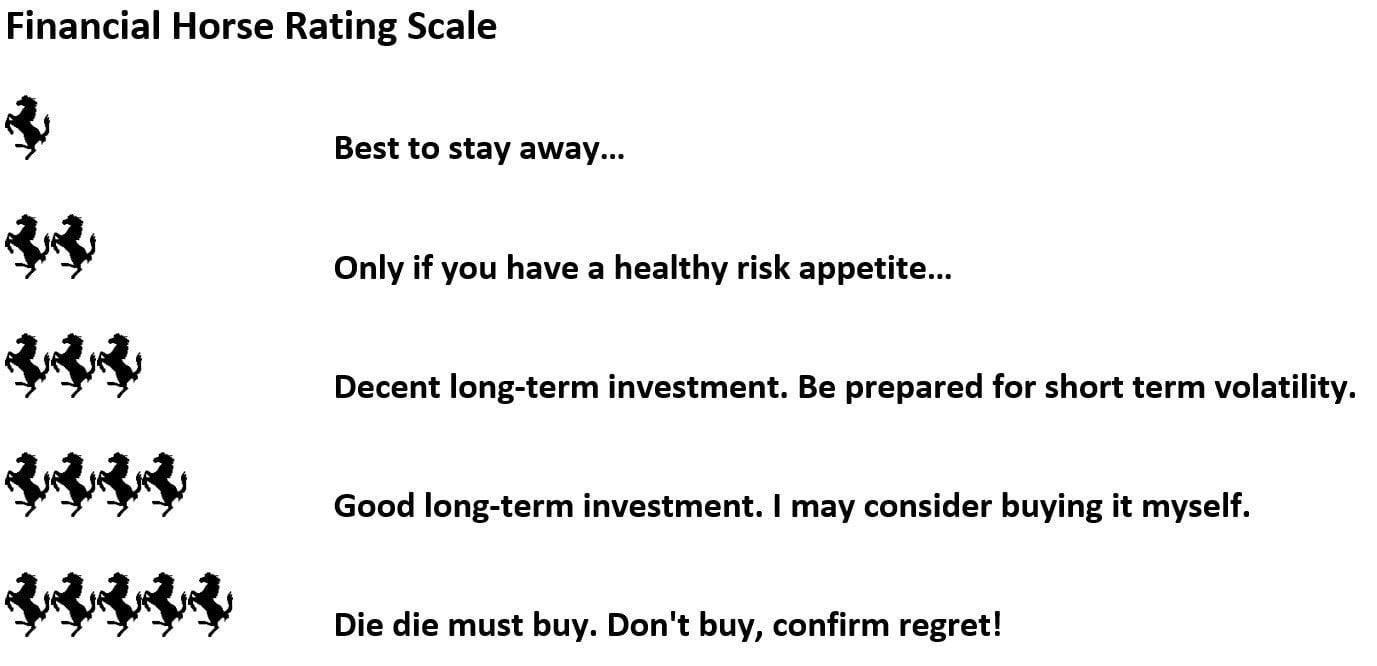

ST Engineering is a 4 Horse rating for me.

ST Engineering – Financial Horse Rating

As always, this article is written on 18 June 2021 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

Hi FH,

As usual thanks for sharing your thoughts. On the barbell approach with balancing defensive (SG banks and REIT ) and growth ( with bias on China & Tech ), what’s the allocation percentage like. It will obviously depends on multiple factors from age, expenses, marco etc, do you have any insights / links to guide a typical SG investors?

Thanks

Haha it’s an entire module in the FH Course: https://financialhorsecourse.thinkific.com/courses/complete-guide-to-investing-for-singapore-investors

I would say it really depends on your age + risk appetite. Start with 50-50, and then tilt towards defensive / risky from there, together with a read on global macro. I think even for my current portfolio I’m pretty close to 50-50 for growth vs dividend/value.