I’ve been getting quite a few questions on T-Bills recently.

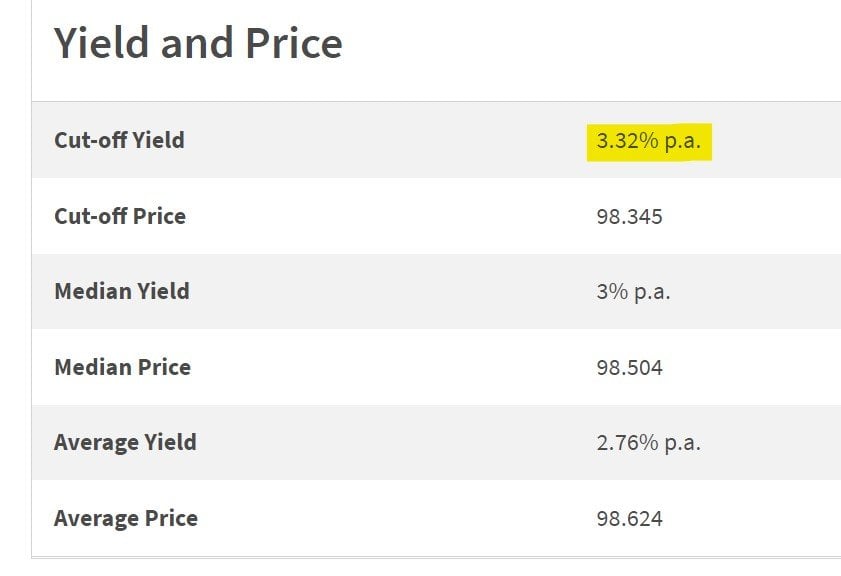

The latest T-Bills yield 3.32%, absolutely risk free.

And with the latest Fed rate hikes, the next round of T-Bills (auction on 29 Sept) will see even higher yields.

So… in times like this, are T-Bills the best place to park cash?

Better than Singapore Savings Bonds or Fixed Deposit?

FH… Why do you keep writing on T-Bills / Singapore Savings Bonds?

Now you may realise that I’ve been writing a lot on T-Bills, Singapore Savings Bonds, and Fixed Deposit recently.

The reason why – is that the macro climate is absolutely terrible.

With central banks in full-on inflation fighting mode, interest rates are marching up relentlessly.

And stocks / REITs have not fallen to the point where this is priced in (in my view).

Until they do, or until central banks change their policies, the best place to be in for a long term investor (who doesn’t want to go short), is probably cash.

And frankly, when you can get close to 4% risk free by being in cash (by end of the year), the opportunity cost of being in cash is as low as it’s even been.

Basics: What are T-Bills?

As defined by MAS:

Treasury bills (T-bills) are short-term Singapore Government Securities (SGS) issued at a discount to their face value. Investors receive the full face value at maturity. The Government issues 6-month and 1-year T-bills.

The key features of T-Bills are:

- Backed by the Singapore Government

- Minimum investment amount is $1000

- Duration of 6 months or 1 year

- Can be bought with cash, SRS or CPF

Advantage of T-Bills

In my mind, there are 3 big advantages of T-Bills:

- Risk Free

- No Limit to how much you can buy

- Good way to benefit from high short-term yields

1) Risk Free

T-Bills are issued by the Singapore government.

The credit risk you are taking on, is the risk of the Singapore government going bankrupt.

Nothing is risk free in this world, but T-Bills are as close to risk-free as it gets.

2) No Limit to how much T-Bills you can buy

This is probably the biggest advantage of T-Bills (vs Singapore Savings Bonds).

There is no limit to how much T-Bills you can buy.

The latest Singapore Savings Bonds only allocates $13,500 per month, capped at $200,000 total holdings per person.

If you have a couple hundred thousand in cash, Singapore Savings Bonds won’t work for you.

Whereas with T-Bills, this restriction is removed.

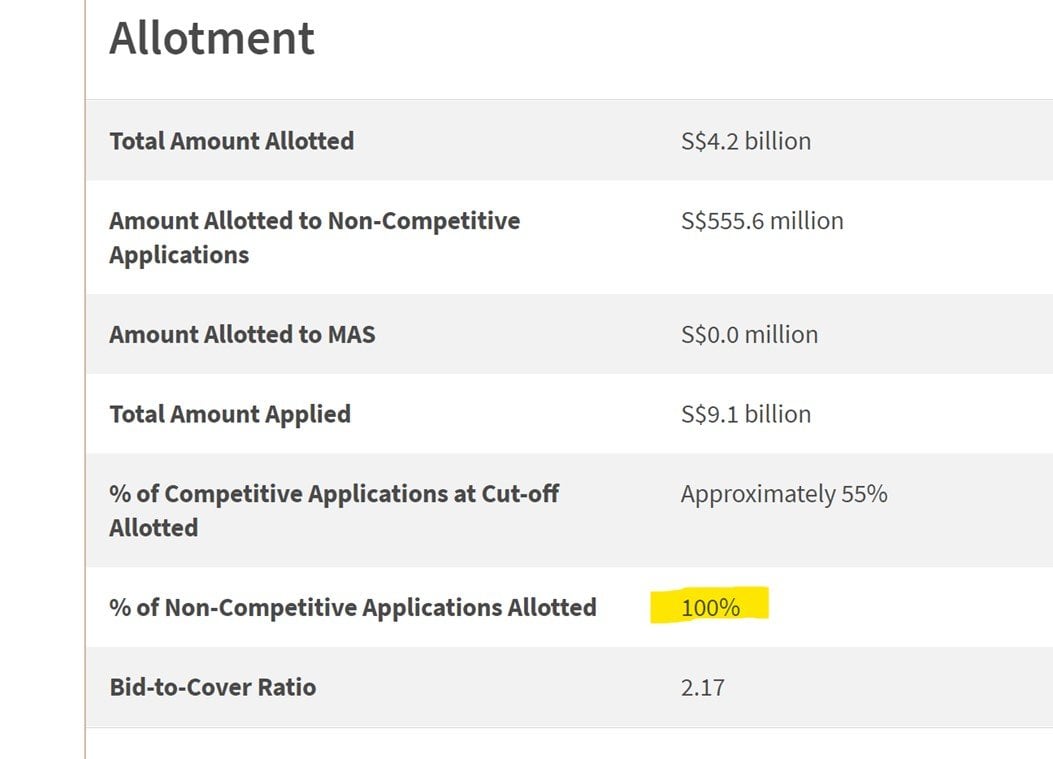

Here’s the latest allotment – 100% allotment for non-competitive applications.

You can literally apply a million in T-Bills and get full allocation.

3) Good way to benefit from high short-term yields

One peculiarity with the Singapore Savings Bond is that the short term yields cannot be higher than the long term yields.

I wrote an article here that sets out the full mechanics, but the long and short is that the yield on Singapore Savings Bonds cannot go down the longer you hold it. Ie. The 1 year interest rate, cannot be higher than the 5 year interest rate.

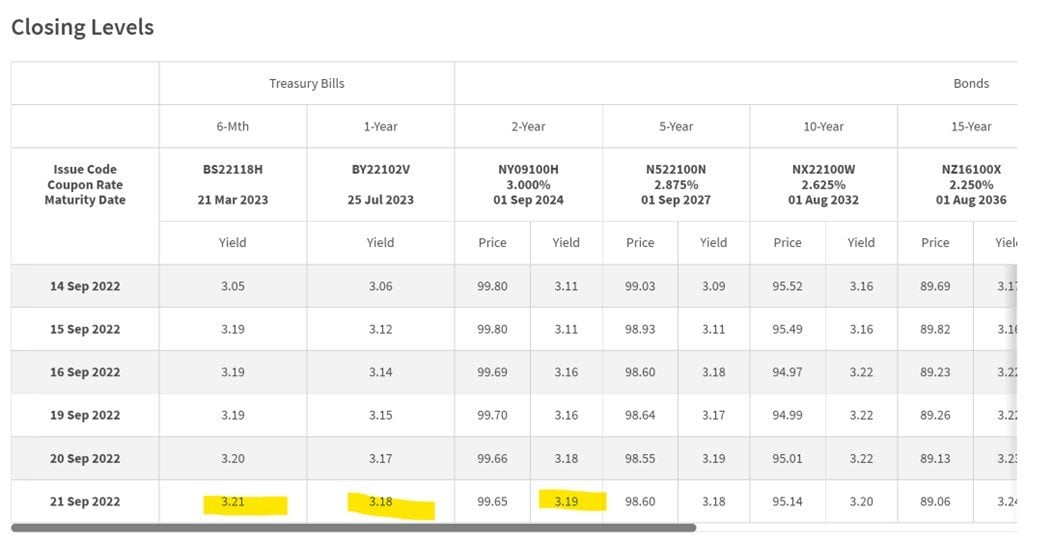

This is a big problem right now, when the short term, 6 – 12 month interest rates, are higher than the 2- 5 year interest rates:

With Singapore Savings Bonds, the curve is artificially smoothed out so that the interest rates will step up.

To put it simply – when the yield curve is inverted (like right now), Singapore Savings Bonds are not an effective instrument to benefit from the high short term interest rates (especially the 6 months – 12 months).

In situations like this, T-Bills are a better way to benefit from the high short term interest rates.

What about Fixed Deposit?

Fixed deposits can work too, but the interest rates for Fixed Deposits are determined by the bank, and they usually are not updated as quickly as T-Bills.

For example, the best Fixed Deposit right now pays about 2.85%.

Whereas the latest T-Bill pays 3.32%.

Are yields on T-Bills attractive in this rapidly rising interest rate climate?

Some of you have been asking – does it make sense to lock in T-Bills for 6 – 12 months, when interest rates are moving up this quickly?

Or should you just wait until Dec for the rate hikes to play out, before buying T-Bills at 4% yields then?

To answer this question requires a bit of maths, so bear with me.

The market is pricing in a 0.75%, 0.5%, 0.25% interest rate hike, to take us to 4.5% – 4.75% (Fed Fund Rate) by Jan 2023:

If this is right, then you can work backward to calculate the blended yield – about 3.8% – 4.0%.

Discount it a bit to maybe account for SGD strenght, and a rate of about 3.6% – 3.7% for a 6 month T-Bill today might make sense.

The latest round of T-Bills were issued at a 3.32% yield.

But since then, the Feds have hiked another 0.75%.

So if the next round of T-Bills yield ~3.6 – 3.7% (give or take), that would be close enough to what the market is pricing.

If you are savvy enough, you can get around the uncertainty by submitting a competitive bid, but more on this later.

Should you wait 1 – 2 months for interest rates to go up before buying?

That said, much of the thought process above probably only makes sense if you’re throwing around a couple million on the T-Bills.

For retail investors, the better question might be where is your money going to go if you’re not buying the T-Bills.

If you’re leaving it in your POSB account to earn a 0.25% interest, then fretting over the 3.3% vs 3.6% yield on the T-Bills seems like being penny wise pound foolish.

So yeah… look at the bigger picture here.

Disadvantage of T-Bills

That said, there are 2 big disadvantages of T-Bills worth talking about:

- Liquidity

- Does not benefit if yields go up (or down)

1) Liquidity

The biggest disadvantage – liquidity.

It’s not easy to get your money back before maturity when you’re buying T-Bills.

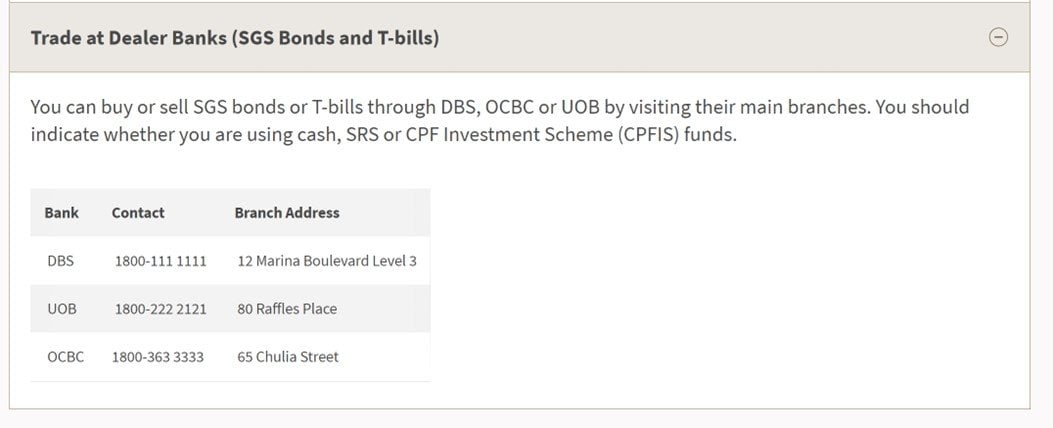

Unlike Singapore Government Securities which can be traded on the SGX, T-Bills are not listed.

If you want to sell a T-Bill, you need to get one of the 3 local banks (DBS, UOB, OCBC) to sell it for you.

And liquidity is not good.

If you’re a high net worth individual and looking to sell a couple million in T-Bills, okay maybe you can convince your private banker to help.

If you’re a retail investor selling smaller amounts – I mean it’s not impossible, but good luck.

Can you get your money back before maturity?

Long story short – if you’re a retail investor buying small-ish amounts of T-Bills, you may not be able to get your money back before maturity.

Your best bet might be to hold to maturity.

And 6 month / 12 months may not seem long when you’re buying the T-Bills.

But cash is like oxygen.

When you run out of cash, you really need the cash immediately.

My advice – don’t put all your liquid cash into T-Bills.

Have some cash set aside for daily spending or other emergency needs.

2) Does not benefit if yields go up (or down)

Yields on the T-Bills are locked in at issuance.

If you bought a 6 month T-Bill at 3.32%, and yields go up to 4%, you’re still only going to get 3.32%.

On the flip side, if 6 months later interest rates are cut to 0%, you’re going to be rolling over your T-Bills at 0%.

Where am I putting my cash?

A few of you have been asking, so I wanted to share how I am approaching cash management these days.

Personally for me in this climate – I would prioritise liquidity.

I would optimise my cash positions for liquidity first, and yield second.

I think in this climate, the chances of a liquidity event in the next 12 – 18 months is quite high, and I want to have immediate cash on hand to buy if that happens.

So the priority for me is:

- Minimum amount of cash in savings account

- Max out Singapore Savings Bond allocation each month

- X amount in T-Bills / Fixed Deposit

- Rest in savings account (depending on liquidity needs)

General Thought Process

I hold a minimum amount of cash in savings accounts, so they can be accessed at a moment’s notice.

This will be accounts like DBS Multiplier, Trust Bank (check out my Trust Bank review here – it’s worth signing up in my view) or Singlife.

The yield at 1-2% is definitely lower than T-Bills or Singapore Savings Bonds, but that’s the price I pay for the liquidity.

After that I will max out my monthly Singapore Savings Bond allocations.

Yields are lower than the market yields, but I think that’s an acceptable trade-off for the liquidity, and the option to lock in yields for up to 10 years.

Of the remainder, I am happy to keep X amount in T-Bills or Fixed Deposit for the higher yields.

T-Bills I would need to hold to maturity, and Fixed Deposit I can break early if I really want to (but there is a bit of hassle that comes with it).

And the rest I keep in a Savings Account, again for the liquidity.

But the exact proportion of each – only you can figure out for yourself. It will have to depend on your age, income status, and risk appetite.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

We also share great nuggets of wisdom on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

What about money market funds? Stashaway Simple, Endowus Cash Smart, Syfe Cash+ etc

Another option here is money market funds.

Think Stashaway Simple, Endowus Cash Smart, Syfe Cash+ etc.

Money Market Funds are a bit tricky, because the underlying cash is invested in a basket of short term securities.

If interest rates move up dramatically, capital losses are possible in the short term.

And in a true liquidity event, it’s not so clear whether you can pull all the funds out without capital loss.

Personally I’m probably staying away from money market funds for now.

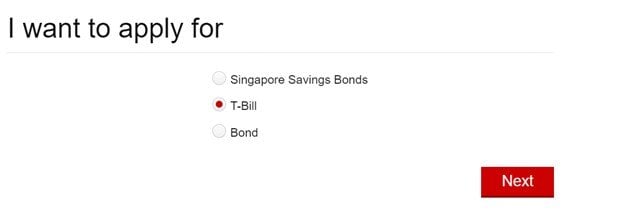

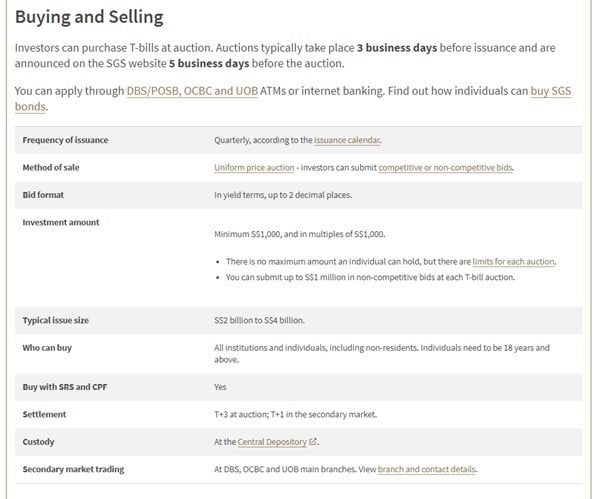

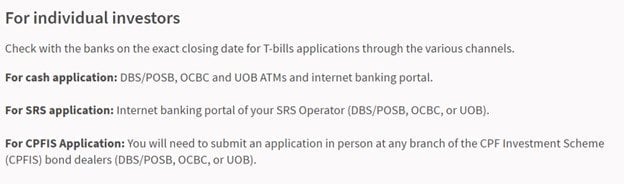

How to buy T-Bills?

You apply for T-Bills the same way as you apply for Singapore Savings Bonds – via any of the 3 local banks.

Here’s the application on DBS’s website, you just pick T-Bills instead of Singapore Savings Bonds.

Typical issue size of T-Bills is about $2 billion to $4 billion (vs Singapore Savings Bonds at $900 million).

So you’re way more likely to get full allocations using T-Bills.

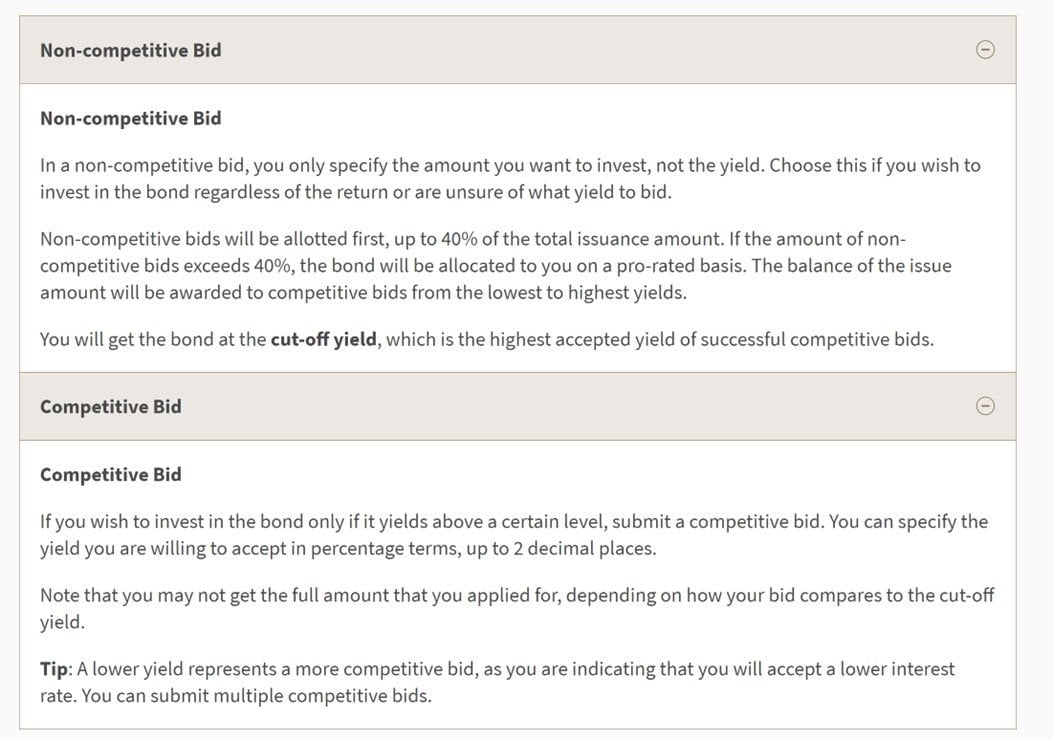

Competitive vs Non-Competitive Bid for T-Bills

One thing to note about T-Bills is that you have a choice between a competitive bid, and a non-competitive bid.

The difference is that:

- Non-Competitive Bid – you specify the amount you want to invest. Whatever the cut-off yield is, you will get T-Bills at that price.

- Competitive Bid – you will buy the T-Bill only if it is issued at a certain yield. For eg. You can enter 3.53%, and you will only buy the T-Bill if the cut-off yield is 3.53% or higher. You can submit as many competitive bids as you want.

General rule of thumb – if you don’t really know what you’re doing and just want to buy the T-Bills, use non-competitive bid.

If you’ve done your numbers right and only want to buy above a certain yield, use competitive bid.

When the auction results are out – the T-Bills will be issued to everyone at the cut-off yield, regardless of whether you applied for competitive or not.

FYI the next T-Bills auction is on 29 September 2022 for those who are interested.

Can you buy T-Bills with SRS or CPF?

Final note that you can buy T-Bills with SRS and CPF.

Now you may say it’s a no brainer to use CPFIS funds to buy T-Bills.

CPF pays 2.5%, while the latest T-Bills pay 3.32%, risk free.

Well … I don’t disagree.

Just don’t forget the liquidity issues above, if you’re using CPF-OA to pay your mortgage.

The other point to note is that you cannot buy T-Bills with CPFIS online. You need to actually go down to a physical branch of the 3 local banks and submit an application in person.

So I leave you to decide whether your time is worth that extra interest.

T-Bills do not pay a coupon (they are issued at a discount)

One peculiarity of T-Bills is that they do not pay a coupon.

Rather, they are issued at a discount to face value.

Let’s say you applied for $1,000 in T-Bills, at a 3% yield.

The T-Bills will be issued at a discount, which means you get $30 at point of issuance.

And on maturity, you get the $1,000 back.

Refinancing tool

With rapidly rising interest rates – it might pay off to look into refinancing if your loan is coming due.

There’s a fantastic tool by Property Guru.

Do give it a try if you’re close to refinancing.

It’s completely free – you just input your mortgage details, and the tool lets you know whether you’ll save money by refinancing.

If the answer is yes, they’ll give you recommendations on what loan to take.

If the answer is no, you can set up a reminder for the tool to remind you when its time to refinance.

I did the same for my own mortgages and found it pretty useful.

Do give it a try here.

As always, this article is written on 23 Sep 2022 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon. You can access my full personal portfolio to check out how I am positioned for the coming downturn too.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 100 USD in Apple Shares with Webull, a zero commission broker.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

You mentioned that the next round of Singapore Government Treasury Bills will be auctioned on 29 Sep 2022. When is the starting date to apply for this particular treasury bill and when is the closing date for application?

You can start applying now, closing is usually a day before.

Dear FH,

Kindly advise how & where I can buy T Bills.

Same as Singapore Savings Bonds – any of the 3 local banks internet banking website or ATM.

FH, how about doing analysis on using cpf oa to invest in t bills whether is really worthwhile considering compound interest and loss of interests in next months if money is withdrawn from cpf

Well if your CPF OA is paying 2.5%, and you buy T-Bills at 3.32%, you will make the 0.82% difference!

If one plans to buy US stocks, one can put money in Interactive Brokers(IB) and convert to USD. IB gives interest of 2.58% (BM – 0.5%) for USD now. If Fed raise interest rate in future, IB’s rate should increase accordingly.

At 2.58%, it is better than any bank deposit rate in Singapore. The downside is exchange rate risk. Nonetheless, if one plans to buy US stocks in future, the exchange rate risk is less of an issue.

Nice, appreciate the heads up!

This is what I’m currently doing, thanks for sharing. It applies only to Pro clients, not Lite tho. USDSGD has risen from 1.35 to 1.41, even with MAS tightening, so I’m happy with USD risk.

Alternatively, I am also thinking of selling OTM SPY puts. Either naked, to impose discipline on buying back into the market and profiting on high implied vol. Or hedged, perhaps through a bull put spread. It’s risky, but its the classic Warren Buffet value buying option strategy. Yield on it would be over 10% pa. While I’ve studied option strategies before for CFA, I have not implemented it in practice and still cautious. What are your ideas for profiting in a down market (other than cash equivalents)?

The other way to profit is to short, but you need careful risk management due to bear market rallies.

You could also long at the bottom of the trading range and trade the short term rallies, with a tight stop loss.

do you need to sign up or pay a fee to move from lite to pro IB?

i think you need a min of 100k usd to get that 2.58%. correct me if i am wrong.

If I can recall correctly, you get 2.58% if balance above 100k. Below 100k is a pro-rated rate. Eg. 50k receives half of 2.58%.

This lets you capitalise on any equity rebound. Trouble with T-bills is that you may miss any rebound.

Hihi – thanks for the write up. One question on the following comment:

“ Unlike Singapore Government Securities which can be traded on the SGX, T-Bills are not listed.”

Just wanted to ask. Do you find any liquidity on SGX on SGS? I struggle to find any. The prices are all over the place, elephant bid ask and very limited volume.

You are right – SGS liquidity on the SGX is very poor.

Much of the real trading is done OTC (over the counter) between institutionals directly.

If you’re Blackrock looking to offload millions in SGS, you probably can get liquidity. If you’re retail looking to sell a couple 10ks, it is much harder.

Dear FH,

1. If I submit a competitive bid at 3.5% for a $10k T-Bill, and the Cutoff Yield is higher at 3.6%, will I still be allocated with some of my bid? And at what yield, 3.5% (my applied yield) or 3.6% (the Cutoff Yield)?

2. If I submit a competitive bid at 3.5% for a $10k T-Bill, and the Cutoff Yield is lower at 3.4%, will I still be allocated with some of my bid? And at what yield, 3.5% (my applied yield) or 3.4% (the Cutoff Yield)?

3. Can I apply for a Competitive Bid and a Non-competitive Bid in the same auction? Thank you.

Rgds

Hi VS:

1. You will get at cutoff yield.

2. You will not get any.

3. Interesting qn, have not tried this one before. Don’t know the answer unfortunately.

Hi FH,

On point 3, what I understand is that this is possible.

Thanks! Appreciate the heads up! 🙂

For purchase of T bills using CPF OA account, must we go to the bank which we maintained our CPFIS account or any bank will do? Must go down personally to submit the form or someone can submit on our behalf?

Hm good question, I’ve not tried this out before unfortunately. Suggest to check with your bank directly.

Hi FH, may I know when is the next round of Singapore Savings bonds application date ?? As I think the next round of SSB rates would be more attractive. Thanks.

Rates are just going up parabolic now …

I do somehow agree with you SSB is more liquid can be withdrawn on shorter notice than T-bills, and has more certainty of the lock in rates when one applies.

You can check the issuance calendar here 🙂 https://www.mas.gov.sg/bonds-and-bills/auctions-and-issuance-calendar

In any case, will be releasing more articles on SSB and T-Bills, as the rising interest rates continue to play out! 🙂

Dear FH,

Thanks for the very informative article.

Can I ask if it make sense to place a big portion of CPF OA into T-bill since it is likely to be higher than 2.5% yield?

On maturity of T-bill, can I confirm that the amount & yield be channelled back to COF OA?

Thanks in advance.

Yes, it’s pretty much a risk-free carry trade.

On maturity, the moneys will go back into your CPF.

Hi FH,

When you apply for a Non-Competitive T-Bill on POSB’s internet banking website, there is this flwg warning:-

“Non-competitive bid may result in a negative bid yield depending on the market condition at the time of this application.”

What does this mean?

1. Can the Cutoff Yield go negative? Has it happened before?

2. Will my application be rejected if that happens? Tks.

Rgds

Well never say never, but I think the odds of this are low.

To answer your question:

1. Negative yield means that you are basically paying money to the government for the privilege of lending money to them. For eg. you subscribe to $1000 of T-Bills at a -1% interest rate, so you only get $990 back. This was a concern when interest rates were stuck at the zero bound, but with interest rates where they are now, it does look like a remote possibility.

2. Has not happened before in my knowledge.

3. No, in the unlikely event that it happens, you will still get T-Bills at the cut-off price if you apply non-competitive. If you are really worried about this you can use a competitive bid.

Hi FH,

May I know how do you decide on the 6-month or 12-month T Bills in this rising interest rates environment?

Thank you.

It depends on many things – your liquidity needs, the yields on 6 month vs 12 month, your outlook on rates the next 12 months etc…

For me, I would probably go with 6 months. More liquidity, and yields are not that much different from 12 month.

Thank you.

You mentioned:

On the flip side, if 6 months later interest rates are cut to 0%, you’re going to be rolling over your T-Bills at 0%.

What does this mean? Will the yield of my T-Bills go to 0% even after I have purchased them at 3.3% when the interest rates are cut to 0%?

Sorry just to clarify. I meant that if you buy a 6 month T-Bill, it will mature in 6 months.

Which means that if you buy new T-Bills with the money you get back 6 months later, you are subject to interest rates prevailing at the time. If interest rates go up to 4% great. If interest rates go down to 1% then tough luck.