The latest T-Bills yield 3.77%.

While CPF-OA yields 2.5% (after the first $20,000).

T-Bills are backed by the Singapore government.

So … Should one buy T-Bills with CPF-OA money, and earn the extra 1.27% interest, risk free?

There’s a bit of nuance to this question, and it’s not as straightforward as it seems.

So I wanted to share views in this article.

Basics: What are Treasury Bills (T-Bills)?

Treasury bills (T-bills) are short-term Singapore Government Securities (SGS), of 6 or 12 month duration.

There are 3 big advantages of T-Bills:

- Risk Free

- High short term interest rates

- Can be bought with CPF-OA (and SRS / Cash)

Risk Free

Backed by the Singapore government, this is as close to risk free as it gets

High short term interest rates

The latest Singapore Savings Bonds yields 3.08% for one year, and the latest Fixed Deposit yields 3.33% for one year.

While T-Bills yield 3.77% for 6 months, and 3.72% for 12 months.

In rapidly rising interest rate climates (like right now), very few products out there will be able to match the interest rates on T-Bills.

Can be bought with CPF-OA (and SRS / Cash)

And probably the biggest advantage.

You cannot use CPF-OA funds to buy Singapore Savings Bonds or Fixed Deposit.

But you can use them to buy T-Bills.

Should you buy 3.77% yielding T-Bills with 2.5% yielding CPF-OA?

Any amount in your CPF-OA above $20,000 earns 2.5% interest.

So… if you don’t need to use the CPF-OA funds.

Should you put it into 3.77% T-Bills and earn the 1.27% spread risk free?

3 big questions in my mind:

- How much CPF-OA interest do you lose by doing this?

- Should you buy 6 month or 12 month T-Bills?

- Will CPF-OA interest rates go up?

Question 1 – How much Interest CPF-OA Interest do you lose by buying T-Bills?

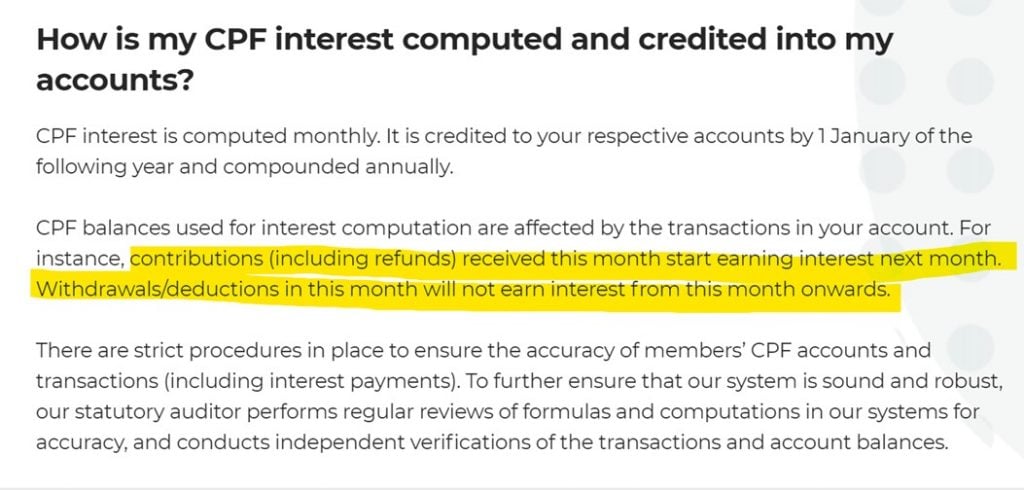

There’s a funky feature about how CPF interest is calculated:

Interest is paid on the lowest balance of your CPF balance that month.

You can see the highlighted portions in the screenshot below.

What this means, in simple English, is that when you use CPF-OA money to buy T-Bills:

- You will not get any CPF interest in the month that you apply for the T-Bills

- You will not get any CPF interest in the month that you get the money back from the T-Bills

For example – If you apply for $100,000 worth of T-Bills on 10 November 2022, maturing on 10 May 2023.

This means you don’t get CPF-OA interest for the $100,000 for the months of November 2022 and May 2023.

BUT – you will get the T-Bills interest from 10 November onwards, up till 10 May.

So effectively, you lose 1 month CPF-OA interest if you buy T-Bills with CPF-OA.

This means the T-Bills interest must be high enough to compensate you for the loss of the 1 month CPF-OA interest.

How high must T-Bill’s interest be for this to be worth it?

CPF-OA’s interest rate of 2.5% divided by 12 is about 0.208%.

Which means doing this trick loses you about 0.208% worth of CPF-OA interest, and you need a higher yield on the T-Bills of about 0.208% per annum.

So anything above 2.71% per annum, and you probably break even (2.92% if you buy the 6 month T-Bills and don’t roll over).

With T-Bills at 3.77% now, we are well above the threshold rate.

How much do you make by doing this, at current T-Bills interest rates?

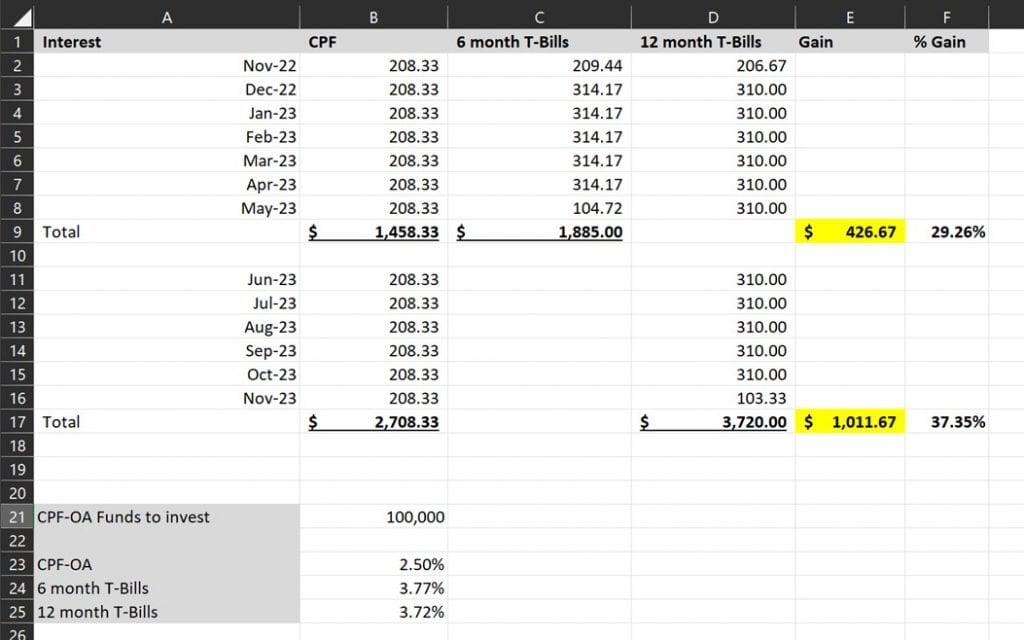

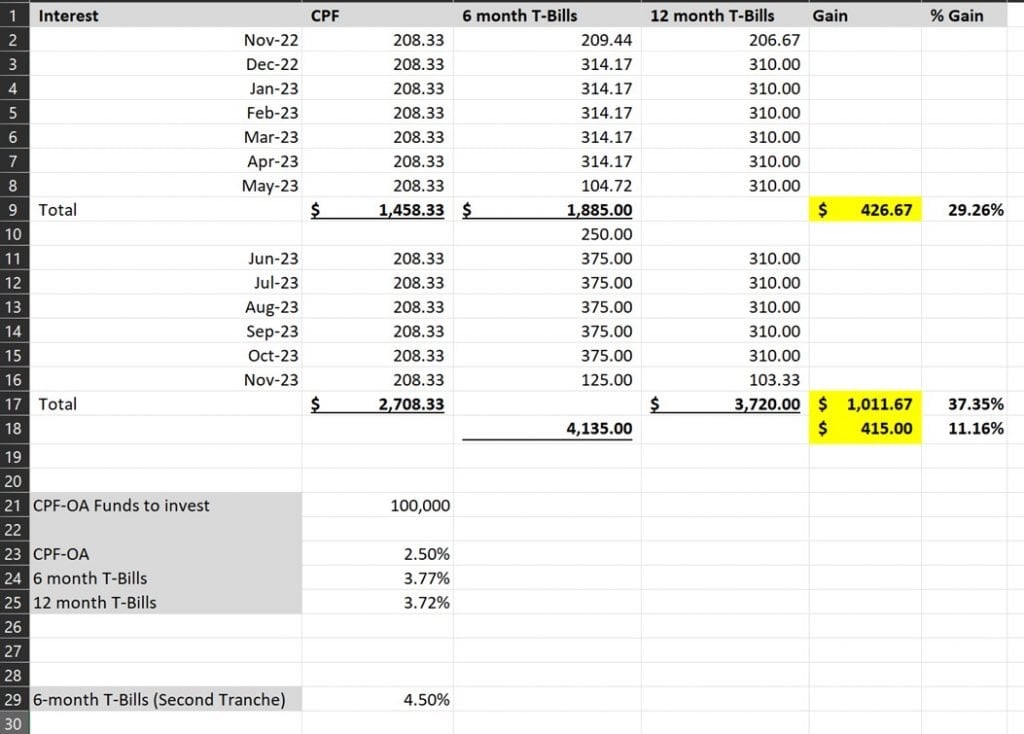

I computed the numbers above for easy reference.

If you’re buying $100,000 worth of 6-month T-Bills, at the latest 3.77% interest rate, you will make $426.67 extra by doing this (for 6 months).

This is a 29% increase in the interest earned.

If you’re buying $100,000 worth of 12-month T-Bills, at the latest 3.72% interest rate, you will make $1011.67 extra by doing this (for 12 months).

Which is a 37.35% increase in the interest earned.

Not too shabby indeed.

The more CPF-OA you have, the more you make.

What about compounding?

Now for simplicity’s sake, I didn’t include the effects of compounding in my numbers above.

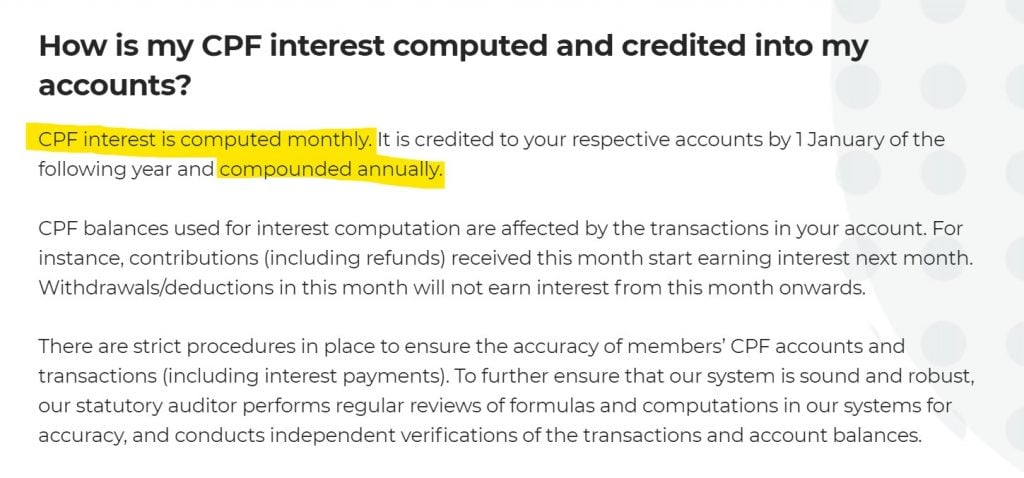

CPF interest is calculated monthly (but only credited annually).

Whereas with T-Bills, because they are issued at a discount, you actually get the full “interest” upfront.

Viewed this way T-Bills actually have superior compounding effect, compared to CPF-OA, because you get to compound the interest immediately.

Question 2 – Should you buy 6 month or 12 month T-Bills with CPF-OA?

The answer to this question depends on where the 6 month T-Bill interest rates will be in 6 months (whether they go up or down).

It also depends whether you can roll over the expiring T-Bills into new T-Bills the same calendar month (to avoid losing an extra month of CPF-OA interest).

Let’s start with the first question.

How high will T-Bills interest rates go?

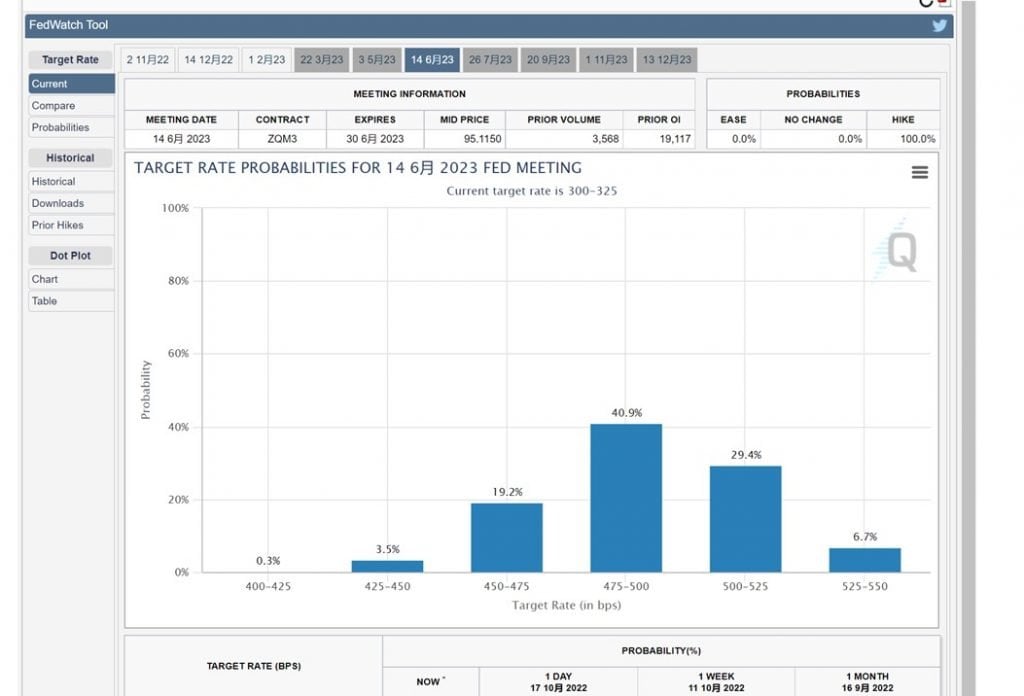

Latest Futures markets are pricing in a peak US Fed Funds Rate of about 4.75 – 5.25%, by mid 2023.

You can see the US 1 and 2 year Treasuries have already baked this in, as they trade at about 4.5% now.

Let’s be conservative and assume SGD interest rates peak slightly below US interest rates.

I think realistically, you could see T-Bills trade anywhere from 4.25% – 5.0% by end of this cycle.

But of course, all of this are just forecasts, and many things can go wrong.

If the global economy starts to collapse, or we get systemic risk, interest rate may get cut quite quickly.

Will you be able to roll over the expiring T-Bills into new T-Bills the same calendar month (to avoid losing an extra month of CPF-OA interest)?

Because of this, it actually makes sense to apply for T-Bills at the start of the month.

This way, they will mature on the start of the month – giving you time to roll over the money into new T-Bills, without spilling over into the next calendar month and losing another month of CPF-OA interest.

So… buy 6 month or 12-month T-Bills?

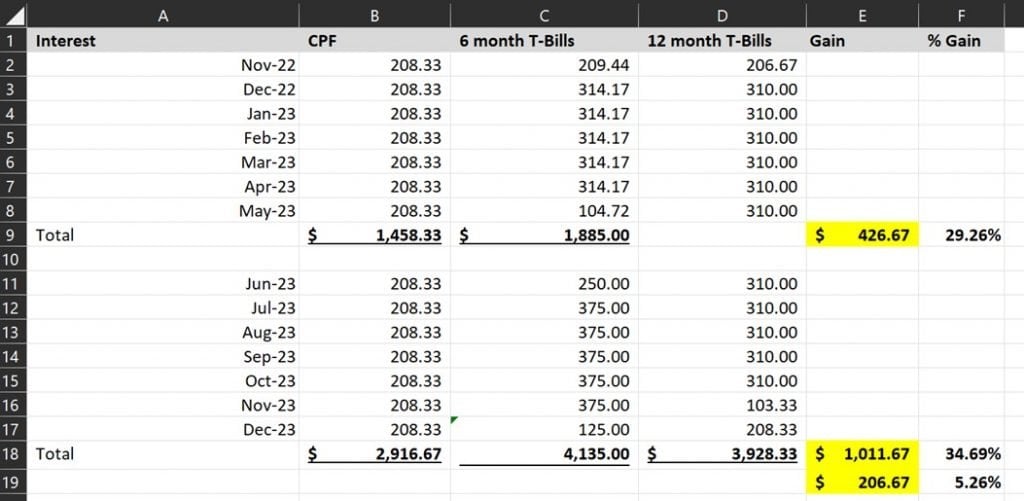

Here are the numbers, assuming that:

- 6-month T-Bills will be 4.5% in 6 months

- You can roll over your T-Bills without spilling over into the next calendar month (and losing another month of CPF-OA interest)

Winner: Buying 6 month T-Bills makes an extra $415, which is an 11% increase in interest.

What if you cannot get the timing and need to spill over into the following month (losing an extra month of CPF-OA interest)?

Winner: Buying 6 month T-Bills makes an extra $206.67, which is a 5% increase in interest.

So as you can see, the key to this question is where the T-Bill interest rates will be in 6 months time.

If you think interest rates will go up and stay up, buy the 6 month T-Bills.

If you think interest rates will go down or stay at current levels, buy the 12 month T-Bills.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Question 3 – What if CPF-OA Interest Rates go up?

Now the other big consideration – is whether CPF-OA interest rates will go up.

If you buy T-Bills with CPF-OA, the interest rate you get is locked in for duration.

You can lose money if CPF-OA Interest Rates go up

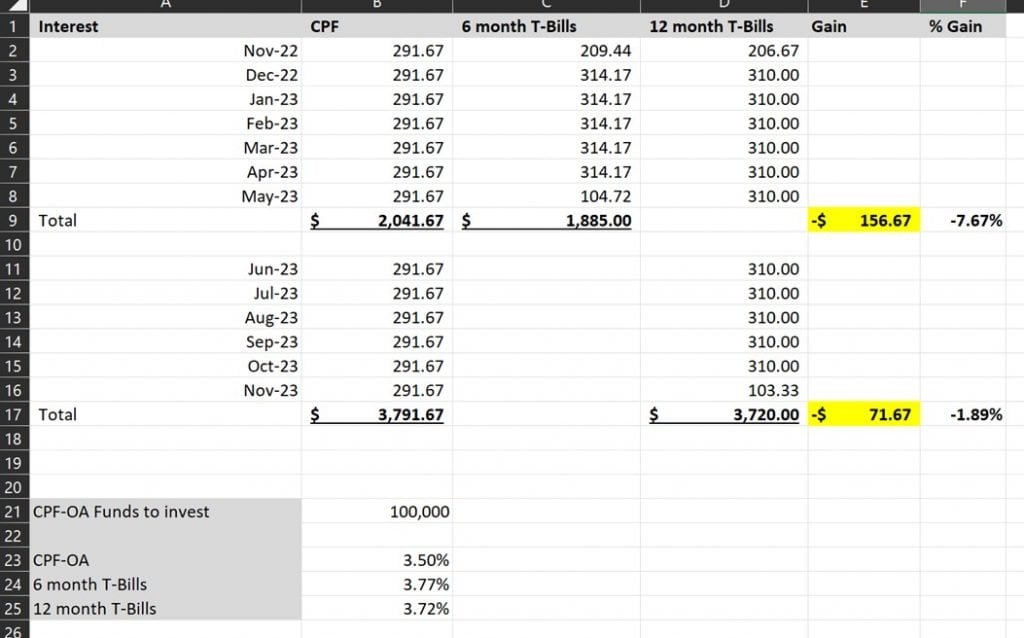

So imagine if the CPF-OA interest rates are increased to 3.5% (or higher).

After factoring in the 1 month lost CPF-OA interest, you might actually be losing money.

Here are the numbers, assuming CPF-OA goes up to 3.5%.

You actually lose money due to the 1 month lost CPF interest.

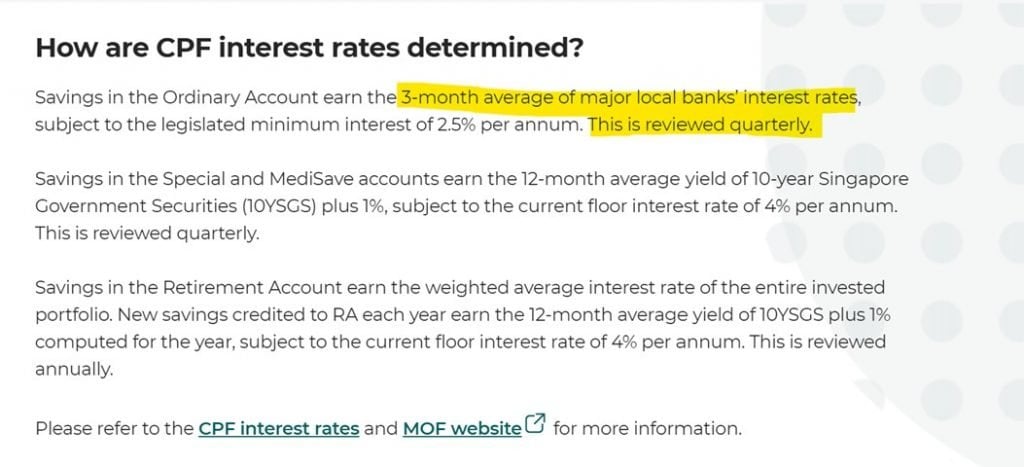

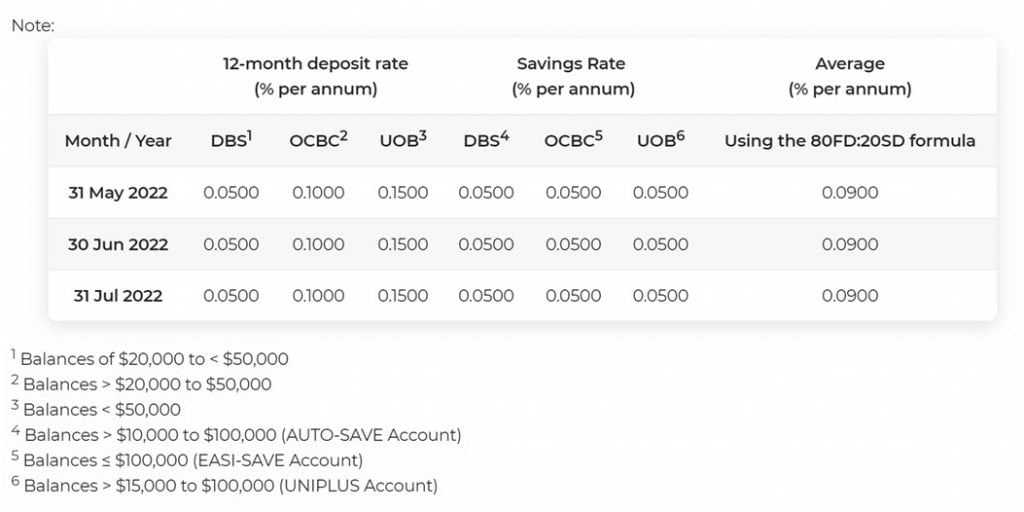

How are CPF-OA interest rates calculated?

From CPFB’s website, CPF-OA is pegged to the lower of:

- 3-month average of the major local banks’ interest rates

- Legislated minimum interest of 2.5%

As of now, the 3 month average of the 3 local banks interest rates is 0.09%.

Even if it moves, I don’t see it going above 2.5%

Which leaves (2) – the legislated minimum interest rates.

Will / Should CPF-OA legislated minimum interest rates go up?

Most of you will have your views on whether CPF-OA interest rates should or should not go up.

The complexity is that HDB loan rates are pegged to 0.1% above CPF-OA interest rates.

So if CPF-OA rates go up, so do HDB loan rates.

Which makes a sensitive political issue.

Now this is a finance blog, and this horse does not want to wade into any political debates.

I’m in the business of predicting what governments will do, not what governments should do.

Gun to my head, I think that if interest rates stay elevated for a prolonged period, CPF-OA rates will probably move up eventually.

But maybe not in the immediate future.

But like I said, this is not a topic I have a strong view on, and I leave it to you to decide if CPF-OA interest rates will go up.

FH… that’s all very technical, can you summarise?

To summarise:

1. As long as T-Bills pay more than 2.71% per annum, you will make money buying T-Bills with CPF-OA (2.92% if you buy the 6 month T-Bills and don’t roll over).

2. However, this is assuming CPF-OA interest rates do not go up, and I leave it to you to make a judgment call on this

3. Whether to apply for 6 month or 12 month T-Bills will depend on where interest rates are in 6 months. If you think interest rates will go up and stay up, use 6 months. If you think interest rates will go down, use 12 months.

4. If you plan to roll the expiring T-Bills over into new T-Bills, it is best to apply for T-Bills at the start of the calendar month, to avoid losing an extra month of CPF-OA interest.

Do you need to use the CPF-OA funds?

Now of course, this is assuming you don’t need to use the CPF-OA funds.

A big drawback of T-Bills is that for retail investors, it is not easy to sell them before maturity.

Unlike SGS which are listed on the SGX, T-Bills are not listed, and can only be sold over the counter (OTC) via the 3 local banks.

So if you need the CPF-OA funds to pay your mortgage, my strong suggestion is to not bother doing this.

T-Bill interest rates are not known in advance

Do note that T-Bill interest rates are not known in advance, as they are determined at auction.

If you are worried, you can ask the bank to put in a competitive bid for you, so you only get the T-Bills above your desired level of interest.

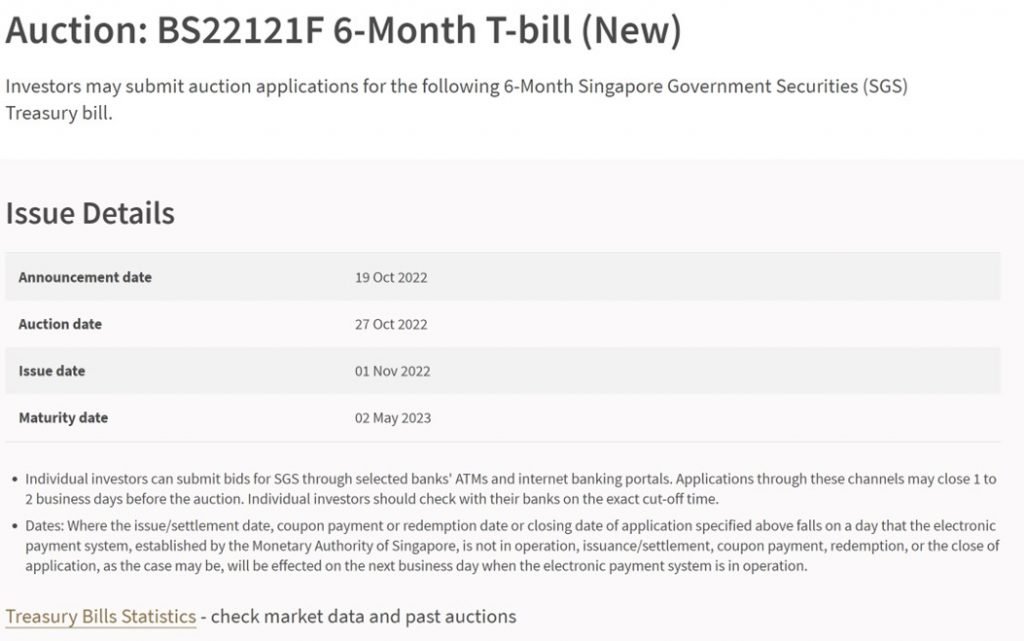

When is the next T-Bill Auction?

Next T-Bills auction is on 27 October, you need to apply at least 1 Business Day before.

Eligibility to use CPF-OA Funds to buy T-Bills

Before you can use your CPFIS funds, you need to have a minimum sum of $20,000 in your Ordinary Account.

And you must be:

- at least 18 years old;

- are not an undischarged bankrupt;

- have more than $20,000 in your OA; and/or

- have more than $40,000 in your SA; and

- have completed the CPFIS Self-Awareness Questionnaire (SAQ)

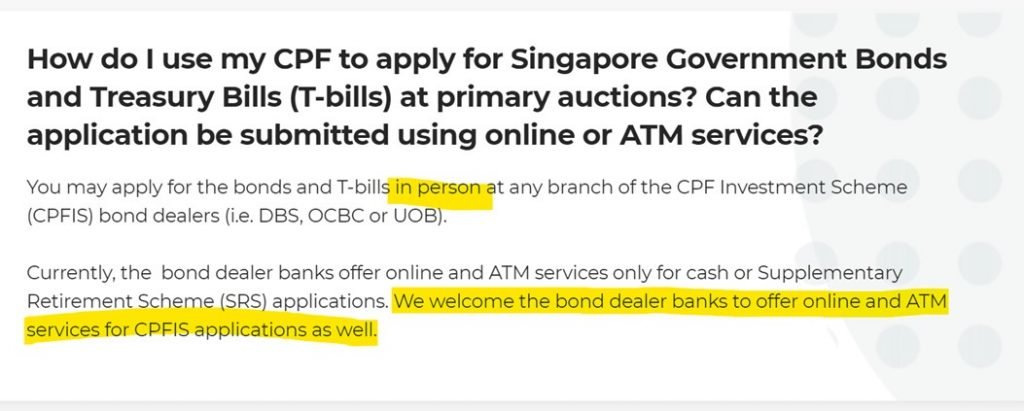

How to buy T-Bills with CPF-OA – You must go down to the bank IN PERSON

I know… this is 2022, after a huge global pandemic.

And I need to go down to the bank… in person… just to buy T-Bills with CPF-OA?!

I suppose the thinking is that before this, nobody was buying T-Bills using CPF-OA, so the banks saw no need to implement this feature.

There’s even a cheeky little note from CPF saying they “welcome the bond dealer banks to offer online and ATM services for CPFIS applications as well.”

Whoever wrote that line, you have my respect sir.

CPF Investment Account (CPF-IA)

FYI that you also need a CPF Investment Account (CPF-IA) with one of the three agent banks (DBS/POSB, OCBC, and UOB).

So go down to the bank that you opened the CPF-IA account with (or if you don’t have one then just open it when you go down).

Do remember to bring your NRIC/ Passport.

CPF-IA not required for CPFIS-SA funds

Sidenote that there is no need to open any CPF Investment Account if you wish to invest CPFIS-SA funds.

That said, CPF-SA pays 4%, which is higher than T-Bills for now.

But who knows, that might change in a couple of months.

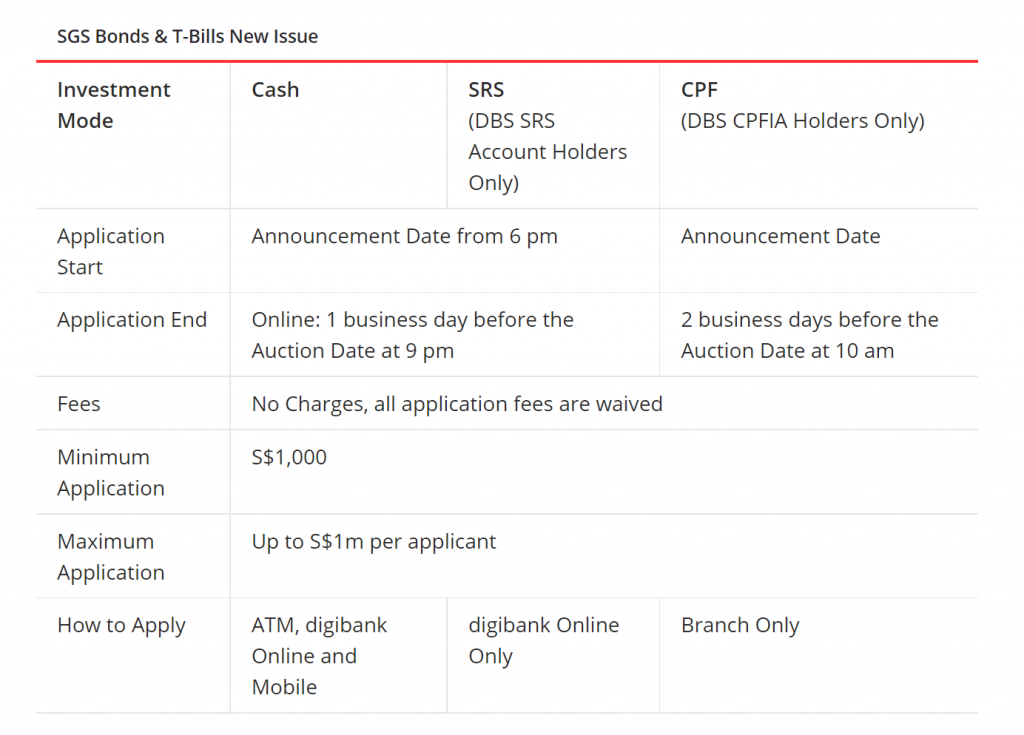

DBS has a great summary on the relevant fees and timings:

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- Whole bunch of freebies – A free packet of rice (1kg), a free Kopitiam Kaya Toast set, a $1.99 Double Mushroom Swiss at Burger King, and 50% off KFC Zinger Set just to name a few.

- 1.0% base interest on your first $50,000 (up to 1.4%)

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

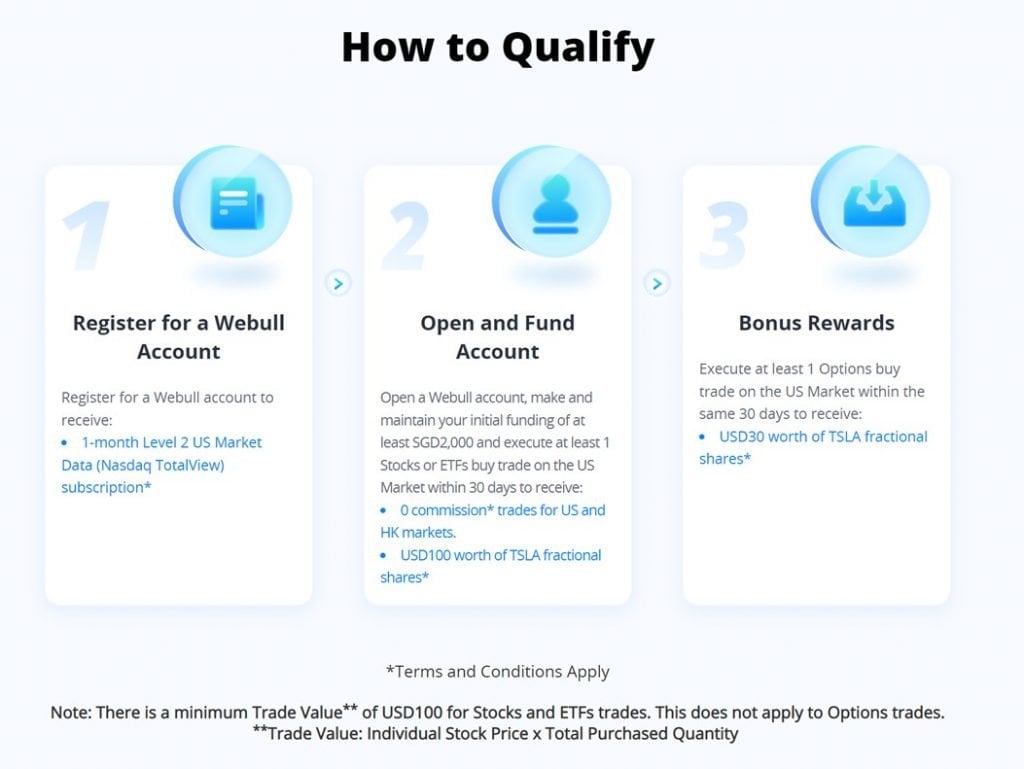

WeBull Account – Free US Stock, Options and ETF trading (Free USD130 (S$185) in Tesla shares)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

To get the USD130 (S$185) in Tesla shares, you just need to:

- Sign up here and fund S$2000

- Make 1 US Stock or ETF trade (you get USD100 in Tesla Shares)

- Make 1 Options trade (you get USD30 in Tesla Shares)

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 100 USD in Apple Shares with Webull, a zero commission broker.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

Enough about SSBs and T-Bills! 🙂 the global macro is the good stuff. Too bad mostly behind paywall now. Your global macro call has been spot on thus far; well done!

It seems like many people are interested in SSBs and T-Bills these days!

Anyway while the more specific trade ideas and price targets are behind paywall, I do try my best to share the gist on the free version of the site. Have an article coming out tomorrow on REITs to share general macro views, hope it helps!

My understanding is CPF interest is compound monthly but credited yearly. You may want to check if you think it’s compounded yearly.

Hm I just checked the CPF website and it says: “CPF interest is computed monthly. It is credited to your respective accounts by 1 January of the following year and compounded annually.”

But perhaps my understanding is not correct here.

Sorry nevermind my understanding is incorrect. You are right – calculated monthly and credited annually. Will update the article.

CPFIS compounded monthly n credited yearly. Interest is not calculated monthly based in the lowest amount but the amount at the end of the month.

I took this from the CPF website:

“CPF interest is computed monthly. It is credited to your respective accounts by 1 January of the following year and compounded annually.

CPF balances used for interest computation are affected by the transactions in your account. For instance, contributions (including refunds) received this month start earning interest next month. Withdrawals/deductions in this month will not earn interest from this month onwards.”

Not sure if my understanding is incorrect here. Or are you referring only to CPFIS?

Sorry nevermind my understanding is incorrect. You are right – calculated monthly and credited annually. Will update the article.

So anything above 2.71% per annum, and you probably break even.

False. Breakeven is 2.917% for 6 month T bill.

Breakeven is 2.71% for 12 month T bill.

Thanks, I actually meant it from a per annum basis, so assuming the 6 month T-Bills are rolled.

But I get your point, have updated the article to clarify this. Thanks for raising.

Please ignore my previous question on using SA. I had wrong info on the SA interest rate.

Hello FH,

Are there any way we as retail small time investor able/allow to buy USA 1 or 2 year Treasuries? If yes, where can we buy and also what are the related cost we should be mindful of?

Thank you

I suppose you mean buying them directly at issuance right, and not via a bond fund. It is not so straightforward to do so.

Why do you want to do so though? You take on the FX risk.

Could just go with T-Bills or SGS.

“Because of this, it actually makes sense to apply for T-Bills at the start of the month.

This way, they will mature on the start of the month – giving you time to roll over the money into new T-Bills, without spilling over into the next calendar month and losing another month of CPF-OA interest.”

Hi FH, just to clarify on the above. Isn’t the maturity date determined by the issue and not dependent on your date of application?

Sorry I meant to get the T-Bills that are issued at the start of the month, if you want to try your hand at optimising it this way.

Hi FH, can you kindly explain how the cut off yield for T bills is determined. Thank you.

Tan

Determined via auction – supply demand is matched to determine the cut-off. Quite a few qns on this, might see if I can do an article to explain.

Quoting your article: “If the global economy starts to collapse, or we get systemic risk, interest rate may get cut quite quickly.”

If I have already purchased T-bills, what happens to my current holdings when interest rate get cut?

I do not plan to sell my holdings until maturity (ie. 6-month)

No impact if you hold till maturity.

The market value of the T-Bills will go up if interest rates go down (inverse relationship), but if you plan to hold to maturity there is no impact.

thank you.

“Because of this, it actually makes sense to apply for T-Bills at the start of the month.”

Can I clarify that you mean the issuance of T-bills should be at the start of the month if the intention is to roll over, not the actual application or auction dates? thanks.

Sorry I meant issuance.

Although if you apply in the previous month and your CPFIS bank deducts the moneys from your CPF in the previous month, you will still lose the previous month interest. So don’t forget to watch the date when the funds are deducted from your CPF-OA.

Hi FH. I tried for the first time to invest some OA funds via my bank on the 25th for the current closing on the 27th. I am unsure how to know whether I am successful in my bid. I was wondering whether I needed to have funds ‘sitting’ in my bank investment account before I could invest or would it transfer from my OA account automatically. Any advice would be appreciated. Thanks.

If you applied non-competitive, it is 100% allotment for this auction so you should have gotten it.

But suggest to check with your bank directly, only they can confirm this. Just in case something went wrong with the application process.

Hi,

Is it that if i bgt it at 3% pa for 6mths, mean no matter what happen to the market, my 3% pa will not be affected even when the market crashed?

If i buying using cash via bank online, does the principal automatically deposit into my bank account after 6-mth?

Thank you

Yes that is right, the 3% is locked in on issuance, if you hold to maturity.

The principal will deposit into the bank account linked to your CDP (the account you get stock dividends with).

Hi,

All above also apply to CPF-SA (for the sum above $40k in SA), correct?

Please ignore my previous question on using SA. I had wrong info on SA interest rate

No problem! Yes this will make sense if T-Bill interest are a fair bit higher than CPF-SA’s 4%.

But I doubt we go much higher than 5% this cycle.

If I bought Tbills with OA, when it matures will the total amount automatically go back to my CPF OA account? If not, then what do I have to do to manually trigger the return to OA?

I believe it goes back into CPF-OA. Suggest to confirm this with your agent bank when you go down, since the application has to be made in person anyway.