Okay my apologies.

The next T-Bills auction is on 21 Dec, so for those of you who want to apply using CPF-OA, you probably need to get it done by Monday, 19 Dec.

That’s not a lot of time, and I probably should have gotten this article out earlier.

But the next auction opens on 28 December, so if you have some time after Xmas – You can pop down to the bank and buy some T-Bills with your CPF-OA, and make some easy money.

T-Bills at 4.4% yield – Must buy with CPF-OA?

The interest rate outlook has changed quite a bit since my previous CPF-OA article, so I wanted to update it.

The key questions are:

- Does it still make sense to buy T-Bills with CPF-OA?

- Should you apply for competitive or non-competitive bid for T-Bills?

- Should you apply for 6-month or 12-month T-Bills?

Does it still make sense to buy T-Bills with CPF-OA?

Short answer – yes.

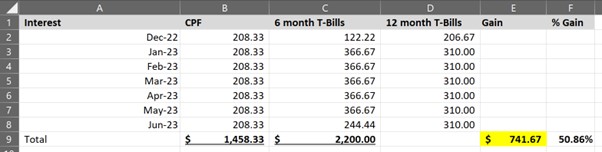

Assuming you invest $100,000 CPF-OA in T-Bills, you will make an extra $741.67 at the latest T-Bill interest rates of 4.4%.

Over 6 months.

That’s even after accounting for the 1 month lost CPF-OA interest.

That’s a whopping 50.86% increase in interest earned over CPF-OA.

The more money you have in your CPF-OA, the more worth it this becomes.

What risks to consider when buying T-Bills with CPF-OA?

The biggest one?

CPF-OA interest rates going up.

If CPF-OA rates do go up, you won’t benefit because you already bought T-Bills with CPF-OA money.

Now – Will CPF-OA rates go up?

It’s a tricky political issue, because HDB mortgage rates are tied to CPF-OA.

And interest rates were stuck at rock bottom the past 10 years while CPF-OA didn’t go below 2.5%.

Now that interest rates go up, CPF-OA goes up immediately?

Not an easy one to call, and I leave it up to you to decide.

Long story short – if you think CPF-OA interest rates will go up soon to match T-Bills, then it wouldn’t make sense to buy T-Bills with CPF-OA.

What is the estimated yield on the T-Bills?

Of course, the other key question is whether we will see 4.4% yield on the next T-Bills again.

Now T-Bills cut-off yields are determined by auction.

Demand and supply are matched to determine the final yield, on a per auction basis.

This makes it close to impossible to predict the exact yield ahead of time, unless you know what every bidder is going to bid.

But… we can still get some clues from market pricing, and make educated guesses from there.

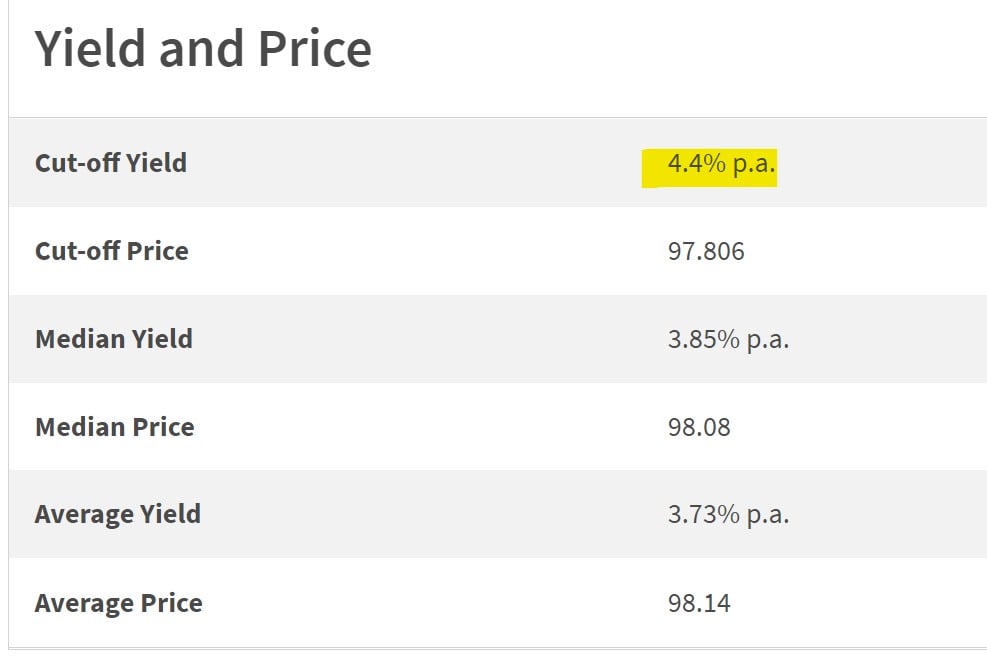

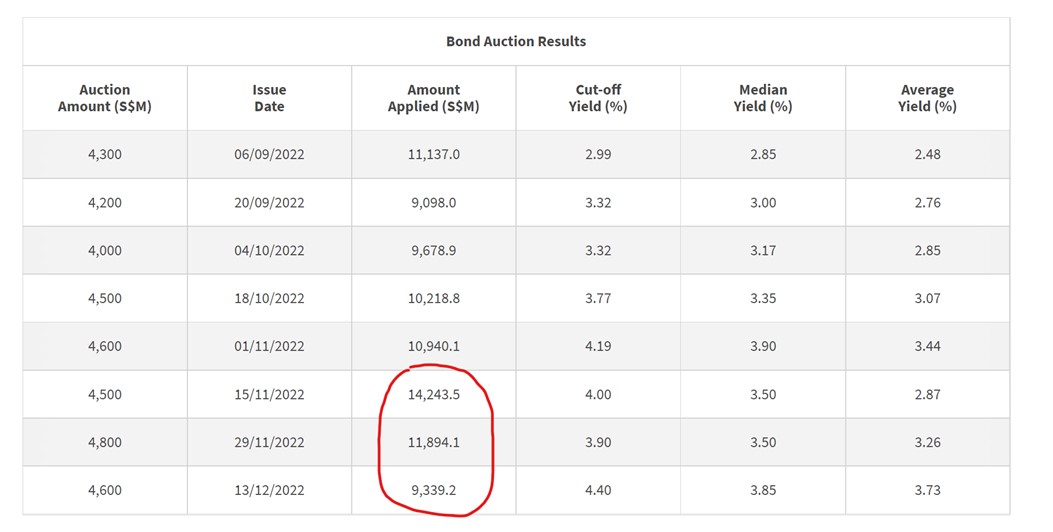

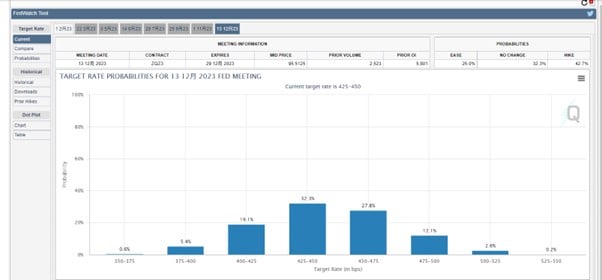

Previous T-Bills Auction – 4.4% yield

The previous T-Bills auction on 8 Dec closed at 4.4% yield, the highest since 1988.

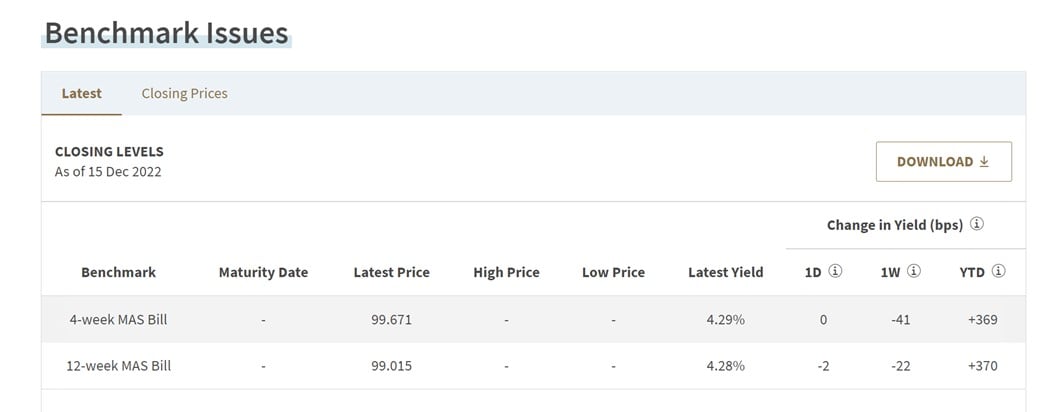

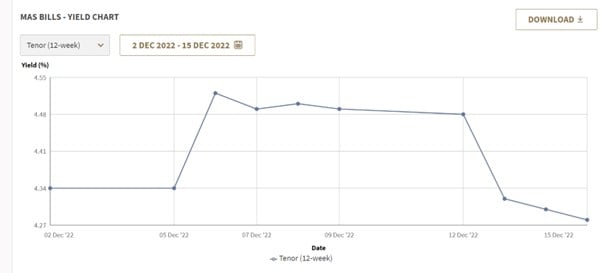

12 week MAS Bills – 4.28%

The latest 12 week MAS Bills are trading at 4.28%.

MAS Bills are only available to institutional investors, so they give you a general idea of what the market is pricing in as fair value – without the noise that comes from retail investors.

Unfortunately though, the pricing shows a clear downtrend in yields since early December.

Why are short term yields dropping despite the Feds raising rates by 0.5%?

I get a lot of questions as to why yields are dropping even though the US Federal Reserve just raised rates by 0.5% this week.

The simple answer – is that the 0.5% raise was already priced in by the market.

What the market wasn’t so sure about, was whether it was going to be a 0.5% or 0.75% raise.

And once Powell confirmed it would be only 0.5%, short term interest rates came down as it took away the possibility of a 0.75% rate rise.

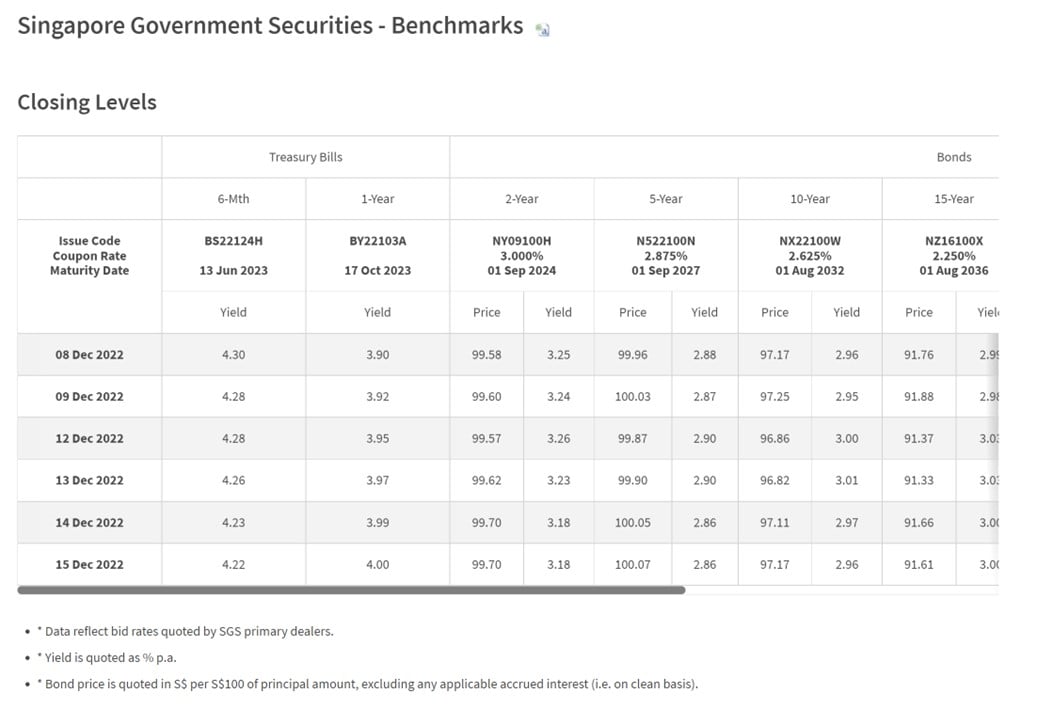

Market Price of 6 month T-Bills – 4.22%

Market pricing for 6 month T-Bills have softened a bit based on the logic above.

It’s come down to 4.22%.

Estimated fair value for T-Bills?

Assuming no curve ball from retail investors?

I would expect it to come in slightly below the 8 December’s 4.4% because of the slower pace of Fed rate hikes.

I would probably say 4.2% – 4.3%, fair value.

Wild card will be retail demand

But of course, no discussion on T-Bills will be complete without discussing retail demand.

There are 2 schools of thought here.

The first is that at 4.4%, and with all the newspaper reports covering it – retail investor demand is going to pour in, bringing yields down.

The second is that retail investor liquidity has been all sucked up by a mix of Fixed Deposits, Singapore Savings Bonds, and older T-Bills.

And that too many of them are on leave / holiday to bother putting in real bids.

This means yields might stay high.

Frankly a tough call, and I have no easy answers for this one.

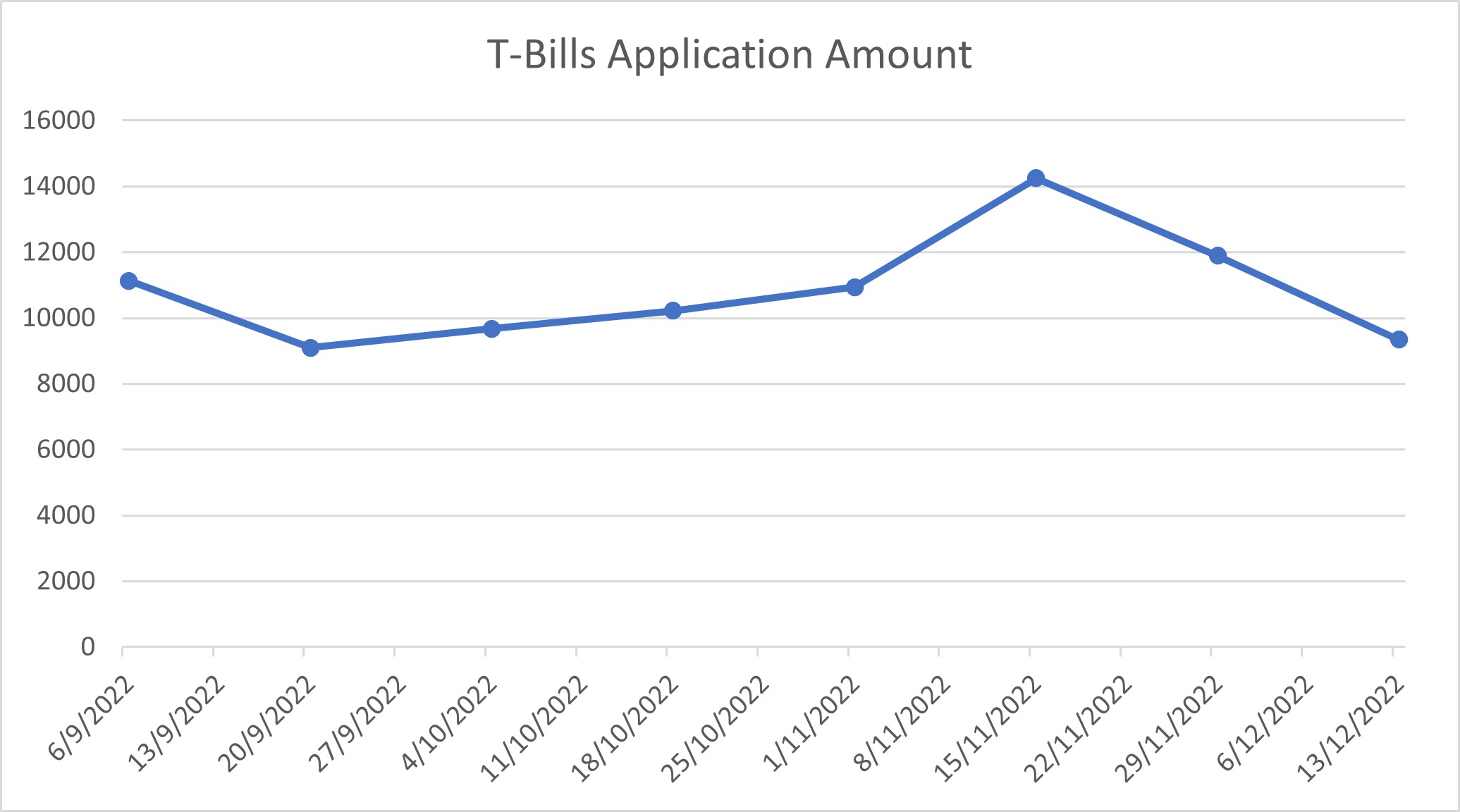

What I do know, is that there was a clear downtrend in application amount the past 3 T-Bill auctions.

But whether this holds true for the next T-Bill auction on 21 December, is anyone’s guess.

Should you apply for competitive or non-competitive bid for T-Bills (using CPF-OA)?

Because of this, I would strongly suggest to submit competitive bids only, if you are serious about buying T-Bills.

The problem with submitting non-competitive bids, is that you’re going to get allotted at whatever the cut-off yield is.

If there is a freak result and the T-Bill yields close at 3.5%, you’re still forced to buy.

With a competitive bid you only get allotted if the final yield is above your bid yield

Example – if you bid competitive at 4.2%, you’ll only get allotted if the final yield is 4.2% or above. And if the cut-off yield closes at 4.4%, you’ll get allotted at 4.4%.

There’s very little reason not to use a competitive bid for T-Bills.

If you submit competitive, the moneys are only deducted from your CPF-OA if your bid is successful

Helpful tip that if you submit competitive bids for T-Bills using CPF-OA money.

The moneys are only deducted from your CPF-OA account if your bid is successful.

If the bid is not successful, the moneys are not deducted, and you continue earning the CPF-OA interest.

So you don’t really lose anything if you submit a competitive bid using CPF-OA money, that fails.

Except of course for your valuable time – as you do need to go down to the bank in person to submit this application for now.

So you’re probably looking at an hour plus of your time at the bank, and I leave you to decide how much that is worth.

What yield to bid for competitive bid for T-Bills (using CPF-OA money)?

Which leads us to the next question.

What yield should you input for competitive bidding?

I know there are some investors who suggest bidding as low as possible (say 1.0%), to guarantee allotments.

After all if you’re going to spend an hour at the bank queuing, you shouldn’t be leaving empty handed.

I’m not a fan of this kind of thinking because if enough people think this way, T-Bills yield is going to close at 1.0%.

So I suggest to approach this question by thinking about your next best alternative.

Think seriously about where the money will go instead of T-Bills.

And then use that as your baseline yield.

What is the alternative to T-Bills for CPF-OA money?

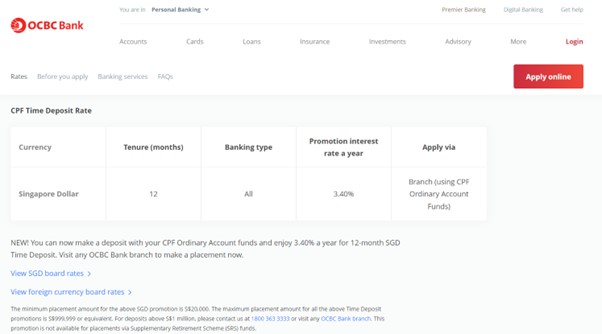

Unfortunately you cannot buy Singapore Savings Bonds with CPF-OA, only Fixed Deposits.

And unfortunately, you can’t just put it into any off the shelf fixed deposit you want.

It needs to be a special “CPF-OA” approved Fixed Deposit with one of the 3 local banks:

For now, the only such fixed deposit I know of is OCBC at 3.4%.

The duration is slightly different though, because it is a 12 months period instead of T-Bills at 6 months.

What yield to bid for competitive bid for T-Bills (using CPF-OA)?

So to answer this question simply.

Fair value for the 21 Dec T-Bills is probably 4.2% – 4.3%.

Unfortunately with CPF-OA the best other alternative is OCBC’s 3.4% fixed deposit, over 12 months.

There’s a bit of duration mismatch (6 month T-Bills vs 12 month Fixed Deposit), so you’ll probably want a small premium to OCBC’s 3.4%.

I know I’m going to get crucified for saying this.

But if you are buying T-Bills with CPF-OA, via competitive bidding, probably anything 3.8% – 4.0% and above would make sense.

The key difference is that CPF-OA cannot be so easily deployed into other alternatives.

So the main risk you need to worry about is not being able to access your CPF-OA, and interest rates going up.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Should you apply for 6 month or 12 month T-Bills?

The answer to this question, depends very much on where T-Bill interest rates will be in 6 months.

And whether you can roll over your 6 month T-Bills the same month, without losing another month’s CPF-OA interest.

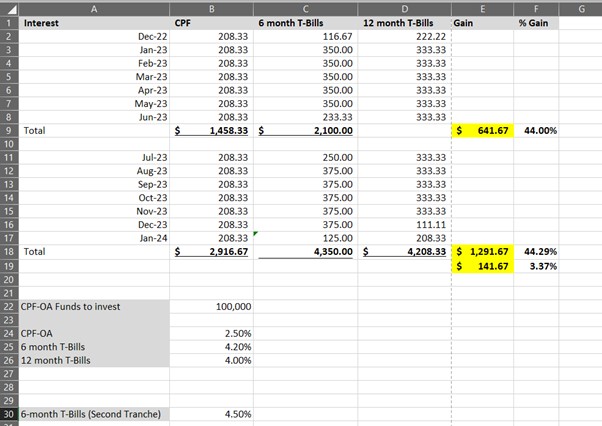

Assuming:

- You can buy T-Bills at the latest market price of 4.2% for 6 month, and 4.0% for 12 months

- Interest rates for 6 month T-Bills go up to 4.5% when you roll over

- You don’t roll over the 6 month T-Bills the same month, and lose another month of CPF-OA interest

6 month T-Bills comes out slightly ahead by $141.67, or 3.37% only.

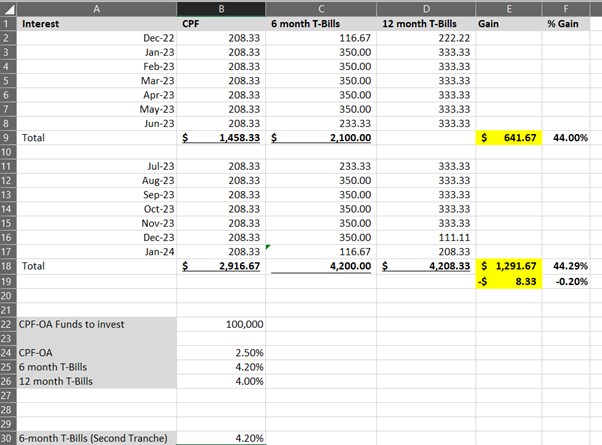

Assuming everything above, but:

- Interest rates for 6 month T-Bills stay flat at 4.2% when you roll over

Then 12 month T-Bills comes out slightly ahead by $8.33, or 0.20% only.

Long story short – they are incredibly close, to the point that I probably wouldn’t fret about this.

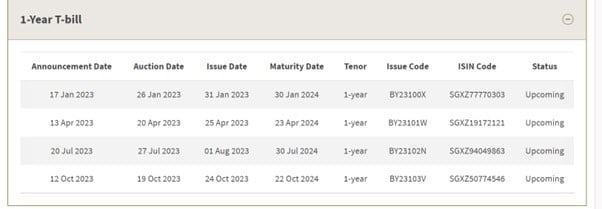

Next 12 month T-Bill auction is on 26 Jan 2023

Your bigger consideration, might be that the next 12 month T-Bill auction is quite far away on 26 Jan 2023.

By waiting until then, you would already have lost 1 month of higher interest, and who knows where interest rates would be then.

If it were me, I would probably just focus on what I can control, and buy the next available 6 month T-Bills.

This way I’m already earning the higher interest today, instead of waiting another month.

For those who really, really want to min-max and squeeze every single drop of yield out of their money though.

Let’s discuss a bit more on where interest rates will be in 6 months.

What does the Federal Reserve think?

Jerome Powell made it clear that while they are slowing down the pace of rate hikes in the short term, the mid term goal remains very much fighting inflation.

And despite a slower pace of rate hikes, they now see the terminal interest rate closing at 5 – 5.25% some time in 2023.

Or in plain English – higher, for longer.

This is what the Federal Reserve sees.

Rates peaking at 5 – 5.25% in 2023, and then decline to ~4% in 2024, and ~3% in 2025.

If you follow this analysis, interest rates will probably be higher in 6 months.

What does the market predict?

The market though, is much less sanguine, and see rates dropping to 4.25% – 4.5% by end 2023.

So… who is right here?

My personal views?

The answer to this question will be your playbook on how to invest in 2023.

And it’s a very tough one.

I think what is clear, is that the worst of inflation is probably behind us.

With Fed Funds at 4.5%, the economy is slowing, and inflation will start to come down.

As we move into 2023, you’ll see the narrative] shift away from inflation, and into growth / recession fears.

The million dollar question now, is whether inflation drops from 7% to 2% in a straight line the next 12 months.

Or whether it bounces around for a bit, settling in a 3 – 4% kind of range.

That kind of scenario could be a total nightmare for the Feds, forcing them to keep rates at 5% for longer than expected.

Remember – the official inflation target is 2%, so 3 – 4% inflation doesn’t really cut it.

So yeah… not an easy call.

What would I do – Buy 6 month or 12 month T-Bills with CPF-OA?

Gun to my head, I think interest rates are *probably* flat or slightly higher in 6 months.

But do I want to bet big money on this?

Not so sure.

But coming back to the question above – if it were me, I would probably just focus on what I can control, and buy the next available 6 month T-Bills.

This way I’m already earning the higher interest today, instead of waiting another month.

It’s money in my hand today, versus holding out for the hope of more money down the road.

But really, it’s your call.

Don’t forget to get your CPF-OA applications in by 19 Dec if you want to go for the 21 Dec T-Bill auction.

Alternatively you can go for the next T-Bill auction on 5 Jan 2023, and you just need to get your applications in by 3 Jan 2023.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

WeBull Account – Free USD150 ($212) cash voucher

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with a free USD 150 (S$212) cash voucher.

You just need to:

- Sign up here and fund S$2000

- Make 1 US Stock or ETF trade (you get USD100)

- Make 1 Options trade (you get USD50)

1080-1080-002-1024x1024.jpg)

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Is it possible there are 2 questions instead of one:

1. Will CPF OA rates go up?

2. If yes, by how much?

I’m hoping CPF OA rates will go up (to say 3%?). But I don’t think I dare to hope it will go up to 4.4%. It just seems unthinkable CPF would raise the rate to match T-bill rates. What do you think?