I’ve been getting quite a few questions on the expected yield for the next round of T-Bills.

Interestingly – this month will see not just the 6 month T-Bills, but also the 12 month T-Bills.

3 key questions I wanted to discuss:

- What is the expected yield on the next 6 month T-Bills?

- For cash investors – Should you buy 6 month T-Bills or 12 month T-Bills (or Fixed Deposit / Singapore Savings Bonds)?

- For CPF-OA investors – Should you buy 6 month T-Bills or 12 month T-Bills?

Quite a bit to discuss, so let’s go!

Next 6 month T-Bill Auction on 13 April 2023

First off – next 6 month T-Bill Auction is on 13 April.

If you’re buying with cash you want to apply by 9pm on 12 April.

And if you’re buying with CPF you want to get it done by 11 April.

Note that there is a 12 month T-Bill Auction on 20 April 2023

Now there are only 4 12 month T-Bills available for auction in 2023.

And the next one will be available on 20 April 2023.

So those looking to buy T-Bills this month will have the chance of picking between 6 month and 12 month T-Bills.

What a treat!

What is the expected yield on the 6 month T-Bills?

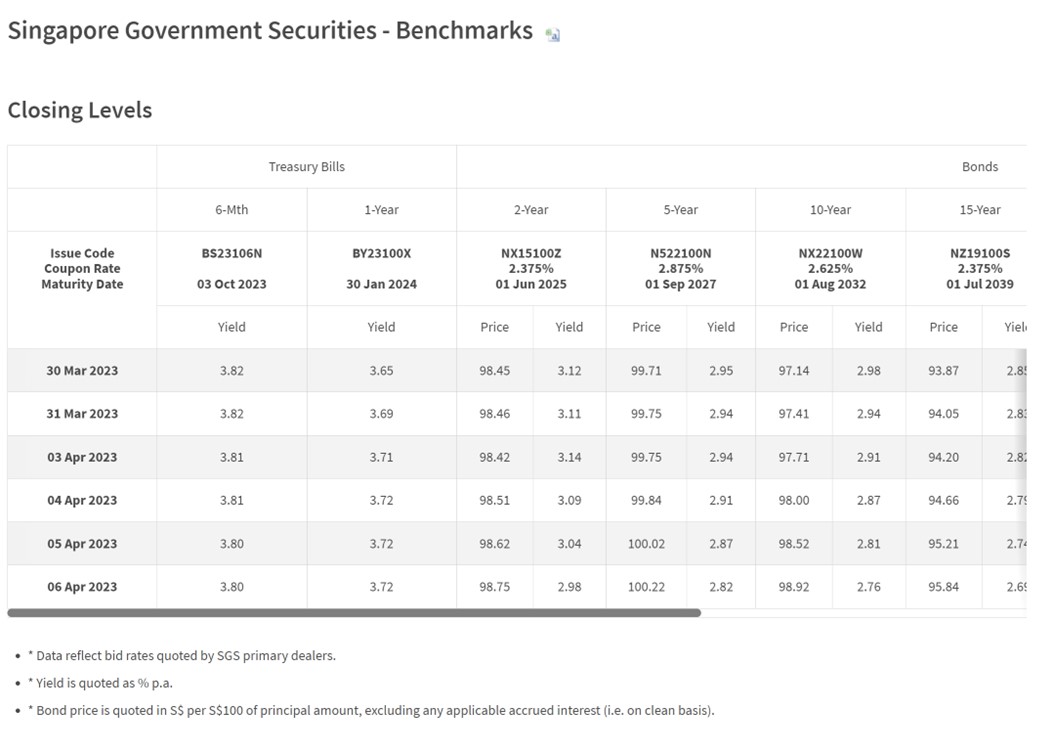

6 month T-Bills trade at 3.80%

The 6 months T-Bills trade at 3.80% on the open market today:

12 week MAS Bills yield 3.98%

While the 12 week MAS Bills trade at a much higher 3.98%.

These are institutional only products, which gives you an idea of where yields would be like without the distortion that comes with retail demand (and CPF-OA money).

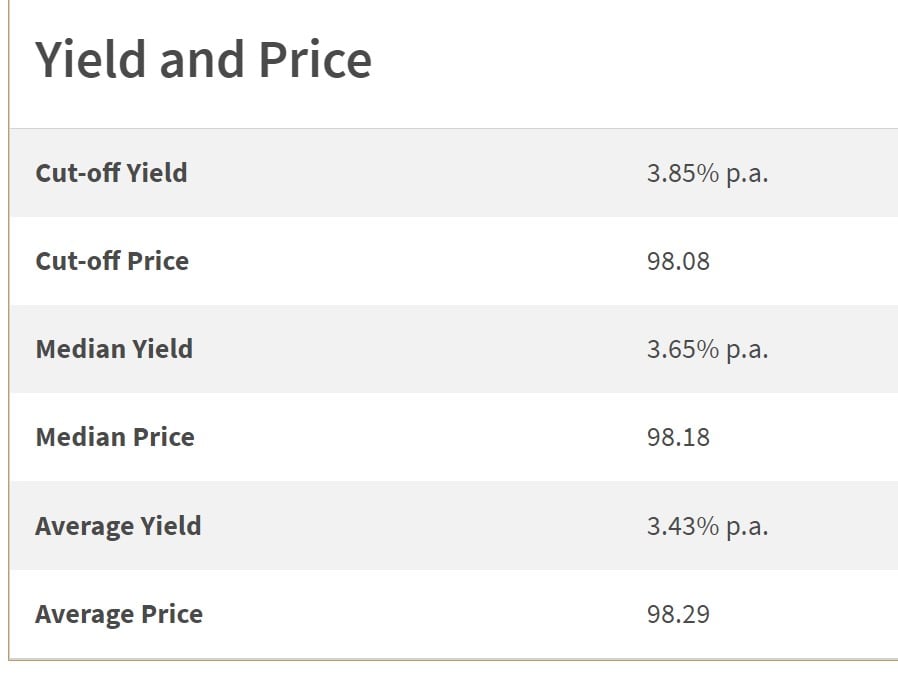

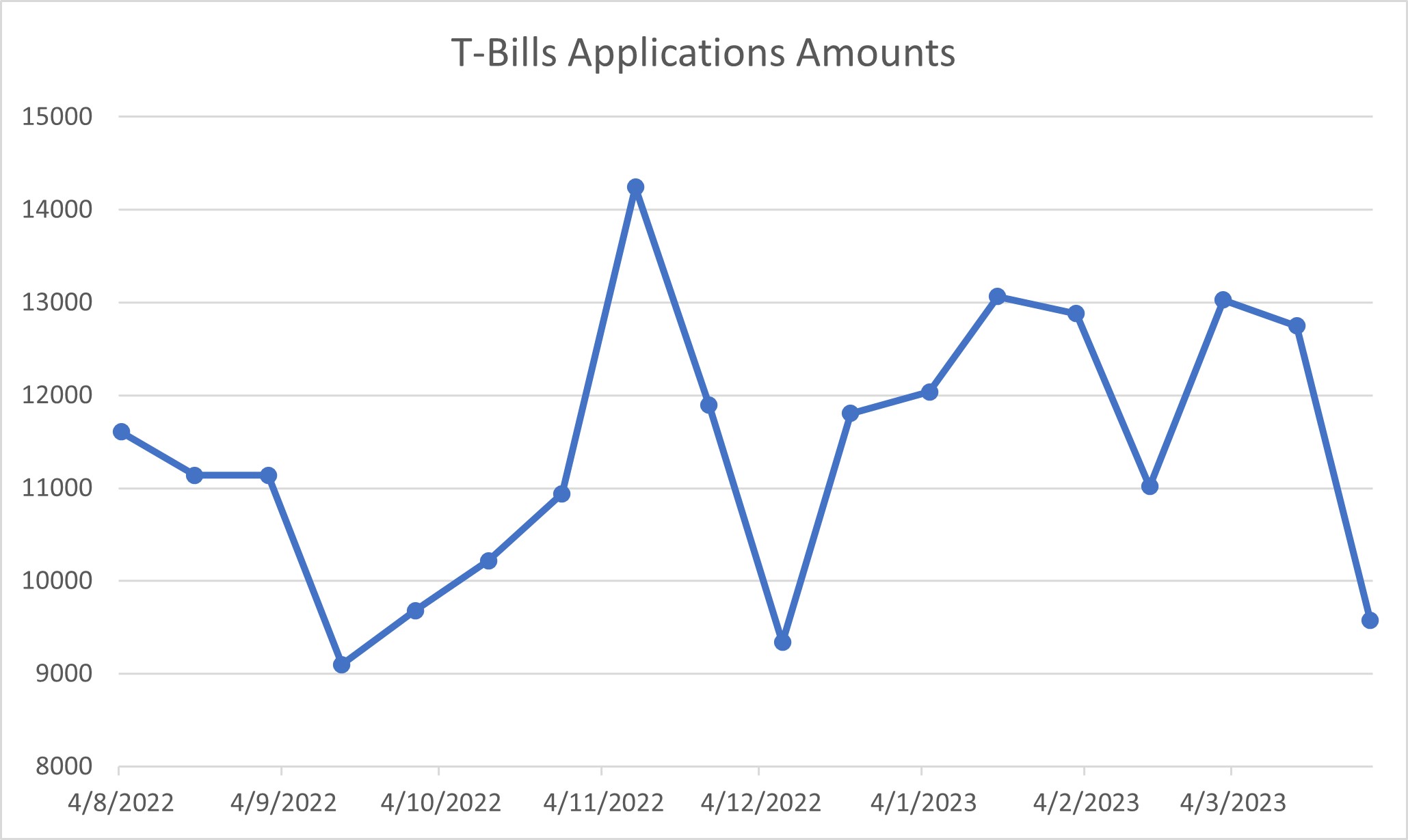

Last T-Bill Auction closed at 3.85% yield (but big drop in demand)

The most recent T-Bill auction closed at 3.85% yields.

However the last T-Bills auction had a big drop in demand.

From close to $13 billion the previous auction, to $9.6 billion.

That’s almost a 25% drop in application amount.

A lot of readers have speculated that this was because of the timing of the auction (end of the month) – which meant that CPF-OA buyers would have lost both the March and April interest.

This is possible, and if true we might see application amounts rebound this time – pushing yields down.

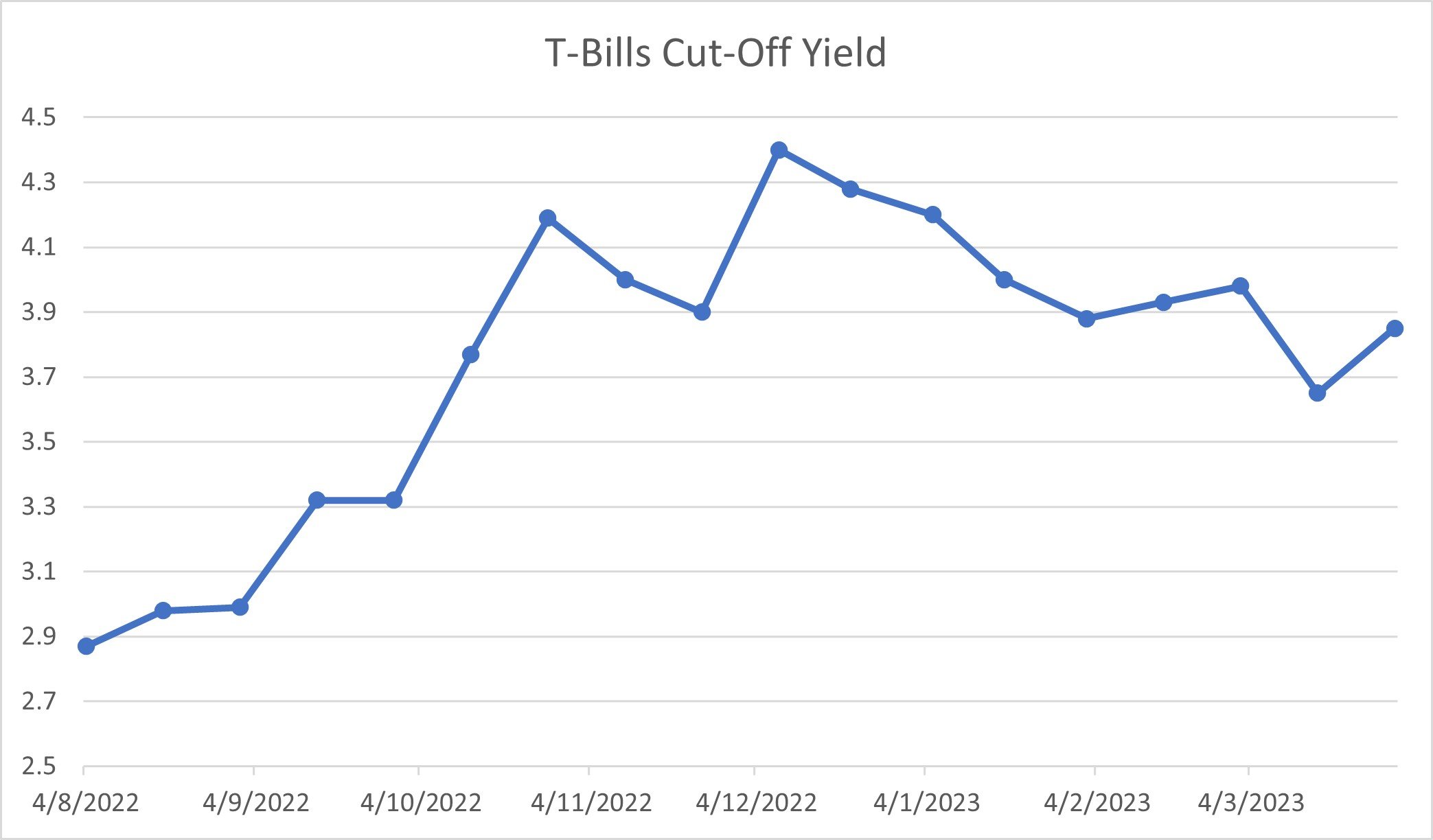

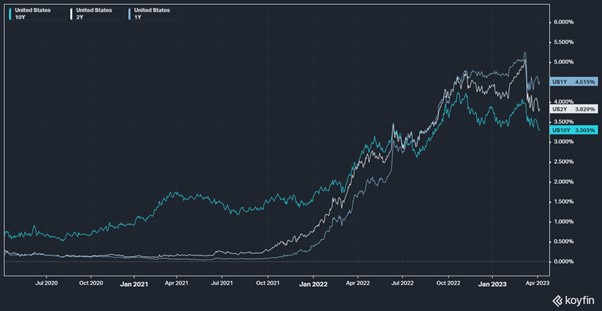

Interest Rate Trend is up (for 6 month – 12 month yields)

Interest rate trends from the past few weeks tells an interesting story.

You can see how the 2 year yield has trended down after March’s sharp decline (due to the banking crisis)

But the 1 year yield has actually trended up.

In plain English – as the banking crisis stabilised, the market has become more realistic on the timing of interest rate cuts.

It no longer expects interest rate cuts so soon, which is why the 1 year yield has gone up, while the 2 year yield has gone down.

So this should be a bullish for 6 and 12 month T-Bill yields.

T-Bills Auction on 13 April – Expected yield of 3.8 – 3.9%

Put all the above together though, and I think you’ll see the next 6 month T-Bills yields come in at 3.8% – 3.9%.

Give or take a little.

As always – I encourage investors to submit a competitive bid just in case we get a freak result and yields drop sharply.

What is the expected yield on the 12 month T-Bills (on 20 April 2023)?

Just a quick note that interest rates are very volatile these days.

That is why I try to write these articles as close to the auction date as I can, to increase the accuracy of the forecast.

So trying to predict the yield on the 20 April 12 month T-Bills is a bit of a fool’s errand, as a lot of things can change between now and then.

Take a guess FH…

If you look at market pricing though, the 12 month T-Bills yield 3.72%.

Gun to my head, I think you’ll see yields come in around there – but maybe on the lower end because of CPF-OA demand.

In any case, that is actually very close to the 6 month T-Bills.

Reason would be because the market is no longer pricing in significant interest rate hikes (or cuts) in the period falling 6 – 12 months from today.

So… Should I buy 6 month T-Bills or 12 month T-Bills (for cash investors)?

Personal view – I think it’s very close.

It ultimately comes down to whether you think interest rates will get cut drastically in 6 – 12 months’ time.

For me I would probably still go with the 6-month T-Bills.

Reason being that these T-Bills don’t have good liquidity, and it’s very hard to get the money back before maturity.

Because of that I would expect a yield premium to lock up the money for 12 months, which I don’t think we will get (because of CPF-OA demand).

If I really wanted to lock cash up for 12 months I would just go with fixed deposit.

Note that this analysis is for cash, CPF-OA investors have quite different considerations as I will discuss below.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

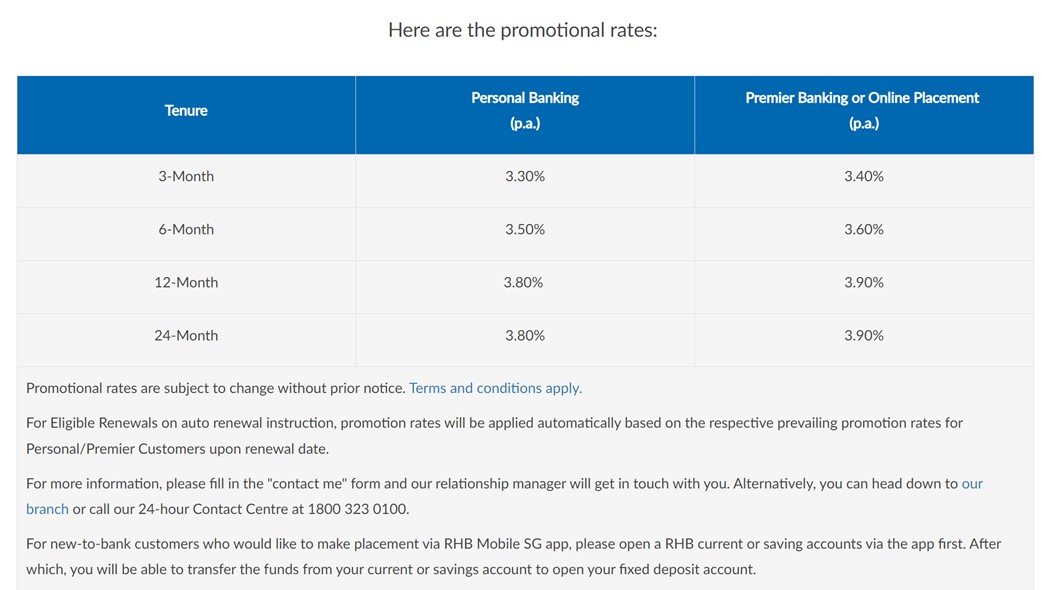

Fixed Deposit Rates yields up to 3.9% – Better Buy than T-Bills?

On that note – the highest yielding fixed deposit in the market right now is with RHB bank.

You can get 3.90% on a 12 or 24 month fixed deposit.

Minimum amount is $20,000.

So between a 12 month T-Bill and a 12 month Fixed Deposit – I think I would go with the Fixed Deposit.

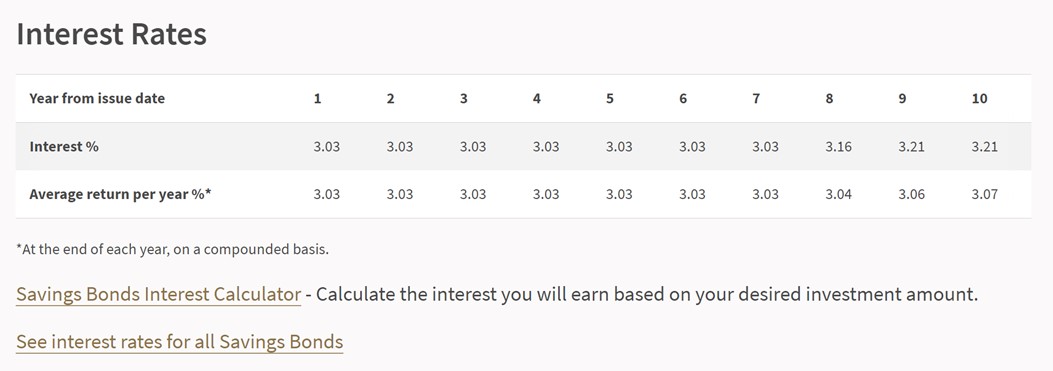

Better Buy – Singapore Savings Bonds vs T-Bills

For reference, here are the interest rates on the latest Singapore Savings Bonds.

You’re looking at 3.03% for the first 7 years, stepping up to 3.07% after 10 years.

Singapore Savings Bonds are quite a different product from T-Bills.

With the current inverted yield curve, I would say go with T-Bills or Fixed Deposit if you want to benefit from the high short term interest rates.

Go with Singapore Savings Bonds if you want the optionality to hold up to 10 years.

I myself hold my cash in a mix of T-Bills, Fixed Deposit and Singapore Savings Bonds.

So yes – there is a place for each of them in a Singapore investor’s portfolio.

It’s ultimately a trade off between yields, liquidity, and duration – and I suggest each investor put some thought into what the right balance for them is.

Why you should buy 12 month T-Bills with CPF-OA (instead of 6 month T-Bills)?

The final question I know many of you will ask.

For those buying using CPF-OA.

Is it better to buy the 6 month, or 12 month T-Bills?

In January – I thought that the 6 month T-Bills were a better buy

I looked at the exact same question back in January, and my thinking then was that the 6 month T-Bills were a better buy.

The reason being that back in Jan:

- Those T-Bills were issued at the end of the month, meaning you lost an extra month of CPF-OA interest on maturity

- Good chance of 12 month T-Bills yields coming in low

- Good chance of interest rates being higher or flat in 6 months

A lot of things have changed since January 2023

Well, fast forward 3 months and a lot of things have changed.

Not least a “banking crisis” completely changing the interest rate outlook from the Feds.

Ask me the same question today, and I might say that the 12 month T-Bills are a better buy (if you are using CPF-OA).

Couple of reasons:

- Maturity Date is not the last day of the month

- 12 month T-Bills yields may come in close to the 6 month T-Bills

- Will interest rates be lower in 6 months?

Maturity Date is not the last day of the month

Unlike the January 12 month T-Bills which would mature on 30 Jan 2024 – giving you virtually no time to roll them into new T-Bills or transfer back to CPF-OA.

These 12 month T-Bills will mature on 23 April 2024.

Which means if you are quick about it, you could probably transfer the cash back into CPF-OA before May 2024 – and avoid losing the May 2024 CPF-OA interest.

This alone is a pretty big point in favour of this 12 month T-Bills.

12 month T-Bills yields may come in close to the 6 month T-Bills

You can also see from market pricing that the 6 and 12 month T-Bills have yields that are quite close to each other.

3.80% on the 6 month T-Bills, 3.72% on the 12 month T-Bills.

Reason being that the market is no longer pricing in significant interest rate hikes (or cuts) in the period falling 6 – 12 months from today.

I think you cannot deny that the interest rate climate has changed completely since January 2023.

Which brings us to the next point.

Will interest rates be lower in 6 months?

In January everyone was still expecting the Feds to hike us to 5.5% and beyond.

So in January, the risk for interest rates was still to the upside.

Whereas today, almost everyone accepts that we’re going to see at most 1 more interest rate hike (if at all).

And after last month’s “banking crisis” – investors are starting to get jittery about when interest rate cuts would start coming into play.

Today, the risk for interest rates is to the downside.

My personal view?

My personal view of course, is that we don’t see interest rate cuts in 2023.

But investing is about risk-reward.

If the 6 month T-Bills trade at 3.80%, and the 12 month T-Bills trade at 3.72%.

And if the interest rate risk over the next 12 months is to the downside rather then upside.

Well – I don’t really see the incentive to buy 6 month T-Bills with CPF over 12 month T-Bills, assuming the auction rates are close to market rates.

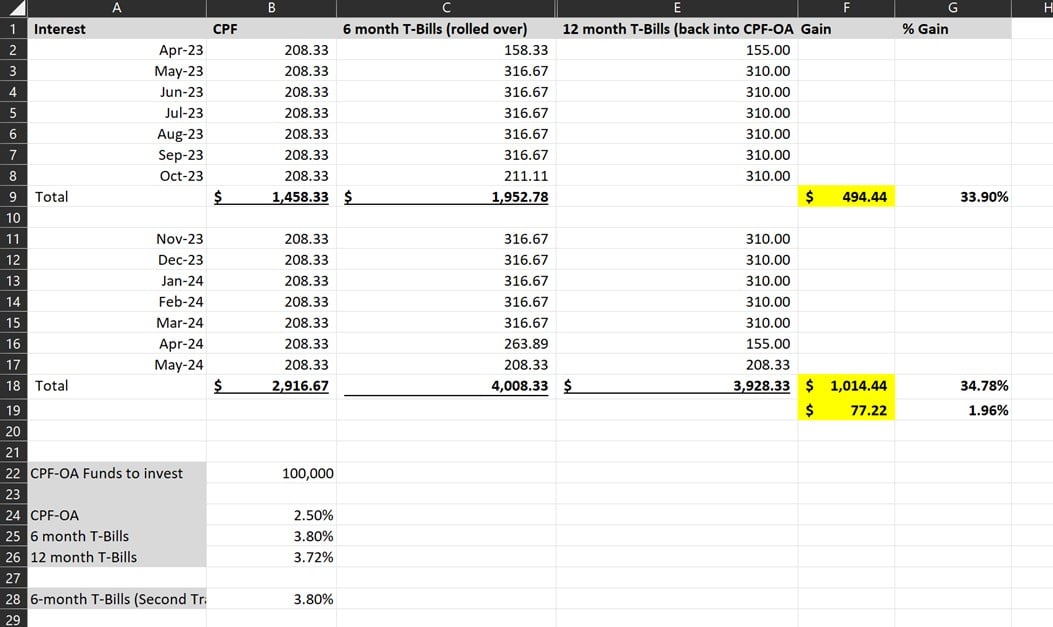

A simple illustration

A simple illustration on this.

Let’s assume the guy who buys 6 month T-Bills:

- Buys them at 3.80% (latest market pricing)

- Rolls them over at 3.80% in 6 months (big assumption here)

- Rolls over the same month (avoids losing another month of CPF-OA interest)

Whereas the guy who buys 12 month T-Bills:

- Buys them at 3.72% (latest market pricing)

Here are the results.

The guy buying 6 month T-Bills makes an extra $77.22 on $100,000.

That’s absolutely tiny, for the amount of additional work and risk.

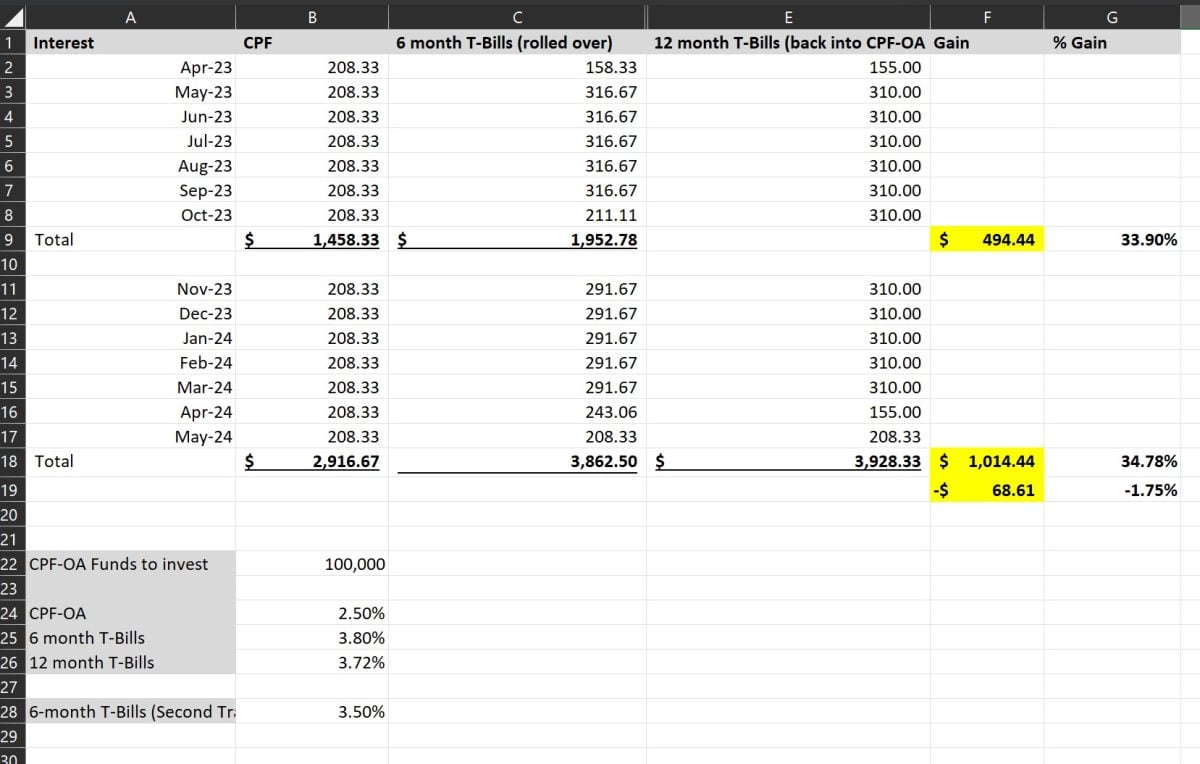

What is the risk taken on by buying 6 month T-Bills?

Because of course – the biggest assumption we used above…

Is that you can roll over CPF-OA into new T-Bills at 3.80% in 6 months’ time (October 2023).

Is this realistic?

Who knows – market seems to be pricing in an economic breakdown in the second half of 2023.

You can see the difference if we assume the 6 month T-Bills are rolled over at 3.5% – suddenly the 12 month T-Bills come out on top.

Not only that, but the guy buying 6 month T-Bills also needs to scramble to roll over the T-Bills into new T-Bills in October 2023.

Whereas the guy with 12 month T-Bills can just sleep in peace knowing he’s locked in his yields for 12 months, and doesn’t need to lift a finger in 6 months’ time.

What is the risk taken on by buying 12 month T-Bills?

Of course, the 12 months T-Bills approach is not without its risks too.

The biggest one being – whether you’ll be able to buy 12-month T-Bills at close to market pricing of 3.72%.

The previous 12 month T-Bills auction in January was quite hotly subscribed, so the cut-off yields came in quite a bit below market pricing.

This is definitely a risk for the April Auction as well.

Especially if many people have the same thinking as I shared above.

So… I leave it up to each investor to decide what is the best course of action.

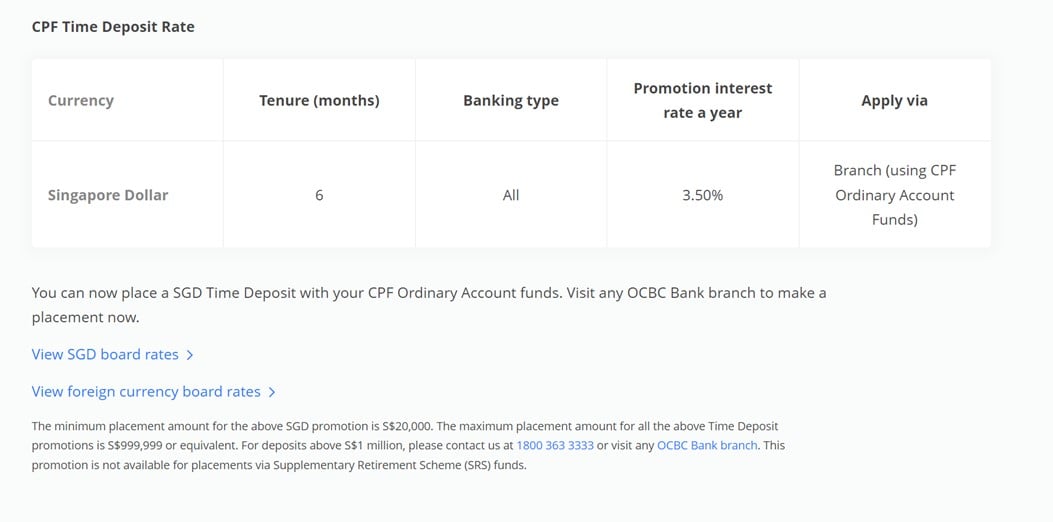

Fixed Deposit not that attractive an option for CPF-OA investors (T-Bills still a better buy)

Just to note that the only Fixed Deposit option available for CPF-OA investors is 3.50% for 6 months with OCBC.

I don’t think this is attractive as it is quite a bit below market yields on T-Bills.

You’re better off just going with T-Bills, especially since the application process is fully online these days.

Timeline to subscribe for the 13 April 6 month T-Bills

In any case, the next 6 month T-Bill Auction is on 13 April.

If you’re buying with cash you want to apply by 9pm on 12 April.

And if you’re buying with CPF you want to get it done by 11 April.

This article is written on 7 April 2023 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon, together with weekly premium macro updates like this one. You can access my full personal portfolio to check out how I am positioned as well.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

WeBull Account – Get up to USD 500 worth of fractional shares (expires 28 April)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares.

You just need to:

- Sign up here and fund any amount

- Maintain for 30 days

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Hi,

The table The guy buying 6 month T-Bills makes an extra $77.22 on $100,000.

May I know how you derive

6 Month T-Bills (roll over)

Apr-23 is 158.33

Oct-23 is 211.11

12 month T-Bills (Back into CPF-OA )

Apr-23 is 155.00

Me quite confused over calculation. Hope you can enlighten me

Sorry just to clarify – I just assumed the number of days in the first and last month for calculation’s sake.

So for example if the first month I assumed you get 25/30 days of T-Bills interest in the month, then the final month will receive 5/30 days of T-Bills interest.

You can play around the numbers as you please, but the result will be the same.

Hello FH.

I asked this in a previous update so you might not have seen it. So I will ask again and hope that you have time for a reply.

I have a question regarding procedure involved with a T-Bill roll-over using CPF-OA. Suppose a 6 month old T-Bill has matured. I understand that the invested amount will then be returned to the investment account of the bank as there is no automatic transfer back to the CPF-OA account. Then suppose that a new roll-over T-Bill investment is planned for. Can and will the new T-Bill be purchased with the funds which are now in the respective bank’s investment account instead of the account holder’s CPF-OA account? I have a T-Bill maturing soon and if the rates are acceptable, I would like to roll it over but do not know whether I would need fresh funds in my CPF-OA if there are aready sufficient funds in my bank’s investment account. Any clarity on this would be greatly appreciated. Thank you.

Sorry for the delayed reply. Yes – you can use the CPF-IA funds to buy the T-Bills directly. But be sure to use the same agent bank that holds your CPF-IA funds. 🙂