So I came across this chart recently that I was really excited to share with you guys.

It basically sets out the Top 10 ETFs bought and held by SRS Investors in Singapore.

Top 10 ETFs bought by SRS Investors in Singapore

Arranged by order of popularity, the Top 5 most popular ETFs are:

- SPDR Straits Times Index ETF (ES3)

- Nikko AM Singapore STI ETF (G3B)

- Lion-OCBC Securities Hang Seng Tech ETF (HST)

- SPDR Gold Shares (GSD)

- Lion-Phillip S-REIT ETF (CLR)

The next 5 on the list are:

- SPDR S&P500 ETF (S27)

- NikkoAM-StraitsTrading Asia ex Japan REIT ETF (CFA)

- ABF Singapore Bond Index Fund (A35)

- Nikko AM SGD Investment Grade Corporate Bond ETF (MBH)

- iShares Barclays USD Asia High Yield Bond Index ETF

I emailed SGX to clarify some points, and this was their reponse:

- The list is as of August, but there hasn’t been major changes since

- They are arranged in order of popularity

- The stats only include self-directed SRS investors. So if you invest your SRS via say Endowus, those stats would not be included in here.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Just created a Discord server where I collate analyst reports and investing resources that I come across in my research. Hit us up here if you’re keen.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

My reaction to the Top 10 ETFs bought by SRS Investors in Singapore

It’s interesting because the way that SRS works, the best ETF would be something like the QQQ (NASDAQ100).

You basically want something to:

- Buy and hold long term

- Focus on capital gains rather than dividend

- Minimal intervention or capital calls required

- Low fees

The problem though, is that you can’t access the S&P500 or QQQ unless it’s via an actively managed fund from Endowus. And that carries with it its own set of fees, which is not ideal.

So the next best thing would be a Singapore focused ETF, like the STI, a REIT ETF, or the Hang Seng Tech ETF.

All of which feature prominently in the top 5 ETFs bought by SRS Investors in Singapore.

So the list made a lot of sense to me.

The Gold ETF surprised me, I would have though gold has fallen out of favour with investors recently. But perhaps these are ultra-long term holdings, as a way to preserve purchasing power.

What is Supplementary Retirement Scheme (SRS)?

For those who are newer to SRS, the core concept is very simple.

You can top up up to S$15,300 a year into your SRS account, and any amount topped up is tax exempt.

The money can be used to invest in SRS permitted investments.

The catch is that if you withdraw before statutory retirement age (62), you need to pay (1) income tax on the money withdraw, and a (2) 5% penalty on top of that.

To give an example, if you withdraw $10,000 at age 40, when your income tax bracket is 15%.

Then you have to pay a penalty of 15% + 5% = 20% on the $10,000.

When to use SRS?

I wrote an article a while back on when to use SRS, so you can check it out for fuller thoughts.

Long story short – I think SRS makes sense if you:

- Have chargeable income of more than $80,000 (such that you’re paying 11.5% income tax on the incremental income)

- Don’t need the money in the near term (eg. to buy a house, fund children’s university education etc)

The strength of the SRS is that you save the tax upfront, and the amount you save on the tax will compound going forward.

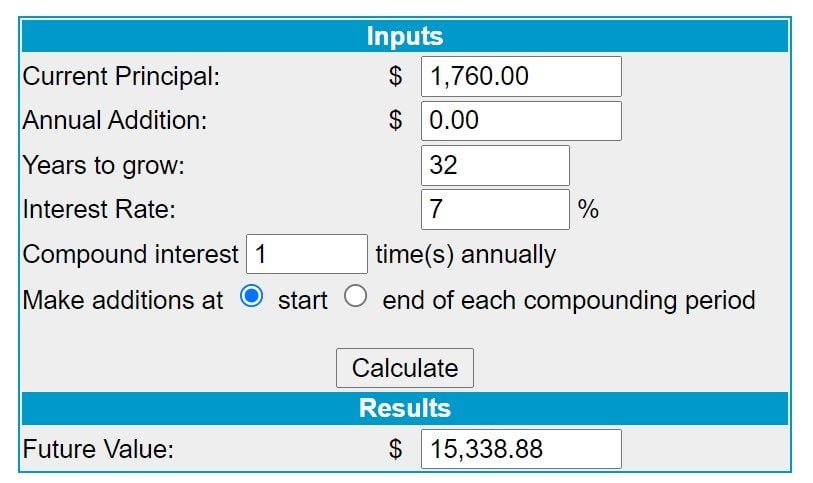

To illustrate – let’s say you top up $15,300 at age 30.

This saves you $1,760 on tax, assuming you’re in the 11.5% bracket.

Let’s say you can generate 7% annual returns on your SRS investments over the next 32 years, and withdraw it at statutory retirement of 62.

That $1,760 you saved on tax at age 30 is now worth $15,338 at age 62.

And that is just the value of what you save on tax alone.

At least, that’s how it’s supposed to work in theory.

In practice most people forget to invest the money, or they invest it poorly, and so on.

So actually just chucking it in an ETF and forgetting about it until retirement is a pretty decent option.

Don’t forget to top up $15,300 by 31 December

It’s that time of the year again, so if you want to use SRS don’t forget to top it up by 31 December 2021 to enjoy the tax benefits.

The max that you can top up is $15,300.

Top up $1 even if you’re not using SRS

Even if you don’t plan to use SRS, there are a lot of articles floating around that recommend you to just open an SRS account and top up $1.

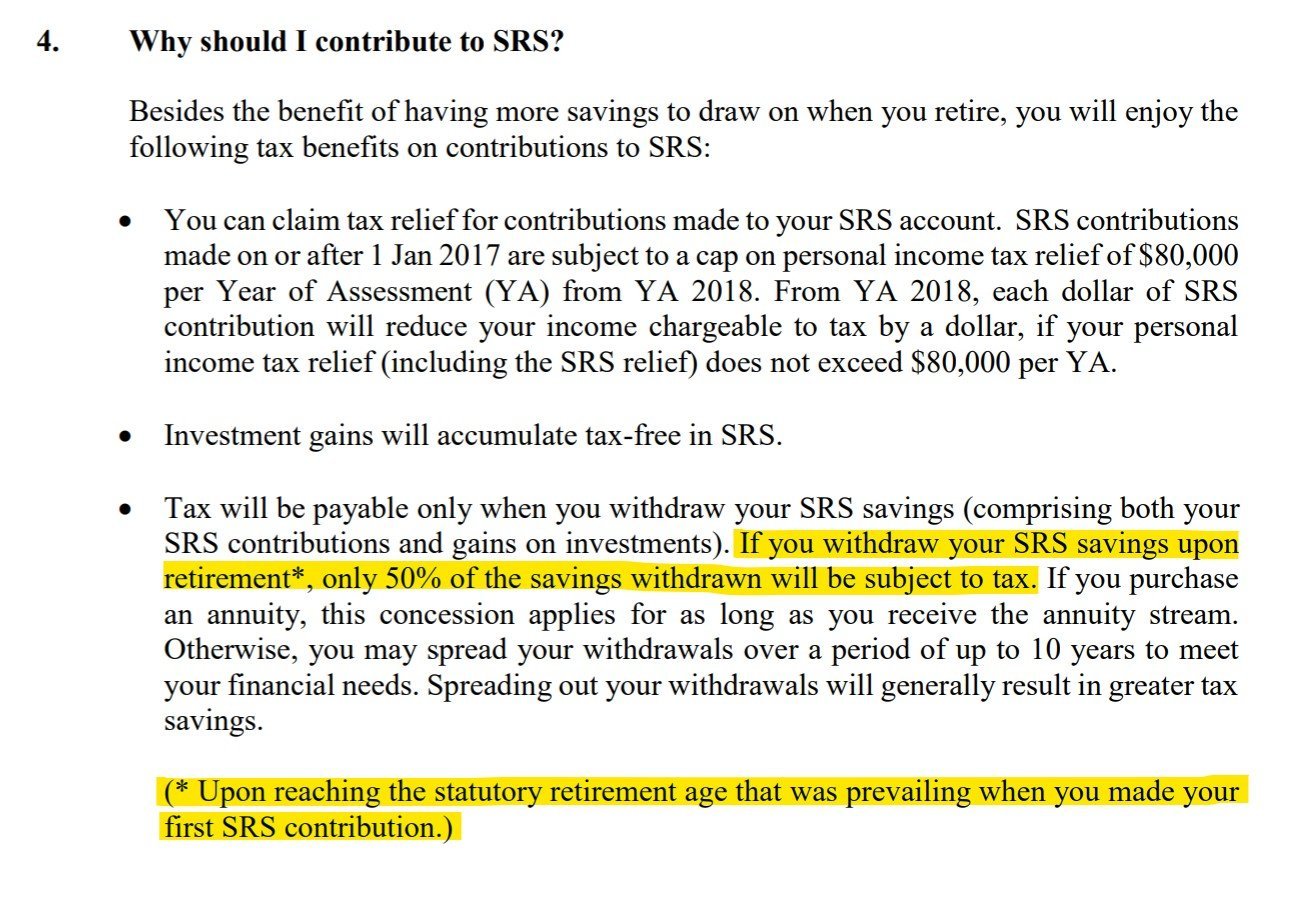

The reason why is because of this document from the Ministry of Finance:

The yellow highlighted words are interesting – because it suggests that the age you can withdraw your SRS savings penalty free is the statutory retirement age that was prevailing when you made your first SRS contribution.

In other words – If the Statutory Retirement Age changes going forward, you are protected as long as you already made your first SRS contribution prior to such change.

So if you top up your SRS today when the statutory retirement age is 62, you can withdraw your SRS penalty free at 62, even if the statutory retirement age changes down the road.

Now I don’t know how true this is because it’s possible that the drafting was an oversight and that the rules may change down the road. It’s not impossible.

But I mean c’mon, it’s $1.

You can open it online these days from any of the 3 local banks, and just chuck $1 in.

If it works, it works and that’s great. If it doesn’t work, you only lost a dollar and a few minutes of your time.

No brainer in my view.

BTW – Running a Big Promo for both Investment Masterclasses.

Keen to learn how to invest property in 2022? Check out the promo here!

As always, this article is written on 23 Dec 2021 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 1 free Apple share (worth $230) you’re new to MooMoo and fund $2700.

Get a Free Apple stock (worth S$230) when you open a new account with Tiger Brokers and fund $2000.

Special account opening bonus for Saxo Brokers too (drop email to saxo@financialhorse.com for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Can I put money in an srs if I’m older than 62?

No, the current age limit to contribute to SRS is 62.

Hi FH,

Thanks for sharing this information and viewpoint on SRS. You amazingly remove all my doubts related to SRS. Thanks for telling all the details about SRS.

Best Regards,

Emily Choo

Thanks! Appreciate the kind words!

Do I get that right – if given the choice between a direct investment into a SG ETF or – say an active VWRA equivalent on Endowus – you would pick the former?

Thanks!

Yes, but on the assumption that I would then use my non-SRS component of my portfolio to buy the cheap ETF version of VWRA. It’s a way of optimising fees holistically across the portfolio.