A couple months back, I wrote on article on the 3 Best Singapore REITs to buy in Singapore.

All 3 were retail/ office REITs, because I felt there was the most opportunity in that space.

Many of them are trading at 30% – 50% discount to book value, which I thought was not justified. At that kind of prices, as long as you stick with a good sponsor and good properties, it’s a ridiculous margin of safety, and very strong upside when COVID eventually comes under control.

BUT – Quite a few readers asked me for a list that would exclude retail / office buildings.

The thinking was that nobody knows how COVID-19 would play out. Who knows how many Robinsons will go under, and how many companies will have permanent flexi work from home (like DBS announced the past week).

Fair point.

Basics: COVID-Proof REITs

So in this article, I challenged myself to come up with 3 of the top COVID-proof REITs to buy in Singapore.

This means no shopping malls, no office buildings, and no hotels / serviced residences.

But Industrial (or logistics), healthcare, data centers – they’re all fair game.

A lower margin of safety for these REITs

For the record, I don’t necessarily think that these REITs are “safer”. They just offer a different risk profile.

Because the REITs in this category are perceived as “immune” to COVID, they have been bid up very strongly by investors.

Most are trading at huge premiums to book value, and low single digit yields.

If COVID takes a turn for the better, or interest rates start to tick up even slightly, we could see violent sell-offs in these COVID winners. We’ve seen that in the Tech/Pharma space the past 2 weeks, but we haven’t really seen it in real estate just yet.

Between an industrial REIT at 50% premium to book and 4% yield, and a retail REIT at 50% discount to book and 4% yield, the retail REIT just looks more attractive to me – as long as it’s a high quality real estate.

But I do get that every investor is different.

Some investors want a steady stream of income because of their risk profile (retirees). Some investors may need diversification because they’re already heavy on retail / office.

If that’s you, this list may come in handy.

BTW – we share commentary on the COVID crisis every weekend, so please sign up for our mailing list, its absolutely free.

It’s a weekly newsletter that goes out every Sunday, and rounds up the week’s posts so you never miss anything.

Don’t forget also to join our Telegram Channel!

[mailmunch-form id=”928667″]

Top 3 COVID-Proof REITs to buy in Singapore

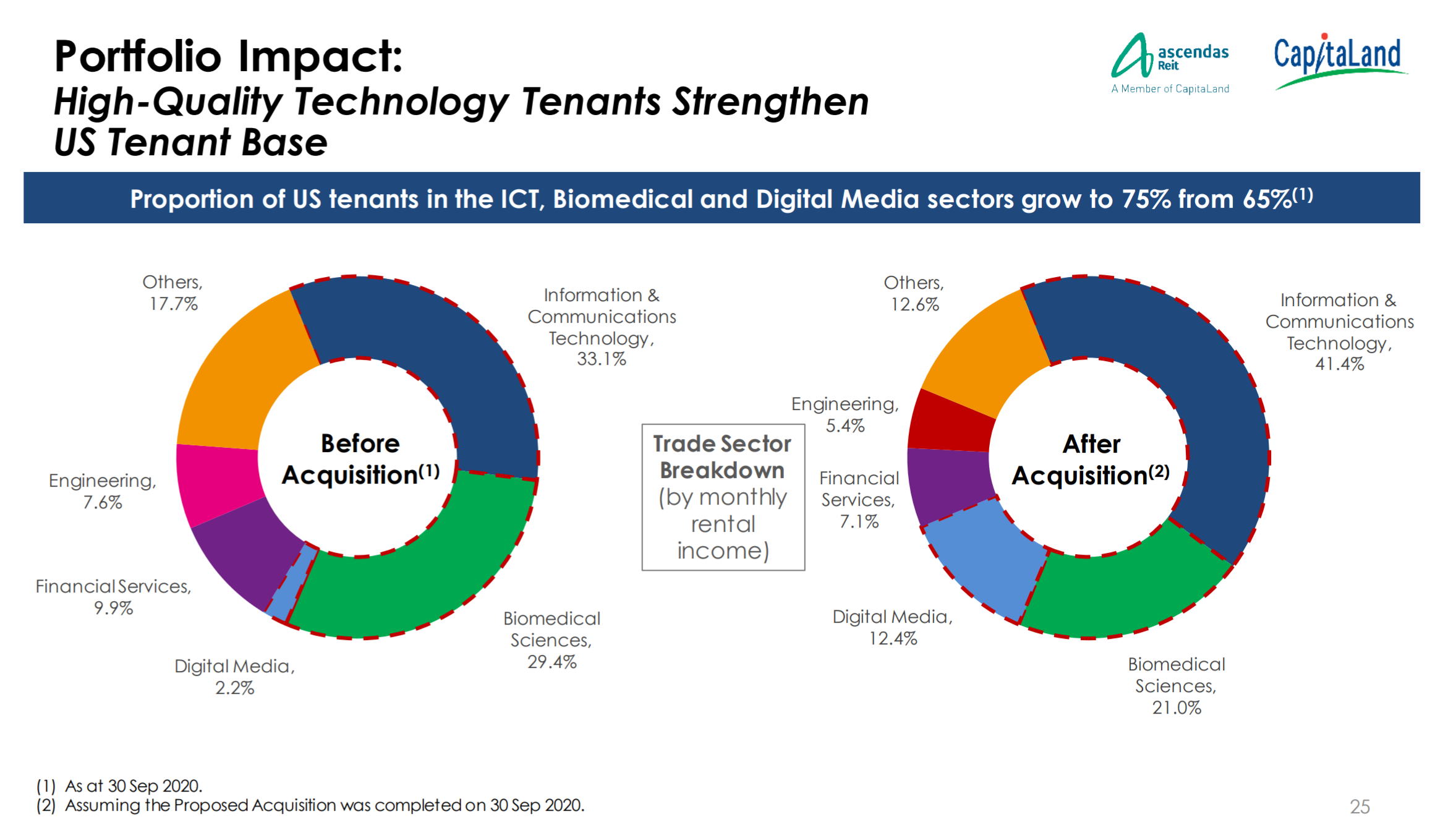

1. Ascendas REIT

Ascendas REIT has corrected very nicely from it’s high of $3.5.

They’ve been pretty aggressive with their acquisitions and fund raise recently, which could explain a bit of the sell off.

But ultimately, if you take a longer-term perspective and look through the short term noise, what you get is:

- A diversified industrial REIT

- With assets in Singapore, US, Australia, UK

- Backed by a very strong sponsor (CapitaLand)

As with most REITs on this list, Ascendas REIT is not cheap.

I’ve set out the valuations against comparable REITs below:

|

Ascendas REIT |

Mapletree Industrial Trust |

Mapletree Logistics Trust | |

|

Price/Book |

1.35x |

1.77x |

1.5x |

|

Yield (Trailing 12 months) |

4.8% |

4.0% |

4.1% |

Mapletree Industrial Trust has bigger exposure to data centers which explains the premium valuation.

And you could make an argument that Mapletree Logistics Trust, because of its property profile (logistics space) may experience higher rental reversions going forward.

But to be really honest, I think all 3 REITs in the table are probably about fairly valued. And all would be good choices.

One interesting thing about Ascendas REIT is that their latest business update showed a -16% decline in rental reversion for Singapore logistics.

This is concerning, because we don’t know if it was a one-off due to a particular tenant, or if it’s going to be a broader trend going forward.

My personal view is that this will depend greatly on COVID and on government support. If the government is going to continue supporting SMEs and companies in Singapore, and the COVID vaccine rolls out smoothly in 2021, all should be fine.

But I can’t rule out something going wrong along the way.

Everyone was long the reflation trade in Jan 2020, and look how well that turned out.

2. Elite Commercial Trust

Elite Commercial Trust is a very interesting small cap REIT that I covered during the IPO stage, so check out that article if you want a full writeup.

Basically, they hold a bunch of office buildings in the UK, which are long leased out to the UK government:

“A majority of the Properties’ lease agreements are due to expire in 2028, and certain lease agreements contain an option for the tenant to terminate in 2023.”

This turns Elite Commercial REIT into a very interesting fixed income proxy – where you get a fixed yield that is very stable, but little to no upside (or downside). It’s basically become like a bond.

The closest analogy in Singapore would be Parkway Life REIT with its 15 year master leases to Parkway Life Group. Or Netlink Trust where the underlying earnings are very stable due to the regulatory constraints on price and its monopoly status.

At the current price of 0.65 it’s a 7.5% yield, and 1.06x book value. IPO price was 0.68 so it’s come down slightly since then, but nothing to shout about.

Post-IPO earnings are generally in line with the forecasts, which is a good thing.

For the record though, Elite Commercial REIT is definitely on a different league in terms of risk. And by different league I mean higher.

It’s a small cap REIT without a strong blue chip Sponsor. Trading liquidity is incredibly thin. Substantial shareholders are mostly private wealth, which makes this vulnerable to a big sell-off like we saw in March. Market cap is only about $200 million, which is tiny in today’s market with the $10 billion REIT behemoths.

But it all comes back to risk reward.

If you want low risk, you can replace this with Parkway Life REIT, but that’s at a 3.3% yield. Or Keppel DC at 2.8% yield.

It’s just a low yield environment now, where even the risky stuff like this trades at a 7.5% yield.

For investors who want something safe to hold 10 years, this probably isn’t it. For investors who want something with high yield, relatively immune to COVID, and are prepared to actively monitor their investments, Elite Commercial REIT could be worth checking out.

3. Mapletree Industrial Trust

I actually considered many other REITs for this last spot. But most of them I felt were either too expensive, or the sponsor just didn’t appeal to me.

So I eventually settled on Mapletree Industrial Trust.

It’s definitely pricey, but you do get very strong exposure to high quality industrial space in Singapore, and data centers in the US.

At current price of $3.00, it’s at 1.7x book value and a 4% yield.

However if you factor in the 38% data exposure, and you use Keppel DC’s valuation of data centers (2.4x book value), it’s actually pretty fairly valued.

The better question here though, might be whether data centers are overvalued.

Everyone thinks data centers are the best thing since sliced bread, especially after COVID. But at the end of the day, all you’re buying is a building, that provides the power and cooling to house data centers. Mapletree, Keppel, Equinix etc, everyone can build that.

And once they realise how hot data centers are (which they have), they will.

It’s different from Google where the competitive advantage is the algorithm, which is incredibly hard to replicate.

With data centers, I really don’t see anything that justifies a 2.4x valuation and a 2.8% yield long term.

But from diversification perspective, I think it’s still wise to have some exposure, especially when it’s in the context of portfolio building.

Diversification is the only free lunch in investing.

We live in a Low Yield environment

If you buy all 3 REITs equally – Ascendas REIT, Elite Commercial REIT, Mapletree Industrial Trust, you get a blended yield of about 5.43%.

That’s pretty decent.

But if you wanted to dial the risk down and you replace Elite Commercial REIT with Parkway Life REIT (3.3% yield), the blended yield drops to 4.0%.

Which really illustrates the dilemma for investors today.

Everyone knows what the safe stuff and the risky stuff are. If you go with the safe stuff, you get a lower return. If you go with the risky stuff, you get a higher return, but of course there is a risk you lose your money.

So it really depends on your own risk profile. How much risk are you prepared to take on, for how much future return?

And ultimately that’s a question only you can answer for yourself.

For those who are keen, my full REIT portfolio is available on Patron, together with my asset allocation. REITs wise I’m definitely overweight Retail now because I see the greatest risk-reward there.

Very Honourable Mention: Parkway Life REIT

For the record, Parkway Life REIT almost made it onto this list.

If it did, it probably would have replaced Elite Commercial REIT.

It’s owns 3 of the most well-known private hospitals in Singapore, and a bunch of nursing homes in Japan.

The Singapore portfolio is master leased out to Parkway Life Group in a 15-year master lease, which ends in August 2022.

The Sponsor has the right to renew for another 15 years (they probably will – where would they move to?), but we won’t know the pricing, and unitholder’s approval will be required.

That’s something to watch for going forward.

Capitalisation rates range from 4.7% to 6.7% which are reasonable. These are leasehold properties though, ending in the 2070s, leaving about 50 years on the lease.

But at the end of the day, Parkway Life REIT trades at a 2.0x book value and 3.3% yield. Prices were more reasonable before they were included in the FTSE EPRA NAREIT Global Developed Index, which unfortunately drove prices up quite a bit.

At this kind of valuations, I think there is some risk here.

Like any fixed income proxy (like Netlink or Elite), if interest rates go up for any reason in the next 5 years, there could be a big sell-off in plays like this.

So I’m not comfortable owning Parkway Life REIT at this kind of prices.

But again, depends on the kind of investor you are. If all you care about it the yield stability, and you don’t mind if market prices tank 20%, then this could be something to consider.

Honourable Mention

Since we’re on the topic of COVID-proof REITs, I wanted to share my view on some other names that I looked at closely for this list.

Keppel DC REIT

It’s just really, really pricey at 2.4x book value and 2.8% yield.

If you compare it with another big data center REIT – Equinix (US listed), it trades at a 6x book value and 1.4% yield.

If you look at it this way Keppel DC can continue to go higher.

Personally for me, I’m not super bullish on data centers to such an extent.

Sure, you could get decent short term returns if COVID takes a turn for the worse, but as a long term investor, this doesn’t look attractive to me.

At this kind of prices, it feels like squeezing water out of a rock.

If you’re bullish on Keppel DC longer term, I would love to hear your thoughts though. What am I missing here?

Mapletree Logistics Trust

I bought Mapletree Logistics Trust in the low 1s earlier this year, and if it goes back there I would definitely buy it again.

It’s a very decent REIT, and I think you can replace Mapletree Industrial Trust or Ascendas REIT with this. That’s perfectly fine.

Cromwell REIT

At a 7.9% yield and 0.6x book value, Cromwell is pretty interesting with its European logistics exposure.

It’s definitely worth looking at if you have a high-risk appetite.

But for me, I thought Elite Commercial Trust’s long lease structure with the UK government gave it a more attractive risk-reward vs Cromwell REIT.

Closing Thoughts – What about the small cap Industrial REITs

I guess a big question after this article is why did I leave out all the small cap Industrial S-REITs.

You know, the ESR REIT, AIMS APAC REIT, Soilbuild etc.

My personal view is that those are not REITs I would want to hold as a long term, generational investor. With the kind of assets they hold, it is hard to see meaningful value growth longer term.

REIT investing is going the way it did in the US – consolidation. In this climate, you either become a giant (like the newly merged CICT), or you become ultra-niche (kinda like Parkway Life or Elite). There’s very little room for the in betweens.

If the US is any indication, the in betweens usually get acquired eventually, or they get privatized.

So for me, I probably would avoid that space.

But that said – they do offer very attractive 7% yields, that could be worth looking at if you’re using certain niche leverage style plays.

Love to hear your thoughts though. What do you think about my list!

BTW – If you’re looking to get diversified exposure to S-REITs, Syfe REIT+ is a great option worth considering, better than the REIT ETFs on the market (in my view). You get exposure to 20 of the largest S-REITs, and there is no minimum investment amount or minimum brokerage fees, which makes this a good option if you’re investing smaller amounts. Find out more here.

As always, this article is written on 20 Nov 2020 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Do like and follow our Facebook Page, or join the Telegram Channel. Never miss another post from Financial Horse!

Join our Facebook Group to continue the discussion, everyone is welcome!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

hi fh, i have been following your articles for a while now and i have found them to be pretty informative.

i have been considering MIT, but have held back because of its exposure to SMEs (i think almost half of its tenants are SMEs). do you think this is a valid concern and if the current price justifes the risk involved?

I think it’s probably about fairly valued, but I would prefer to wait for a better entry pice personally.

Hi FH,

just wondering, how you got the yield of 7.1% for elite commercial reit? their yield from 2020 was more like 2.95%

You will need to annualise the yield though. They haven’t paid out for the full year yet.

Hi FH, I am quite stuck in deciding my investment money between selecting dividend stocks and REITs. During disastrous times like Covid period, what would you think can weather through? I am looking at long term, wanting to generate passive income when Im old.

Interesting question – why do you need to pick between dividend stocks and REITs. Why not get both?

I would have thought the better question is how to select between dividend stocks/REITs on one hand, and growth stocks (eg. tech) on the other hand.

I think the days of buying 1 stock and holding that into retirement are over (assuming you’re just starting on your investment journey). The world is changing too quickly these days, and I think any portfolio will require constant management in the coming years. We’re living in a time of great change, and our investment portfolio should reflect that reality.