It’s been quite a while since we talked about dividend stocks on Financial Horse.

So that’s exactly what I wanted to do today.

Top 3 Dividend Stocks that I would consider buying in 2023 (as a Singapore Investor).

With a minimum dividend of 5.0%.

Let’s go!

Just to be clear – Nobody is saying to buy these stocks tomorrow… Macro risk is very elevated

Just to be absolutely clear.

Just because a dividend stock is on this list – doesn’t mean that I’m saying to go out and buy it tomorrow.

I’ve shared my macro views in other posts.

The long and short is that I think there is a good chance of a recession in the next 12 – 18 months.

And how dividend stocks perform in a recession, let’s just say not terribly well.

So view this more as a list of dividend stocks to keep on your watchlist.

To be bought at the right price over the next 12 – 18 months.

Top 3 Dividend Stocks to buy in 2023 – Minimum dividend yield of 5.0% (as a Singapore Investor in 2023)

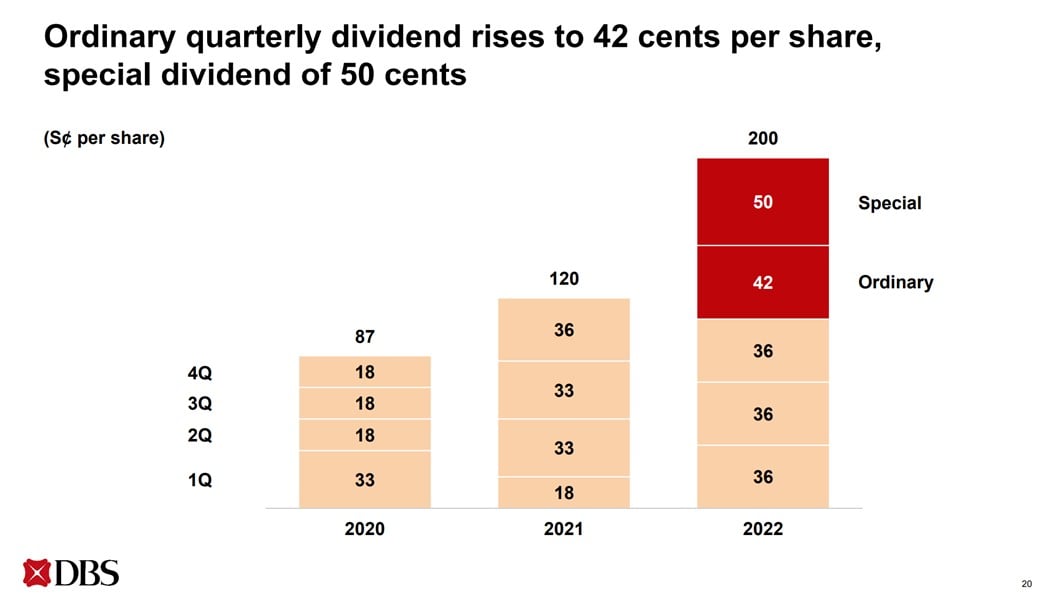

DBS Bank

Price: $32.32

Annualised Dividend Yield – 5.2% (using 42 cents ordinary dividend annualised, excluding special dividend).

Price / Book: 1.47x

DBS Bank needs no introduction.

Singapore’s largest and most ubiquitous bank.

Dividend Yield?

In Q4 2022 DBS just raised their quarterly dividend to 42 cents.

Annualised – that works out to a mind blowing 5.2% dividend yield.

Yes that’s exactly right, DBS Bank pays a higher dividend yield than a DBS savings account or T-Bills.

Risks with this Dividend Stock

I know that almost every Singaporean investor loves DBS Bank, so I’m not going to spend too much time talking about the pros – You guys already know them by heart by now.

Rather, I’m going to talk about the risks:

- Will the US banking problem get worse?

- Is DBS’s price too high given the possibility of a 2023/2024 recession?

Will the US banking problem get worse?

It’s fairly clear by now that the immediate fallout of the US bank failures has been contained.

But that doesn’t mean the problem has disappeared.

No… the problem has merely evolved.

Here’s Bridgewater:

The problem for the US banking system is not a bank run (which policy makers have already addressed with emergency liquidity) but rather that the repricing of deposits will put material pressure on bank profits and thus their ability and desire to make loans and buy bonds.

The aggregate hit to banks will range from modest to extreme depending on how fast deposits reprice, with many banks seeing significant profit declines and a portion of the system facing insolvency or zombification.

Basically – the immediate risk of bank runs has been solved via Fed emergency actions.

But the deeper underlying problem remains.

Banks have gotten complacent and come to rely on a decade of easy money, with a flood of deposits that they paid 0% interest rates on.

Well, now that market interest rates are at 4%+, depositors are taking out all that money.

Which means banks lose a key funding source (cheap deposits), which they need to replace with funding at market interest rates.

All while their loans are made at 2021 levels of low interest rates.

In plain English – your input costs go up, while your output price stays the same.

And that hits profitability.

So the next stage of this “banking crisis” will evolve into a profitability one, which is not over by any means.

More US banks may fail before this cycle is over.

I get that many of you will say that DBS as a Singapore bank does not face the same problems as US regional banks.

To be fair, I do agree with this to a certain extent.

But as the US economy weakens and more US banks fail, I don’t expect DBS to be completely immune either.

Is DBS’s price too high given the possibility of a 2023/2024 recession?

Which brings me to my next point.

Here’s the 20 year chart of DBS’s Price to book.

Banks are about as cyclical as it gets.

Average Price/Book is 1.3x.

Generally speaking – if you buy DBS Bank at 1 Standard Deviation below average P/B (1.0x).

And sell it at 1 Standard Deviation above average P/B (1.5x).

You generally do quite well.

Sure it doesn’t work perfectly and in some cases like 2007 it can go as high as 1.7x book value, but you get my point.

Is this Dividend Stock at cycle highs?

So with DBS already at 2018 cycle high valuations.

And with the risks for the global economy (and interest rates) towards the downside in the next 12 – 18 months.

Do you think the next 30% move in DBS’s share price is up or down?

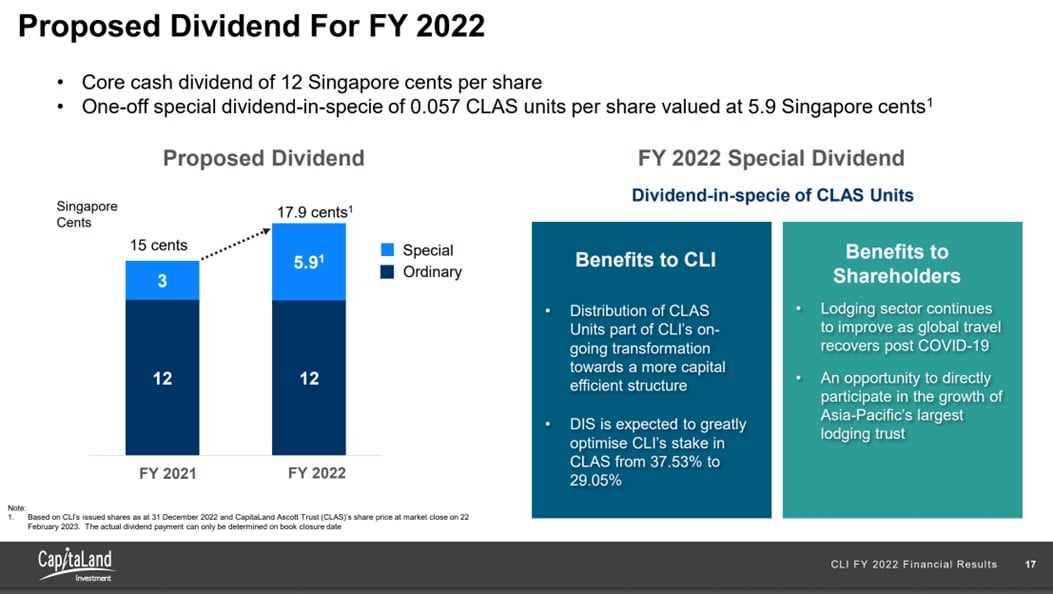

CapitaLand Investment

Price: $3.75

Annualised Dividend Yield: 4.77% (including special dividend), 3.2% excluding special dividend

Price / Book: 1.24x

Full disclosure that I was a long time CapitaLand Limited shareholder.

After the restructuring into CapitaLand Investment and the share price jumped to $3.5-3.7ish, I dumped the entirety of my stake in 2022:

But let me just put it out there that I’ve been very impressed by what current CEO Chee Koon has done with CapitaLand since taking over.

Real Estate developers tend to be boring, unsexy businesses – a value trap.

But Chee Koon – through a series of restructurings has managed to unlock a lot of value for shareholders and turned it into quite an exciting company.

From the merger with Ascendas, to the privatisation of the CapitaLand Development arm – this horse is truly impressed.

Market seems to think this way too, as CapitaLand Investment has consistently traded above book value since listing.

I’ve been impressed to the point where if I get an attractive entry point in the next cycle, I could see myself buying back a position.

What is the Dividend Yield?

If you include the special dividend, CapitaLand trades at a 4.77% dividend yield.

It drops to 3.2% if you exclude the special dividend though.

Risks with this Dividend Stock

As with DBS, let’s talk about the risks with CapitaLand:

- Incoming global real estate weakness

- Big China Real Estate Exposure

Incoming global real estate weakness

I’ve shared that I see global Commercial Real Estate (CRE) as one of the ground zeros of the coming crisis.

To me – CRE is one of those areas that levered up significantly the past decade, with valuations priced on the assumption that interest rates would stay at 0%.

Now that interest rates have gone higher, this is going to trigger a lot of pain.

Real estate cycles are as old as time itself, and there are only 2 ways this can play out:

- A sharp repricing (down)

- A prolonged period of pain

For now, I don’t necessarily see (1) playing out.

I see this crisis as quite different from 2008 because the banks are much sounder this cycle.

Rather, I think (2) is more likely to play out.

Some analysts out there are predicting a 40% peak to trough decline for US real estate prices (coincidentally the same number used in the Fed stress test).

If true, a lot more pain for real estate lies ahead.

The benefit of CapitaLand Investment over a REIT is that CapitaLand has a fee income business from real estate management.

Which technically speaking, should allow it to outperform REITs in a higher interest rate climate.

Big China (and Western) real estate exposure

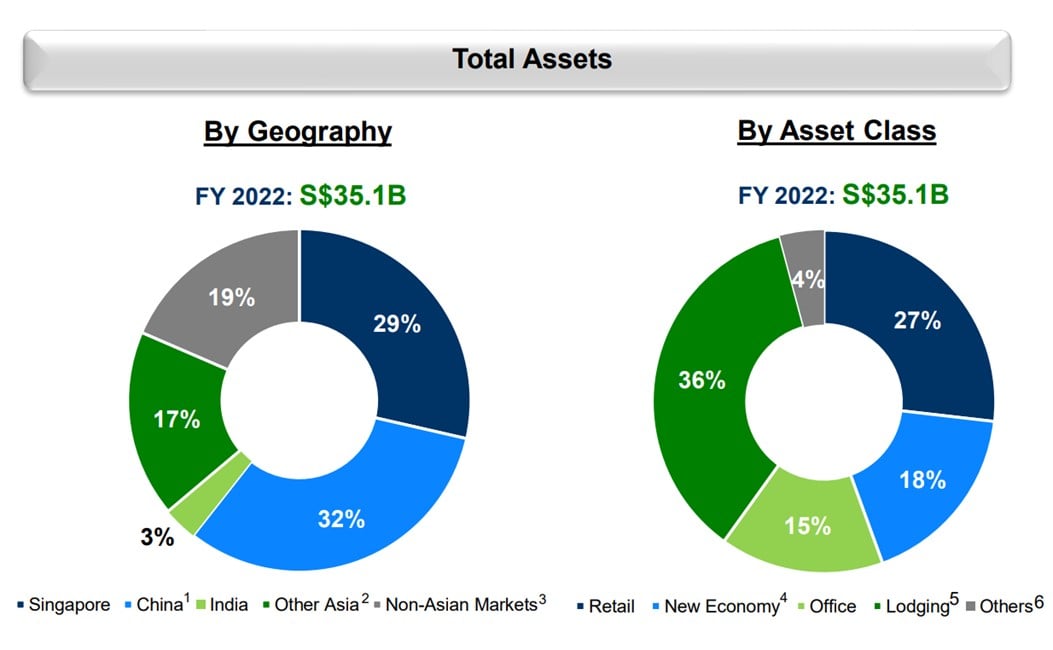

But I say *should*, because you should also note that CapitaLand has huge exposure to China real estate.

In fact almost 32% of its asset base is China real estate.

That’s even bigger than its Singapore real estate (29%).

I know many investors are not comfortable with China exposure, and think that China real estate is a big black hole.

I mean I don’t disagree with that view.

But at this point in the cycle – are you more worried about China real estate, or US/European real estate?

Funnily enough I might actually be more concerned with the latter.

And CapitaLand has almost 19% exposure to non-Asian real estate as well.

Sometimes that’s the problem with being too diversified.

As long as any part suffers, you suffer.

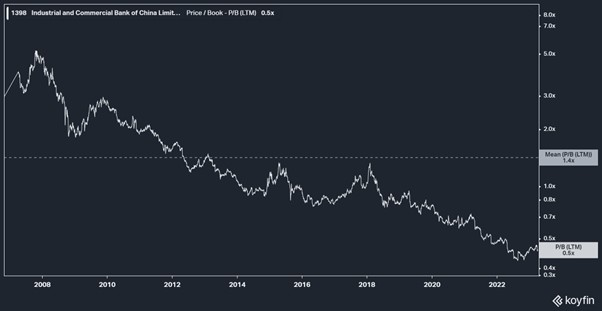

China Banks

ICBC

Price: $4.19 HKD

Annualised Dividend Yield: 8.1%

Price / Book: 0.5x

For the record, I know that CapitaLand’s dividend is only 4.77% and below the 5.0% dividend rule I set for this article.

So I decided to make up for it in the third name.

With a mind blowing 8.1% dividend yield – it is a China bank ICBC.

Here’s the ICBC long term chart, and frankly it doesn’t need to be ICBC, any of the Big 4 China banks work for this (BOC, CCB, ABC).

The thesis for ICBC is simple.

Don’t ask too many questions about what’s on ICBC’s books, because you won’t like the answer (nor will you get a straight answer frankly).

Don’t expect ICBC to be run like a JP Morgan, because this is China and the banks are an extension of the state (furthering state goals).

But you do get implicit support from the CCP, and you get to collect your 8.1% dividend each year.

Is that a deal you would take?

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Risks of this Dividend Stock

Risks – where do I even begin.

Remember how I talked about not asking too many questions about the loan book.

Here’s the 20 year Price/Book chart.

It is a Log Chart, so you can see how it’s gone from 5.0x book value post-listing to 0.5x book value today.

Most of these loans are real estate loans, that will probably never be able to be repaid.

So the 0.5x book value is masking a lot of these bad loans.

And that’s even before we talk about Xi Jinping and his plans for China.

Or geopolitical risk with the US.

A Taiwan war is not my base case this decade, but it’s also not something I can say is absolutely impossible.

If a Taiwan war plays out, what do you think happens to ICBC’s share price?

If ICBC gets cut off from SWIFT and the US banking network, can it survive?

So ICBC is not without risks, but that’s also why you can pick it up at a 8.1% dividend yield.

I leave it up to each investor to form their own views.

Whatever you decide, I would say that position sizing is important.

In this new era of geopolitical risk, you don’t want to be overexposed to any one country (including China).

Very Honourable Mention: Energy – Shell, Exxon Mobil

I actually really, really wanted to include an energy stock on this list.

But I couldn’t because all the big Oil majors have very inflated share prices, which means a low dividend yield:

- Exxon – 3.10% dividend yield

- Shell – 3.55% dividend yield

- Conoco Phillips – 5.00% dividend yield

Don’t forget the US listed shares will have a 30% dividend withholding tax.

Factor that in and energy looks like more of a capital gains play than a dividend play.

Sure you can get CNOOC which pays a 15% dividend (or China oil plays), but that brings in all the China related risks we talked about above.

So for that reason I left energy out of this list.

But let me just say that I see energy as forming a key part of my portfolio this decade, as I think we will enter a decade of higher structural inflation.

Patreons get access to my full portfolio and positioning (and stock / REIT watch with names I am keen to pick up). Check it out here if you are keen.

But… do we get a recession first?

That said, the short term 12 – 18 month outlook for energy is very, very murky.

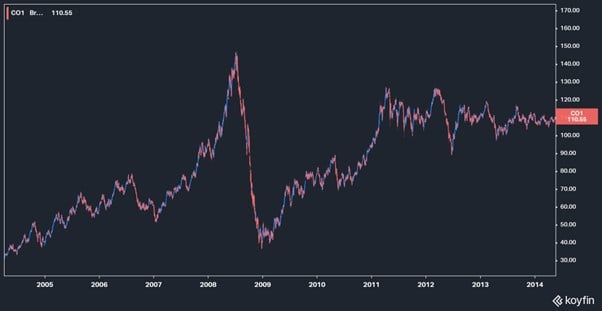

Here’s Brent Crude, you can see how it’s dropped sharply from post-Ukraine war highs of 120.

Here’s Brent Crude overlayed with XLE (energy stocks ETF).

It’s a chart crime I know.

And yes I know that this only looks at oil prices for immediate delivery, not those 2 – 3 years out.

But the point is clear.

Over the past 12 months, front end oil prices have dropped sharply.

While energy stock prices have kept powering higher.

With commodities you need to understand that a small supply-demand imbalance can have a drastic impact on prices.

Just look at what happened in 2015 and 2020 (with negative oil prices).

If we do get a recession, that will take out a fair bit of oil demand – then the question is whether OPEC will cut supply to match.

Here’s oil in 2008:

Oil went as high as $150 in the days leading up to the financial crisis.

And then absolutely cratered to $40.

There’s a reason why all the hedge funds are shorting oil these days.

Long story short – it’s not so straightforward with oil in the short term, so I would be more cautious.

I do see myself adding to oil (and probably most of the names above) in the next 12 – 18 months though.

Patreons will get access to my latest macro views and my buy/sell timings.

Closing Thoughts: Top 3 Dividend Stocks to buy in 2023 – Minimum dividend yield of 5.0% (as a Singapore Investor in 2023)

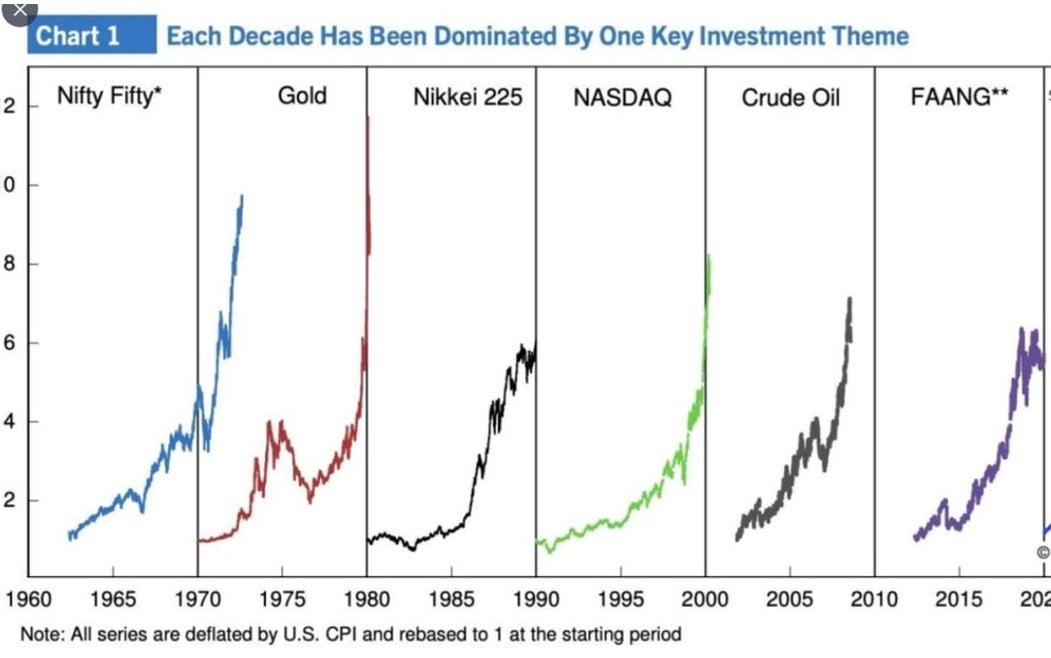

I wanted to leave you with this chart below.

Every decade has a theme.

In the 60s it was the Nifty Fifty (Disney, IBM etc).

In the 70s it was Gold.

In the 80s it was Japan’s Nikkei.

In the 90s it was NASDAQ with the Dot Com bubble.

In the 00s it was oil.

In the 10s it was FAANG.

But the lesson here – is that last decade’s winners never last forever.

They have a good run, and then the run ends there.

How will FAANG perform in a period of higher structural inflation and higher interest rates?

What will this decade’s investment theme be?

This article is written on 14 April 2023 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon, together with weekly premium macro updates like this one. You can access my full personal portfolio to check out how I am positioned as well.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

WeBull Account – Get up to USD 500 worth of fractional shares (expires 28 April)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares.

You just need to:

- Sign up here and fund any amount

- Maintain for 30 days

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Hi FH,

I noticed you are using Koyfin, is it the paying tier or the free one? Is it good compared to TIKR?

Thanks!

I have a paid subscription. A bit of a personal choice – but I like it to be honest.

Find that it helps my research quite a bit, instead of having to manually pull up the data.

Can’t compare to a Bloomberg of course, but the price point is completely different.

does it have good Singapore and HK stocks data as well? I’m thinking of subscribing because as you’ve said, the price point is really good. What about stockrover? You’ve got any experience with their platform and usefulness?

The SG and HK info isn’t as good as the US data, but still much better than free sources like Yahoo Finance. It was worth the signup for me at least.

Not tried Stock Rover unfortunately.

For oil and gas, it’s an unsexy business and the attention has moved elsewhere. Sadly, even if there is attention it’s usually negative (green > oil and gas)

Guess you would have to be a patient investor for the catalyst

Not sure if I agree with this one. I think O&G / commodities might be one of the key secular plays this decade.

It’s the short term that is uncertain.

A recession does wonders for demand-supply imbalance in the short term.

Hi

Interesting article. I would replace Capital land with CNOOC — higher dividend play, inflation hedge, correlate more with oil prices than China

On next decade play, emerging markets/ China is my pick

Interesting. Curious to hear how much of your portfolio you would allocate to China this decade.

I’m bullish China too (China banks and China oil names like CNOOC), but in this new era of geopolitical risk I think position sizing matters a lot.

How the US-China relationship plays out this decade has a very wide range of possibilities.

I have around 33% in HK stocks currently. I do not have fixed allocation; I just buy when it’s cheap.

Understand – appreciate the sharing. About 20 – 30% for me, does fluctuate depending on the macro conditions and valuations like you said.

Dear FH

Very nice piece

Fully agree

I hold all three in your original list with relatively small holdings in CLIM and ICBC ( plus equally small holdings in ABC CCB BOC BOCHK Bankcomm). I first bought these mainland PRC banks in early 2020 and added some later during the pandemic

The three years of uninterrupted dividends have been nice and in HKD that held up well! Your hypothesis is right – they are neither desirable additions but not to be sold off either! The state backing will ensure they survive but they may all be hit along with all asset classes if there is war

CLIM is once again something that will get hit badly if rates stay higher plus geopolitical issues. Hence, I will not add unless it is much lower, say 3.25 or lower

In fact, I will buy the SG blue chip REITS over CLIM, as they only have rates to contend mainly

The fed will pivot by second half and the forward looking markets have already priced this in with SG REITS running up

DBS OCBC UOB – All three are deserving a place in this list and their fundamentals are robust enough to tide over recession

These stocks are meant to be bought at drops and held through

I added all three over last three months and in fact will add more , if markets correct

I hold SHEL BP very long term and am hoping to add and build up my XLE stakes if at all oil drops again

To put it in a nutshell, I will add to all the above at opportunities except the China banks

Warm regards

Garudadri

Very interesting comment Garudadri, appreciated as always.

I too picked up some PRC banks quite a while back and added more last year. Like you said, share price has been a wild ride, but the dividend (fingers crossed) has been solid thus far!

I think they are a decent addition to a dividend portfolio, but with the right position sizing of course. Nobody can call for certain how the US-China relationship will play out.

I do agree the Feds will pivot eventually (possibly in the next 12 months). But I can’t shake this feeling that the market is missing that something big needs to happen first to force the Feds to pivot. What would this event be – and would it be positive for risk across the board?

Energy names like Shell I am holding long term as well. Picked them up in 2020 on the oil panic, and up very handsomely since. With LSE listed Shell there is no dividend withholding tax which is a very nice touch.

Hi FH, I’m not a Singapore investor but like to read your views. I’m Australian based and in the energy space here it’s very hard to look past thermal coal stocks that are paying very high dividend yields even at current thermal coal prices. No new mines are coming online globally pretty much while a lot of good deposits are at least temporarily out of play as in Russia. The share prices of the big 4 on ASX (Yal, WHC, NHC and Ter in order of production) are all elevated coming down from record highs as is the coal price, but the relationship between coal prices and share prices is out of whack. Worth a look if you are thinking to add energy to your portfolio. In the small cap O&G space there are also some good picks (OEL is mine), but also imagine there are better picks on other bourses that you are across and would be interested to see you post about one day.

Keep up the good work ????

Hi Nik, thanks for the support and the very interesting comment!

I have indeed been looking at coal recently as well for the reasons you mentioned.

Like you said, the mid term supply-demand picture looks attractive.

But never pulled the trigger though because I’m not as familiar with the supply side dyanmics as someone like you for example.

But thanks for raising this, will definitely look deeper into coal.

Everyone says a recession is coming.

Here’s out of the box thinking. In July 2022, Wilfred Ling CFA over at ifa.sg says on record to buy. NASDAQ is up over 20% since. Here’s why I think market may have bottomed in Oct.

1. Inflation is coming down.

2. Unemployment will slowly creep up, maybe not to recessionary levels, but enough to see wage pressure ease.

3. Big banks in Q1 reporting have no loan loss provisions.

4. Tech mass layoffs are good for margins.

5. You do well by buying at max pain, when people think you are stupid for buying. Because everyone thinks there is a severe recession coming.

Been thinking the exact same myself to be honest.

I think this is definitely possible, and cannot be ruled out.

But not so sure if this would be my base case though.

Question for you though – I assume you had bought in late 2022 based off this reasoning. Where we are in the cycle today – would you sell to lock in profits, or hold on the belief that what you shared above will continue to play out?

Depends on your cash level lah. I don’t know what % your core portfolio is. But I think only trimming tech. If you’re still working then you don’t need to sell that much to build war chest.

Nividia is a good hedge for China war, don’t you think? Semiconductors.

But NVIDIA semicon is manufactured by TSMC in Taiwan though. Not sure how much of a hedge it would be in a true China war.