So I was looking around for great Singapore dividend stocks to put my SRS funds in the past week. And I must say, when you google “Top Dividend Yield Stock Singapore” or “Best Dividend Yield Stocks Singapore”, some of the top search results are actually borderline negligent. Not going to name names, but many of them went on to rank dividend yield stocks in Singapore by their dividend yield, without taking a deeper look at the business model, the dividend payout ratio, the cash flows etc.

When I started Financial Horse, the goal was very simple. There was no good, high quality financial content out there catered for the Singapore investor, and I wanted to address that problem. So I knew I absolutely had to write an article on the Top Dividend Yield Stocks in Singapore. All 5 picks in this article are stocks / REITs that I would definitely consider buying for my own portfolio.

Basics: Dividend Yield stocks in Singapore

I am a huge fan of dividend yield stocks. You invest a sum of money, and the stock pays you a certain amount of money each year. Sometimes, the share price even goes up. What’s there not to like? To top it all off, dividend income in Singapore is not taxable at all (unlike the US), so I’ve always loved using Singapore for yield plays, and using US for capital gains plays (capital gains in the US is not taxable for Singapore investors). And with dividend stocks, as long as the dividend and cash flows stay intact, drops in share price are actually a fantastic opportunity to accumulate more if you know what you’re doing.

I like to think of dividend yield stocks as individuals. Imagine you have a fresh university graduate who earns S$3000. He spends S$1000 each month, leaving S$2000 in free cash. If he commits to pay you (the investor) S$3000 a month going forward, for quite obvious reasons its going to be a risky investment. Either he grows his future earnings incredibly quickly, or he is going to reduce the amount he pays you (dividend cut), or he is going to go into default (bankruptcy).

Imagine then you have a 45 year old CEO. He makes S$500,000 a month, including stock options. He spends S$100,000 a month, leaving S$400,000 in free cash. If he commits to pay you S$300,000 a month going forward, that’s a very different investment from the graduate above. Because while this guy has the cash flow to do it, the key considerations would be future growth (he’s already making S$6 million a year, how much more can it grow?) and sustainability (is he going to get fired?).

Selection Criteria

In selecting the top 5 dividend yield stocks / REITs in Singapore, I looked at a couple of criteria:

- Yield – For this article, I wanted to be a bit more aggressive with yield. I tried to look for companies with a minimum 5% yield, while balancing it with sustainability of the dividend yield.

- Dividend Payout Ratio – This measure the dividends paid out to shareholders against the company’s net income. The lower the better.

- Sustainability of net income – The ability of company to keep earning the same amount of income going forward.

- Future Growth – Will the company be able to grow earnings (and dividends) in the future?

SingTel

Okay. I know that I wrote an article in the past saying that I am not a fan of SingTel. But times have changed.

And probably the greatest change to me, had been the interest rate policy from the US Federal Reserve. For those who missed it, Jerome Powell basically came out to say that there were no more US rate hikes in 2019.

This has made SingTel attractive to me in 2 ways:

Forex weakness negated – A significant chunk of SingTel’s earnings come from outside of Singapore. An aggressive Fed translates into USD strength, which is bad for most Emerging Market (EM) currencies. SingTel suffered in 2018 partly because of EM currency weakness, which resulted in poor earnings when restated in SGD.

In 2019, I no longer see this as an issue. EM currencies are likely to have a much better year, so Forex weakness is no longer going to be a headwind for SingTel going forward.

With forex headwinds out of the way, you’re basically left with a psuedo ETF of Telco providers across asia, including India, Thailand, Australia etc. There’s definitely going to be the competition risk and technological risk, but then you also get the upside in share price gains if SingTel can execute property.

Alternatives are less attractive – When Mapletree Commercial Trust and SingTel were both trading at 5.8% yields, I would absolutely go for the former. But when Mapletree Commercial Trust is trading at a 4.9% yield and Singtel is at 5.6%, I think Singtel starts looking attractive.

The yield environment has shifted quite significantly in the past few months, and with plenty of blue chip REITs trading at sub 5% yields, SingTel starts looking pretty attractive.

SingTel is committed to a 75% payout ratio going forward which is sustainable, and trades at about a 5.6% yield today.

There are real risks arising from:

- Challenges to the business model – Long term, it is questionable whether telcos will still retain pricing power.

- Capex costs – 5G will eventually come into play and require significant Capex. Singtel also recently injected large funds into Bharti Airtel (India) to better compete in the Indian market.

- Increased domestic competition – Competition from other players in the various markets Singtel is in may erode profits.

It’s not the safest dividend stock on this list for sure. But all the risks above also mean that there could be large capital gains if SingTel were to pull it off. For example, if Bharti Airtel emerges as the winner in the Indian market, then SingTel share price is going to jump.

Investing is ultimately about risk-reward, and at current prices, I think SingTel looks interesting. You get decent growth, and a 5.6% dividend to boot.

Summary

Dividend Yield: 5.6%

Sustainability of dividend: Moderate

Future Growth: Good

Ascott Residence Trust

Ascott REIT trades at about a 6% dividend yield today (dividend payout ratios for REITs or business trusts are not meaningful because they pay out more than 90% of profit), at at about book value.

What I really like about Ascott REIT are two things:

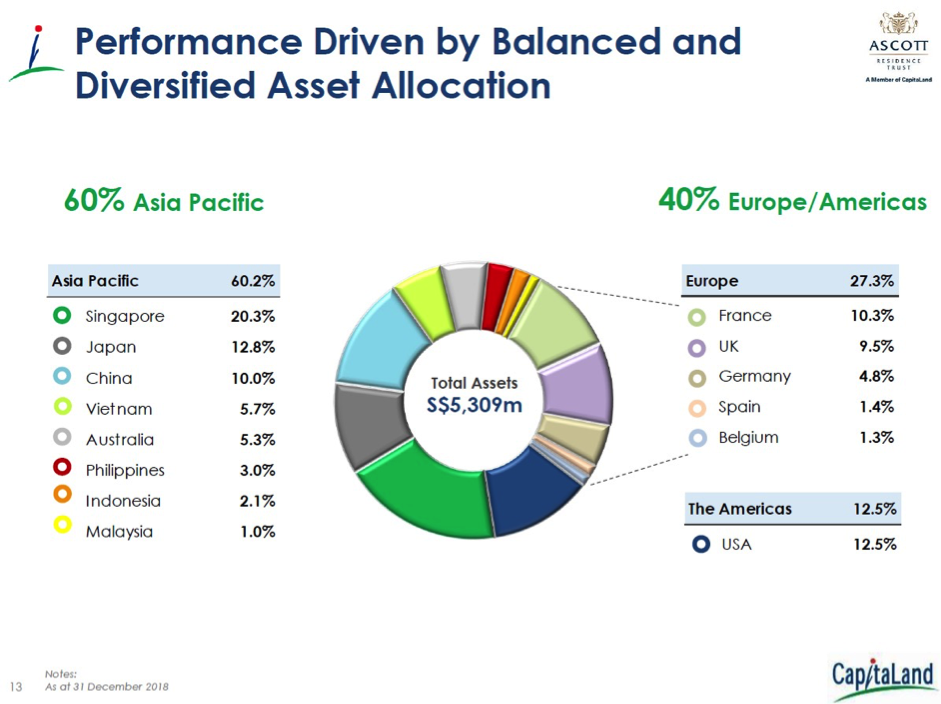

Broad Geographical Exposure to Hospitality – Ascott REIT gives you broad exposure to the hospitality asset class across the globe. Of course, there is some risk arising from increased competition from the Airbnb-style plays, and from the other hospitality providers going forward, but I personally believe that Ascott, with it’s CapitaLand backing, will find a way to cope with such competition.

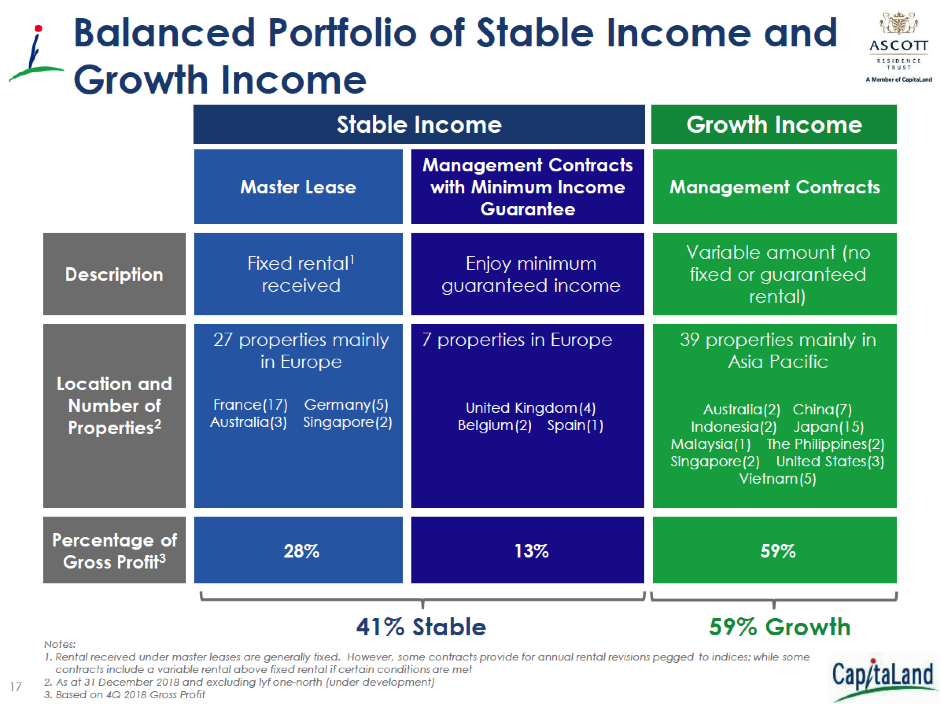

Spread of stable and growth income – Ascott REIT has a good mix of stable and growth income. The stable income comes from (1) Master Leases (where the operator pays the REIT a fixed amount of rent each month) and (2) Management Contracts with Minimum Income Guarantee (the operator guarantees a minimum income to the REIT each month), and the growth income comes from management contracts where the REIT enjoys the full upside. The split is about 41% stable income, and 59% growth income.

Of course, the growth wouldn’t be as great as one where it is 100% management contracts, but in terms of limiting the downside, I quite like this mix. If global hospitality takes a downturn from a global recession, the hit to earnings for Ascott REIT wouldn’t be as bad because of the stable income component.

One potential concern over this REIT is the acquisition of Ascendas by Ascott’s Sponsor, CapitaLand. Ascendas Hospitality Trust and Ascott Residence Trust have overlapping investment mandates, and the official note from the CEO is that they may look to either change the investment mandate, merge the two, or sell one. So until that is resolved, expect some uncertainty over the future of this REIT.

But again, when you’re collecting 6% a year, can’t really complain too much!

Summary

Dividend Yield: 6.0%

Sustainability of dividend: Moderate

Future Growth: Moderate

Mapletree Logistics Trust

Mapletree Logistics Trust has had a huge runup in unit price the past year, from 1.2 to about 1.44 now. Some of that is due to the macro environment, but a good part of it is also their ability to grow earnings and acquire high quality logistics properties.

What I really like about this REIT, is that it gives you broad exposure to the Asian logistics market from a real estate perspective. Logistics demand across Asia is going to explode in the coming years as Asia develops further and eCommerce grows, so I think the opportunity here is massive.

Unfortunately because of the runup, it’s trading at a 5.45% yield now, and a 15% premium to book, which is slightly expensive. From a longer term perspective though, I still really like this REIT.

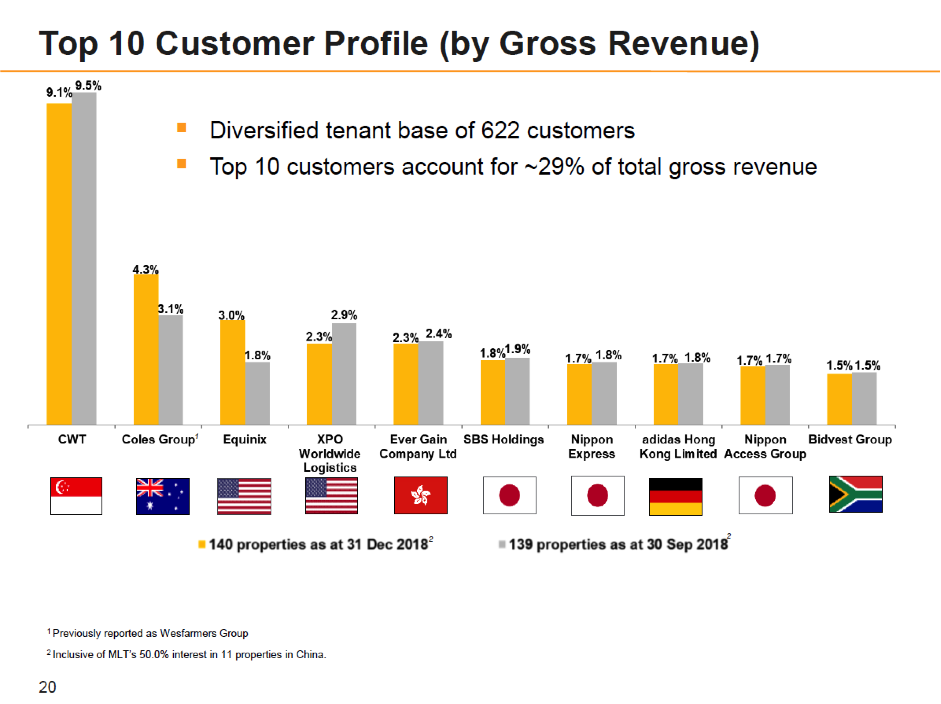

There was a slight issue with one of its big tenants CWT, who recently defaulted on certain repayments. CWT accounts for about 9.5% of Mapletree Logistic’s income, so if CWT defaults, that could be bad news for the REIT.

Anyway Mapletree Logistics Trust came out to issue an announcement to say that they have 6 months rental deposit from CWT, and that CWT hasn’t defaulted on any rental obligations so far. The latest news has also been that CWT has managed to fully redeem its upcoming bond redemption.

In any case, given the high quality nature of the assets held by Mapletree Logistics Trust, I think any selloff from this CWT saga could present a good buying opportunity. I for one, would be adding heavily if this trades at a high 5.x% yield.

Summary

Dividend Yield: 5.45%

Sustainability of dividend: Moderate

Future Growth: Good

Frasers Commercial Trust

To be really honest, I’m not a huge fan of the assets held by Frasers Commercial Trust. They’re just not the best in class kind of assets that Mapletree Commercial Trust has. I’m also not a huge fan of the big Australian exposure, since the Australian economy may go through some weakeness (possibly a mild recession) in the coming years.

But this REIT makes up for it with a whopping 6.5% dividend yield, at a 7% discount to book value, and a low 28% gearing. Even if it takes a slight hit in earnings, you’re probably still looking at a low 6% yield, which is nothing to be sniffed at.

They’ve also done a fair bit of AEI on both of their Singapore assets to boost earnings, and it seems to be working out well.

As a portfolio diversifier, and a way to juice the yield, I think Frasers Commercial Trust could be a great choice.

Summary

Dividend Yield: 6.5%

Sustainability of dividend: Moderate

Future Growth: Poor

Netlink Trust

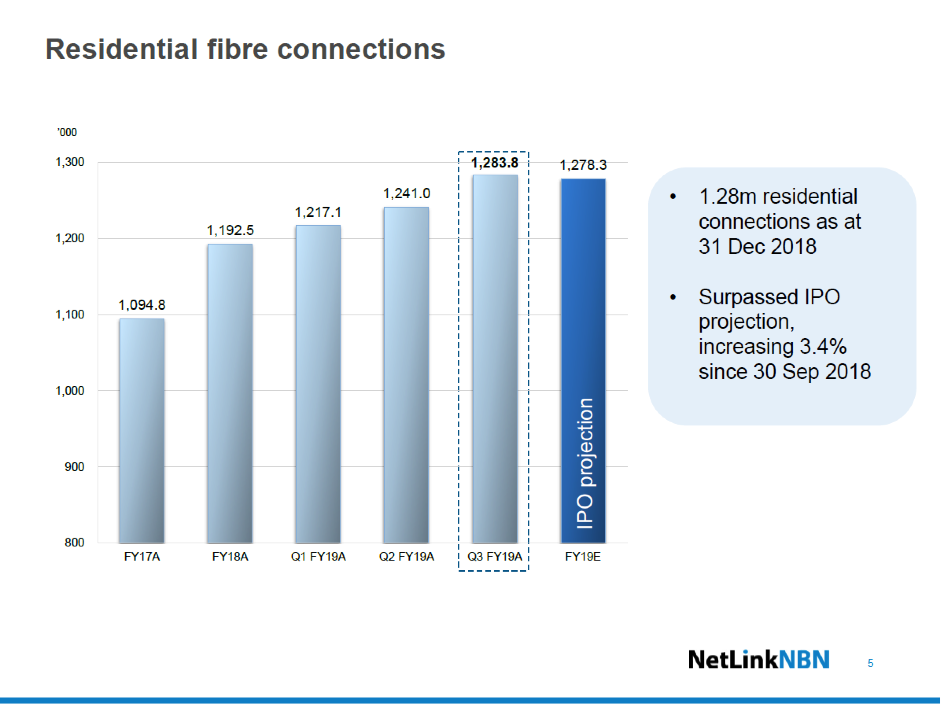

I really like Netlink Trust. They own a bulk of the fibre connections in Singapore. Every time you use a fibre connection at home, or you use it for a business, you’re probably paying Netlink a small fee. And no other player even comes close to matching Netlink Trust’s extensive fibre connection in Singapore, nor are they likely to, given the huge upfront cost required to build such a connection.

Netlink Trust reported a 2.44 cents dividend for the second half of FY2018, which works out to be about a 5.8% dividend yield. That’s really attractive given the monopoly status of Netlink.

Growth numbers are actually looking pretty decent as well – outpacing the IPO forecasts, so there could be more upside in here. Ultimately though, because almost all Singapore households will eventually be on Fibre connections, the longer term growth will need to come from population growth and new households. I still believe that the longer term vision for Singapore is to hit a 10 million population, so if we do, there’s a lot of room for Netlink Trust to grow.

The biggest tail risk would be technological disruption. However, I just don’t see any competition to fibre networks on the horizon, at least for residential and business use. No one is going to use 5G for unlimited video streaming at home, the costs would be prohibitive.

Capex costs is another big one, because if the fibre connections degrade, replacing them is going to be huge time and cost, given that most of these fibre networks are buried underground. It’s been manageable so far, and while the accounting life of the fibre is 25 years, Netlink trust themselves expect the fibre to last far longer than 25 years. I’m not an engineer so I can’t comment on how true this is, so if any reader out there has industry knowledge, would love to hear from you!

Summary

Dividend Yield: 5.8%

Sustainability of dividend: Good

Future Growth: Good

Closing Thoughts

And there you have it! My top 5 dividend yield stocks / REITs in Singapore to buy right now. I have some spare funds in SRS that I’m looking to deploy, so I’ll probably pick from one of the 5 above in the coming weeks.

Whether you like this or not, do share your thoughts in the comments section below!

Please also note that this article is based on prices and facts as at 18 April 2019. I can’t rule out the possibility that facts may change in the coming weeks and months that would affect the analysis above. If that happens, I may not update this article, but I’ll probably update my thoughts on the FH Stock Watch, so do consider signing up if you’re keen. It basically functions as my own personal stock watch, so I update it as and when I have new ideas for stocks I am interested in, and when situations change such that existing stocks are no longer attractive.

Happy Easter Weekend to all readers!

Till next time, Financial Horse, signing out!

Enjoyed this article? Do consider supporting the site as a Patron and receive exclusive content. Big shoutout to all Patrons for their generous support, and for helping to keep this site going!

Like our Facebook Page and join the Facebook Group to continue the discussion! Do also join our private Telegram Group for a friendly chat on any investing related!

Dear FH, your articles and insights have been very helpful. I would like to seek your opinion if it’s a good time to buy Netlink Trust now just for the stable dividend payout? I understand that the price is not exactly low now. Thank you for taking time to reply.

Hi! Yeah I get what you mean. The way I see it though, is that it really depends on your investment horizon. If you’re a long term investor (eg 5 to 10 years), Netlink is at about a 5.9% yield now which is fantastic given the economic moat and future growth runway.

Short term though, it’s hard to say, because of the volatility from the trade war, there’s no way of saying for certain how stocks will trade.

Cheers!

Dear FH, thank you for your objective feedback. I appreciate it. Have loaded some for long term growth after reviewing. Thanks!

No problem at all, glad that it was helpful! I bought some netlink trust recently as well. 😉

Dear FH, , I m a new investor. All these stocks are at their 1yr high. Is it your

Haha your question seems to have got cut off at the end unfortunately. 🙁

Dear FH, when should be the right time to buy into these stocks? What about CMT? should it be considered as a good dividend yielding stock as well?

can you give your summary on CMT in terms of :

Dividend Yield:

Sustainability of dividend:

Future Growth:

Timing is always tricky, and not something I get right myself all the time. My advice is to look at your own objectives, and decide whether you’re a short term or long term investor. If you’re long term you should be happy when prices drop since you have more opportunities to buy in, if you’re short term… well then you need to have stop losses in place and a good trading strategy.

CMT is pretty expensive right now, so there could be a real risk of capital loss at this prices. My take:

Dividend Yield: Low

Sustainability of dividend: Good

Future Growth: Medium

Hi,

What’s the sudden demand for Singtel? Due to 5G? I’m rather skeptical investing in our local telecom as they have struggled with profits & may have lost local support in the past few years, may be due to their nature of the business.

That aside, Could you advice why MLT & not north asia trust or MIT? North asia has better dividends & is cheaper than MLT

Dear FH, is there a particular period (s) where most sgx stocks would pay out dividends? Wondering when I can expect to receive income from dividend paying stocks. Thanks!

They usually tend to be after their AGMs. So it will be around May-June for those companies with a Dec year end, and sept for those with a March year end. REIT are usually either semi annual or quarterly distributions.

Cheers!

Hi FH,

I’m at the stage wondering if to take profit for Singtel or to wait for ex-div date. Volume seems to be dipping.. would like to know your view on this. Thanks lots!

Ascott Residence seems to be paying dividend by returning capital and hence yield sustainability may be questionable. Note that the latest 2Q19 DPU of 3.431 cents consist of 1.888 cents of capital distribution(not capital gain). I am unable to find any basis of the capital distribution which unlike other Reits distribute only capital gains. It seems like it is simply return capital to keep dividend more stable and therefore its sustainability is worrying. Ascott Residence NTA and DPU have been declining from year 2014 to 2018 – NTA from $1.37 to $1.22 per share and DPU from 8.2 to 7.16 cents/share. Am I missing something?

I believe there was a sale of their assets recently, so some of the gains was returned in the form of yield. If you check the underlying cash flow, I believe it’s still fine.

Hi FH; Ascott Residence seem to be boosting its dividend by using capital distribution and hence its dividend yield sustainability may be questionable. Its latest 2Q2019 DPU of 3.431 cents consist of 1.888 cents of capital distribution(not capital gain). I am unable to find any basis of the capital distribution which unlike other Reits returning only capital gains. It seems like Ascott Residence simply return capital and therefore is worrying especially when looking at the declining trend of NTA and DPU over 2014 to 2018 in its annual report: NTA decrease from $1.37 to $1.22 per share; DPU decrease from 8.2 to 7.16 cents. I am not sure if I missed anything?

Good analysis, thank you.

Nobody can predict the future. Do your homework well, decide n take action. That is investment, and accept that there will be gains and losses.

I have 3 of your top 5 dividend recommendations and with big positions, and 1 of your recommendations on radar. Given the near zero interest rate environment we are likely to re-enter again, your analysis is sound.

Thanks for sharing your thoughts, and glad that you liked this! I too agree that the coming months will be very interesting, let’s see where this takes us. 🙂