I know what you guys are thinking. Financial Horse has gone nuts. REITs are the most overvalued they have been this cycle, and he is writing about what REITs to buy?

And to be fair, I absolutely get that. I think the big, blue chip REITs like those from CapitaLand, Mapletree and Frasers etc are looking really expensive now. I also get that the recent economic data is looking very weak, and that barring drastic measures from global central banks or government, we’ll probably see an economic slowdown in the coming quarters.

So with that in mind, here are 2 ground rules to give some context to this article:

Economic Data is Weak – The recent June PMI data is looking really weak across the globe. In fact, if you trace it back, it looks a lot like the economy may have peaked in Dec 2018 / Jan 2019. And the rise in asset prices since then, could be mainly due to rising expectations of easing monetary policy (ie. Interest rate cuts).

With the G20 “trade truce”, it’s also clear that the current round of tariffs are not going away anytime soon. All that was agreed to was to return to the negotiating table. Given the complexity of such a deal, it’ll take probably around 6 months optimistically to negotiate a new deal, so it’s likely to be done only by end of the year. That’s a lot more time for the tariffs to take their toll on the global economy.

But financial markets are like life. Nothing is set in stone. If central banks start easing monetary policy drastically, or governments unleash a new fiscal stimulus package, all that can change overnight. So this article is still important to understand the options available to us, in the event that things change drastically.

High Yield REITs only – When I first wrote the Top REITs article back in Sep 2018, MCT was trading at 10% premium to book, at a 5.5% yield. Would I buy MCT again at that price right now? Of course I would.

But things have changed a lot since then. MCT is now at a 4.4% yield and a 30% premium to book. Would I buy MCT at this price? Well, I’m going to think twice.

But we have to take the markets as they are, not as we want them to be. So the original rules I set for myself for REIT picking still stand, namely:

- Minimum Yield of 5.5% for new REIT purchases

- Not more than a 15% premium to book value

Which basically rules out most of the bluechip REITs from this list.

What you do need to know though, is that because the yield environment has deteriorated across the globe, to find REITs that fulfil these criteria we need to move further out on the yield spread. So the risk premium you are taking on goes up.

But while the REITs on this list are slightly riskier, I generally selected only those REITs with what I find to be an attractive risk-reward.

With that in mind, here is my list of top 5 High Yield REITs in Singapore to buy right now (July 2019 Edition)! Keyword being High Yield. Please also note the disclaimer below:

The content here is for informational purposes only and should NOT be taken as legal, business, tax, or investment advice. It does NOT constitute an offer or solicitation to purchase any investment or a recommendation to buy or sell a security. In fact, the content is not directed to any investor or potential investor and may not be used to evaluate or make any investment. If you are in doubt as to the action you should take, please consult your lawyer, stockbroker or financial advisor.

1. Ascott Residence Trust

Unless you were living under a rock a past week, you probably heard about the Ascott REIT acquisition of Ascendas Hospitality Trust. As an Ascott Unitholder, I really like this deal because:

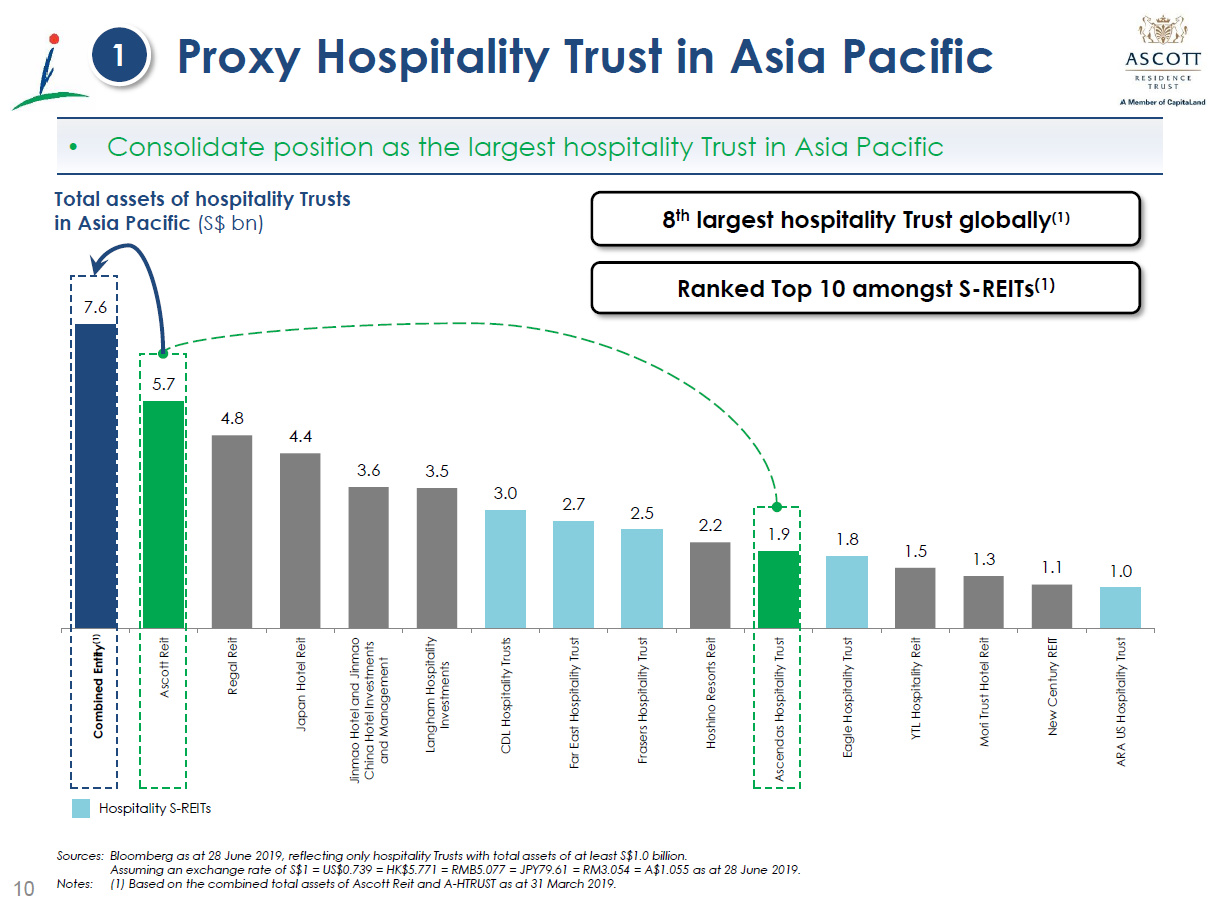

- Market Cap – I’m a sucker for size and scale. In this modern age, I think if you’re in real estate, you need to be big to compete. This acquisition consolidates Ascott REIT’s position as the largest hospitality trust in Asia Pacific. This helps it attract investments from the big institutional funds and index funds, which have minimum market cap and liquidity requirements.

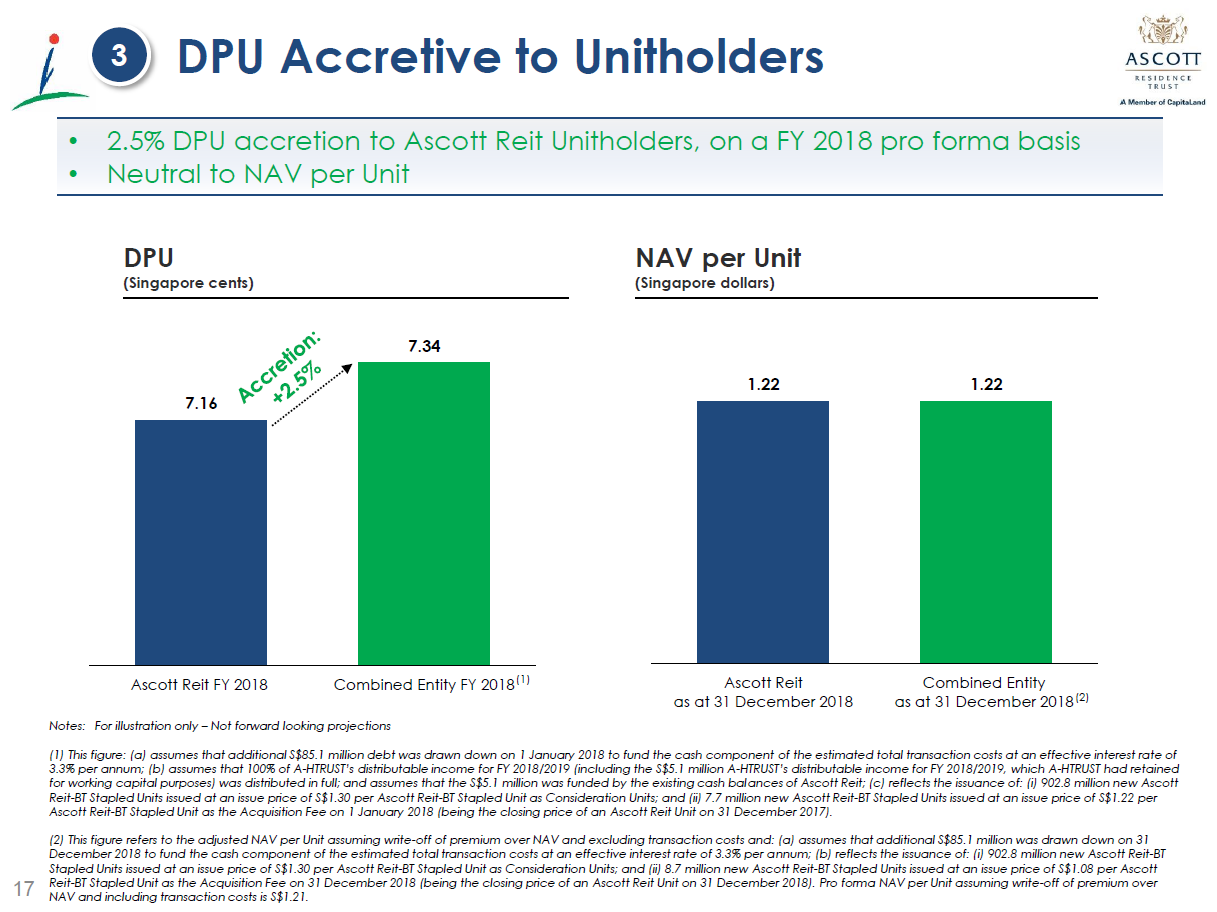

- Acquisition Price is decent – I think the price paid is pretty decent as well, it’s very nicely DPU accretive for unitholders, with no dilution to NAV.

If you buy Ascott REIT right now, you’re buying in at a 5.6% forward yield (2.79% yield spread), and a mere 7% premium to book. In exchange, you get a highly diversified hospitality portfolio spread across multiple countries in Asia, Europe and US.

As with hospitality plays, you always want some fixed income component in the leases because the industry is highly cyclical. Ascott doesn’t disappoint, with about 46% of its leases being fixed in nature. This provides some protection against the downside in the event the global economic slowdown worsens drastically.

Summary:

P/B = 1.07

Yield = 5.6%

Based on: Price = 1.31, NAV (pro-forma post acquisition) is 1.22, DPU (pro-forma post acquisition) is 7.34

2. ESR REIT

I thought long and hard before including ESR REIT on this list. I see ESR REIT as being riskier than usual blue chip Mapletree/CapitaLand REITs we usually talk about, so please don’t blindly buy this REIT without knowing what you’re getting into.

But this REIT does have its plus points too. It’s a pure play Singapore Industrial/Logistics play, trading at a 14% premium to book, and a very nice 7.5% yield. In other words, it’s kinda like an Ascendas REIT, at a much cheaper price (and different assets).

It’s Sponsor, e-Shang Redwood, is backed by the PE firm Warburg Pincus. This gives the Sponsor a nice supply of dry powder going forward. Real Estate is all about having a sound financial backing, and going into an economic slowdown, this is one point that I really like.

Unfortunately, this also means they’re very aggressive in terms of acquisitions. They recently just bought over Viva Industrial Trust, and going forward, we can probably expect more acquisitions. That’s not necessarily a good thing for a REIT, because you don’t want to be constantly coughing up money for equity offerings unless the REIT is buying an amazing asset. Case in point, ESR REIT just did a private placement at an 8.3% discount to market price.

So while I’ve included ESR REIT on this list because I like its yield, it may be a riskier (compared to stuff like MCT/CMT) investment with the possibility of more equity fund raisings going forward. On the safer side, there will be REITs like Frasers Commercial Trust or Frasers Logistics and Investment Trust. But of course, those guys are trading at a 5.6% yield, so you know, can’t have your cake and eat it.

It’s really about risk-reward here, and I think because of the huge runup in prices for the blue chip REITs, ESR REIT marginally passes the test for me.

Summary:

P/B = 1.14

Yield = 7.5%

Based on: Price = 0.535, NAV is 0.468, DPU annualised is 4.028

3. IREIT

If ESR REIT is the popular guy at a party who wants to get all the girls, then IREIT is the guy who is completely comfortable with what he has.

This REIT has only done 1 acquisition since it’s IPO back in 2014, which is pretty much unheard of these days.

It depends on how you see it, but as a unitholder, I definitely don’t think that’s a bad thing. I think scale only really matters if you can grow to the size of S$7 billion plus market cap, at which point you start getting noticed by the big institutional investors.

If you can’t then you may just be growing for the sake of growing. And don’t forget that each transaction incurs hefty acquisition and transaction related fees, that are paid for by the REIT and coming out of DPU.

All that talk about growing to diversify is overrated as well, because as a unitholder I can simply just buy another REIT to get the diversification I need in my portfolio.

So when you’re IREIT’s size ($490 million market cap), and realistically there’s no way to get scale without a massive acquisition and huge liquidity injection, I’m perfectly happy for the REIT to remain small, as long as they keep paying me my distributions. And at a 7.3% annualised yield, I’m a pretty happy unitholder.

The assets are German assets, with long term leases already locked in (91% of leases are only due for renewal in FY2022 and beyond). Germany is attractive these days because going forward I expect the European Central Bank under the new Christine Largarde to ease monetary policy aggressively. this means German Bund Yield are going to become even more negative than they are now (their 10 year bund yields are now –0.4%, that negative sign is not a typo btw). For a REIT with German assets borrowing in euros in Germany, that’s a great thing to have.

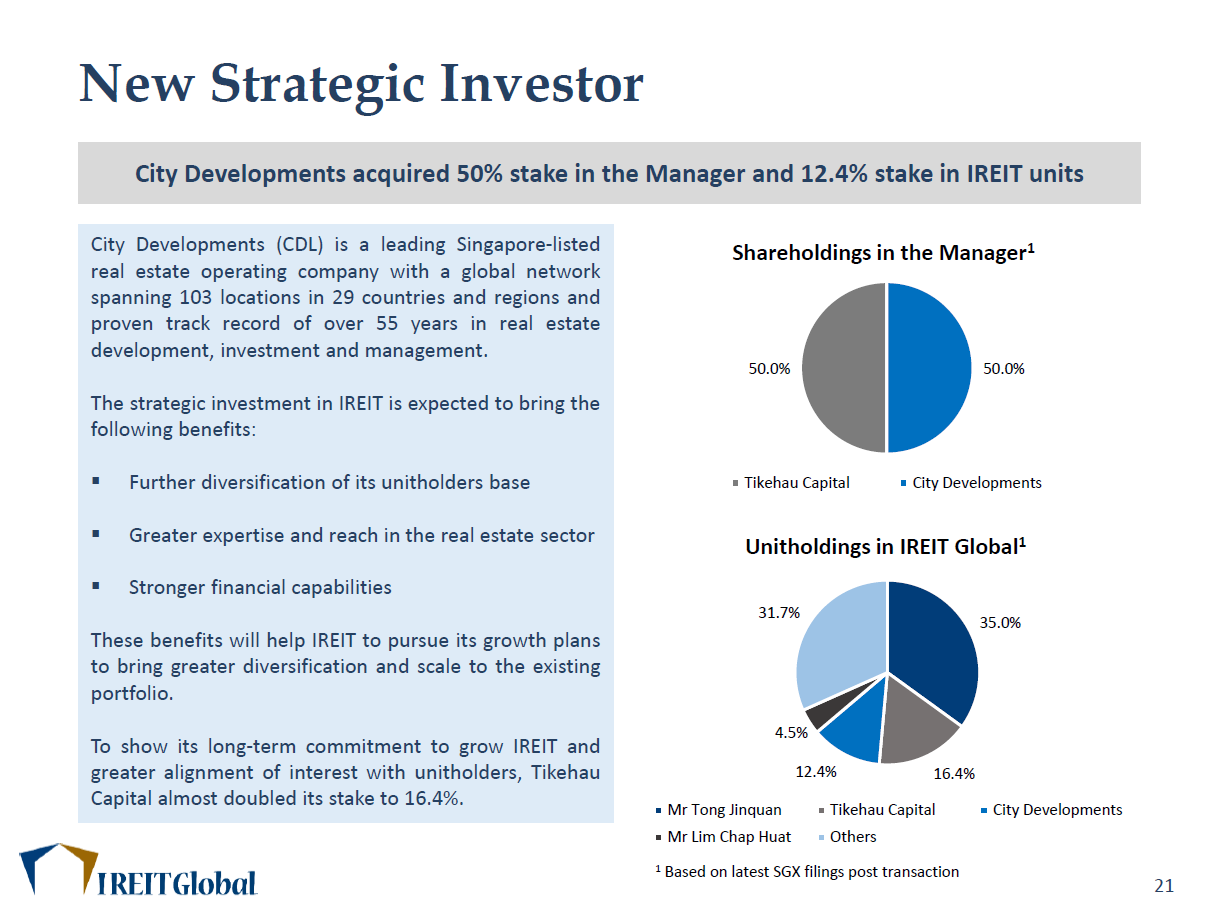

Interestingly enough, CDL just bought a 12.4% stake in IREIT and a 50% stake in the manager. I’m not quite sure what to make of this. Does it mean that a big acquisition is coming? Or is CDL simply trying to gain some exposure to German assets are an attractive price. It’s hard to say, and we’ll need to keep an eye on this one going forward. But with that 7.3% yield, I’m more than happy to wait and see.

Summary

P/B = 1.08

Yield = 7.3%

Based on: Price = 0.775, NAV is 0.72, DPU annualised is 5.68

4. Eagle Hospitality Trust

Eagle Hospitality is really interesting. We’ve talked about this REIT previously (see IPO review and IPO debrief), so I’ll dive straight into the details.

Because there’s so much negativity around this REIT, and because it’s come down in price quite nicely post IPO, I actually think this could be an attractive buy. For the record, I recently added this REIT to the FH Stock Watch, although I did say I like it a lot more at 0.65.

At it’s current price of $0.70 though, it’s a 20% discount to book, and a 9% forward yield based on the forecast numbers in the prospectus. Worst case if they miss revenue forecasts, you’re probably still getting an 8+ % yield, so the margin of safety on this REIT could be really attractive.

Again, hospitality plays are cyclical, so if there is a US recession in 2020, this is probably going to get hit. 66% of the revenue for 2020 is fixed rate in nature, so at least there’s some downside protection.

Ultimately, it’s all about risk-reward, and that 9% yield is baking in a lot of bad news, which I don’t think is warranted at this stage. I still think the Queen Mary saga is blown out of proportion, and if the price dips further, I may look to open a position.

Summary:

P/B = 0.80

Yield = 9.08%

Based on: Price = 0.70, NAV is 0.88, Forecast DPU is 9.08%

5. Prime REIT

I know, Prime REIT hasn’t even IPO-ed yet. But I was going through the prelim prospectus the other day, and the numbers looked pretty interesting. It’s US office assets (similar to Manulife REIT), but IPO-ing at book value, and a 7.4% forward yield. Compared to Manulife’s 9% premium to book and 6.7% yield, Prime REIT looks to be offered at a 10% discount to Manulife.

And after the horrible IPO performance from Eagle Hospitality Trust, perhaps this was done to avoid a similar fate.

I’ll do a more in depth analysis on Prime REIT once the offering details have been finalised. In the meantime, other acceptable REITs to replace Prime REIT are: Manulife (1.09 P/B, 6.7% yield) and Keppel KBS US REIT (1.0 P/B, 7.74% yield).

Summary:

IPO P/B = 1

IPO Yield = 7.4%

Based on: IPO numbers as disclosed in the prospectus

Manulife is 1.09 P/B, 6.7% yield

Keppel KBS is 1.0 P/B, 7.74% yield

Closing Thoughts

The REIT market has split into 2 the past couple of months. The blue chip REITs from CapitaLand, Mapletree etc have gone up in prices massively. At the same time, the smaller cap REITs have still stayed about the same.

So if you’re looking to buy some REITs now, I personally think there’s a lot more value to be had in the small cap REITs. Of course, the risk you’re taking on with small cap REITs is definitely higher, so you do need to understand if that’s something you’re comfortable with.

Just to caveat though, please note that the global macro environment has weakened significantly in the past 12 months. The latest 10 year SSB now yields 2.01%, and I expect interest rates to drop further in the coming quarters as central banks switch to a more accomodative monetary regime, as the global economic slowdown starts to bite. So the next 12 months could be very interesting, and there may be a lot of volatility in global asset prices. So don’t rush out to buy the 5 REITs on this list without understanding your financial objectives, your risk appetite, and your holding period. Because in the short term, asset prices can go anywhere.

Finally, please note that this article is valid as at July 2019. If economic conditions deteriorate further, or prices change, this article may become out of date as I probably would not be updating the numbers here. So do ensure that you double check the figures before investing.

I will update the numbers and any new stock picks I have on the FH Stock Watch, so you can check that out if you’re keen.

So there you have it. The Top 5 High Yield REITs in Singapore to buy right now (July 2019)! Agree with this list? Any high yield REITs that I missed out? Share your thoughts in the comments section below! I respond personally to all comments!

Enjoyed this article? Do consider supporting the site as a Patron and receive exclusive content. Big shoutout to all Patrons for their generous support, and for helping to keep this site going!

Like our Facebook Page and join the Facebook Group to continue the discussion! Do also join our private Telegram Group for a friendly chat on any investing related!

How about EC World? The price had came down quite a fair bit and the yield look comparable with some of the Reits u mentioned.

Personally, as an investor I don’t like the sponsor for EC World, but of course, that’s just my opinion. I prefer to be safe rather than sorry, but I could be wrong. 😉

Hi, what do you think of Cromwell? It is more diversified than iREIT global in the European market. While its share price has been reset several times because of fund raising, management has at least hit operational promises and current yield is particularly high.

Quite similar to the situation for EC World, where I personally, as an investor, don’t like the sponsor. Again, there’s no right or wrong answer here, so if you like the REIT, by all means go for it! 🙂

Any thoughts on AIMS APAC REIT?

Personally, I’m not a huge fan of the sponsor. I had some in the past but sold it eventually. Of course, that’s just my take. 🙂

I’m a beginner in REITS, though I’ve bought some previously. Just a question, if you had to choose 1 among those 5 on your list, which would be your choice? 🙂

TBH, if I had to choose I probably wouldn’t be buying REITs, I think they’re all pretty pricey now. But if you held a gun to my head and made me buy 1 REIT for myself from this list, probably Ascott.

Hi,

Due to the recent events that’s happening around the world, I may be buying into some Singapore based US REIT. Do you think it is a good idea despite being subjected to the 30% withholding tax deduction?

Hi, the US REITs that are listed in Singapore have full tax transparency, so you wouldn’t incur any withholding tax. 🙂

Hi!

I am a beginner in reits & was wondering how did you calculate the premium to book value?

Also, you mentioned you are not a fan of the sponsor of cromwell reit, can i understand why?

Thanks!

Lynn

You take the market price as the numerator, and divide it by the NAV per unit (you can get this from the financial statement/quarterly report.

I don’t like Cromwell’s Sponsor because of their actions leading up to the IPO, and immediately after, but it’s really a personal thing. That said, I’m hearing lots of good things about them these days, so I may change my mind haha.

I am new to REITs….like to understand the minimum investment to buy it. I am trying to invest via FSMone platform, it is possible?

Yep, FSMone works! Minimum investment is 100 units (lot size on SGX), although if you’re using the minimum your transaction fee as a percentage of your investment would be large, so it’s not ideal.

Any insight on why Ascott has lost more value than other REITS during COVID-19 and regained less of those losses yesterday than than the others? Am hesitant to invest more there at low price point in case there are risks I’m unaware of. If they struggle they could payout less and appreciate less. Any insights here? Many thanks.

Well Ascott is a hospitality play, and it looks a lot like this entire sector is going to be badly hit in 2020 from COVID-19. That probably explains the price action? If you compare with other hospitality REITs, the story looks to be pretty similar.

Considering severity of COVID-19 do you think Ascott could go bankrupt, fail as a business, our shares could become worthless?

Impossible to say with certainty. My current view is that it is unlikely due to sponsor backing.

That said, I also sold Ascott 2 weeks ago. 😉

That certainly doesn’t inspire much trust 🙁

Do you have any good trading account to recommend for using? Thanks

Sure you can check out this article: https://financialhorse.com/best-stock-broker-2020/