REITs have been getting a lot of bad flak recently. I like to think that this is down to 2 reasons.

Firstly, because REITs are yield instruments traded on the public capital markets, the market tends to value them together with fixed income products. Accordingly, when interest rates goes up, the price of REITs tends to drop in tandem with other fixed income products, as investors now expect a higher yield from their investments.

Secondly, because REITs are essentially a leveraged property investment (you buy property, gear up to 30-40% permanently, and collect the yield), a rising interest rate environment will increase the cost of funding for REITs. Much like how your mortgage payments go up when interest rates go up, the same thing happens with REITs, affecting the amount of distribution received. Indeed, the weighted average cost of debt I’m seeing for most REITs these days is in the 3+ % range, and when you look at the recent acquisitions in the Singapore market that are being transacted at a 2-3% yield on cost, it really makes you wonder how DPU accretive any new transaction will be for a REIT.

I actually don’t disagree with the 2 arguments above. I agree that there are headwinds facing the REIT industry. But I also think that from the perspective of a long term investor, REITs are still very reasonably priced, with many good opportunities in the market.

I like to think of a REIT investment as an investment in the underlying property, only with a lot of leverage. Imagine that you invest in a fantastic office building right smack in the heart of CBD, that is generating 4% yield on cost right now. With leverage, the yield is boosted to 5%. Now what happens when argument (1) above comes true. The equivalent is that the price of the property drops, because investors demand a higher yield on cost from the property. But does this matter to me? Hell no, because as a long term investor, I don’t really care what price other investors are willing to pay pay to buy the property from me, because I am not selling regardless. I am happy to sit on my hands and collect the yield.

What about argument (2)? When the cost of borrowings goes up, each refinancing will cause the weighted average cost of debt to go up. However, in a rising interest rate environment, this typically signifies a stronger economy, and I may be able to pass this off to tenants by increasing the rental reversion. Of course, this doesn’t work all the time, because like every good Singaporean property owner knows, the amount of rental you can charge is also influenced by supply and demand. Which is why it’s also important to understand the dynamics of the asset class you are buying into. Although that said, if you’re lazy or can’t be bothered, you can just diversify.

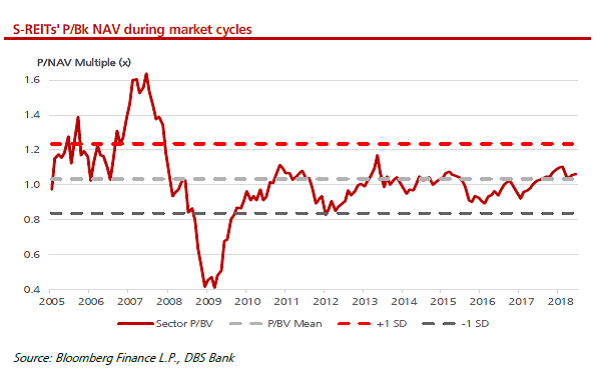

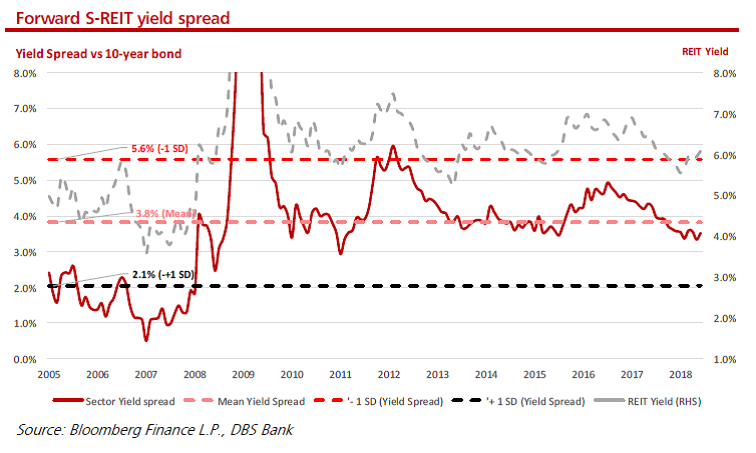

And as you can see from the charts below, from a longer term perspective, REITs are actually trading at quite reasonable valuations.

Source: DBS Research

In this article, I’m going to pick 5 REITs that are attractive to me as an investment currently. The rules are simple:

“Financial Horse, imagine that you own no REITs at all (omg the horrors). You have S$100,000 to pick 5 REITs for your new portfolio, and make the purchases over the next 1 month. You cannot sell the REITs for the next 10 years.”

Basics: What to look out for in a REIT

One of the first articles I wrote on Financial Horse was on the 5 things to look out for when investing in REITs. Very simply, they are:

- A strong sponsor

- Reasonable P/B ratio

- Sector / Geographical allocation

- Quality of Assets

- Distribution Yield

For this exercise, I would have to pick 5 REITs that reasonably meet the 5 points above right now.

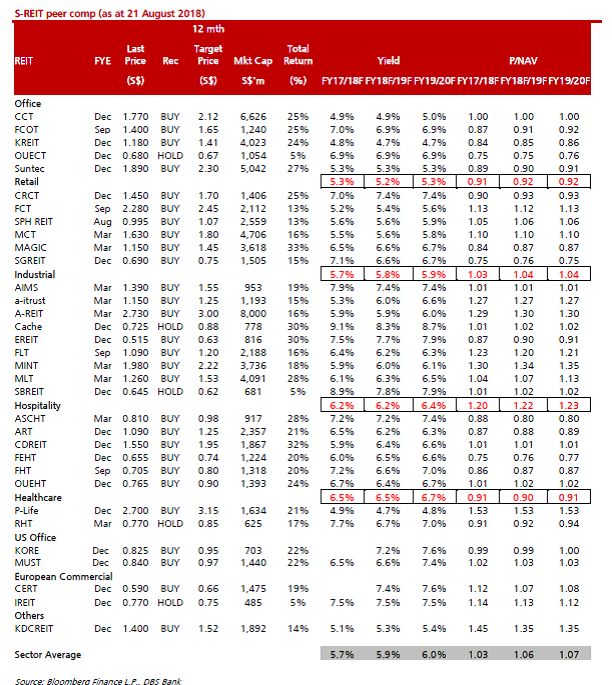

I published a REIT screener created by a reader earlier this week, but that screener used numbers from the FY2017 annual reports and excluded China REITs, which was not acceptable for the current exercise. I wanted the latest 2Q2018 numbers, and I also wanted access to China REITs, as I think there are great opportunities in that space right now. Accordingly, I’ve used the numbers compiled by DBS research below (I did some checks and the historical numbers largely check out).

1. Mapletree Commercial Trust

You guys must be sick of hearing about Mapletree Commercial Trust by now. I seem to mention Mapletree Commercial Trust in every REIT article I write. You can take a look at my original article for why I love this REIT so much, but simply put, it’s a pure Singapore play that offers exposure to 2 of the best in class properties in Singapore: Vivocity and Mapletree Business City Phase 1. It’s also backed by Mapletree, arguably my favourite REIT sponsor in Singapore. A lot of investors are wary about over exposure to retail these days due to the impact of ecommerce (a view I don’t share), and if you have such concerns, Mapletree Commercial Trust offers a blend of exposure to retail, business park and office.

I have to admit the current unit price (S$1.62) isn’t fantastic. It works out to about a 5.5% yield, and a 1.1x P/B. This REIT went down to the low 1.5+ range earlier this year when everyone was freaking out over rising interest rates, and I absolutely loaded up on this REIT back then. 1.5+ is a fantastic price, but even at it’s current price, I still really like Mapletree Commercial Trust.

2. Mapletree Logistics Trust

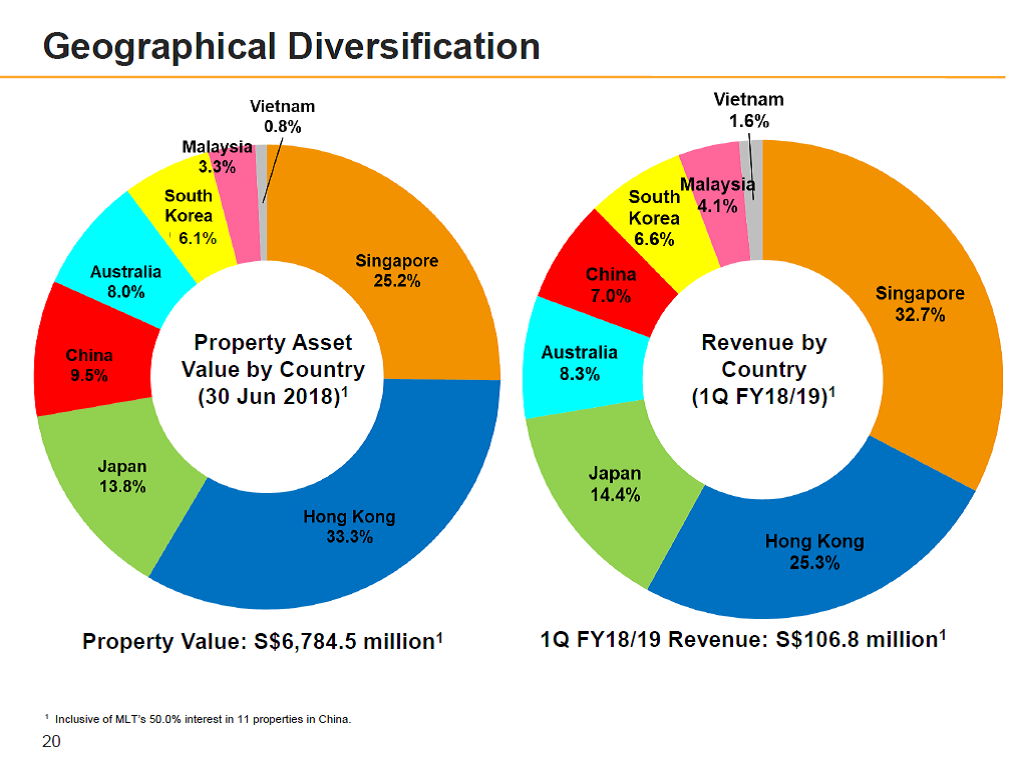

Within the industrial and logistics space, my choice would be Mapletree Logistics Trust. A lot of investors like Ascendas REIT and Mapletree Industrial Trust, both of which are pure Singapore industrial plays, but personally I like the higher yield (6.1%) and more attractive P/B (1.04) offered by Mapletree Logistics Trust. I also like the exposure to logistics (I think the logistics asset class is going to have massive secular tailwinds in the coming decades), and the broad exposure to Asia.

Mapletree Logistics Trust recently acquired five great ramp-up logistics properties in Singapore from a subsidiary from HNA. It was a very interesting sale and leaseback from the HNA subsidiary (probably to raise cash in their bid to deleverage), but HNA’s loss is MLT’s gain. The chart’s below don’t reflect this latest purchase, so expect Singapore as a proportion of MLT’s portfolio to go up.

3. Ascott REIT

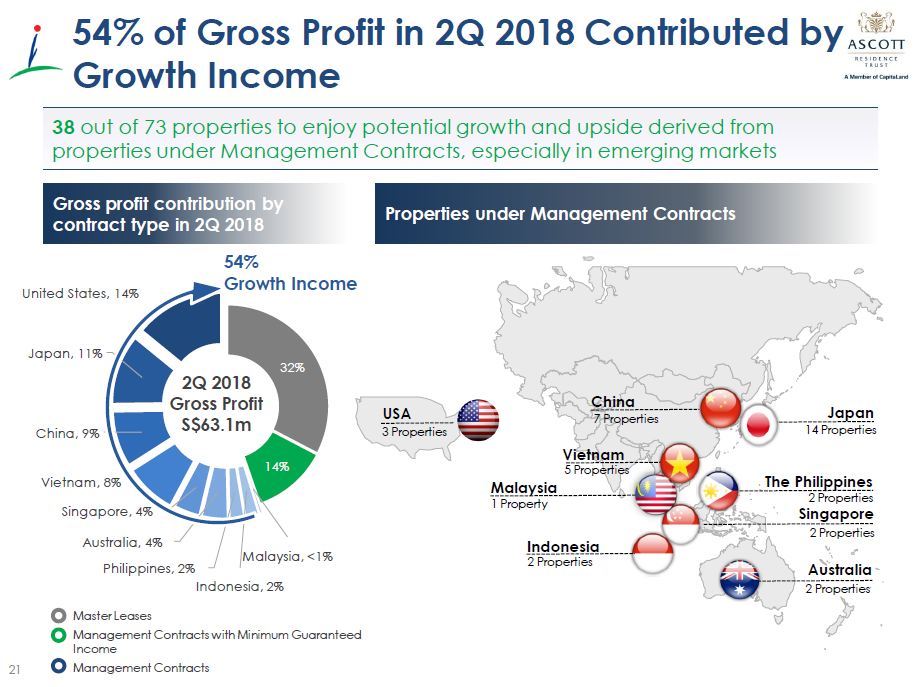

My choice in the hospitality sector is Ascott REIT. It’s currently trading at a 6.5% yield, and 1.0 times book value. Ascott REIT offers very broad exposure to the global hospitality sector, and I also like the blend between fixed Master Leases and Management Contracts. The former provides a fixed income to help smooth out gains, while the latter allows Ascott REIT to enjoy the upside from improving rents in the hospitality sector.

One problem with the hospitality sector is that the latest numbers have not been attractive. RevPau (Revenue per available unit) numbers have been showing weakness across the board, and it remains to be seen if this is a temporary or longer term thing.

However, given that I am picking REITs from a long term perspective, this bothers me a lot less. There may be some weakness in the short term, but this would be offset by the broad diversification in this 5 REIT portfolio, and in the longer term, this would offer exposure to the upside offered by the hospitality sector.

4. CapitaLand Retail China Trust

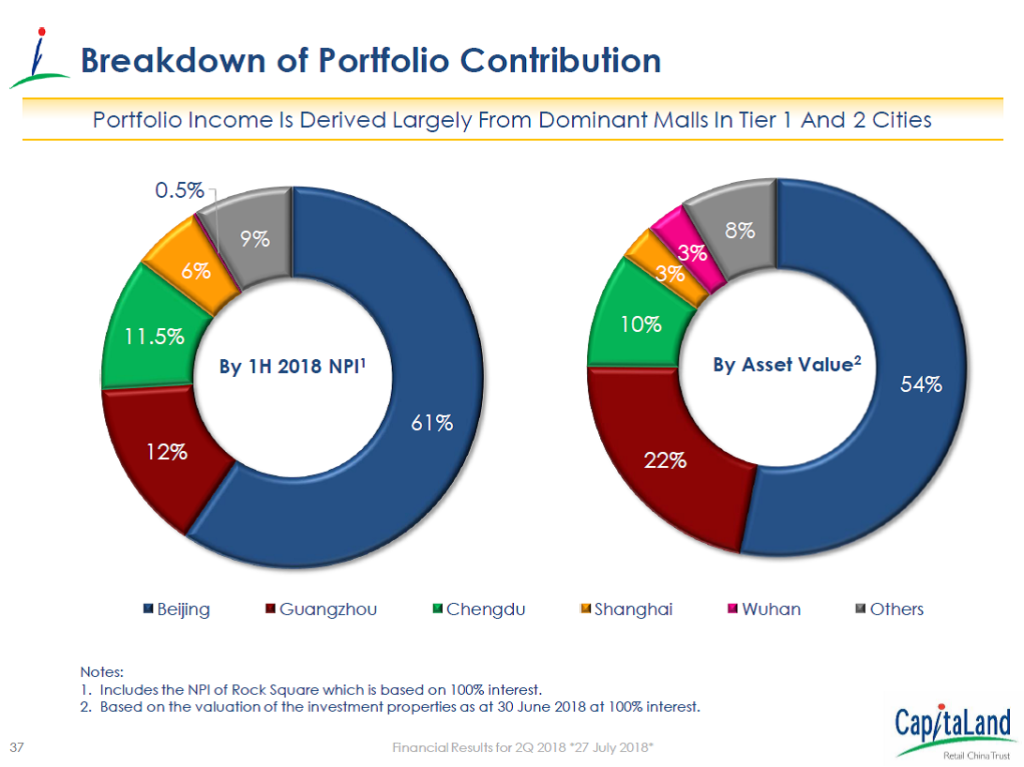

This may be a controversial one for some of you guys. Some people absolutely swear off China REITs. For me, I like the long term prospects of China, and I love the fact that other investors hate China, because of the opportunities this offers to a discerning REIT picker. If you take into account the recent acquisitions done by CapitaLand Retail China Trust, and offset the depreciation in the RMB, you’re still looking at what is comfortably a 7+ % yield, and a 10% discount to book value, which is pretty attractive from a risk reward perspective.

I get that this is a pure China play, and exposure to China retail at that! But the shopping malls owned by this REIT are located in Tier 1 cities in China, and if you’ve visited any of them before, you’ll know that they are mainly necessity malls targeted at average Chinese shoppers. Personally, I don’t see ecommerce replacing shopping malls entirely. If you look at the recent moves out of China, you’ll see that the big boys like Alibaba are starting to rent brick and mortar stores (similar moves from Amazon), that to me, really illustrates the limits of ecommerce. The way that offline retail is done will need to evolve, but the need for a physical store front in convenient locations, will remain.

The pure China point, is troubling due to the current trade war. I think the trade war will affect China in 2 ways:

- Retail Spending. I think the impact to retail spending in China will be muted, given how big the size of domestic consumption is these days. Cities that are heavily reliant on trade, basically the greater bay area of Hong Kong, Shenzhen, Guangzhou etc, may see an impact, but CapitaLand Retail China Trust should be relatively shielded given that a huge proportion of its assets is in Beijing.

- RMB depreciation. The impact of the trade war on the RMB can be a dissertation in itself, but suffice to say, my personal view is that China’s depreciation of the RMB is done for now, and we’re not going to see major moves in the near future. If so, this should provide a floor on the unit price.

The fact that CapitaLand is a strong sponsor and one of the biggest players in China (about half of CapitaLand’s portfolio is in China) is an important point as well. This isn’t one of those family and friends China REIT with zero liquidity that we’re talking about here (not naming names, but you know what I mean;)

5. Netlink Trust

I’m going to cheat for the last one. Netlink Trust is a business trust, not a REIT, but I absolutely love this one. Check out my original article for the full reasons why, but simply put, I think Netlink Trust offers the monopoly that comes with being a sole telco operator, without the messiness that comes with being an actual telco player. Singtel, Starhub and M1 (check out the links for my previous articles on them) are all facing great pressures due to rising competition, the switch to SIM only, and the potential entry of TPG Telco. With Netlink Trust, you basically own the underlying fibre connection that almost all home internet connections ride on, with no real competitor.

Instead of owning real estate, you own fibre networks, and instead of rent, you charge a fee to telco players to use your fibre network. It trades at a 6% yield currently, but don’t expect to see fantastic revenue growth as the amount of “rent” chargeable is tightly regulated by the authorities. But a 6% yield, from what is essentially a monopoly, is good enough for me.

Honourable Mention: Singapore Office REITs

I’m sure the savvy REIT investors out there would have realised that I didn’t include any pure play Office REITs here. The only exposure to the office space comes from Mapletree Commercial Trust.

And that was intended, because I just don’t like the valuations in this space right now. Office properties (20 Anson, 55 Market Street) have been transacted at 2-3% yield on cost recently, reflecting the ridiculous prices investors are willing to pay for a good quality office building these days. And that is reflected in the unit price of the office REITs. Keppel REIT and CapitaLand Commercial Trust are currently trading at sub 5% yields. I get that rental reversions in the office space are on the rise, but a lot of these increased rents won’t kick in until next year. Until the yields are more compelling, I prefer to remain on the sidelines.

Closing Thoughts

As always, please don’t blindly rush out and buy REITs based on this article. Take the time to understand the properties you are buying into, the industry dynamics, and the strategy of the REIT. If you do so, you’ll find it incredibly rewarding to construct a broad, diversified portfolio of REITs that will pay you a healthy distribution for years to come. It’s actually okay to mix in a REIT with a higher yield when the rest of your portfolio has safe and stable properties, as this will increase the yield of your overall portfolio.

To quote a Warren Buffet analogy, REITs are like chicken rice. We’re going to buy them for the rest of our lives, so when the price of REITs/chicken rice come down, why would you not be happy? Take the opportunity to stock up on them when they are cheap, and when prices go up years down the road, you’ll be pleased that you had the foresight to do so.

Financial Horse, signing out!

Financial Horse has a set of 7 Commandments for Successful Investing, that I ask myself before making every investment, and that I will never break regardless of the situation. Enter your email below to receive a copy in your inbox!

[mc4wp_form id=”173″]

Enjoyed this article? Like our Facebook Page for more great articles, or join the Facebook Group to continue the discussion!

What about earnings growth rate??

That’s a good question. It’s included by implication under the quality of assets, becaue if the asset is good, it would translate into positive rental reversion and earnings growth. Although now that you mention it, the historical earnings trend may be able to indicate additional information that wouldn’t be evident purely from an examination of the asset. I may see if I can build this into the analysis in future.

Cheers!

Hi FH,

Good article as always!

Can I check r all the above mentioned consistent dividend grower? I would think for holding long term, it will be much more rewarding if the management can consistently grow the dividend

They are, although there will be exceptions during the GFC. I would focus more on the revenue and cash flow though, because everything else, from profits to DPU, can be subject to finnacial engineering.

With REITs, investors need to look at the long-term picture of the specific companies as well as their reputations. Also, the liquid stake/dividends matter at the end of the day as this is the investor’s income.

Definitely agree with you on this. Cheers.

Good sharing.

I have both MLT (logistic is low risk and asserts all over Asia), CRCT (China growth story) and SPH reit (new reit with only 2 malls, potential to grow).

On my watch list is hospitality trust, could you do a comparison on FE, CDL and Ascott reits.

Haha thanks for the share! I don’t really like SPH that much to be honest, but that’s just me. That’s an interesting topic you raised, let me look into them. I’m actually an Ascott unitholder myself. 🙂

Hi FH,

I’ve been reading about REITs the past week and to be frank, I am really excited by it! As a new investor to stocks/reits, I would like to ask how important is it that we acquire the units when it is undervalued. PB < 1

MapleTree Comm Tr seems great!. but it is currently trading at premium – Would you have invested at this point of time?

Price to book ratio for the following:

Mapletree Comm Tr – 1.17

Mapletree GCC Tr – 0.86

Ascott Reit – 0.85

CapitaR China Tr – 0.88

Thanks!

Hi Derek!

Great question! One thing to note about valuations is that the manager has a lot of control over the valuation they want to use. In your case, you’ve quoted only Mapletree and CapitaLand REITs, who have strong corporate governance so this shouldn’t be an issue.

Yes, I think MCT at it’s current price is not cheap, but it’s still a decent buy. MCT is trading at a premium to book because it’s Singapore assets (market perceives them as more stable) while the other 3 REITs you cited all have strong global and China exposure (market is discounting China exposure currently due to trade war uncertainty.

Hope this helps! 🙂

Many thanks FH!

Hi FH, I’m a fresh grad new to investing and I have to say that your articles are great in giving me that much needed crash course behind what I should think about before investing 🙂 Great quality content!

1. Saw that building a REITS portfolio you’ve suggested requires reading of reports, tracking of news to understand the fundamentals. If I don’t foresee myself being able to understand these fundamentals (no time / insufficient knowledge), would it be a better idea to: Invest in REITS ETF / invest in the 5 REITS you mentioned (once-off) / just not invest in REITS altogether?

It’s definitely a steep learning curve since I just got started investing in Robos, STI ETF and SSB as well, and those are much simpler / less risky, albeit with far less returns.

2. Correct me if I’m wrong: Does it mean that REITS are likely to be more worth buying during a financial crisis, given the need for them to refinance (supply) and investors who might be looking to sell due to falling sentiments (demand)? Is there anything I failed to consider?

Really hope that you will reply me. Thank you!!

Hi Valentina,

Welcome to Financial Horse and glad that you’re finding it useful!

1. I fully understand what you mean. Unfortunately the REITs ETF have quite a high expense ratio, which holds me back from recommending them fully. I would say you can try to pick 5 REITs across asset classes, and stick only to CapitaLand and Mapletree REITs, and that should be good enough as a once-off investment. You don’t need to check on them regularly, just once or twice a year to see what new properties they are buying, and how the yield is holding up. In the long run, you’ll be surprised by how much you learn. You can actually just start with 1 or 2 REITs, and slowly add more over time.

2. Yes, REITs are capital market products, and because they are freely traded, they will fall in a financial crisis situation. So yes, the best time to buy is of course during a financial crisis, but what I found is that when all hell is breaking loose, there are very few investors who are calm enough to be buying REITs/Stocks then. Hopefully, we will be one of those!

Thanks so much for the reply!

Got it on your recommendation 🙂 How much would you recommend I invest (at minimum) for each REIT, for the transaction fee to be worthwhile? I just started work, so I’m not sure if it’s a good idea to put a huge lump sum investment into 1-2 REITs, given that REITs would then become >90% of my portfolio for these few years. Especially since I’m only doing small sum investing (~$300/mth) for starters. What do you think?

And if I’m investing in Mapletree and Capitaland, would you recommend me to start with Mapletree Logistics first, or Mapletree Commercial Trust?

Just googled what an expense ratio means. Understand that it’s the annual fee you’re paying as a percentage of your investment. Does investing in individual REITs incur an expense ratio too, and how does it compare to REITs ETF?

Lastly, if I were to invest in REITs as a once-off, is it then important for me to time the market, or do you feel it is okay to invest as long as it is below 1.15x book value (as per your other article)? Thanks again FH!

Hi FH,

I’m in a similar situation as OP here. If I’m only just starting out, with minimal salary (S$2500), it’ll take me optimistically 1.5 years to save enough for my target stash of emergency funds, and accumulate a sum of $3000-$4000 to do a lump sum investment in 1 counter of REITs. I do have S$15,000 in savings so far, however, inclusive of discretionary spending fund and living expenses.

I read your article on MCT and am very interested in it. But given that time in the market is very important (especially since I do feel that we’ll have a market downturn in 3-5 years), is 1.5 years too long of an opportunity cost to be accumulating money? Would you recommend me to (A) save for 1.5years before looking at REITs, (B) DCA around $100/mth into MCT via Maybank KE (and maybe 1 other counter), (C) tap on my current $15,000 savings to invest $3000 into MCT now – given my context?

Hesitant about waiting out on MCT, since I’m not sure if the price will spike further in the next 2 years, if more investors deem it to be a valuable asset – especially with MBP Phase II ongoing. Or… I guess there’s also saving and waiting till the next crash in 3-5 years to invest hahaha

That’s a very good question. If you’re investing S$1000 using the cheaper broker out there (eg. DBS Vickers Cash Upfront), it’s a S$10 minimum commission which works out to 1% of your investment sum. It’s not ideal, but I think given the cicumstances, a S$1000 investment works.

You won’t lose much even if it drops (or goes up), but the key here is to build up your familiarity with the financial markets, and on investing knowledge. At your age, the main focus should be on increasing your earnings (either through your career or your business) and building up financial knowledge, so that you’ll know how to manage your money when it eventually comes.

Although since you’re on Financial Horse and asking these questions, you’re probably well on your way there!

TLDR: My personal choice in this case would be to invest in S$1000 sums. The DCA plans do have transaction costs as well.

Hi FH

Do you think its still ok to invest in reits, thinking of long term investment. Thanks

Absolutely, from a long term (5 to 10 years) investment timeframe, I think current prices are attractive, although there are a few counters that I think are priced quite expensively, do watch out for those.

Mid term (2 to 3 years) it’s a bit murkier, because I think we are nearing the end of this short term debt cycle. But as a long term investor, just use the next recession as a chance to add to your position.

Cheers!

what about fortune reit since the next few decades we are looking at the china growth story?

I think Fortune REIT is too Hong Kong focused for my liking. As a rough illustration, in 1993 Hong Kong’s GDP was 27% of China’s GDP. in 2017, it was less than 3%. Where this will be in 20 years is anyone’s guess, but the point here is that Hong Kong’s bright future is by no means guaranteed, as opposed to a city like Beijing, Shanghai, or even Shenzhen. The fact that Hong Kong real estate prices are so pricey these days also makes me a lot more cautious on Hong Kong as an investment destination.

Cheers!

Hi FH

i am a newbie to REIT and considering to invest REITs for the first time and come across your article. This is indeed very informative and helps me to make decisions. I would like to ask you some questions: May i know what is the min amt to invest in each REIT? How many REIT do people usually invest for a start? And if i really want to invest for a beginner, which is the most safe and recommend REIT?

Hope to have your advice soon. Thanks!

There’s no minimum amount, it will be 1 lot which is 100 shares. I generally try to invest a few thousand each time to minimise transaction costs. 4 to 5 REITs is ideal for diversification, and try to split them across asset classes. For a beginner, REITs from CapitaLand or Mapletree are usually safe, but the prices are on the high side now, so it really depends on your investment timeframe.

Hi Financial Horse,

Thanks for sharing your insights. I noticed that First REIT has underperformed significantly in the recent months, hence yield is optically looking attractive. May I please ask your view on this REIT? Many thanks.

To be honest I don’t follow First REIT too closely, as I think it’s quite a high risk counter given the geography and the sponsor. Personally I would probably not invest unless the yields are highly attractive (>10% and sustainable)

Hi FH,

Thank you for the great insight, as per usual.

Will you be updating this some time in the next few months by any chance?

Thanks,

P

Hi P,

Thanks for the comment!

Unlikely to unfortunately, I typically don’t revisit old posts. If you want my personal stock ideas you can follow me on Patron, that would be constantly updated.

Otherwise, I may eventually do a new article on the Top REITs when the time is right or when market conditions have changed. 🙂

Cheers!

Hi FH,

Thanks for the reply and well-noted!

Will look into your Patreon, thank you so much.

Best,

P

Don’t you think investing in an individual REIT will be riskier than investing in a REIT ETF for example the NikkoAM Straits Trading Asian ex Japan ETF (assuming you buy at reasonable price)?

The REIT ETF has a pretty high expense ratio that I don’t really like. And when you buy at ETF right now, you’re basically buying into all the big, blue chip REITs are all time highs, which is not something I really like too. So yeah.. I prefer to DIY it, but of course, if you’re keen on ETFs for the ease and convenience, it’s still better than not investing in REITs at all! 🙂