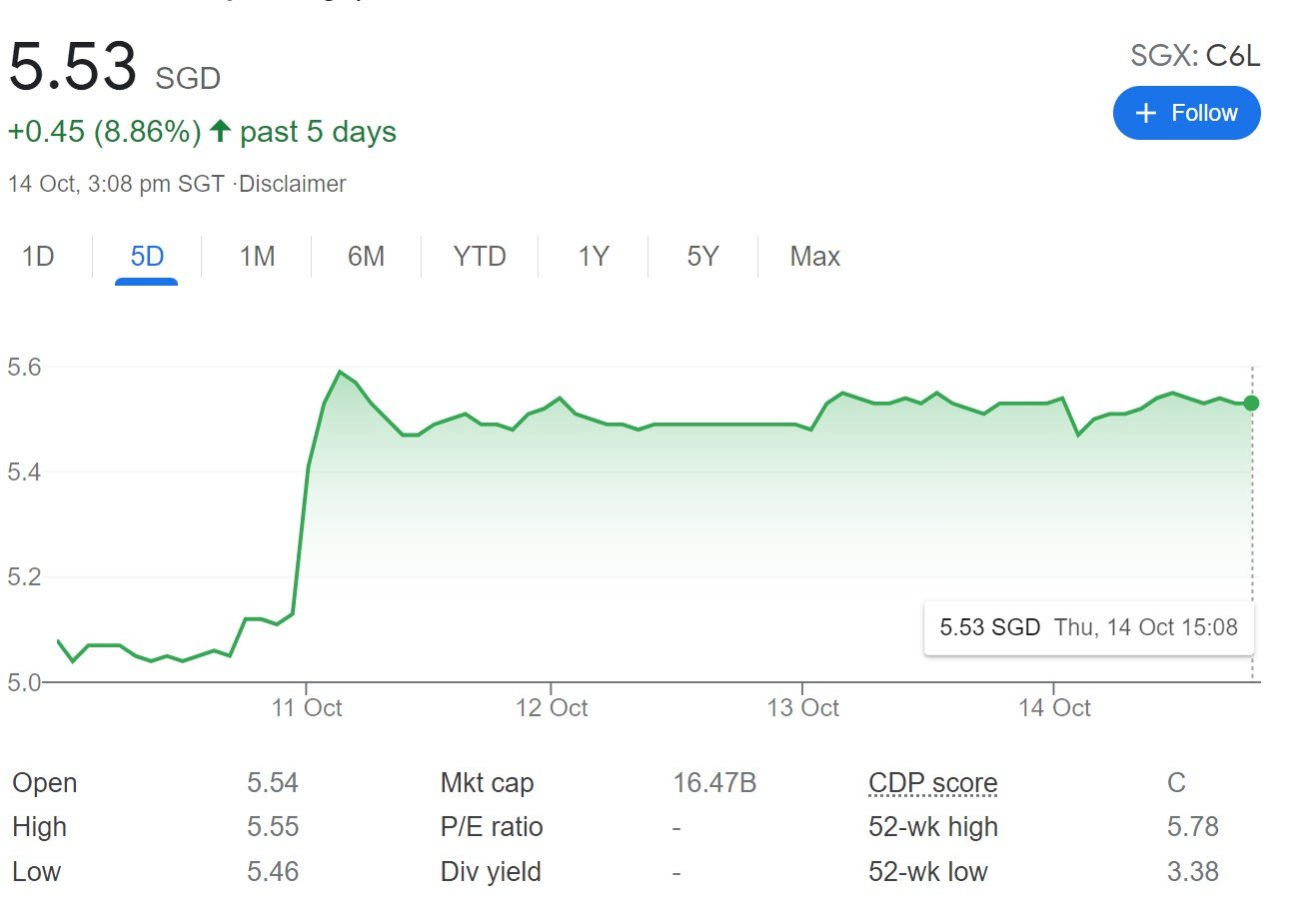

So… with the announcement of the Vaccinated Travel Lanes (VTL) last week, a lot of Singaporeans got very excited.

So much so that the SIA website went down.

And SIA shares spiked 10% on Monday after trading resumed.

That got me thinking – Is there a tradeable opportunity here?

Let’s say I wanted to pick a few stocks that would benefit from the global travel recovery. As a Singapore investor how best should I play it?

And is it already priced into the stock?

*Launch of the Stocks MasterClass!*

A lot of you have reached out to ask how to invest in growth stocks, how to allocate between US / China / Singapore, how to position size, when to buy growth stocks vs dividend stocks etc.

You’ve asked about how best to invest in stocks, from the perspective of a Singapore investor.

Now I try my best – but this is something more than what can be shared in my weekly articles.

This calls for an entire framework to investing.

Been working on this the past 18 months – Launch of the Stocks MasterClass! ????????????

Find out more here!

Basics: How to bet on the travel recovery?

The Motley Fool has a nice chart that shows the main travel related stocks:

- Airlines

- Hotels

- Short Term Rentals

- Amusement Parks

- Sustainable Travel

Strategy =/= Execution … What is priced in?

As I was researching this article though, I realised that for the more obvious plays like airlines and hotels, a lot of the COVID travel recovery has already been priced into the stock.

Stocks are forward looking by nature (by about 6 months), so in the world of stocks COVID is no longer a big concern.

Things like rising fuel prices, staff walking out, matter far more to travel stocks right now.

So the easy COVID recovery money has already been made, and to outperform from here would require some out of the box thinking.

Top 5 Travel Stocks to buy for Singapore Investors (2021)

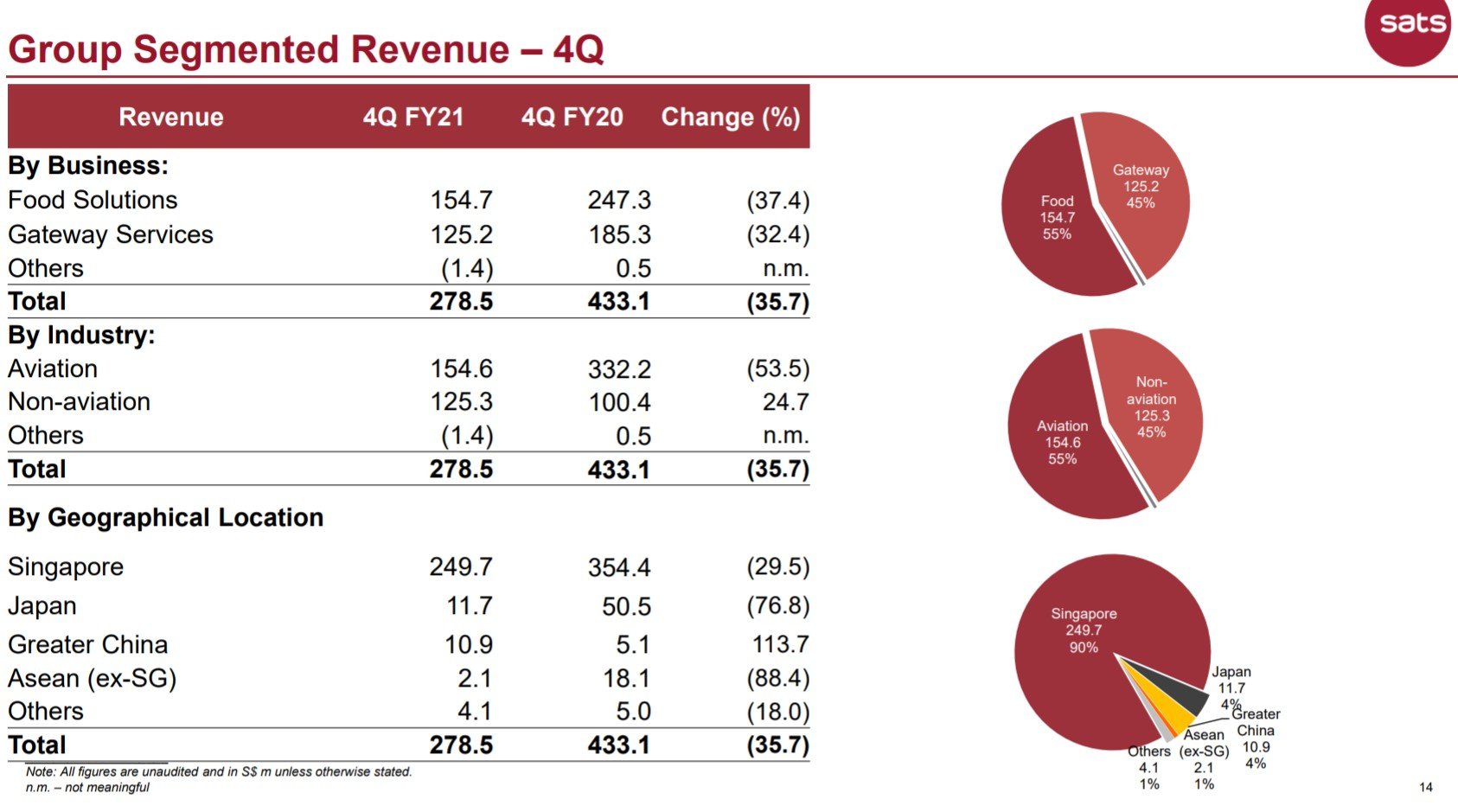

SATS

As Singapore investors, this list would never be complete without a few Singapore stocks.

And trust me, I looked at a number of travel related stocks in Singapore, but I couldn’t really find many that I really liked.

In the end, one that I settled on was SATS.

SATS is a food and gateway services company.

In simple English, they run a food catering business (Food Solutions), and they also provide food for airlines (Gateway Services).

In the most recent quarter, food was 55% of the business, and gateway was 45%.

Breaking that down further – 55% of the revenue was from aviation, and 90% of revenue comes from Singapore.

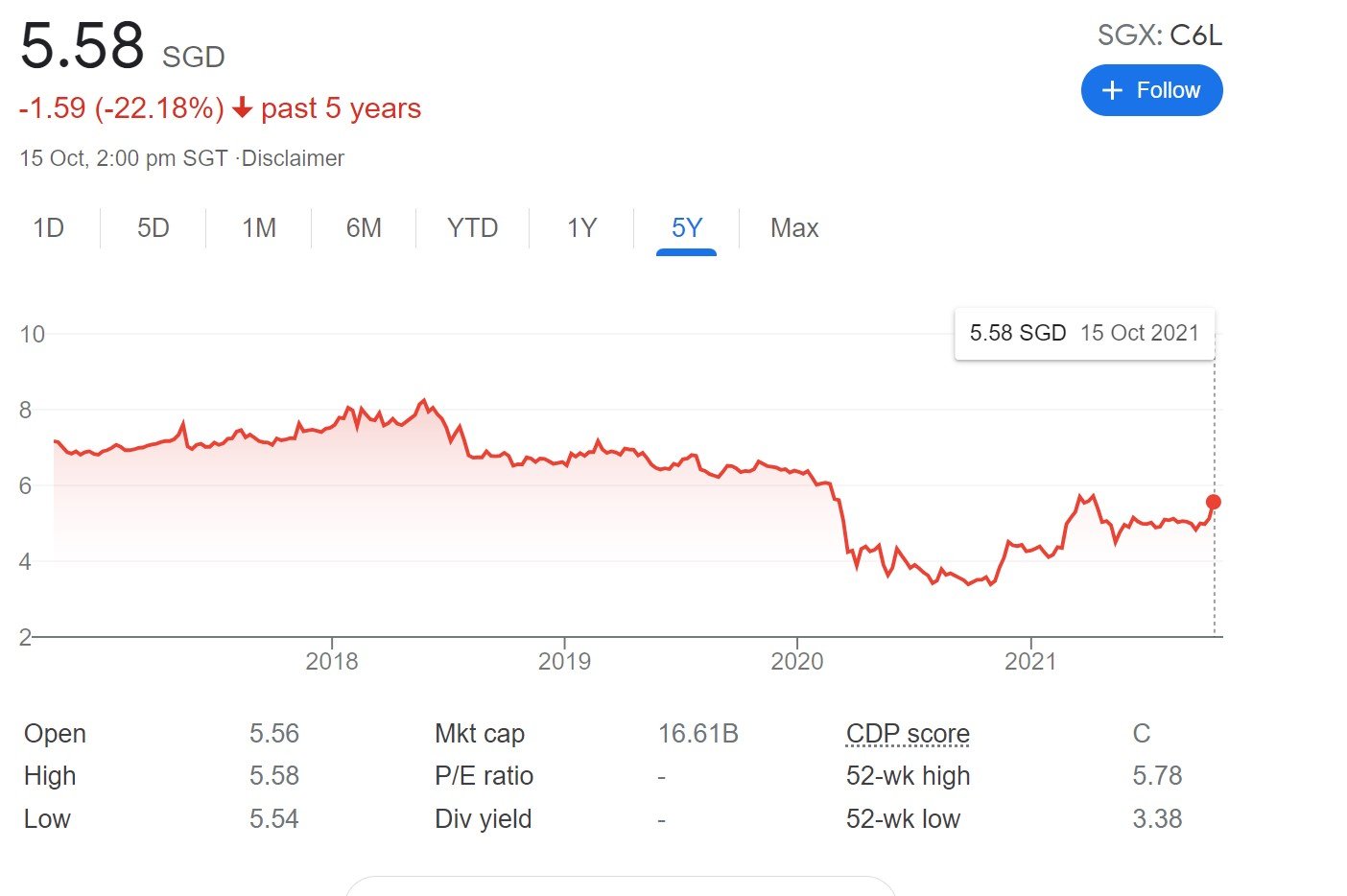

The problem though, is that SATS price pre-COVID was about 4.8.

It is at 4.37 now – only 8% below pre-COVID prices, when the revenue is still down 35%.

At this price, much of the COVID recovery has already been priced in.

Which means that any future share price gain is unlikely to be driven by COVID recovery, and more by factors that haven’t been priced in.

Food inflation perhaps. Or organic growth of SATS food business.

What I like about SATS is the very stable, recurring business from being a monopoly supplier to SIA and Changi Airport. And also to the army via SFI (for the guys out there I’m sure you have fond memories of SFI).

Just like ST Engineering that’s a very stable core base of earnings, and beyond that SATS has also been quite aggressive about trying to grow the food business.

In a more inflationary world, food services like that could be a good hedge. And if earnings recover to pre-covid levels, we’re looking at about 4% yield for SATS stock, which isn’t too shabby.

Why not SIA?

The other big contender for this spot was SIA.

SIA also has recovered to 22% below its pre-COVID price (adjusted for the rights, but doesn’t take into account the massive number of MCBs issued).

But frankly, I’m really not a fan of the airline business.

As shared previously, I think the key problem with airlines is that they offer a commoditized product – which means they lack pricing power. If Emirates comes in and offers tickets 50% of the price of SIA, you bet that a big chunk of flyers will take Emirates instead.

Throw in rising fuel costs, problems with hiring pilots and air crew and it’s just not a fantastic business to be in.

From a fundamental, valuations standpoint, if SIA has already recovered to pre-COVID levels, it’s hard to see where future gains will come from.

So between SATS and SIA, I eventually settled on SATS.

But frankly I didn’t really like either of them.

There just wasn’t much choice in the Singapore market.

Ascott Residence Trust

The next stock I settled on, was Ascott REIT.

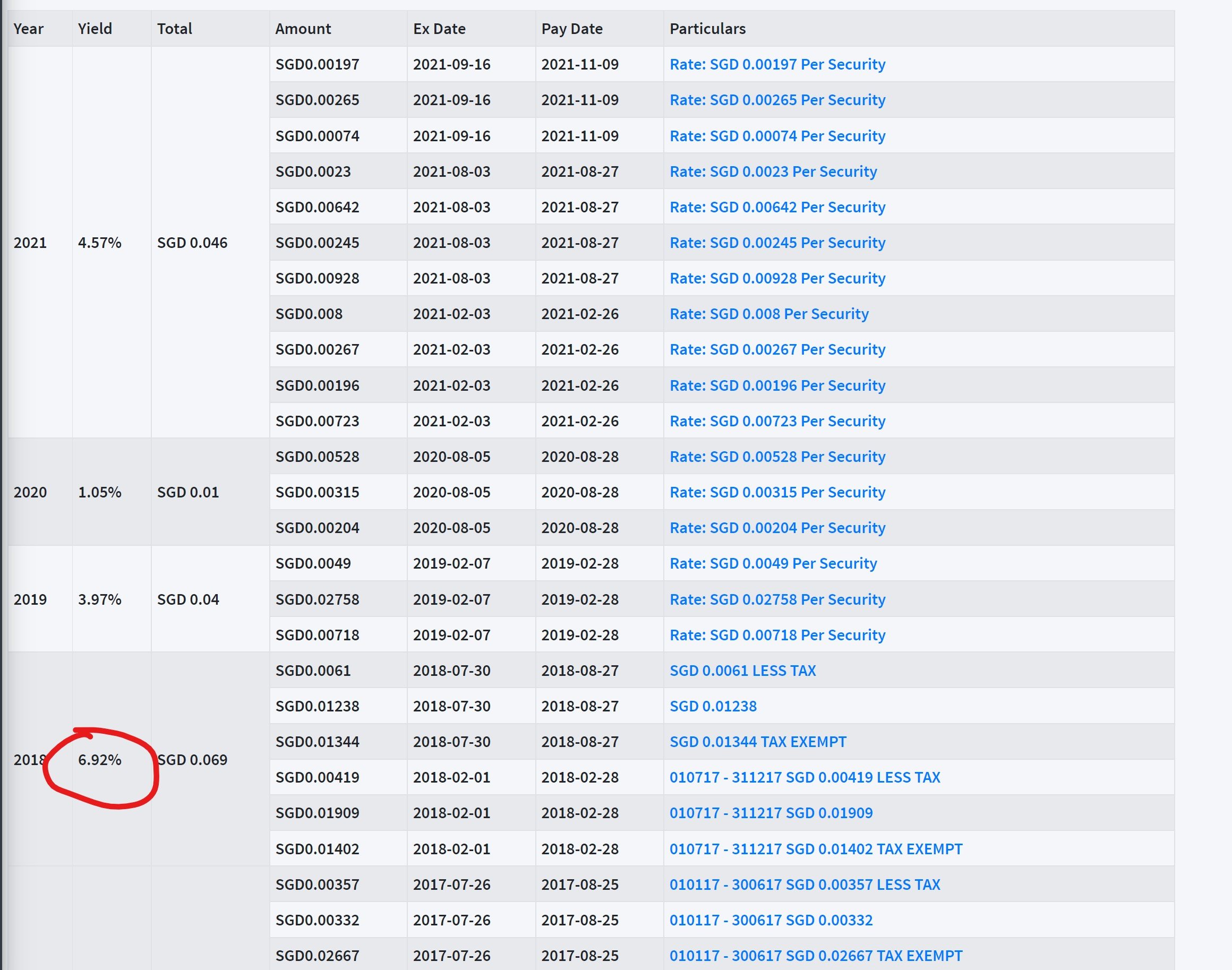

Ascott REIT trades at a 4% annualised yield currently, but that’s because COVID has severely impacted the earnings from its serviced residences.

If earnings go back to pre-COVID, Ascott could be paying a 7% yield at this price, which is pretty juicy if you consider the 25% discount to book value.

I also like their recent foray into student accommodation.

Student accommodation is a solid business and delivers very stable, recurring revenue. Lots of potential for growth here.

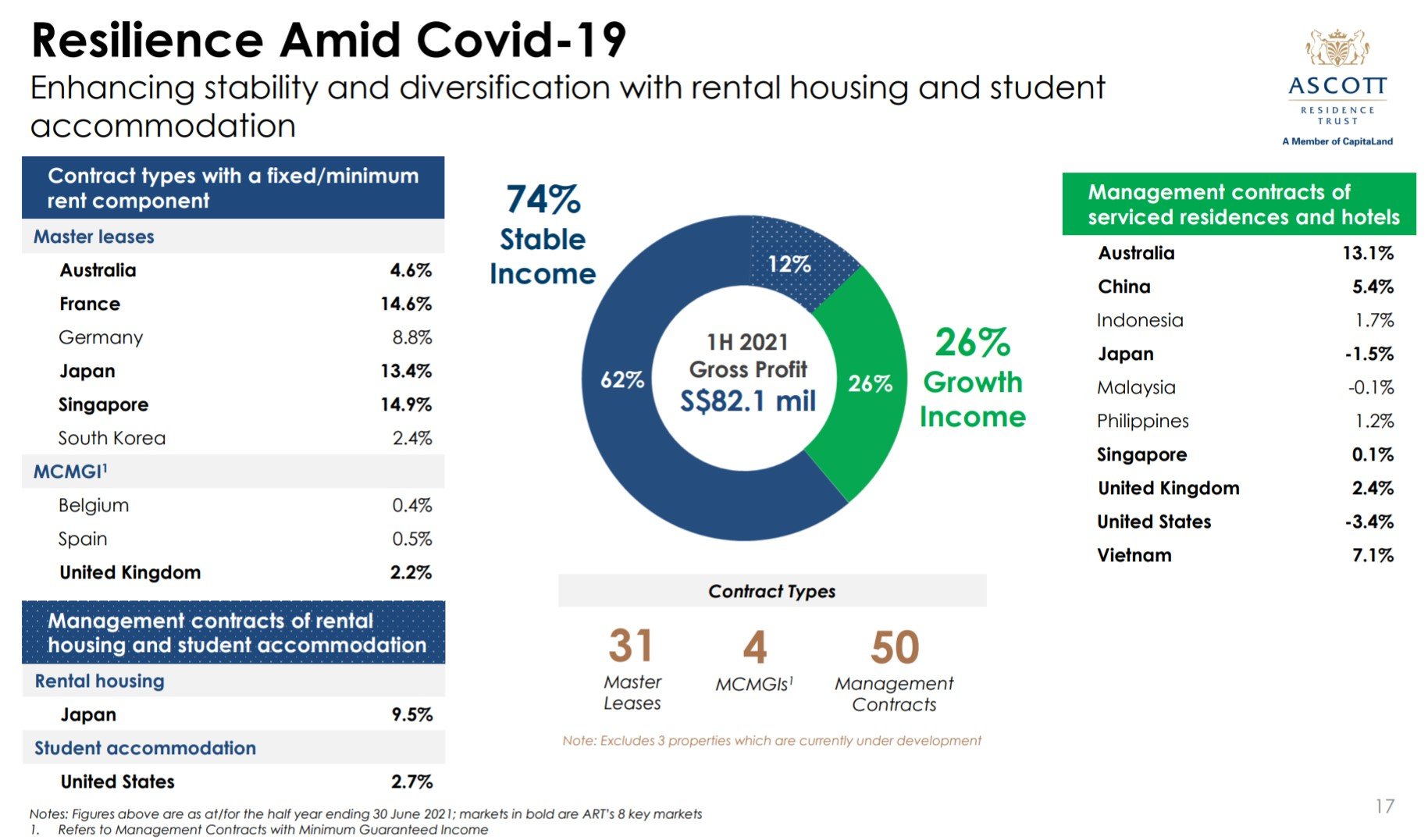

What I also like is that 74% of the 1H2021 profit is derived from contracts with a fixed/minimum rent component.

So even if hospitality takes years to recover, there still is some minimum income for the REIT.

But at the same time, if hospitality does recover, there is upside from the percentage based fee income.

That’s downside protection will allowing you to benefit from the upside.

My main gripe with Ascott REIT – is that I just don’t think the hospitality business is a great one to be in anymore.

It’s not unique to Ascott, I could say the same about Marriott, Hilton, IHG etc.

The underlying problem is that with the rise of the Online Travel Agency (OTA), hospitality has become a scale business.

Everybody books via Booking.com these days, which takes an obscene share of the margins.

The only way you get to negotiate with Booking.com for a larger share of the margins?

It’s if you have scale. Big, big scale.

Last I heard the minimum was 1 million rooms globally before Booking.com would even bother negotiating with you, but this number may have changed since.

Long story short, running a hospitality business today is pretty low margin, and you have to worry about operational problems like your staff quitting on you or contracting COVID.

The real fat margins have gone upstream, to players like Booking.com and Airbnb.

Alternatives to Ascott Residence Trust: CDL Hospitality or Far East Hospitality

AirBnb

The more I think about the hotel business, the more I think the better way to bet on the travel recovery is not to buy the hotels, but to buy the online travel platforms.

And of all the platforms, AirBnb is the one that stands out for me.

AirBnb has 5.6 million listings globally, across 100,000 cities.

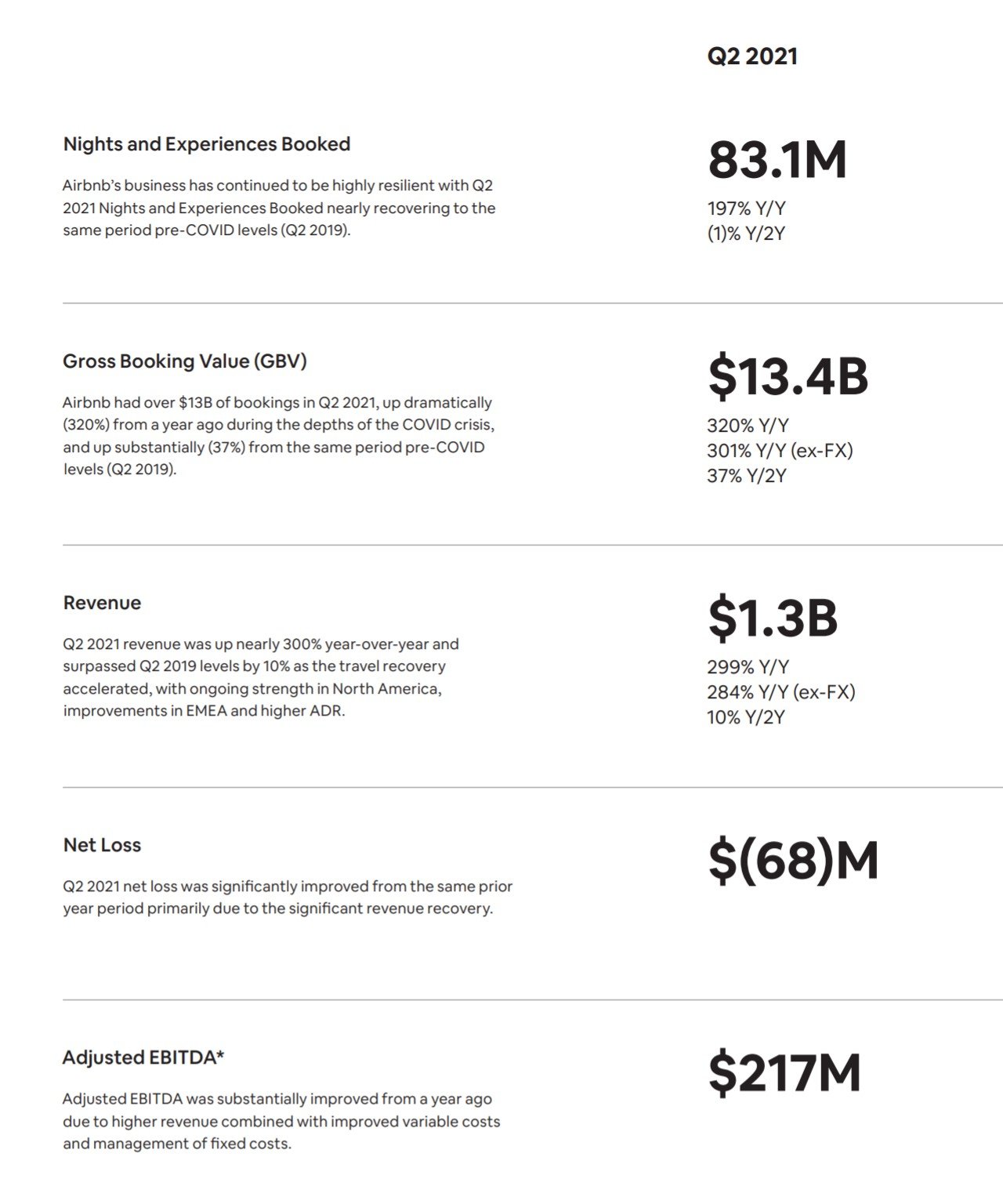

Airbnb had 83 million bookings as at Q2 2021, which is just 1% below pre-COVID levels (Q2 2019).

Once a platform grows this big, the network effects are just ridiculous, and they become incredibly hard to disrupt.

Today Airbnb is listing homes, tomorrow they are listing hotels, car rentals, and Disney park tickets.

They have the potential to grow into the Amazon of travel.

The main competitor I would say is Booking.com.

While Airbnb specialises in home stays, Booking.com specialises in hotel stays. And both are trying to encroach into each other’s space.

If you’re not sure who will win, there a good argument to be made that you should just buy both and be done with it.

Valuations are not cheap though, and investors are pricing in a lot of future growth.

But with their size and network effects, I find it hard to see any other player that can disrupt the Online Travel Agencies in the short term.

Alternatives: Booking.com, Expedia, Trip.com

Meituan

Where Airbnb /Booking.com dominates globally, in China the dominant player to emerge is funnily enough – Meituan.

Trip.com (携程) used to be the number 1 player for the longest time, but Meituan recovered from COVID much better than Trip.com, and today Meituan is the number 1 player in hotel and travel bookings in China (blue bar is Meituan, grey bar is Trip.com).

The numbers are very impressive too (emphasis mine):

Our in-store, hotel & travel segment continued to post steady growth, with revenue growing by 89.3% year-overyear to RMB8.6 billion in the second quarter of 2021. Operating profit increased 93.7% to RMB3.7 billion in the second quarter of 2021 from RMB1.9 billion in the same period of 2020, and with operating margin increasing to 42.6% from 41.6%.

For hotel bookings, demand for travel continued to rise compared to the previous quarter. Our domestic room nights surpassed 140 million for the second quarter of 2021, representing a stellar 81% year-over-year growth, and a two-year CAGR of 22% from the same period of 2019. For high-star hotels, we continued to increase platform supply to meet the changing demand from consumers, and further strengthened our service quality and operational capabilities. For low-star hotels, we solidified our leading position, and continued to penetrate further into lower-tier markets, through the accelerated digitization process and offline traffic conversion.

One potential problem with Meituan is that for now, their hotel bookings are mostly on the lower end range, while Trip.com dominates the higher end.

It’s kind of like the Pinduoduo vs Alibaba vs JD fight, where each player controls a different segment of the market.

So this fight isn’t over just yet.

With Meituan, you’re also buying into the food delivery business, and also exposure to the CCP crackdown.

If that’s not something you’re comfortable with, it may be best to skip Meituan.

Alternatives: Trip.com

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

[mc4wp_form id=”173″]

ExxonMobil

I know I know.

FH has been going on and on about oil for the past 12 months, like a broken record.

I get it, I’m sick of talking about oil too.

But when I look at demand supply dynamics, I don’t see anything changing at all.

Energy producers are still afraid of investing into oil because of the whole ESG movement.

At the same time, oil demand is recovering strongly as the world emerges from COVID.

Not enough supply, rising demand, and you get the chart below:

This trade has made me a lot of money the past 12 months, and I think there could still be room to run.

The biggest risk with oil is a supply increase. There are 2 main swing producers: (1) US Shale Oil, and (2) OPEC.

Idle rigs from US Shale needs about 6 to 12 months to come back online though, so even if you start today you won’t see the new supply kick in until 6 months later.

And US energy investors have learnt to avoid Shale like the plague.

Which leaves OPEC as the swing producer.

OPEC has proven themselves to be very shrewd at manipulating oil prices for a while now (to the detriment of SIA).

Put yourself in OPEC’s shoes. What’s the best course of action going forward?

If you let oil go to $200, global markets will tank, and everyone will accelerate their move away from oil. Bad idea.

If you let oil go back down to $40, you can’t balance your budget, and you have domestic unrest.

The most logical conclusion here is that OPEC will likely have oil trade in the $60 – $100 range going forward.

Not too high that people transition away from oil, not too low that they can’t make money.

Oil has rallied a bit too much too fast, so I would be cautious in the near term. But 1 to 2 years out I still think there’s room to run for these oil stocks.

And if inflation does truly stay with us for a while, oil could just prove to be a fantastic hedge.

Alternatives: Chevron, Conoco Phillips, Shell

Long Term Perspective

A big caveat that this analysis is from a longer term point of view.

Short term stock trading is mostly driven by sentiment and flows.

SIA may be high now, but it can still continue going higher short term if sentiment is very strong.

I’m not disputing that.

For this article, I’m looking at these stocks more through the lens of a longer term investor, with a 3 – 5 year holding period.

Over such time periods, things like earnings and revenue growth will come into play, more than sentiment.

Closing Thoughts

Full disclosure – I hold positions in Airbnb, Meituan, and Exxon. I used to have a position in Ascott REIT too but I sold it in Jan 2020 after the Wuhan lock down, and I never bought back in. Full Portfolio available on Patreon if you’re keen.

I think the obvious conclusion for me from this article is that much of the COVID recovery is already priced into stocks.

The market is efficient like that.

To really make money going forward, you need to think a few steps ahead of the market – into issues like rising fuel prices, rising interest rates, potential reversal of monetary policies etc.

I’ve set out some of the travel related shares that I think could do well in the coming years, but I would absolutely love to hear from you.

What other shares do you think are poised to benefit strongly from the travel recovery?

*Launch of the Stocks MasterClass!*

A lot of you have reached out to ask how to invest in growth stocks, how to allocate between US / China / Singapore, how to position size, when to buy growth stocks vs dividend stocks etc.

You’ve asked about how best to invest in stocks, from the perspective of a Singapore investor.

Now I try my best – but this is something more than what can be shared in my weekly articles.

This calls for an entire framework to investing.

Been working on this the past 18 months – Launch of the Stocks MasterClass! ????????????

Find out more here!