Happy Chinese New year to all readers!

If 2021 was the year of the meme stock, 2022 might just be the revenge of the value stocks.

A year of sticky inflation, 5 rate hikes from the Feds, and quantitative tightening promises to be a tough year for the former high flying growth stocks.

So… What are the top value stocks to buy in 2022?

From the perspective of a Singapore investor?

Rules for selection – Top Value Stocks to buy in 2022, as a Singapore Investor

General rules:

- Taking Prices as they are today

- 3 – 5 year holding period

And I know – I’ve been accused of including too many “ah gong” stocks in my lists.

So in the spirit of taking in reader feedback, I’m going to mix it up a little, and try to keep this list a bit more fresh and dynamic.

Because of that, I will also include an honourable mention list for investors with a higher risk appetite, and who are comfortable with market timing.

Top 5 Value Stocks to buy in 2022 (as a Singapore Investor)

ST Engineering

Market Cap: $11.65b

Dividend Yield: 4.0%

ST Engineering has been trading rangebound for most of 2021, and today is trading at the lower end of its range at $3.6+.

At this price, you’re getting a stock with a 4.0% dividend yield, so at least you’re getting paid to wait.

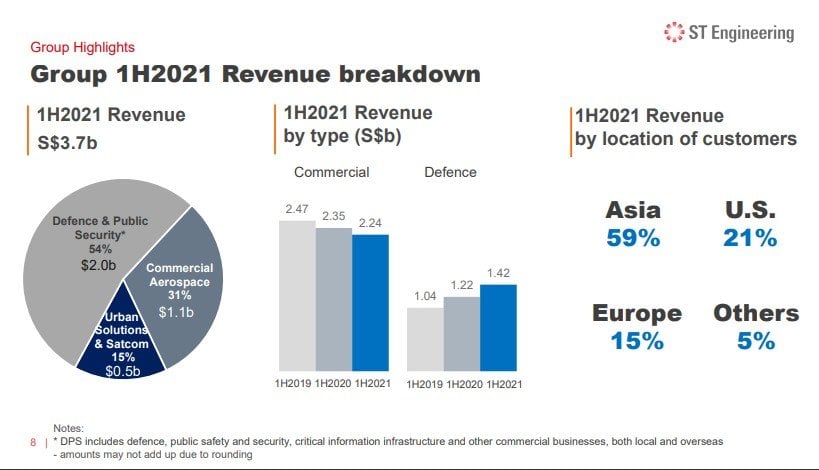

Broad revenue split is set out below.

The biggest chunk is defence (equipment supply to the SAF, 54% of revenue), followed by aerospace (31%) and urban solutions (15%).

Aerospace is recovering very nicely as COVID starts to normalize, and that should accelerate going forward as the less deadly Omicron takes over the world.

There are a couple of red flags to watch out for though.

The commercial revenue has been shrinking for a few years now. So far, the defence revenue has been growing to make up for it, but this is still a worrying trend.

Dividend payout ratio at 90% also indicates the possibility of a dividend cut if there is a big hit to the underlying earnings.

That said, if you remove these red flags the stock would probably trade at $4+, so in some ways this is “priced in”.

ST Engineering is about as boring an “ah gong” stock as it gets, but 2022 might be the year for boring industrial plays like this. Collect the 4% yield, and any upside in stock price is just icing on the cake.

Grab Holdings

Market Cap: US$20 billion

In the spirit of mixing things up, I actually thought Grab kinda made sense to be on this list.

Having collapsed 45% from it’s IPO price, Grab is just $20 billion market cap at latest price.

If it goes even lower I think that could be a fantastic value pickup, as a longer term play on South East Asia’s growth.

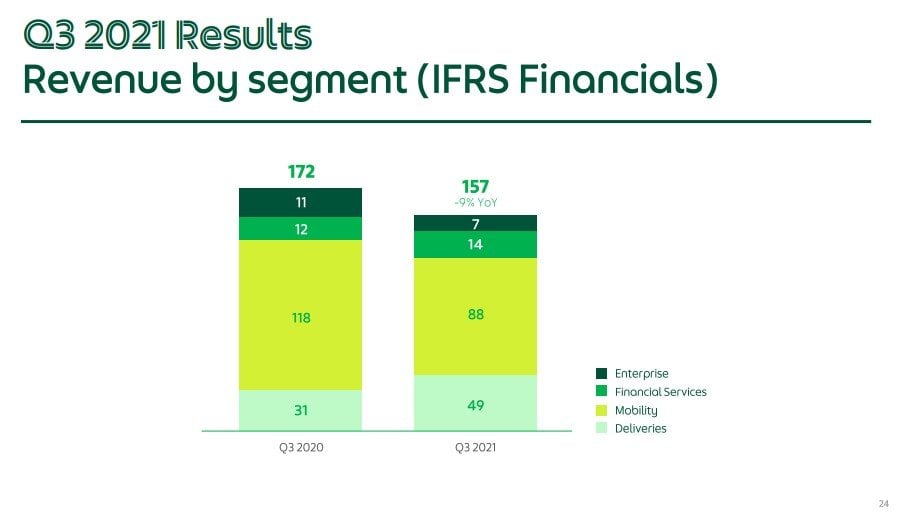

The revenue split for Grab is very interesting:

Key takeaways for me are:

- Mobility (ride-hailing) revenue shrank drastically from 2020 – 2021

- Delivery (food deliver) revenue increased almost 60% in the same period

For now at least, ride hailing is still the biggest revenue generator for Grab, but the delivery and fintech arm are growing nicely.

If you are bullish on South East Asia tech, the only alternatives are Sea ($85b valuation) or Gojek-Tokopedia (rumoured to list at $25 – $30b valuation, which is just a pipe dream now).

Comparatively speaking, Grab could be a decent enough play on the whole platform ecosystem.

They recently won a digital banking license with Singtel, so with good execution that could be a big growth driver too.

The problem is that Grab is still not turning a profit. The delivery business is anticipated to break even soon, but the ride hailing and fintech arms will just be burning through cash in the near future.

Because of that, there’s probably no need to rush into the stock, and 2022 may present better buying opportunities as monetary policy tightening plays out.

Update: I did a deep dive into Grab here, so do check it out if you want to learn more about this stock.

moomoo

If you’re looking for an online brokerage account, moomoo is a low cost trading platform to buy US, HK and Singapore listed stocks.

Fees are competitive at:

- Singapore: 0.03% (minimum SGD 0.99) + Platform Fee of 0.03% (minimum SGD 1.5)

- Hong Kong: 0.03% (minimum HKD 3) + Platform Fee of HKD 15

- US: USD 0.0049 per share (minimum of USD 0.99 per order) + Platform Fee of USD 0.005 per share (minimum USD 1)

Check out my review on moomoo here, and get 1 Apple share (worth ~SGD 220) + SGD 40 cashback when you sign up and deposit SGD 2,700 or equivalent (USD/HKD).

Sign up link here.

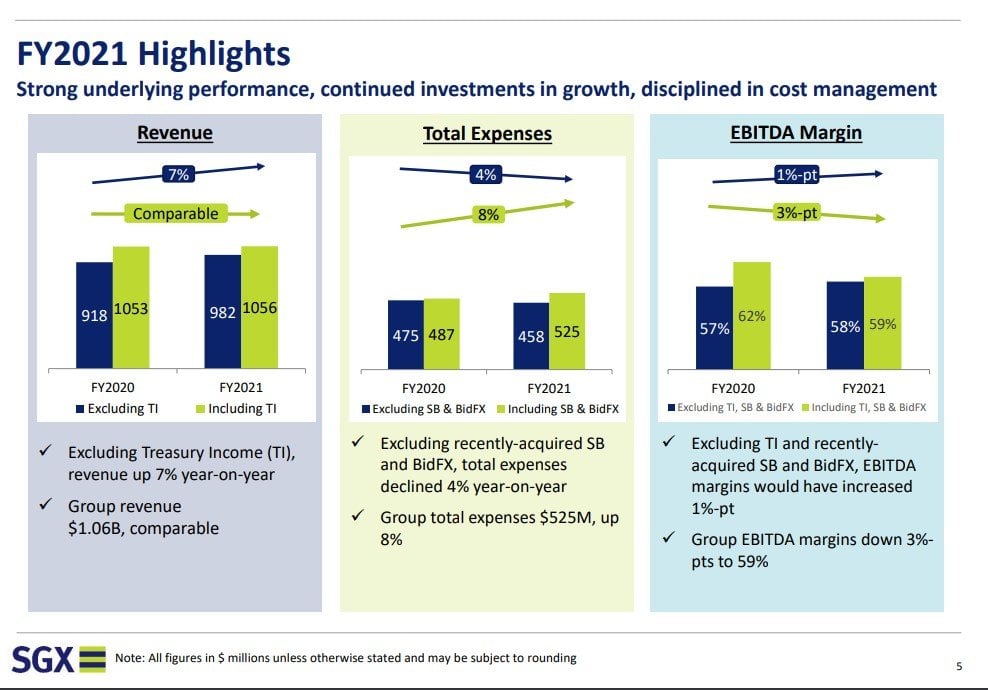

SGX

Market Cap: $10.2b

Dividend Yield: 3.35%

Coming back into boring old-world stocks – here’s SGX.

I’ve never been the biggest fan of SGX because I didn’t see much upside in the stock.

I just couldn’t see where the future growth would come from.

As it turns out, the strategy for SGX might just have been to do nothing at all, and let our biggest competitor (Hong Kong) play itself out..

With all the near-term headwinds that Hong Kong is facing from zero-COVID and Beijing’s clampdown, it looks like Singapore will be the major beneficiary.

SGX’s revenue split is set out below, equities being the biggest chunk, followed by FICC (Fixed Income, Currencies & Commodities) and DCI (Data, Connectivity & Indices).

I mean I still don’t see much growth going forward, but there shouldn’t be material decline in revenue either.

The FY2021 earnings are set out below, and I think that looks about right. Single digit revenue growth, and flat margins going forward.

Dividend is not amazing at 3.35%, but like I said, I think this is a year where returns for asset classes across the board will be muted.

This is not a year to stick your head out with risk exposure, it’s a year to just hunker down and focus on capital preservation.

Survive to the next phase with your capital intact, then go all-in when the Feds start easing again.

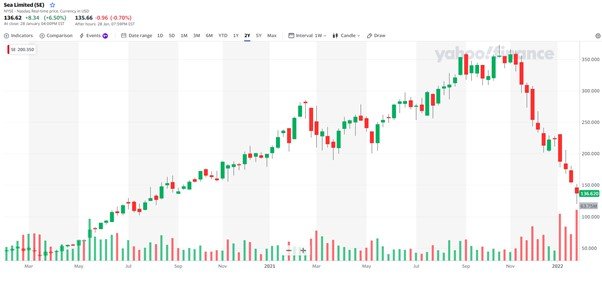

Sea Limited

Market Cap: $85 billion

Last year’s high flying poster boy has been absolutely massacred this year – down 60% from its October high literally just 3 months ago.

That said it’s not fair to single Sea out, because almost all the high flying tech stocks are getting crushed.

I did a fuller piece on Sea recently, so do check it out if you’re keen.

Long story short is that while I agree 2022 will be rough for high beta stocks like Sea, at a certain price it may become a good buy.

They are executing very well on the eCommerce front in their core markets of Southeast Asia, Taiwan and Brazil.

Expansion into Poland, France, Spain and India could bear fruit too.

The fintech arm is also very promising, with Sea having won a digital banking license in Singapore.

Word is that they are executing very well with Seamoney in Indonesia too.

Garena Free Fire (gaming) looks to be slowing, so that will be a big one to watch. Without the gaming business to generate free cash flow, the rest of the business is just bleeding cash to gain market share.

And 2022 is not the year you want to be seen as a bottomless pit of losses.

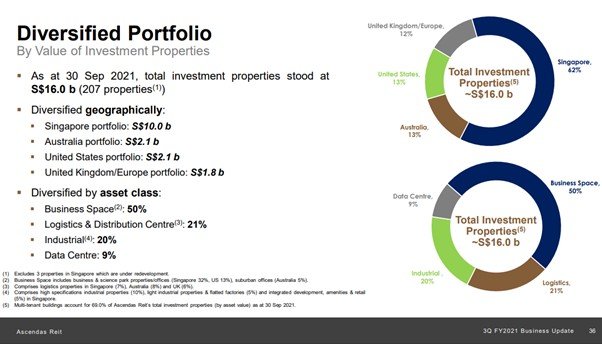

Ascendas REIT

Market Cap: 10.4b

Dividend Yield: 5.2%

Given how cheap most of the blue-chip REITs are trading now, I felt that this list just wouldn’t be complete without including a REIT.

And with REITs – man I just want to buy them all right now.

Mapletree Industrial Trust, CapitaLand Integrated Commercial Trust, Mapletree Logistics etc, I want them all.

I’ve been holding back because I think a better opportunity will present itself before this year is over, but I definitely could be wrong on that.

Whatever the case, I think buying the blue-chip REITs at these prices, and holding them long term, would probably net decent returns.

At current price, Ascendas REIT offers a 5.2% yield, for a broadly diversified industrial portfolio worth $16 billion.

I could get on board with that.

Because Ascendas REIT has already sold off on the interest rate hikes, I think some of the macro headwinds might already be priced in.

But you never really know how things may play out in this new higher inflation / rates volatility regime. So some caution is still warranted.

The next support level might be at $2.5 which goes way back to 2018/2019, and would work out to a 6% yield.

If it ever goes back there, I’m just going to back up the truck and load up.

Honourable Mention – Great Value Stocks to buy in 2022 (as a Singapore Investor)

And now for the list of honourable mention.

These are stocks that I still like, but didn’t make the list for some reason, eg:

- Timing is not right

- Potential Red Flags

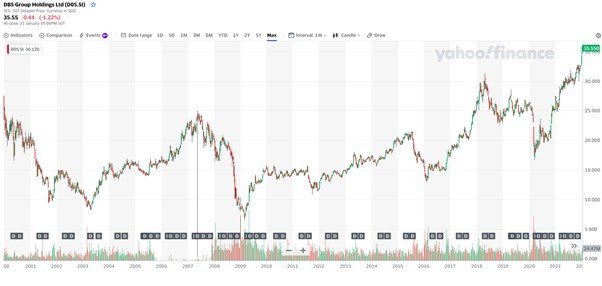

DBS Bank / UOB Bank / OCBC Bank

This is the 20 year chart of DBS, and you can see, banks are about as cyclical as it gets.

Every time investors get overly exciting about rising interest rates, and bid DBS up to a high, you almost always know that a big drop is coming soon.

And I think we are nearing that point.

DBS could probably still go higher from here, but at some point in the future the Feds are going to reverse their monetary policy tightening and the banks are going to come back down to earth.

For a 3 – 5 year holding, I don’t think it makes much sense to buy the banks at current levels.

Better to watch for the Feds to reverse course before adding.

Dairy Farm International Holdings Limited

A lot of you have been asking me about Dairy Farm – and my simple view is that it is a value trap.

Don’t get me wrong, I love the business, and I think supermarket/pharmacy style plays are a good inflation hedge.

The big problem is that Jardine majority shareholding.

Until such point as that is resolved, I frankly don’t see a prolonged uptrend in the stock.

Netlink Trust

I’m a big fan of Netlink Trust.

I loaded up on Netlink back in 2018 the $0.70+ range, and took profit at about $1+.

Hopefully with rising interest rates in 2022 I would get the opportunity to load up again.

The underlying dividend is rock solid (basically “rental” of fibre connections in Singapore).

But with little to no upside because prices are controlled by the IMDA.

This is as utility like a stock you can get, so the key to playing Netlink it to catch it at the right price.

moomoo

If you’re looking for an online brokerage account, moomoo is a low cost trading platform to buy US, HK or Singapore listed stocks.

Fees are competitive at:

- Singapore: 0.03% (minimum SGD 0.99) + Platform Fee of 0.03% (minimum SGD 1.5)

- Hong Kong: 0.03% (minimum HKD 3) + Platform Fee of HKD 15

- US: USD 0.0049 per share (minimum of USD 0.99 per order) + Platform Fee of USD 0.005 per share (minimum USD 1)

You also get access to features such as:

- 100+ Drawing Tools and Indicators

- Heatmaps to identify top performing sectors at a glance

- Stock Screener

- 24/7 Financial News Coverage

- AI-Powered Analytical Tools

All collated in one place, which is pretty convenient:

Check out my review on moomoo here, and get 1 Apple share (worth ~SGD 220) + SGD 40 cashback when you sign up and deposit SGD 2,700 or equivalent (USD/HKD).

Sign up link here.

Closing Thoughts: Top 5 Value Stocks to buy in 2022 (as a Singapore Investor)

And there you have it – Top 5 Value Stocks to buy in 2022, as a Singapore Investor.

That being said, I don’t think 2022 is the year to try to be too clever with fundamental stock picking.

This is a year to respect the broader macro, and respect the money flows.

When things sell-off, the market will throw the baby out with the bathwater.

Switch into fundamental stock picking mode only when the dust settles.

With the Feds switching into 5 rate hikes and Quantitative Tightening in the span of 12 months, I think something is going to give way in the markets, sooner rather than later.

As always – love to hear what you think!

All views expressed in this article are from Financial Horse.

No content herein shall be considered an offer, solicitation or recommendation for the purchase or sale of securities, futures, or other investment products. It does not take into account your investment objectives, financial situation or particular needs. All information and data, if any, are for reference only and past performance should not be viewed as an indicator of future results. It is not a guarantee for future results. Investments in stocks, options, ETFs, and other instruments are subject to risks, including possible loss of the amount invested. The value of investments may fluctuate and as a result, clients may lose the value of their investment. Please consult your financial adviser as to the suitability of any investment.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

Gong xi fa cai FH. I hold SGX exactly because it’s going nowhere, as such it falls under my ‘safe dividend’ basket. Maybe this year you should be Financial Tiger hahaha

Hope u dont end up pig for market, or worse donkey. Buying those SGX stock suck big time,

I think u better ioff buy GOOG MSFT or FB.

Haha Gong Xi Fa Cai LME! Interesting – for your SGX holding, do you plan to trade it, or just hold long term and collect the dividend?

My plan is to treat it like a perpetual bond. Under this framework, I look for low beta stocks, stable core business, decent dividend yield at 3% and above. So yes, I am holding long term and just eat the dividend, which means forever unless I really need the money.

On trading, I will also consider trading if there is a good opportunity. For example, between End 2020 – Mid 2021 was a good trading opportunity. The $11 price then was totally over-optimistic. But such windows come once every 5 – 10 years for SGX stock.

Would you consider energy plays in Singapore like Sembcorp industry Sembcorp marine Keppel Corp?

Yes, open to consider. Most of the oil majors have been bid up very strongly, so if I wanted to bet further on the oil recovery it might have to be via the oil services players which havent recovered so much yet.

sgx , netlink and VICOM are like high-yield fixed deposits.

ST eng is backed by ah gong. When it crashes, you can safely hoot and wait for rebound, won’t go wrong..

seriously, dairy farm ???

and grab and SEA are “value”??? more like money sucking blackhole. lol really don’t understand what’s your obsession with SEA?

lol, have you run out of content? going back to writing sg zombie stocks again ?? wouldn’t it be better if you write new areas like biotech, future tech, quantum, etc.

Haha alright! Will consider writing on such areas. The problem if I do is that people will freak out at the 50 times Price/Sales, so can’t please everyone I guess. 😉

honestly, you think Southeast asia can rise fast meh? look at our neighbouring countries …. sg will probably be still the most developed for a few more decades, i don’t see nearby countries catching up that fast.. well except maybe vietnam. .. there are some sensitive i don’t want to write in this public space, but i think we all know the reasons ..

Hi FH,

Interesting post. When you said value stocks, I thought the list would be filled with Ah Gong Reits as they are at lowest in quite some time so qualify as value already although they can become even cheaper before turning around as you mention.

Surprised to see Tech like Grab and Sea on list. I am skeptical they can be called value…Grab hasn’t shown an ability to make a dime yet and are continuing to bleed money fast. Tencent and Alibaba would be much better value than these 2 in my view.

Yeah, if I had my way this list of stocks would be FAANG + CapitaLand/Mapletree REITs. But then where’s the fun in an article like that.

So I wanted to mix it up a little in this article. There is a risk that growth stocks may overcorrect this year, so I wanted to get readers to think outside the box. Just like how 2020 was a great opp to buy banks/oil, this year might be a great chance to buy growth.

Happy CNY Chan Mali Chan! 虎年大吉!!!

This year gonna be volatile, their valuations might drop soon. Imvestors should invest in the future tech. Also its always good to know more about other tech areas than the usual SaaS and faang. Out of Faang , fb and netflix growth forward are dubious given their share price dropped so much recently— funds have their doubts. Apple is also peaking. Very reliant on phone and services sales. We need to look for smaller cap to bet on for huge returns going forward. Increasingly i am staying out of bigtech except for chips stocks. Most SaaS are far from profit and dubious whether they can fight the bigtech monopolies

Alright, will see if I can cover more tech going forward. This might be a great year to pick up growth.

Just felt that there is some contradictions. In this article, Grab is recommended to buy. But in another latest article, it was mentioned that you wont recommend buying Grab even though it is currently priced much lower than its IPO price.

Yes after doing a deeper dive into grab I changed my mind on the counter. 🙂

How about ComfortDelGro an asset heavy, cash generator/ dividend payer that makes money from ‘mobility’. I think Grab is a falling knife but CDG has almost certainly bottomed out.

I actually bought CDG in mid 2020 based on this thinking but closed it for a small profit 6 months later. I think the risk is that it could be a value trap. Could be wrong, but I see better uses for the cash elsewhere.

But that said I definitely get the appeal of CDG, it’s just not for me.

Dear sir, An analyst friend of mine has recommended purchase of growth stocks like AEM holdings and Nanofilm technologies after this recent correction.

He says in these 2 counters we can double our money in a few years time and are .among the best buys on the STI for the Singapore investor who is looking for growth stocks to invest in.

What is your opinion?

awaiting your reply, thank you

.

Haha well, good for him to have such strong conviction!

For me I’m a lot more cautious. Rising rates and QT are going to be massive headwinds in 2022.