This article was submitted by a Guest Contributor. The opinions expressed in this publication are those of the Guest Contributor.

Thanks to the wonderful world of Reddit, we have compiled some horror investment stories from Reddit users, sharing the worst investment advice they have received over the years.

Hopefully, we can learn from their painful lessons!

PSST! Financial Horse has started a new Reddit thread for Singapore Investors – Join here!

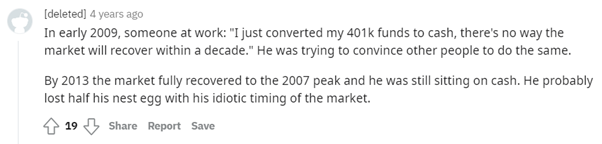

1. Cashing out at the first signs of trouble

While it may seem natural to offload stocks during a financial crisis or during any major economic event to avoid losses, sitting out of the market for excessive periods of time, can cost you.

Also the fear of getting back in, or finding the “perfect time” to get back in, can often paralayze investors into inaction.

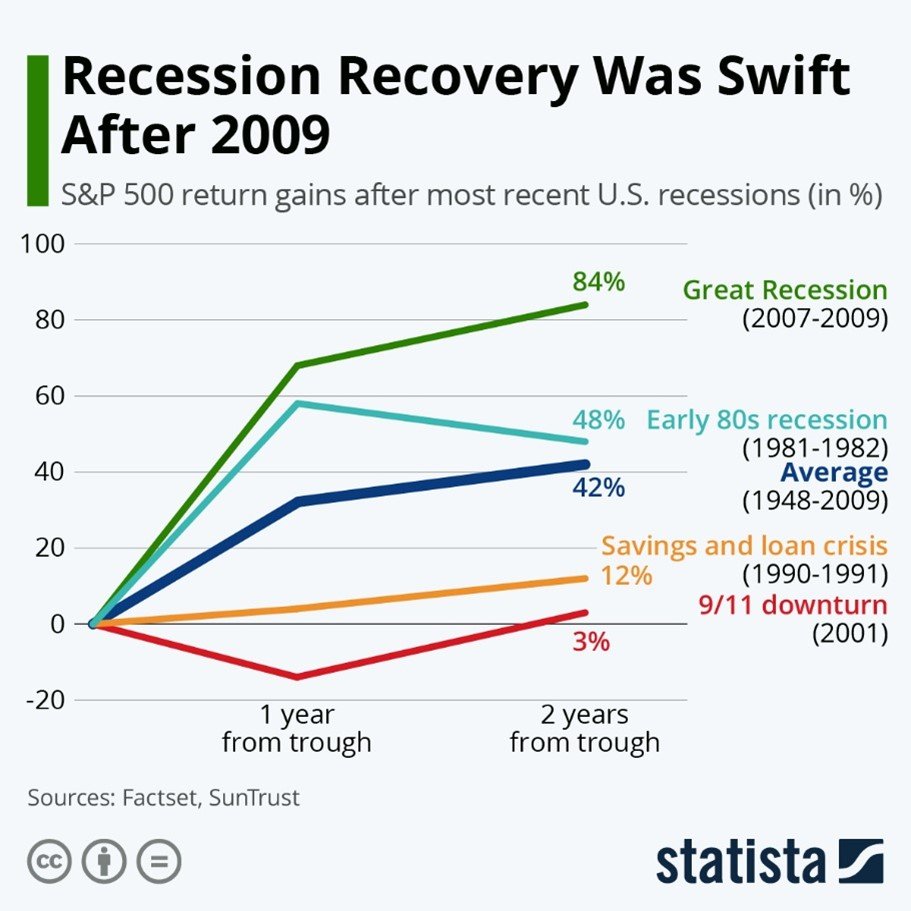

Source: Satista

The chart above demonstrates that the greatest gains in the S&P 500 comes fairly quicly after a crash in the market.

David Ragona, director of retirement operations at 401(k) provider Human Interest, told CNBC that “If 200 years of stock market history is any indicator, it is likely that investment markets will rebound from negative news and price declines.”

Following the most recent March 2020 sell-off due to the COVID-19 pandemic, it took only 6 months to reach pre-pandemic levels and the markets have continued to soar another 30%.

Of course, these are simplistic analysis of market timing, but the overall point is that very often, it pays to stay invested, rather than hope to be able to pull out your money, and re-invest at the “right” time later.

Crucially, signs of financial market recovery are often very difficult to pinpoint. Charlie Munger, vice chairman of Berkshire Hathaway, noted during its 2021 AGM, that it is impossible for Berkshire, much less for ordinary retail investors, to accurately predict the bottom of the stock market and anyone who expects Berkshire to do so is “out of his mind”.

If one of the world’s best asset managers isn’t hoping to predict the bottom of a crisis, you shouldn’t too.

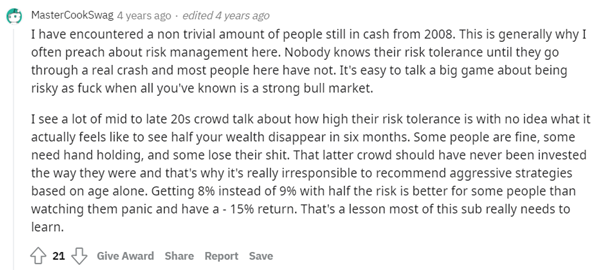

2. Understanding your true risk tolerance

In tandem with staying invested during a financial crisis, it is important to understand your appetite for risk.

The above redditor rightly points out that a lot of younger investors have only known a strong bull market.

What happens when you actually see your stocks crash in your portfolio? Can you really remain calm and not panic sell?

Vanguard, the world’s largest provider of low-cost mutual funds, notes that investors can adjust the percentage of bonds and equities portfolio to match their risk tolerance. A portfolio with higher allocation to bonds generally enjoy lower capital gains, but also has less deviation between its best and worst performing years – hence, may be suitable for lower risk investors.

Beyond portfolio allocation, investors need to be aware of volatilities in certain industries and geographies. For example, stocks of technology and internet companies are notoriously volatile. Investments in China are also known to be risker given the regulatory climate (see Financial Horse’s post on the China Tech Crackdown!).

It is important to allocate your assets to suit your risk appetite – and to understand the broader macro climate that your investments operate in.

3. Using Leverage to invest

While it is not uncommon for major financial institutions and sophisticated investors to use leverage to enhance their returns, doing so as a retail investor can be very dangerous. This is also closely related to #3 understanding your true risk tolerance above.

If you’re a long-term investor planning for your retirement, you would need to be mindful of the risks of leveraged investments.

The March 2021 collapse of Archegos Capital Management showcased the epic destruction of untapered risks. The aftermath of the collapse contributed to more than US$10 Billion in losses to banks who were providing that leverage.

In Singapore, trading Contract for Difference (CFDs), are a widely used instrument to leverage trade positions. However, it is important to be sure you know what you’re getting into before you opt for such higher-risk strategies.

We’ve also seen countless “options” courses being advertised on social media – definitely do your own due diligence before embarking on such investing strategies.

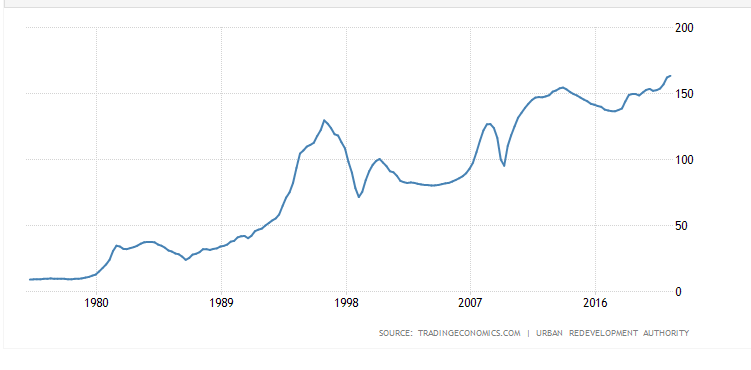

4. Property investments as “safe-havens”

The idea that property is a “never-go-wrong” asset is particularly relevant to Singapore investors.

The fact that our land is limited, and the incredible gains that previous generations have obtained from investing in real estate, has ingrained this mentality into our heads.

Singapore Residential Property Price Index

Source: Trading Economics/URA

However, as housing prices has increased significantly, it remains to be seens whether property investing can return the same type of gains as before.

While it definitely remains a viable asset class for Singapore investors, new investors may need to have a more realistic view of the potential returns in the future.

The recent Paris Ris 8 launch raised eyebrows on the price hikes for available apartments, with DBS calling it “3 years’ worth of price action in 1 day” given that a 2-bedder was going for as high as S$2k psf.

While it is uncertain whether valuations were frothy, it does raise the question if property owners are risking too much on the “guarantee” of capital gains or rental yield – especially at these eye-watering psf.

Additionally, because of land-scarce Singapore, property remains a high-ticket item for most Singaporeans. A $1,000 stock trade gone wrong is something many investors can stomach, but a $1,000,000+ property purchase? Not so much.

The Department of Statistics Singapore showcases that approximately 50% of a Singaporean’s household wealth comes from residential property assets.

“You must understand that the nature of buying property has changed – few can fit into investment objectives of exiting (profitably) in 3-6 years,” says Kevin Feng, PropNex group district director.

Mr Feng also cites the 20% additional buyer’s stamp duty (ABSD) on Singapore property purchases as one of the biggest obstacle to a quick flip.

Many Singaporeans have also turned to overseas destinations as a result – which offer “lower-priced” property prices.

However, in many Southeast Asia destination popular with Singapore investors, political climate and forex risk remains a big concern. For example, Myanmar or even closer to home JB, has left many property investors burnt.

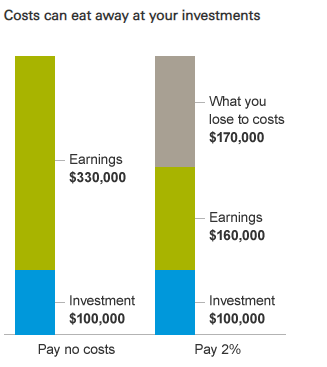

5. Fees don’t matter

In today’s age of low-cost passive index investing, it is easy to forget the hefty impact of recurring fees.

Source: Vanguard

As illustrated by Vanguard, the impact of 2% difference in fees over 25 years would generate losses of almost 40% of one’s final portfolio. It is therefore always important to keep a close eye on fees that brokers or providers of mutual funds charge.

In Singapore, common recurring brokerage fees are Custody Fees. Recurring fees, usually displayed as an expense ratio, can also be found for almost all low-cost index or mutual funds.

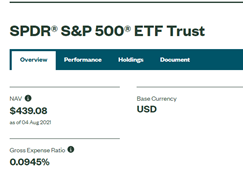

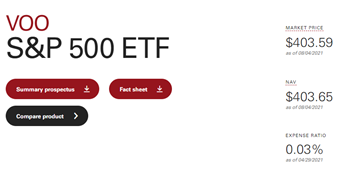

For example 2 funds tracking the same S&P 500 Index, the SPDR S&P500 ETF Trust and the Vanguard S&P500 ETF have different expense ratios, with SPDR’s triple that of Vanguard’s.

It is important for investors to take note of these fees, especially recurring ones, if they hope to maximize gains from their long-term investments.

Conclusion

The above 5 categories of investing mistakes/advice serve as a timely reminder for investors.

Let’s learn from our fellow Reddit investors and be mindful of our investing strategies and risk tolerance.

This article was submitted by a Guest Contributor. The opinions expressed in this publication are those of the Guest Contributor.

Join Financial Horse’s Investing Community!