There’s never been a better time to be a cash heavy investor.

Whether it’s Fixed Deposit, T-Bills, Singapore Savings Bonds, or money market funds, you’re looking at some of the highest yields on cash in over a decade.

In today’s article, I wanted to discuss the UOB Stash Account, which offers an interest rate of up to 5.00% p.a. on $100,000.

The main highlight of this account is that there are very few hoops to jump through.

Unlike a UOB One account, or DBS Multiplier or OCBC 360 where you need to (1) credit your salary and (2) spend a minimum amount on credit cards.

The only requirement for UOB Stash Account is that the average month balance of the account should not be lower than that of the previous month.

So for retirees or students that don’t have a salary.

Or if you already have a UOB One / DBS Multiplier / OCBC 360 account and want another high yield savings account (instead of locking it up in T-Bills or Fixed Deposit).

UOB Stash Account is well worth looking into.

What is the UOB Stash Account?

The UOB Stash Account is a savings account with UOB Bank.

It allows you to earn up to 5% p.a. on your money held with UOB.

Interest gets paid out monthly and there’s no lock-in period – so you can withdraw your money any time!

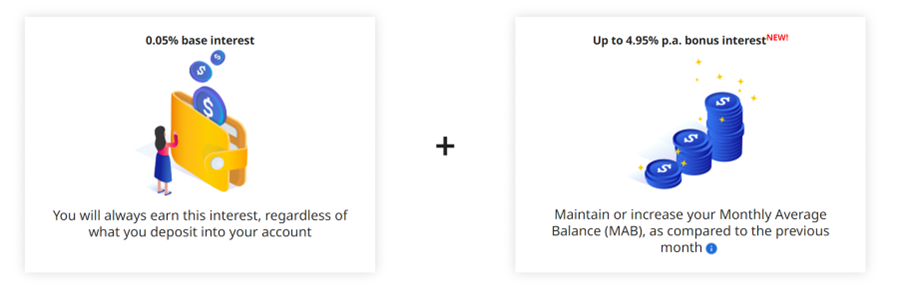

What is the interest rate for the UOB Stash Account?

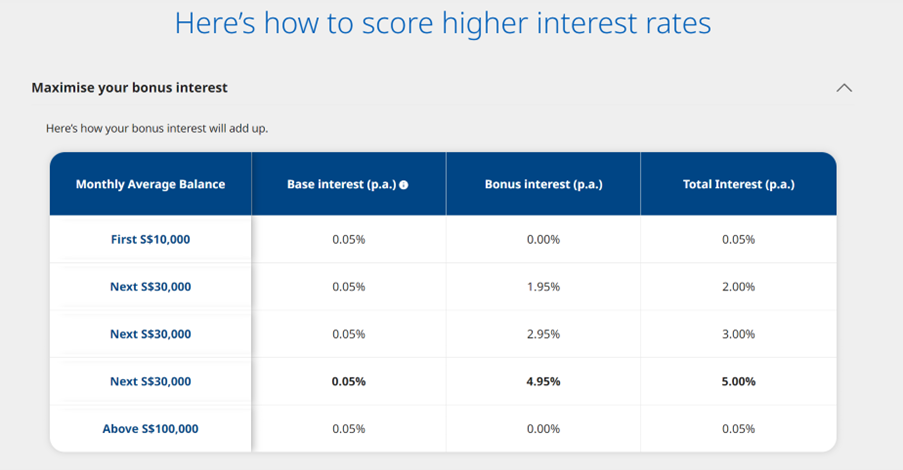

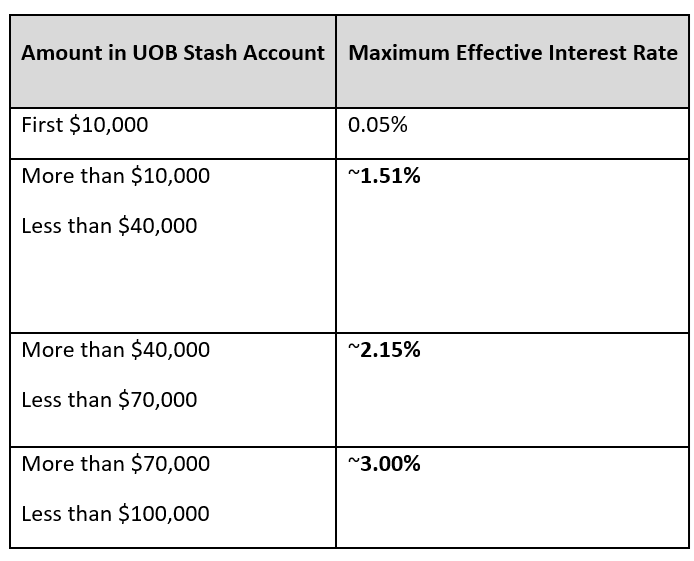

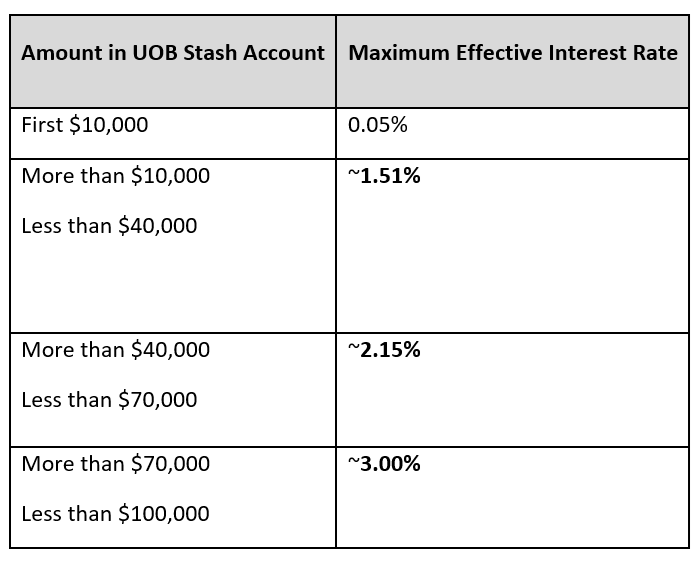

The breakdown of interest rates for the UOB Stash Account is set out below.

It starts out at 0.05%, and then steps up to 5.00% depending on how much you hold in UOB Stash Account.

I’ve computed the effective interest rate on the UOB Stash Account below:

|

Amount in UOB Stash Account |

Maximum Effective Interest Rate |

|

First $10,000 |

0.05% |

|

More than $10,000 Less than $40,000 |

~1.51% |

|

More than $40,000 Less than $70,000 |

~2.15%

|

|

More than $70,000 Less than $100,000 |

~3.00%

|

Effectively, if you hold $100,000 in UOB Stash Account, you are looking at 3.00% p.a. interest.

If you plan on putting less than $100,000 in though, do note that the effective interest rate may not be as attractive.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

What do you need to do to enjoy the UOB Stash Account Interest Rates?

Unlike other accounts like UOB One / DBS Multiplier / OCBC 360 which have a whole slew of requirements you need to fulfil (mainly to spend a minimum amount on a credit card and credit your salary).

There is only 1 simple requirement to enjoy the UOB Stash Account interest rates.

The monthly average balance of the UOB Stash Account needs to be equal to or higher than that of the previous month.

That’s all there is to it.

Say you put $100,000 into the UOB Stash Account, and just leave it there, you’ve already fulfilled the requirements.

This is a huge advantage for retirees or students who don’t draw a salary.

Or for those who draw a salary but have it credited into another high yield savings account (and want another).

How does the 3.00% interest compare to other available options available?

Okay for the record – I get that the 3.00% is not as high as the yield on the latest T-Bills or Fixed Deposit.

But you do have to realise that there’s an important advantage with UOB Stash Account in that this is a savings account – you can withdraw the money any time you want.

Whereas with a T-Bill you may not be able to get your money back before maturity easily.

And with a Fixed Deposit breaking it early will forgo all the interest.

And comparing UOB Stash Account with something like a DBS Multiplier or OCBC 360 account is not really fair too, because those require salary credit and minimum spend on credit card.

What are the alternatives to UOB Stash Account?

So the real comparison is to a savings account that doesn’t require you to jump through any hoops.

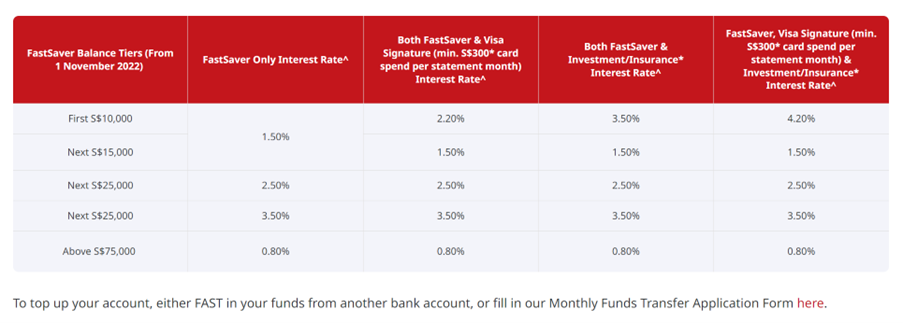

The CIMB FastSaver Account is one such alternative.

The effective interest rate is 2.5% p.a. on $75,000.

It’s still below that of UOB Stash Account, but can be considered if you don’t have $100,000 to stash away (pun fully intended).

This is probably the best alternative to UOB Stash Account I could find.

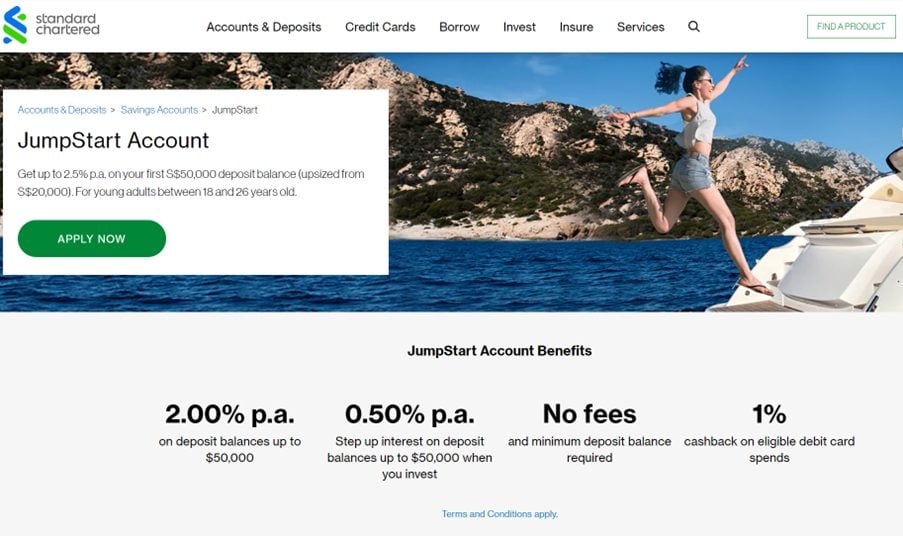

The Stanchart JumpStart Account offers 2.00% p.a. on deposit balances of up to $50,000, but you must be between 18 and 26 years old to open a SCB JumpStart account.

Many investors may not qualify for the age range unfortunately (but if you do it is worth checking out).

And then there are savings accounts like Trust Bank which offers 1.5% on $75,000.

Or Singlife with 1.4% on $100,000.

How does the UOB Stash Account compare to other savings accounts?

I’ve set out the comparison table below.

If you have $100,000 to set aside, UOB Stash Account has the best rates.

|

Account |

Effective Interest Rates |

Remarks |

|

3.00% on $100,000 |

Monthly average balance cannot be lower than previous month |

|

|

2.50% on $75,000 |

|

|

|

2.00% on $50,000 |

Must be between 18 and 26 years old |

|

|

Trust Bank |

1.5% on $75,000 |

|

|

1.4% on $100,000 |

|

What are the drawbacks with the UOB Stash Account?

The main drawback of the UOB Stash Account is that you need to maintain or increase your account balance from that of the previous month to qualify for the bonus interest.

So for example if you hold $100,000 in the UOB Stash Account in May 2023.

And in June 2023 you decide to take $1,000 out.

Then you lose the entire interest on the remaining $99,000 for the month of June.

But you will continue to earn interest in July as long as the $99,000 does not drop further.

It’s definitely an annoyance, but I don’t think it’s a big problem as long as you work around it a bit.

For example you can try to draw on other accounts first before touching the UOB Stash Account.

And if you need to draw from the UOB Stash Account, it makes sense to draw a big amount rather than just touching it for $100 and losing that month’s interest.

So I don’t see it as a big problem, considering that the upside is that you get full liquidity from the money in the form of a savings account.

If something unexpected happens and you need the money, all the funds can be transferred out immediately.

Unlike say T-Bills or Fixed Deposit or Singapore Savings Bonds, where you may need to wait a while until you can get your money back.

My Personal Views on the UOB Stash Account?

Personal views – I don’t think the UOB Stash Account will work for everyone.

You can see from the table below that you only enjoy the full benefits if you can put a full $100,000 in UOB Stash Account.

Investors who are not prepared to leave that amount idle in a bank account might be better off with Fixed Deposit or T-Bills.

But for those who can, and want something fully liquid (instead of T-Bills or Fixed Deposit), it’s well worth checking out.

Note that the 3.00% is actually higher than the yield on the latest Singapore Savings Bonds.

Considering that the money is fully liquid, it’s a pretty attractive option in my view.

I myself opened a UOB Stash Account recently and put some money in there, as a liquid source of funds.

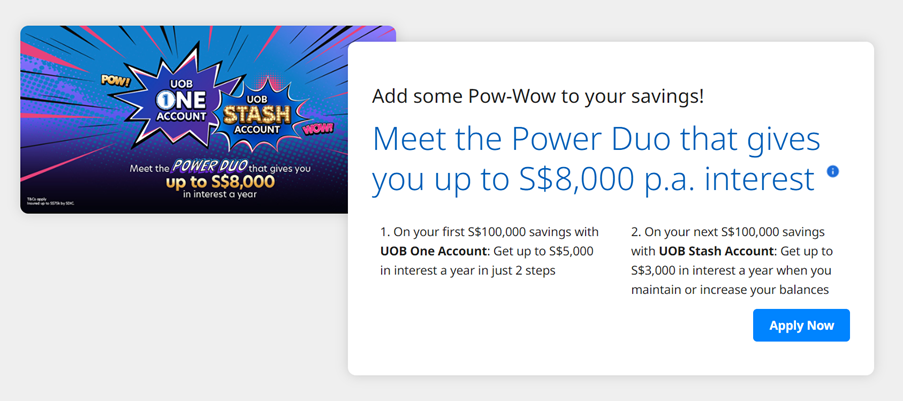

UOB Stash Account + UOB One Account – 4.00% Interest on $200,000

UOB is also hyping up the fact that the UOB One Account and UOB Stash Account go very well together.

The thinking goes like this.

UOB One Account offers the highest interest rates in Singapore for a high yield savings accounts.

If you credit your salary and spend $500 a month on UOB credit cards, you can earn 5.00% on $100,000.

But any amount in excess of $100,000 in the UOB One account only earns 0.05%.

What if you have more than $100,000 that you don’t want locked up in a fixed deposit or a T-Bill?

Well, that’s where UOB Stash Account comes in.

If you put S$100,000 into the UOB One Account and earn the maximum effective interest rate of 5% p.a., and another S$100,000 into the UOB Stash Account and earning the maximum effective interest rate of 3% p.a., you’d earn a total interest of S$8,000 in a year.

That’s basically 4.00% p.a. on $200,000, which is a pretty respectable interest rate.

So yeah, if you have $200,000 lying around that you want to earn decent yield on, and keep it fully liquid such that you can draw on it any time.

UOB One + UOB Stash Account is a good option.

Account Opening – UOB Stash Account

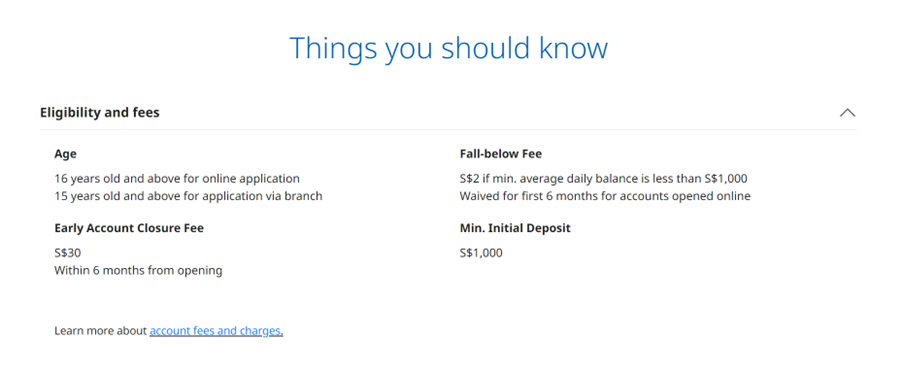

Do note that the minimum balance for the UOB Stash Account is S$1,000.

If your monthly account balance falls below S$1,000, a $2 fall-below fee will be imposed.

However – this fall-below fee is waived for the first six months for UOB Stash Accounts opened online.

Almost anyone can open an account too.

You don’t need a salary, and you can open an account as long as you are 15 years old and above.

Account Opening Promotion for UOB Stash Account (Up to $210 Lazada vouchers)

There is also an account opening promotion for UOB Stash Account now.

Basically – you can get up to $210 Lazada vouchers if you:

- Open a new UOB Stash Account online

- Deposit at least $5000

- Hold them until the end of the following month.

I’ve extracted the Terms & Conditions below, you can read the full T&Cs here if you are keen.

1) Up to S$210 worth of Lazada cashback vouchers with an additional of up to S$60 cash credit is for customers who have successfully satisfied the relevant conditions of the UOB Online Account Opening Promotion (1 May to 31 July 2023):

- Up to S$210 worth of Lazada cashback vouchers will be awarded to ALL customers who (i) successfully open a UOB Uniplus Account, UOB Lady’s Savings Account, UOB Stash Account, KrisFlyer UOB Account or UOB One Account online from 1 May to 31 July 2023, (ii) deposit at least S$5,000 of Fresh Funds into their new UOB account during the calendar month which their new account opening month falls within, and (iii) hold the deposited Fresh Funds till the end of the following calendar month.

- S$60 cash credit will be awarded to the first 200 New-to-UOB-Deposits customers per calendar month who meet (i) to (iii) mentioned in (a) above.

- S$30 cash credit will be awarded to the first 200 Existing-UOB-Deposit customers per calendar month who meet (i) to (iii) mentioned in (a) above.

How to apply for the UOB Stash Account

To open a UOB Stash Account, follow these simple steps.

Step 1: Visit the UOB Stash Account website

Step 2: Click on “Apply now”

Step 3: You’ll be prompted to login into your UOB account if you already have one

And that’s about it!

I submitted my application online and had it approved within minutes, after which you can use the account immediately.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!