For the record – I detest war.

I think that in this day and age, sending young men or women to die, whatever the political cause, is unforgivable.

But this is a finance blog, and I’m going to leave the discussion about what the West (or Russia) should / should not do to others.

In this article, I’m going to focus exclusively on how I think this Ukraine war will play out, and the impact on financial markets.

Russia is a major commodities producer

The first thing to understand – is that while the Russian economy is small in the grand scheme of things (GDP smaller than Italy), it is a major commodities producer:

Oil – Russia is 3rd largest oil producer in the world, with 11% of world’s supply (after US and Saudi Arabia)

Wheat – Russia and Ukraine supply 29% of global wheat

Natural Gas – Russia supplies 40% of Europe’s natural gas

Palladium – Russia supplies 40% of world’s palladium

Aluminium – Russia supplies 6% of world aluminium

And what is the world short of right now?

Exactly the stuff that Russia produces – commodities.

You can see the impact on commodity prices the past month.

Oil up 10%, Wheat up 11%, Aluminium up 13%.

The only one that hasn’t moved in a big way is natural gas, because the preliminary indications are that sanctions will leave Russian natural gas untouched.

And when you zoom out and look at year to date charts, here’s what the numbers look like.

19% increase in soybean prices. 27% for oil. 40% for coal.

Pretty ridiculous numbers considering we’re only 2 months into the year.

Will Commodities prices go even higher?

So Russia produces a lot of the commodities the world needs, very desperately.

Whether the price of these commodities will go even higher, is going to depend on 3 things:

- How long will the Ukraine war last?

- How will EU/UK/US respond with Sanctions?

- How will Putin respond to Sanctions?

Question 1 – How long will the Ukraine war last?

War is war, and you should never expect the information coming out of either country to be reliable.

And there is significant uncertainty over how long this war will last.

What is Putin’s endgame?

Nobody even knows what is Putin’s endgame here.

Some may say that it is to prevent Ukraine from drifting towards the West, and it’s a national sovereignty issue for Russia.

The more cynical may say he’s doing this just to stay in power.

Others may say that he’s lost touch and become unhinged, hellbent on redrawing Russian borders to recreate the Soviet Union.

What I would say, is that whatever you see in the media about Putin, is what he wants you to see.

So that emotionally charged speech he gave about Soviet history, Nazification of Ukraine etc.

All a show.

And I would caution against jumping to hasty conclusions on what Putin really wants.

The only person who knows is Putin himself.

A Blitzkrieg, or Russia’s Vietnam?

Because of that, the range of possibilities are very high.

Early indications are that Russia is facing stiffer resistance than expected on the ground.

But again – war is never easy to call.

The war could be over by this weekend. Or it could drag on to Christmas.

If I were forced to make a call, I would say that the base case is that the Ukraine war shouldn’t last long, and military escalation should be limited.

But the longer this goes on, the higher the possibility of miscalculation by either party.

Question 2 – How will EU/UK/US respond with Sanctions?

Putin is tough to predict, but the West is much easier.

Barring a significant escalation in the conflict, I frankly do not see the EU/UK/US responding in a manner that would severely impact Russian commodities exports.

The initial sanctions are in line with this.

Sure, a couple of Russian billionaires can no longer access their offshore accounts. The ability of Russians to get loans offshore has been curtailed.

Boohoo.

But we don’t see any of the nuclear options. Russia still has access to SWIFT. Natural gas is still flowing to Europe.

The west has already expressly ruled out boots on the ground, so the probability of military escalation from the West is not high.

My base case here is more of the same. Lots of “thoughts and prayers” with Ukraine, but no significant sanctions or military escalation from the West.

Update (28 Feb): With the announcement on Russian Banks being removed from SWIFT, and measures to be taken against Russia’s Central Bank reserves, this assumption is now no longer valid. The implications of this are actually very deep and far ranging, and I will be doing a Patron post to update.

Question 3 – How will Putin respond?

If the EU/UK/US doesn’t respond in a big way, neither will Putin.

Again – Sure, some diplomats will be sent home (if they haven’t already). Some flights from EU to Russia will be stopped.

But no nuclear options. Russian commodities will continue to flow into the West, and commodity prices stay within the current range.

BUT – What if something goes wrong?

But, the thought process above shows the key question mark is Question 1 – How long will this war last?

War being war, many things can go wrong here.

Ukrainian soldiers can put up a tougher resistance than expected. Russian forces can go deeper into Ukraine than expected.

And the longer this drags on, the higher the potential for miscalculation.

Maybe a port in Ukraine gets blown up. A key natural gas pipeline. A key transportation railway.

Once that happens, commodity prices may spiral out of control very quickly, and global supply chains may deteriorate further.

Feds are forced to hike interest rates?

I’ve see a lot of takes that the Feds will be forced to stop rate hikes because of Ukraine.

I think that’s just absolutely nuts.

US inflation is running at 40 year highs, and now war in Ukraine which will worsen supply chain disruptions and commodity prices.

And your solution is to keep interest rates at zero?

The Fed is so behind the curve here it’s no longer funny.

Had they stopped QE and done a couple of rate hikes earlier they would at least have some tools in the box to respond to the Ukraine war.

But with inflation at 40 year highs and the Feds still doing QE and at zero interest rates, I just think policy wiggle room here is incredibly limited.

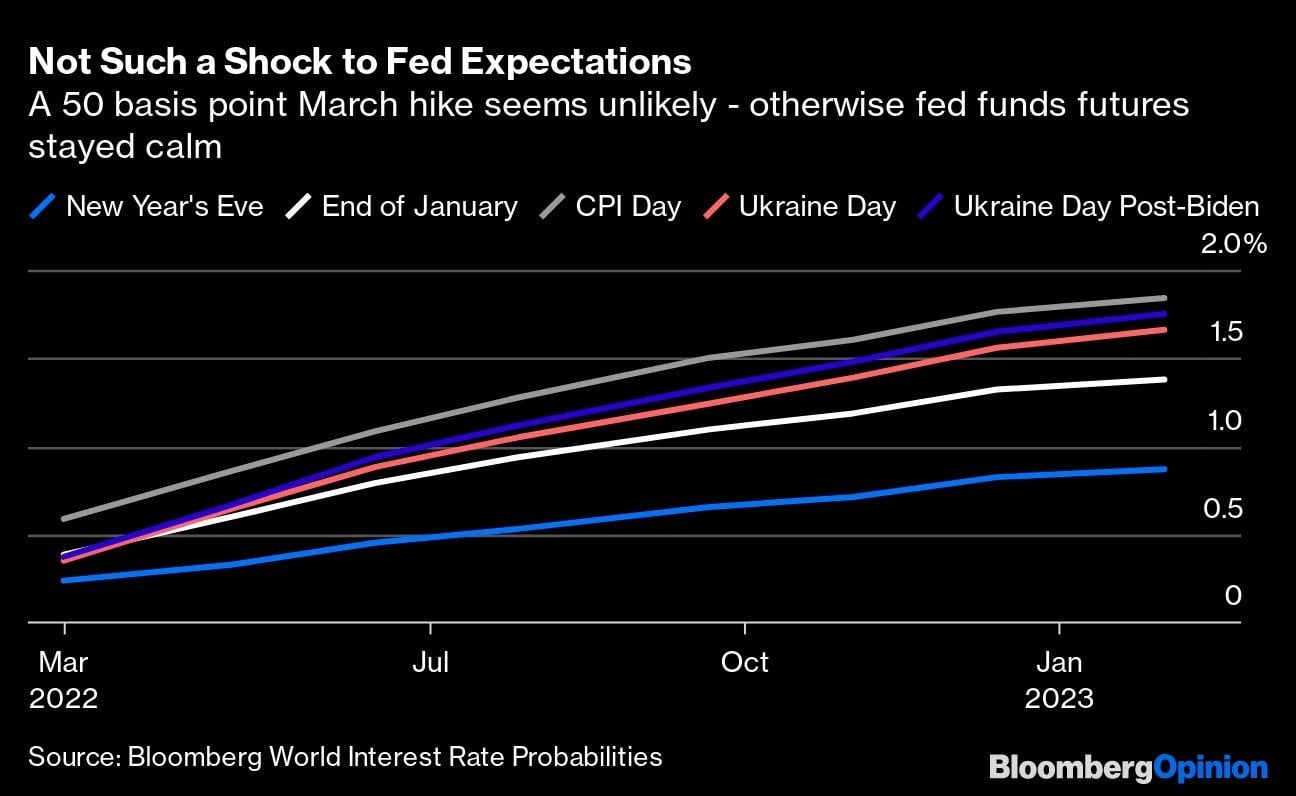

For what it’s worth – the market agrees with me.

All that has changed after the war started is that a 50 bps hike in March is now off the table. But the pace of rate hikes is still expected to be fast and furious, at 1.5%+ by Jan 2023.

I don’t think this is the bottom for 2022

Now for the record – I don’t think we’ve seen the bottom for 2022.

We haven’t even had the first rate hike for crying out loud.

That said, I still went ahead this week and bought a bunch of S-REITs.

I’m still keeping powder dry and saving the bulk of my purchases for later in the year, but I did start to buy this week.

Why I bought the market crash

Broadly, 3 reasons why I did so:

- Possibility of short-term bottom

- Valuations for S-REITs are attractive for long term positions

- Possibility of a 1970s style stagflation

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Just created a Discord server where I collate analyst reports and investing resources that I come across in my research. Hit us up here if you’re keen.

Possibility of short-term bottom

US market action on Thursday night felt too much like a short-term bottom to me.

You know how the market opened with big names down 8% – 10%, and then over the course of the day they recovered to close up 10% or more?

That felt like the short-term capitulation move, when the shorts closed their positions.

That could trigger a short-term relief rally.

There are a couple of other indicators that back this up.

Firstly – systematic and institutional players have been selling for weeks on end. Hedge Funds have been reducing exposure drastically as well (with retail buying from them). That could exhaust some of the selling pressure.

And with earnings season out of the way, companies are free to do stock buyback. FAANG has a ton of cash, and could easily do >$100 billion this quarter. AMD just announced an $8 billion buyback. So has big oil.

Hedging activity has gone through the roof as investors buy put protection. That’s usually a contrarian signal.

And from a historical perspective – Gulf War, Iraq War, 9/11 etc, these were usually not sell-off catalysts beyond what was priced in. And I would say much of the short-term impact is already priced in.

Now of course I could be wrong here, these things are not an exact science. Which is why we back it up with fundamental analysis.

Valuations for S-REITs are attractive for long term positions

As shared last week, I agree with DBS that valuations for S-REITs are attractive for long term positions.

You’re buying blue chip REITs with Singapore real estate for a 5.5% yield.

That’s the yield we last saw in 2018, when interest rates were at 2% and at the peak of the rate hike cycle.

At these prices, that’s a fair bit of a margin of safety baked in.

And again for the record, I don’t think this is the bottom for REITs. I think we maybe see a 5% – 10% move lower before this cycle is over.

But (1) I could be wrong, and (2) very few people have the nerves of steel to deploy that much money when the markets are plunging.

Because of that, averaging in makes sense once REIT prices hit your own price targets, as they did for me the past week.

Possibility of a 1970s style stagflation

Now this last one is a wildcard.

If you asked me in Jan what’s the possibility of a 1970s style stagflation playing out, I would say maybe 5%.

But the past week has caused me to rethink this.

Stagflation is still not my base case of course, but I think the probability of it has increased significantly.

I can now envisage a chain of events that starts with the Ukraine war causing more significant impacts on global supply chains and commodities prices than expected. Into a Fed that hikes 6 times this year. Into inflation that remains sticky and doesn’t drop significantly.

That’s potentially a very tricky situation to be investing in.

You’ll have rising nominal interest rates, yet negative real interest rates once you adjust for inflation.

That could spark a stampede out of negative real yielding government bonds, into the safety of real assets.

Practically speaking – Think workers demanding higher salaries because inflation is 7%, business owners forced to pass on increased costs in the form of higher prices, feeding back into a vicious cycle of demands for wage increases.

Or think consumers pulling cash out of bank deposits to spend on a car/house today, before prices go even higher.

Once this kind of thinking gets rooted in mainstream psychology, it can be very hard to break.

The last time this happened in the 1970s, Paul Volcker rose interest rates from 11% in 1979 to 20% in 1981, and completely broke the market.

Where are we in this 1970s cycle?

Of course, I don’t think we’re there yet.

We’re still at the stage where people flood into real assets, and there is hope of the Feds controlling inflation without breaking the market.

In 1970s terms, we’re still in the middle parts of the decade.

If this stagflationary scenario plays out, the way you’ll want to protect wealth is to own real assets, in safe jurisdictions.

Singapore corporate real estate exactly fits that bill in my books.

Hence I bought blue-chip S-REITs, focussing primarily on those with Singapore real estate.

You can check out Patreon for the exact buys I made, and how I am invested in my portfolio.

Closing Thoughts: Will this decade look like the 1970s?

It’s funny how these things work.

40 years on, completely different set of players, with all the marvels of internet technology, and there are a lot of parallels with 1970s.

Think – Central banks that kept monetary policy too loose with negative real rates for a decade.

All while inflation was blamed on supply side issues.

Private sector was blamed for being too greedy with profits, wage unions for wage-price spirals, OPEC for manipulating prices.

Price and wage controls were instituted, but failed to curb inflation.

Sound familiar?

In the 1970s this played out in waves the whole decade, with inflation coming and going for almost 10 years.

By the end of the decade, people were so sick of inflation that Jimmy Carter nominated Paul Volcker as Fed Chair, who went on to raise interest rates to 20% and broke inflation once and for all.

Setting the stage for 40 years of price stability, and bringing us to where we are today.

Is humanity doomed to repeat the same mistake we made in the 1970s?

As always, this article is written on 26 Feb 2022 and will not be updated going forward. Latest thoughts (and my stock watch and personal portfolio) are available on Patron.

Looking to buy Bitcoin, Ethereum, or Crypto?

Check out our guide to the best Crypto Exchange here.

Looking for a low cost broker to buy US, China or Singapore stocks?

Get 1 free Apple share (worth $230) you’re new to MooMoo and fund $2700.

Get a Free Apple stock (worth S$230) when you open a new account with Tiger Brokers and fund $2000.

Special account opening bonus for Saxo Brokers too (drop email to saxo@financialhorse.com for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

I was watching an interview with rebecca patterson from bridgewater, where she said historically the Fed raises the rates to 2X the inflation rate to bring it back in line. So if the Fed goes up to 2%, chances are the inflation rate is not going down to 2%. Question is, will the Fed stay at 2%? Or will it hike further and cause an inversion, and only loosen monetary policy once inflation comes back down regardless of slowing economic activity like volcker did? Or, will the Fed live with higher inflation in a bid to stabilise employment and economic activity? This is the big question mark right now, and there’s alot of uncertainty moving forward. I guess the S-REIT assumption is that, even if a volcker style scenario happens, the S-RETIS are sturdy enought to withstand a global recessionary environment?

That’s a really interesting comment. I guess no one really knows how it’s going to play out, the range of possibilities is just too high at the moment.

If volcker happens, global CRE is going to drop 20-30% across the board. So I’m not under any illusions that S-REITs will do well if the Feds are hiking to kingdom come. But timing matters too. Feds pulling a Volcker in 2022, and Feds doing it in 2025, are 2 completely different events. In the latter, CRE may have risen 50% from now till then in a higher inflationary scenario.

Perhaps another point to add, is that don’t forget that QT is on the table as well. If the Feds were truly worried about inversion, what they can do is implement aggressive QT to bring the long end up, while hiking the front end to ensure it doesn’t invert.

Do u think inflation has peaked yet? Do u think fed can solve inflation?

Frankly? I don’t know. The range of possibilities is very high, and the Ukraine war is added uncertainty. There are strong arguments both ways, and while I lean towards the camp that inflation will stay sticky for a while, I’m also not crazy enough to think that this is the only possible outcome.

The best one can do is to invest based on one’s view of the probabilities, and remain open to change one’s mind when the facts / data changes.

War has driven oil upwards so inflation will continue rising? Will fed be forced to hike more? If so then we are risking a economy slowdown or even recession. I think the probability of inflation sticking around is high. Difficult to solve inflation without recession. What do you think? Either outcome is bad for growth stocks. Will big tech remain steady or continue to fall? What u think?

I actually did a Patreon article to share latest views: https://www.patreon.com/posts/russian-banks-63159174

What I would say is that short term chaos aside, the result of this Ukraine war is to create higher and more sticky inflation. In this article I talked about the possibility of Feds hiking but failing to bring down inflation (soft stagflation), and I think the chances of that have gone up this week.

Plan to do an article this weekend to dive deeper into what kind of stocks to buy in such an event.

Hello FH,

You mentioned buying blue chip S Reit that focus on SH real estate. What about going for big name SReit that focus on oversea asset instead so that we can diversify a bit more and spread out the risk. Most SG ppl already have plenty of risk associated with SG already (job, Hdb flat, CPF)

I think that’s perfectly fine – the equivalent is buying an overseas private property.

What I would add though, is that real estate is a very local business. So even though one may venture overseas with REITs, it’s important to understand the real estate one is buying, and stay within one’s circle of competence. For me I am most familiar with Singapore/China, so with my REITs I usually focus on those markets.

On a scale comparable to the Turkish lira crisis where Trump was at loggerhead with the Turkish presidents unorthodox regime and sanctions of all Turkish exports , Russia is 10x in scale and rubbing salt to the existing fuel prices crisis, what do you think ? Hike or let the fire burn out by itself?

Can anyone see the analogy and draw conclusion

Turkey US conflict (2016-7)

Ukraine vs Russia (2022)

1. Economic sanctions

2. Localized financial crisis

3. Lira & Rubble in trouble

4. Absurd interest hike

5. Turkey (pea sized)

6. Russia (golf ball)

7. Throwing fuel to fire current oil prices