I received a couple of great questions from Patrons recently on:

- What to buy when the Fed pivots

- How to play the China “reopening”

Believe it or not, the 2 issues are actually somewhat intertwined – given the implications the China “reopening” will have on inflation, and consequently the timing of the Fed pivot.

So it’s worth discussing both together.

Here are the respective questions:

What to buy when the Fed pivots?

Hi FH,

On the assumption that Fed will pivot with a rate cut or QE in mid to long run.

Assuming one has no knowledge edge in individual stock picking

Assuming this forms the higher risk end of the barbell portfolio, with reits,propety,bonds on the other end taken care of

To ideally make a profitable, high beta play on the Fed pivot catalyst.

Which of these routes would you prefer?

1 – Invest in a tech stock ETF like QQQ after Fed show committment to easing

2 – Invest in Ether / Bitcoin as a index to Crypto

How to play the China “reopening”?

Hi FH,

Would like to hear your thoughts on the impending China opening:

- Any stock play that can benefit from this?

- Won’t it benefit Singapore’s (And the whole world’s economy)? Hence there might be some stocks worth buying in SG like Genting?

- Will this potentially cause inflation to skyrocket? (Will fed then continue to raise the interest rates more aggressively?)

How to play the China “reopening”?

Let’s start with the China “reopening”.

As I shared in the previous China update, even before the Party Congress there have been rumours on the ground that airport staff are being told to prepare for a potential reopening in 2023.

After the Party Congress, such rumours have been kicked into overdrive.

To the extent that Chinese stocks have recovered quite strongly from the lows based on such rumours.

Is a China “reopening” guaranteed?

That being said, there has been no official word from CCP on this issue.

In fact, official policy stance is that COVID zero is still in place.

And you can still see lockdowns in Zhengzhou (hitting Foxconn’s iPhone production) keeping in line with the COVID zero policy stance.

Now whether we will see a China reopening is ultimately a political question, and not something I have an edge in predicting.

So personally this is not a trade I will be making.

If China reopens, I will play it accordingly. If China doesn’t reopen, I will play it accordingly.

But I will not be making bets based on whether China reopens.

What about those who are inclined to do so?

For those who want to do so however, there are 3 ways that come to mind

- Reopening Stocks– Airport, Airlines, Retailers, Restaurants (possibly casino or tech)

- China dividend stocks (but broader risk)

- Oil

Now I assume anyone making this trade will understand the basics of position sizing and stop loss, so I won’t delve too much into the risk management aspects of the trade.

Reopening Stocks

The most obvious one, is the COVID basket of reopening stocks.

Whatever did well globally when the world reopened – use the same playbook in China.

So think Airport stocks, Airline stocks, Retailers, Restaurants.

If you’re feeling adventurous you can go for the Macau casinos or tech (eg. Meituan or Trip.com), but these days both carry a hefty regulatory risk premium given CCP’s crackdown.

The problem of course, is that this basket being the most obvious play, has already started to go up.

So if you really wanted to make this play, you would probably need to frontrun the CCP’s reopening announcement.

By the time they actually announce the reopening (if at all), much of the reopening may already be baked into the price.

And like I said, I don’t have a strong view on when / how China is going to reopen, which does make this a tricky play.

China Dividend Stocks

China Dividend Stocks are dirt cheap now.

The big 4 China banks are trading at close to 10% dividend yields.

China Mobile trades at close to a 10% dividend.

CNOOC (China oil company) trades at close to a 20% trailing dividend (10% forward).

The problem of course, is that such dividend stocks are not really a direct play on the reopening.

How these stocks play out going forward will depend very much on China’s debt restructuring for the real estate sector, how they transition their economy, how the US-China cold war plays out etc.

So the big problem with this basket is that this is more a play on China generally than on China’s reopening.

Oil

Which leaves oil.

Interestingly, oil might be my favourite way to play the China “reopening”, if I were so inclined.

You see the main worry with oil in the short term is the upcoming recession.

With the Feds taking us to 5% and beyond, a 2023 recession is pretty much a done deal, the only question is when and how deep it will be.

If we get a severe global recession (eg. 2008), that could actually cut anywhere from 2 – 3% of global oil demand.

If we do get a China “reopening”, then well you just solved the demand problem for oil.

Because whatever demand was cut due to the recession, may be offset by the China “reopening”.

And meanwhile on supply side things are looking dire, with Russian supply getting hit, and the SPR releases to be cut back after the Nov elections, and OPEC+ cutting supply.

So again, I don’t know if China will indeed reopen, or when they will do so, or in what form.

But if they do, that has pretty big implications for oil, and which might be an interesting way to play it.

What to buy when the Fed pivots?

Which brings us to the question on what to buy when the Fed pivots.

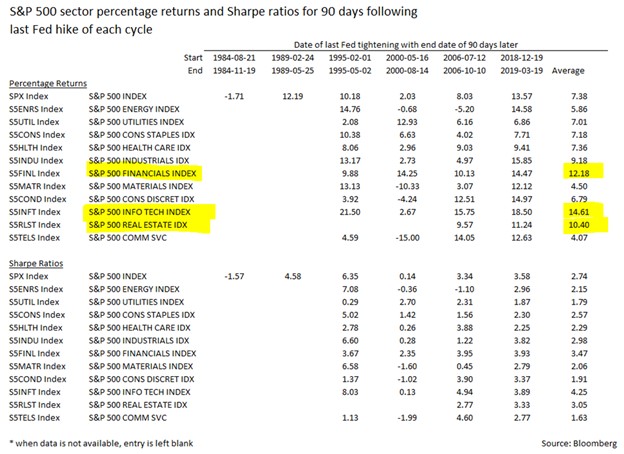

Now the traditional answer of what to buy when the Fed pivots any time the past 40 years, is:

- Financials (banks)

- Technology

- Real Estate

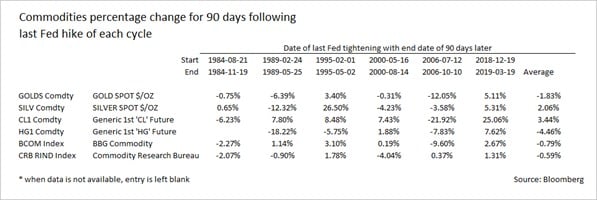

You can see the performance of the 3 asset classes below, both returning about double digit returns in the 90 days following the end of the Fed tightening.

Whereas commodities did not do so well:

Problem with this analysis?

Now the problem with this analysis of course – is that this is using returns from the past 40 years.

And remember how I keep saying the past 40 years was just one giant secular bull market for bonds with falling interest rates?

Which means any backtesting you do on the past 40 years, is backtesting in a climate where interest rates are in a secular downtrend.

And perhaps more importantly, in a climate where inflation is not a problem.

And of course brings us to the crucial difference between 2022/2023, and any time the past 40 years.

Inflation is very much a problem today.

How does this tie back into China’s “reopening”?

Which is where China comes in.

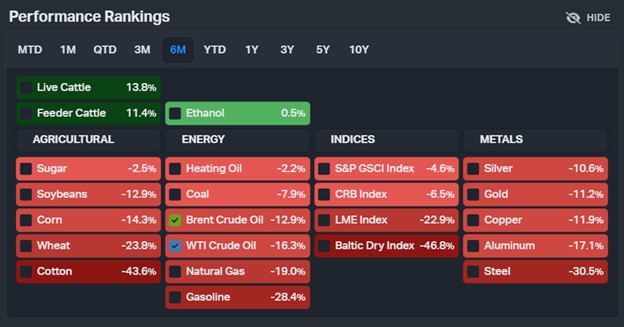

You see oil prices have come down quite a bit since the Ukraine war highs.

Through a combination of SPR release and recession fears, Oil is actually down 12 – 16% the past 6 months:

For a Fed that is desperate to bring inflation down, having oil prices go down is very helpful indeed.

What if inflation refuses to come down?

If we get a China “reopening”, then the outlook for oil becomes much more tricky.

Supply side the SPR releases will fall away soon, while Russian supply is a big question mark. Meanwhile OPEC+ is talking about supply cuts.

And while everyone has been gambling that a recession will cut demand for oil, what if the recession coincides with a 2023 China reopening, that brings back a big chunk of oil demand?

And what if oil prices go up in 2023 amid tight supply, exacerbating the inflation problem for the Feds?

Now let’s say you’re in mid 2023, inflation is running at 4-5%, and the Feds Funds Rate is at 5%+.

And the economy starts to roll over, and markets start to break.

What do the Feds do next?

Do they cut rates despite inflation being high?

Or do they keep rates high, despite the economy starting to roll over?

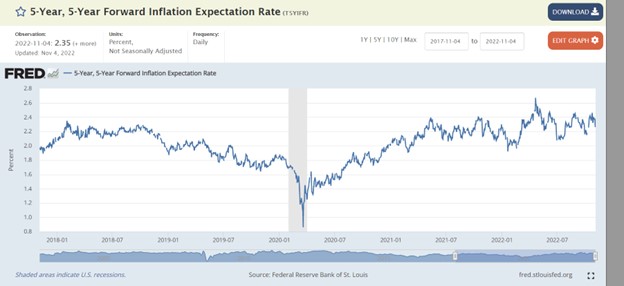

Inflation expectations are anchored, because investors believe the Feds will tame inflation

As shared in last week’s article, long term inflation expectations so far are very manageable.

Because investors believe that the Feds will be able to contain inflation, or at least will try to.

Now imagine what happens if inflation is at the 4-5% range in mid 2023, and the Feds start to cut rates.

What’s going to happen to inflation expectations?

What to buy… depends very much on where inflation will be when the Feds “pivot”

So the simple answer to this question, is that if this were any other time the past 40 years, where inflation is not a problem, you buy (1) banks, (2) tech, and (3) real estate.

The problem this time around is that inflation is a problem.

So you cannot answer this question without knowing where inflation will be at the time when the Feds start to cut.

If inflation is still high when they cut, then you’re going to be looking at a more inflationary future, a debasement of currency style scenario.

In which case you probably buy commodities, precious metals, banks.

Maybe real estate too if you get a good price, but in this scenario expect higher interest rates for longer, which will impact real estate returns.

Whereas if inflation is low / contained when they cut, then it’s exactly the same as the past 40 years. You buy banks, tech and real estate.

Which are we likely to see?

A real Fed Pivot is probably a 2023 story, so we still have months to go.

No real need to frontrun this trade as well, because the data to come in the months ahead will tell us who is winning in the fight between inflation vs recession.

For now at least, I fear for the former scenario.

Given how strong the labour market is. And given the willingness of OPEC+ to cut supply, all while the west fails to invest into new supply (while cutting off SPR release).

Makes me quite concerned over how much inflation will come down by 2023.

But like I said, no need to frontrun this trade.

Just let the data tell us which way inflation will go.

Jerome Powell has stressed the Feds would be data dependent. They will watch the data, and so should investors.