Regular readers will know that I think we are headed into the golden age of macro investing.

After 10 years where global interest rates were stuck at the lower bound, the return of inflation has changed everything.

For the first time in 10 years, we are seeing central banks diverge on monetary policy.

This has created record volatility across all asset classes.

And nowhere is that more apparent than in Forex (FX) markets.

I know not all of you are interested in FX markets, but how this plays out has broader implications on central bank monetary policy, and consequently on how we invest.

For obvious reasons I won’t be able to cover everything in today’s article (FX is a massive topic), but I will try my best to cover the big overarching themes, so that you have an idea of how we got here, and where we may be headed in the months ahead.

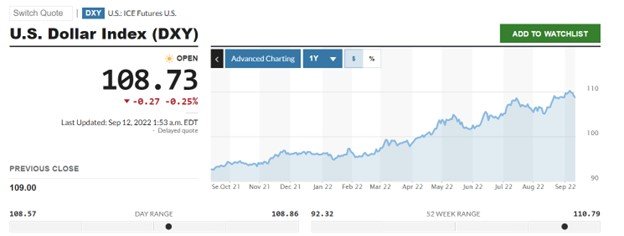

US Dollar (USD)

Let’s start with the king dollar, whose rapid appreciation this year has wreaked havoc across financial assets.

Key factors driving the USD

In the short term, the key driver for the USD is tightening monetary policy.

Feds are taking us to 3.75% on the Fed Funds Rate by end 2022 / early 2023.

With higher interest rates than the rest of the world, this has driven capital from the rest of the world back into USD assets.

In the medium term, there is a structural demand-supply mismatch for US Treasuries.

With Quantitative Tightening, the Feds are moving from a net buyer of Treasuries, to a net seller.

At the same time, US banks (which used to be a large buyer of Treasuries), are close to regulatory limits which limits their ability to buy treasuries going forward.

All while the US-China “cold war” means that China is unlikely to be buying large amounts of US Treasuries going forward, and may even look to pare down their stake.

If US spending continues to increase going forward (and it likely will in the medium term), the question arises who is going to buy all these new Treasuries that are going to be issued.

With the tightening liquidity, private sector may not be able to absorb all the extra supply.

My Personal Views on the USD

Short term, I think we may be close to peak USD here.

With the Feds at 3.75% by end 2022 / early 2023, we are close to the later stages of the hiking cycle for the US.

Yes, the terminal rate may go beyond 4%, and interest rates may stay at 4% for a while, but the fact remains that the Feds are almost done with their front-loading of rate hikes, while the European Central Bank has only just started.

In financial markets it’s the rate of change that matters the most, and the pace of interest rate hikes for the US will slow soon, relative to other central banks.

Which *should* be bearish for the USD.

Of course, the exception here is if we get a market risk-off event.

USD rallies in times of uncertainty, so if there is a market crash the USD will benefit strongly.

But medium term, with increased US spending, and the marginal buyer of US Treasuries out of the picture, I would expect depreciation of the USD.

Japanese Yen (JPY)

The JPY is driven by 1 very simple factor – the fact that the Bank of Japan (BOJ) has chosen to maintain 10-year interest rates at 0.25%.

They are implementing yield curve control, which means they will buy whatever amount of JGBs it takes, to maintain interest rates at 0.25%.

Of course, when you artificially fix your interest rates at 0.25% when every other central bank around the world is hiking, your currency is going to depreciate.

And depreciate it did:

Here’s the 30 year chart of the JPY, which really puts things in perspective.

Current levels on the JPY are nearing 1997 Asian Financial Crisis levels of bad:

My Personal Views on the JPY

The Japanese are a proud people, not prone to admitting mistakes.

And their ability to stomach pain, is higher than any other society.

So the investors calling for the BOJ to suspend yield curve control, are still too early in my view.

The BOJ will bend, but not this fast.

With a weaker JPY, the BOJ will finally be able to do what they have been trying for a decade to do – bring inflation into Japan.

So short / medium term, leaving aside the technical bounces, I think JPY will continue to slide.

150 on the USD/JPY is a key technical level to watch.

That being said, at some point in time in the medium term the BOJ will relent, and the JPY will rally.

That’s probably more of a 2023/2024 story though.

Euro (EUR)

The Euro has had it tough of late.

This is down to 2 factors.

Firstly, the decision to maintain interest rates at zero bound despite the Feds aggressive hiking.

And secondly, their energy crisis.

Talking about the European energy crisis will call for a full article of its own, but to sum up, a decade of poor energy decisions have taken us to where we are today.

Which at this point, is almost inevitably causing to cause a European recession this winter. The only question is how deep the recession will be.

And because Europe is a net energy importer, a weak euro will drive commodities prices up (Commodities are priced in USD), worsening inflation.

The ECB understands this fully well.

Hence their recent decision to hike interest rate by 0.75%, with expectations of a terminal rate in the 2.75% range.

My Personal Views on the Euro

Simply put – the market did not expect the ECB to be this hawkish.

They are literally raising rates into an EU-wide economic slowdown, which is something you usually see in Emerging Markets like Turkey, not the second largest economic bloc in the world.

But because the ECB has flipped hawkish, I actually would expect the Euro to hold its own going forward.

It probably won’t rally strongly barring a change in the Russia situation, but talks of the Euro dropping significantly below parity against the USD are probably too pessimistic.

This will be a tough winter for Europe and the European economy, but the ECB cannot allow the Euro to depreciate too much because of how it would drive up the cost of energy imports, and worsen inflation.

In any case, when you have a supply driven recession like what Europe is going through now, keeping interest rates low will do little to solve the problem. So they might as well just raise rates to support the Euro – which is exactly what they are going to do.

This means higher rates, which means money back into the EU, which would support the Euro short term.

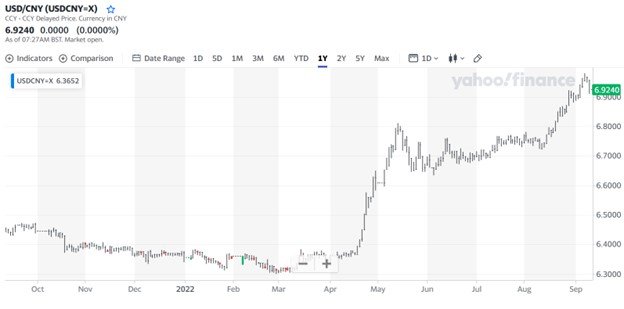

Chinese Yuan (RMB)

Unlike all the previous currencies on this list, the RMB is not a free float currency.

The RMB is broadly similar to the Singapore Dollar – in that the RMB is allowed to float freely within a narrow band, but the exact limits of the band are not disclosed to the market.

China’s problem though, is that they are navigating COVID Zero, a real estate debt situation, and a restructuring of their economy – at the same time.

Each of which would significantly hamper economic growth by itself, let alone all 3.

And just like the EU, China is a net commodities importer.

So the usual solution is to stimulate economic growth is to inject stimulus, but China stimulate without weakening the RMB, which would bring inflation.

So far at least, China has kept the RMB very strong (as compared to other major currencies), which means low inflation, but a lot of economic pain domestically.

My Personal Views on the RMB

Unlike the other currencies on this list, I do not have a strong view on where the RMB is headed.

China is a top down economy, so policy decisions are made at the very top and floated down.

Many of the decisions are politically driven rather than market driven.

And politically, there’s a lot of uncertainty over how the next 12 months is going to play out.

Much may become clearer after Xi is re-elected at next month’s party congress.

In any case, at this point in time, I don’t have a strong conviction on how the RMB will play out going forward.

Singapore Dollar (SGD)

Finally, the Singapore dollar.

In the grand scheme of things, Singapore is a tiny economy, so movements in the SGD have almost no impact on the global economy.

It does for us though, as investors who live in Singapore and spend in SGD.

For what it’s worth, Singapore situation this time around, is immeasurably better than it was during the 1997 Asian Financial Crisis.

Reserves are very strong, the economy is performing well, and tight controls on property ownership / debt ratios help to prevent a property crash that may come in other markets in the months ahead.

In some ways, I think the SGD may prove to be a safe haven currency / asset in the coming year or two, the equivalent of the Swiss Franc in South East Asia.

So if you want to play it safe, you could do a lot worse than holding SGD denominated assets in Singapore, and leaving it to the Singapore government / MAS to manage the volatility for you.

As always, love to hear what you think!