So I was calculating my net worth allocation for the FH Net Worth tracker recently. And I was really surprised by the amount of cash I was holding. In fact, my cash + bonds position was more than half my total investible assets.

Now this was an intentional move because I feel we are very late in the credit cycle, so I wanted to increase my cash position and position more defensively. But still, I was taken aback by how much cash I was sitting on uninvested.

So I had a serious look at the various asset classes in Singapore, to decide where to allocate the excess cash. And that was when I started getting worried.

Simply put, many asset classes in Singapore right now, are looking pretty fully valued, especially given the macro climate we have.

Macro Environment – Why so serious?

But first, let’s take a look at what’s so scary about this macro climate. There are a couple of points in particular to highlight:

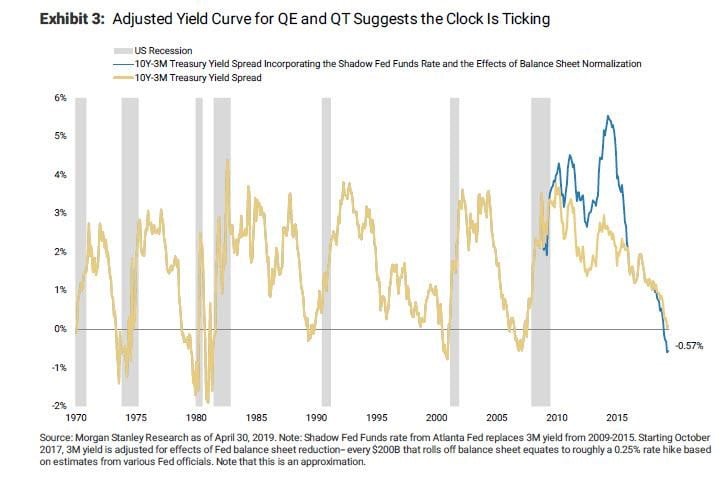

Yield curve inversion – The US 3s10s curve has inverted. And if you take Morgan Stanley’s word for it, they find that if you add on the effect of Quantitative tightening, the yield curve actually inverted in late 2018, which means we could be looking at a US recession pretty soon. For beginner investors among us, a yield curve inversion happens when the short term interest rates are higher than longer term interest rates, and historically speaking, this usually results in a recession within 12 to 18 months. If we assume inversion in late 2018 according to Morgan Stanley, it means a late 2019/early 2020 recession is in play.

US China Trade war – The US China Trade war is getting really bad, really fast. All the developments around Huawei and rare-earth bans look particularly troubling. I still believe a deal will eventually be struck, but between now and then, there could be enough damage to global trade and investor sentiment that takes us into the next downturn.

US Mexico Trade war – And if China wasn’t enough, Trump literally just announced 5% tariffs on Mexican goods for as long as they fail to contain the issue of immigrants crossing into US. These tariffs come into effect in June, and can potentially rise to 25% if the issue is not resolved. Mexico is a huge trading partner for the US (most US companies manufacture in Mexico to reduce costs), and if this is carried out, it’s going to wreak havoc on the US supply chains.

End of Fed tightening cycle + falling US bond yields predicting rate hikes – As an investor, it’s actually not the Fed tightening cycle that you should be watching for, it’s the Fed cutting rates. The rate hike cycle is usually too early in the cycle to provide actionable trading signs. But when the Feds start pausing rate hikes, and starts talking about rate cuts (like they did the past week), that’s when it’s time to really start getting worried.

In fact if you look at the Fed futures market these days, it’s pretty much pricing in 2 rate cuts in 2019. That’s never a good thing.

Layoffs in Sequoia China, CNN, Ford – Sequoia recently announced that they could be cutting up to 20% of their investment staff in China. Sequoia is one of the biggest and most prestigious private equity players around, so when they start cutting 20% of their investment team in China, you know there are problems there. Couple this with reports of layoffs in companies from CNN to Ford, and it starts looking troubling.

Uber IPO – Let’s not mince words. The Uber IPO was a disaster. When you talk about having a $120 billion valuation, only to end up pricing your IPO at the bottom of the price range, having it drop 15% in a couple days of trading post IPO, let’s just say it wasn’t the best IPO ever. In fact Softbank just took up a $4 billion margin loan on their Uber stock to repay investors, which send a lot of conflicting signals to the market. An IPO is just about the only viable exit strategy for most Unicorns, so with IPO sentiment this jittery, it casts doubts over the success of any future IPO. WeWork anyone?

Rise in default rates in P2P lending in SEA – Ok this one is purely anecdotal. But I’ve noticed that the default rates in Peer to Peer lenders in South East Asia (Funding Societies etc) have been slowly inching up. If so, that’s not a good sign, because these SMEs are usually the first ones to fall in a downturn. I don’t have hard evidence to back this up, so if anyone out there does feel free to share in the comments below (or drop me an email)!

Now I guess some of you out there will just say I’m cherry-picking the bad news to support my argument. I get that. That’s a definite possibility, and it could really be that I’m so convinced the cycle is ending that I only see what I want to see.

But I just think when you look at the big picture (yield curve inversion, end of Fed tightening cycle), and you look at the details (layoffs, trade war, Uber IPO), it really does look a lot like we are very late in the credit cycle. Individually, I wouldn’t read much into the above, but put them all together and that’s a different story. Am I right or wrong on this? Please share your thoughts below!

REITs

So you take that macro outlook, and you look at where Singapore REITs are trading. And gosh, does it look like dreamland over here.

This is the 5 year chart of Mapletree Commercial Trust, which is now trading at a 4.8% yield and a 20% premium to book. Really?

I could pull up the charts and data for any other blue chip REIT (CapitaLand Mall Trust, CapitaLand Commercial Trust, Frasers Centerpoint Trust) and they’ll pretty much tell the same story.

What am I missing here? Why are people still buying REITs at these prices?

Singapore Dividend Stocks

Singapore Dividend stocks on the other hand, are interesting. The market has come down quite significantly for some of the blue chip dividend plays, especially those China related ones. The bank stocks have come down a fair bit too.

So I actually think there are opportunities here for a long term investor, who is prepared to average in right now and ride out the volatility.

Names that I like include Netlink, Singtel, CapitaLand, and the 3 local banks, but again, because I already have exposure to many of them, I’m slightly wary of adding too strongly to my position at this stage in the cycle.

Singapore Savings Bonds

I’ve set out the yields from the latest June bonds, against the January 2019 bonds below.

The 1 year yield has come down from 2.01% to 1.88%, and the 10 year from 2.45% to 2.13%. That’s a huge move in just 6 months.

Would I invest in Singapore Savings bonds at these kind of yields? Well, SSBs are basically the risk free rate for SGD assets, so it sets the benchmark for all other risk assets. So unfortunately, I’ll still invest in it if I had spare cash that I didn’t want to take any risk with. There’s just no alternative.

June 2019

| Year from issue date | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

| Interest, % | 1.88 | 1.88 | 1.88 | 2.03 | 2.13 | 2.15 | 2.24 | 2.32 | 2.41 | 2.48 |

| Average return per year, %* | 1.88 | 1.88 | 1.88 | 1.92 | 1.96 | 1.99 | 2.02 | 2.06 | 2.09 | 2.13 |

Jan 2019

| YEAR FROM ISSUE DATE | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

| Interest,% | 2.01 | 2.14 | 2.25 | 2.35 | 2.45 | 2.53 | 2.62 | 2.70 | 2.79 | 2.90 |

| Average p.a. return, %** | 2.01 | 2.07 | 2.13 | 2.18 | 2.24 | 2.28 | 2.33 | 2.37 | 2.41 | 2.45 |

Residential Property

Probably the most interesting asset class right now is residential property.

Just this week, news came out that Braddell View was trying (and failed) to sell the property in an en bloc tender, with a reserve price of $2.08 billion. I found this pretty interesting because here we are talking about the rapid deterioration in the global macro climate, and then these guys are trying to get a property developer to cough up $2.08 billion (excluding construction costs) to buy over their land. Really?

To put it mildly, it’s going to be hard to find a developer to be able to (and willing) to splash out this much liquidity in this macro climate, especially after the cooling measures imposed by the government last year.

But that’s also the thing about Singapore residential property, because it’s such a tightly controlled market (by the government), it’s actually less responsive to global macro factors than we would think. Add to that the fact that property is illiquid and usually takes 9 to 12 months to respond to what’s going on in the world, and you have a very unique asset class.

The ABSD charges imposed by the government last year (12% for second property) have done their job to take out the burgeoning exuberance in the residential market, but most sellers seem to have missed that memo. As a result you have a market where sellers still have high asking prices, and buyers, noticing the change in climate, are only prepared to pay a much lower price. Until one of them decides to change their mind, you’re just going to have a market with falling transaction volume, which is what we’re seeing.

Would I buy a property now? I think long term, because the government intervenes so strongly in the residential market, you’re going to have an asset class with a slow and gradual increase over time. So even though prices are still at a historical high, I think if you find one that you like, and you’re in the market for a new property do go for it. Even better if you’re a new buyer and can avoid the ABSD.

Would I buy a property now? I think long term, because the government intervenes so strongly in the residential market, you’re going to have an asset class with a slow and gradual increase over time. So even though prices are still at a historical high, I think if you find one that you like, and you’re in the market for a new property do go for it. Even better if you’re a new buyer and can avoid the ABSD.

But don’t forget that because property is so unique, it’s really about find that one house that you love. If you do, it’s probably worth buying regardless of where the global macro is, because again, given how the government intervenes, I don’t think you’ll get sharp price movements either way for long periods.

Closing Thoughts: What did I do in the end?

Now the purpose of this article wasn’t to spread fear and uncertainty, so my sincere apologies if it did. It was really just to share my personal experience the past week of reviewing the general investment options available to Singaporean investors, and my thought process in deciding where I wanted to invest the cash.

So what did I do in the end? I took whatever cash I had left in my SRS account, and invested it into Netlink Trust. The non-SRS cash I had? I left it in DBS Multiplier to take advantage of their new S$100,000 limit.

I still think we are very late in the credit cycle, and we’re going to see more volatility in the coming months. And that’s why I continue to maintain an outsized cash position. But I could turn out to be completely wrong on this though, which is also why I haven’t sold any of my existing positions. If the market continues to keep going up, hey, I’m still well exposed to stocks and REITs.

I would absolutely love to hear your thoughts on my asset allocation strategy though. Is this what you’re doing as well? Or do you think it’s the stupidest thing you’ve ever heard? Share your thoughts in the comments section below! I respond personally to all comments!

Enjoyed this article? Do consider supporting the site as a Patron and receive exclusive content. Big shoutout to all Patrons for their generous support, and for helping to keep this site going!

Like our Facebook Page and join the Facebook Group to continue the discussion! Do also join our private Telegram Group for a friendly chat on any investing related!

I agree with your analysis and have been quietly reading your articles. Thank you for sharing generously. I am choosing to keep some cash to buy the banks when the share prices come down further.

Thanks for sharing your thoughts! Hope that you’ve found the articles helpful. I too, would like to increase my exposure to the banks if they drop more ;).

Just like you, I looked at my portfolio this week & couldn’t find it in me to pop much into the Sg market. Again, like you, I bought some Netlink. What’s your take on Keppel DC reit & the oil/industrials? Also 5G?

I like Keppel DC but it’s too expensive for me right now. I don’t follow MOG too closely, so hard to comment on that apart from the fact that it’s very cyclical, a lot depends on what OPEC does, and the late stage credit cycle makes oil look scary. 5G is interesting, but there’s no easy way to play 5G right now because of the trade war. It’s one of those where executing the trade idea can be challenging.

Hope this helps!

I am doing the same thing as well, more because of inertia though! Took time to learn and slowly deploy capital, so have quite a fair bit of my portfolio still in cash and bonds.

In the first quarter of this year I wanted to get in and was feeling a little bit fomo, but valuations had run up and I was uncomfortable, as global growth had already been slowing and the trade deal had yet to be signed. Turns out to be the right call at this point, but could have been wrong as well, in which case there would be a an opportunity cost of holding cash.

In my opinion, I think the factors you point out are interlinked. With the trade war the main catalyst. The bond markets are reacting to the trade issue, which is why you see yield curve inverting again and markets pricing for fed cuts. The trade war will have a real far reaching economic impact that could be really really disruptive. Channels through which economic activity will be affected are via exports, employment, investment, and confidence. Surveys I have seen of companies as well as anecdotes I have heard indicate that companies were waiting for clarity on the trade deal, before making further decisions on investment and employment.

In Singapore, I think the banks currently look attractive to me. In the US markets, China-exposed companies have cheapened significantly (eg. BABA, AAPL), as have semiconductor companies (trade war + tech war = boom). Am looking to add to these. Thoughts? 🙂

Thanks for sharing your thoughts! We seem to have quite similar thinking – I too, am interested in the China exposed stocks, semicon, and Singapore banks. Timing wise though is tricky. Because these 3 have come down so much since the start of the year though, I may just start buying in over the next few months, as part of a long term position.

Hi, nice article and I have been following reading it. Would you consider the nikko am sg Igbond etf? It appears to be recession free (based on other bonds history) & yielding about 3%. Better than SSB ? Please share your thoughts. Thanks.

Good point. I suppose the IG corporate bond ETF could be a good alternative. What makes me nervous about that ETF is the lack of liquidity though, so it might be tough to exit in a pinch. Expense ratio is pretty high too.

But I guess beggars can’t be choosers, so yeah, it’s definitely a viable alternative to cash/SSBs.

If developer not buying property why should you buy. I think we can at least test the 2016 levels again and even lower if macro environment worsens. Reduce p2p and reits exposure. Bond yields look Low but can go lower. Bond buyer here. Fed last hiked rates in Dec. If u think that’s the last hike, then at jun now we are in the beginning of the easing cycle. Not too late to buy bonds.

That’s a good point actually. One way out could be to buy US treasuries, if indeed this is the beginning of the easing cycle, there could still be big gains for bonds.

I think property is so regulated these days that the government won’t permit a prolonger slide in residential prices, as they can easily remove the cooling measures. So if one were looking to buy a residential property long term, the next 12 months could be a good time. I do agree though, that we could still test the 2016 levels.

Hi Financial Horse….thanks for writing this blog. However, not sure whether this time’s inverted yield curve is similar to the ones before as this one is fed induced. Check out this article by Forbes – https://www.forbes.com/sites/johntobey/2019/05/31/yes-the-inverted-yield-curve-foreshadows-something-but-not-a-recession/ will be good to get your thoughts.

Also, on sitting on cash – i feel investing for goals such as retirement, house, etc. via mutual funds should not be stopped as even if a recession comes buying across time period will average out the cost and gains but yes from wealth creation standpoint may make sense to go big on liquid assets for taking a desired position when apt time comes.

I agree that this time the yield curve inversion is different because of central bank policies. But if you look at the morgan stanley report they argue that if you factor in QE/QT, the inversion already happened late last year. Individually I wouldn’t reach much into it, but pair it with all the other macro factors going on and I think we should be slightly cautious. I dont think a recession is a done deal though, it depends a lot on how central bankers and governments round the world react, and how this trade war affects economic growth.

I’m definitely not sitting on cash long term though, there are some attractive opportunities in china related stocks / Singapore banks that I may average into in the coming months.

Residential property? You are right to show the property cycle chart.

I made a mistake in 1997 when property prices were at its peak when I bought a private property. The exuberance then was if one is not in the game one would lose out. I remembered a caricature on a wall showing an old man still waiting to purchase his first property and he was waiting for its price to fall. On hindsight wisdom, Asian Financial Crises strike in 1998, that private property did not see daylight until 2012. 14 years!

Hi Fred, thanks for the great comment, and for giving some perspective to the discussion! My personal thinking is that this time round, the government was quite quick to respond with cooling measures, so the residential property market didn’t get as overheated as it did back in 1997. Without the exuberance, there also wouldn’t be as big a crash when the downcycle inevitably comes around.

But that’s just my take on this ;).

Cheers.

Hi FH,

Been reading your articles freely for its sober no- hard -sell analysis. Been buying up US until run up in USD/SGD snd still trending to 1.40.

I will be crude . In my not too humble opinion of studying and investing the stock markets, and getting hands burnt over penny stocks, I still believe the stock market is only way to go just ask Warren . However, for newbies, please dont play with monies your family needs and learn to manage Greed and Fear.

Volitility is the name of game and it is in favour of nothing venture- nothing gain.

Back to my crude analysis of stocks , these are one word adjectives I describe for various markets :

STI – SPINELESS

HSI- MORIBUND

NYSE- ADVENTURE

So I have been stocking JPM , GS, Amazon, LMT , Appl, MSFT, and adding Halliburton and KHC of late!

Thanks again for your generous sharing!

Haha thanks for the sharing. Agreed with you that long term, stocks are definitely the way to go. I have a fair bit of US stocks too, but I find it incredibly hard to outperform there simply because the US market is so competitive and efficient. So these days, I mostly just buy the US index and the big tech companies, and focus on picking stocks in Singapore. 😛

Cheers!

Hi FH,

I have been learning alot from your articles and have been trying out investing recently. Can I just ask, how do you calculate a 20% premium for MCT? Is it different from price to book value?

Hi Xavier, Welcome to Financial Horse!

Yep it’s the same as price to book value. It is sometimes also called price to NAV. An easy shortcut is to check yahoo finance, their Price/Book numbers are pretty accurate most of the time.

All the best with your investment journey. Feel free to drop by if you have any queries at all. 🙂

Hi, in your opinion do you think that Reit price is too high now?

Interesting question, I’ll see if I can do an article on this. Cheers.

I am an auntie and I really enjoyed reading your post. Simple and not overloaded with boring data that auntie like me don’t understand. Keep up the good work!

Thanks, glad that you enjoyed it! 🙂

In other news: Mapletree Commercial just shot up to $2.05, 5 days after you (IMO rightfully) declared it as too expensive at $1.91 😛

I think my retirement REIT portfolio needs a plan B. The questions is whether to leave the units I bought at 1.7x untouched or not (given this portfolio is meant to outlive me). How do you go about yours?

Haha really interesting question, I’ll see if I can do an article on it. 😛

What are your thoughts about insurance stocks (ie AIA) and healthcare stock?

To be honest, I haven’t studied either of them in great detail, so I’m not able to comment intelligently. The healthcare stocks that I do know though (Raffles Healthcare, Parkway Life etc) all seem to be trading at premium valuations.