It’s been a while since we’ve done a big macro piece for stocks.

I love global macro investing, so in today’s article, I’m going to condense all my latest views on global macro into one single article, just for FH readers.

Whether you agree with me or not, I absolutely want to hear your views below!

BTW: Anniversary Promo for the FH Course and REITs MasterClass ends this Sunday! Don’t miss the chance to pick up both courses at big discounts – with big freebies thrown in! Check it out here.

FYI we’ll share commentary on the 2020 crisis every weekend going forward, so for those of you who haven’t signed up for our mailing list, please do – its absolutely free.

It’s a weekly newsletter that goes out at noon every Sunday, and rounds up the week’s posts so you never miss anything.

[mailmunch-form id=”928667″]

Basics: What’s happened so far?

A quick recap of what’s happened in 2020.

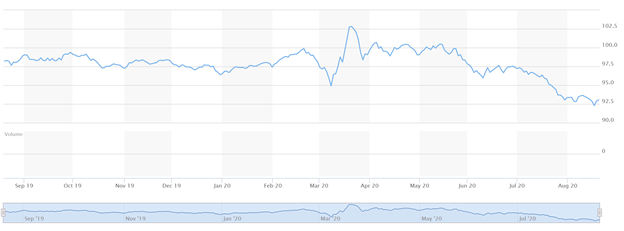

In March, when COVID started spreading to Europe and US, it sparked a massive risk off.

The dollar index surged to 102.5, and there was a liquidity crisis reminiscent of Lehman in 2008. Everyone was scrambling for the exits, and there were no buyers. Risk havens like gold and treasuries plunged together with stocks.

So the Feds stepped in in a big way. Over the course of March, they:

- Slashed interest rates all the way to 0%

- Committed to unlimited Quantitative Easing – buying as much treasuries as required to stabilize markets

- Committed to buying corporate bonds

Number 3 was the line in the sand. The Fed had never bought corporate bonds, ever. Their willingness to cross this line so easily was a big signal to the markets that they would do whatever it takes.

From there, the markets rallied all the way till today.

Investment Grade and High Yield spreads (above) measure the cost of borrowing for companies (low is good).

It spiked massively in March, but has come down drastically since.

I’ve used the 15 year charts so you can compare it to Lehman 2008. This time around, the Feds acted super quickly.

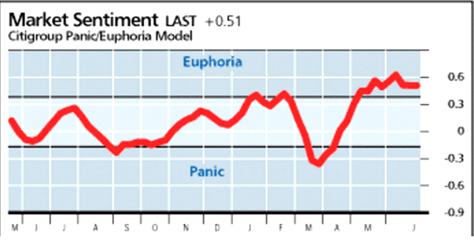

Feds committing to unlimited QE on 23 March 2020 marked the short-term bottom in this crisis. Markets rallied from panic all the way to euphoria in 2.5 months, making this the shortest bear market in history… ever.

But that’s all the in the past now. As investors, we’re always forward looking.

So we need to ask – what does the future hold?

The Insolvency Phase

In our earlier articles from March, we mentioned that after the liquidity event of March, we would move into a Hope phase. In the Hope phase, there would be a rally from oversold conditions, and investors adopt the view that COVID would be a short term event with a V-shaped recovery.

The Hope phase played out very strongly from April to June, and from July it started slowing as the second wave in US/Europe came back.

Either way, it looks like we’re nearing the end of the Hope phase now.

What comes next is the insolvency phase. And unlike the liquidity event in March or the Hope phase, which play out as shock and awe with big movements in financial markets, the insolvency phase tends to be more of a miserable grind.

The insolvency phase is characterized by corporate bankruptcies, widespread layoffs, and reduced consumer / business sentiment. Exactly what we’re going through now, and will continue going through in the next 6 – 12 months.

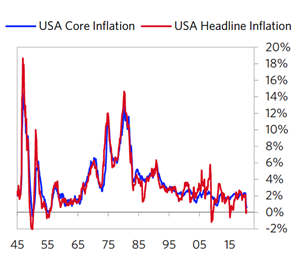

A Song of Ice and Fire – Inflation, or Deflation?

Medium to longer term, I see only 2 ways out of this crisis.

To quote a popular TV show – It is A Song of Ice and Fire.

We either emerge from COVID19 in the icy embrace of deflation, or the fiery grasp of inflation.

To understand how deflation plays out, we can look at Japan. It’s 10 years of slow growth, grinding insolvencies and unemployment, low levels of corporate investment and growth, and stagnant wages. It’s no fun.

For the inflation scenario, we actually don’t have any recent example. We need to go back to the 1970s or the 1940s to understand how it plays out.

Both were very tricky periods to be investing in. Hold the wrong asset class and you lose a big chunk of your wealth because of inflation.

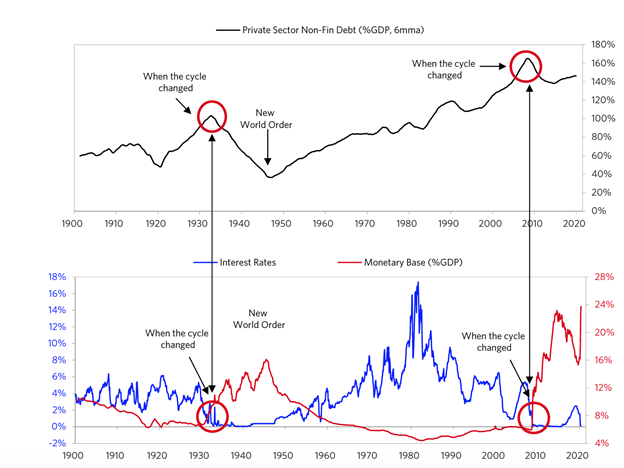

Why is the Great Depression the holy grail in economics?

I’ve been doing a lot of reading on how the Great Depression played out.

Why is the Great Depression so important?

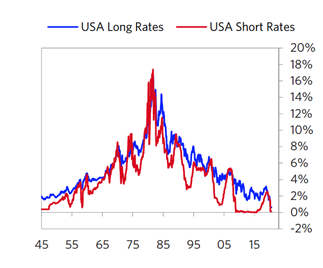

It is the only other time in the past 100 years that the US interest rates hit zero, and stayed there.

Now a bit of context to understand why this is so important. The dominant tool in economics over the past 50 years has been monetary policy (ie. interest rates).

The thinking was that whenever you have a bad recession, the central bank cuts interest rates, and the global economy will recover. People are rational right, so lower the cost of money, and people will borrow money to start businesses, and the recession is over.

This was what happened from the 1970s till today.

Everytime there was a recession, the Feds cut rates (usually about 5% before the recession is over). When the economy recovered, they raised rates.

But, and this is important, the increase in rates during the good times, are less than the cuts they made during the bad times.

2008 was a good example. Feds cut rates from 5% to 0%. But from 2008 to 2020? They only raised rates from 0% to 2.5%.

This means that over time, the broader trend in interest rates is downwards.

That’s exactly what we’ve seen.

Leaving aside the short term cycles, the broader trend in interest rates from the 1970s till now has been downward.

The death of Monetary Policy

So now that interest rates are zero, what happens next?

Which is where the Great Depression comes in handy. Because this was the only other time interest rates were at zero for 10 years or more.

You can see this from the chart below. And if the Great Depression is any guide, what happens next is that:

- Interest rates stay low… for a long time

- Money printing is going up… a lot

And what is the impact of that?

If the Great Depression is any guide – inflation, big inflation.

3 things that worry me short term

But the Great Depression was also unique because it eventually resulted in World War II, which skewed things in a big way.

I don’t think inflation is a done deal just yet.

Short term, there are 3 crucial macro points to keep a lookout for.

1. Monetary Policy

The Federal Reserve is the most important central bank in the whole world. 70% of global trade is denominated in USD, and USD liquidity determines financial conditions for the whole world.

That is why as investors, we hang onto every word Jerome Powell says.

The recent remarks though, are worrying.

What they’ve been saying, is that they will commit to keep interest rates low at least until 2024. They will also keep up the current pace of QE.

But very little mention of what else they are going to do next.

This is important because without big new steps from the Feds, a big tailwind for stocks is removed. And that’s why I think we’ve seen major indices mostly rangebound since June when Fed buying started to taper.

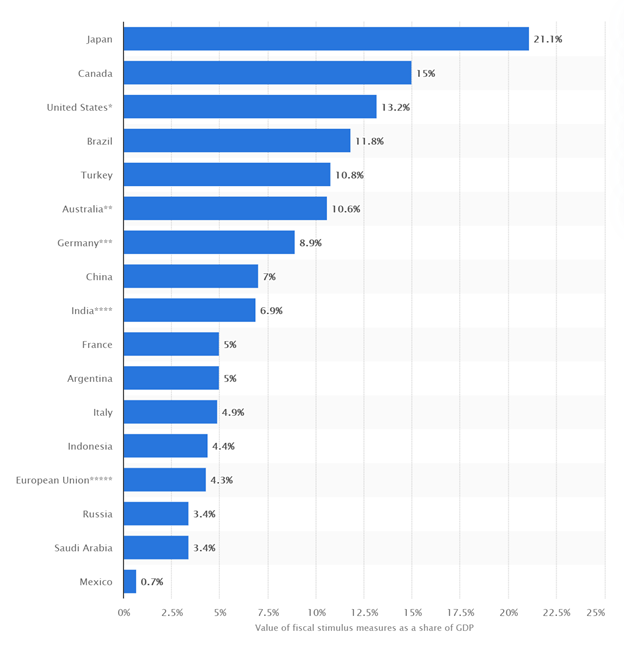

2. Fiscal Policy (Singapore Budget and Global Budget)

Fiscal is the other big one.

We’re in the midst of the worst economic recession since the Great Depression / World War II.

US unemployment is in excess of 10%. Singapore’s unemployment will tick up in the coming months too.

A lot of countries and companies have been kept afloat because of massive budgets run by their local government.

Just take Singapore for example – we dipped into our reserves for a $100 billion budget. That’s 20% of our GDP – putting us right up there close to the top.

We’ve never touched our reserves this way in Singapore’s history, which gives you an idea of how unprecedented this is. And we used that for cash handouts to the population, and income support, corporate assistance etc.

Same in the US, where unemployed were getting more than what they were getting from their day jobs.

A lot of this stimulus was possible because back in March, COVID19 looked like an unprecedented natural disaster. And just like any big natural disaster, it was assumed it would pass, and everything would go back to normal. V shaped recovery right?

Well, it’s become obvious that’s not happening. COVID19 is here to stay at least until we get large chunks of the world vaccinated.

What started out as a sprint, has evolved into a marathon.

And I believe fiscal policy will become more challenging going forward. We’re already seeing that in the US budget delay, Singapore’s reduced $8 billion budget, and in Europe.

COVID19 started out as a supply and demand shock. Increasingly, it looks like supply can recover quickly, but demand is much slower.

Once COVID goes away, the factories reopen, and they start building cars. But because people are unemployed or worried about their job, they no longer buy cars at the same pace they used to.

So going forward, I expect more fiscal policies directed at the demand side rather than supply side. Cash handouts direct to consumers, or something like the SingapoRediscovers campaign for example.

3. Virus Situation

We’ve talked about the virus in the past, so I won’t dwell on it too much here.

Long story short – there are still many ways that this can play out, from vaccine by early 2021, to second wave in winter, to evolving into more deadly strain.

Which outcome plays out, will have big economic consequences.

A lot of people are assuming this will all be over by next year. That may not play out.

Bonus Mention: Inequality

The last point I wanted to mention, is inequality.

I don’t know if you guys feel it, but inequality has gone up massively.

It’s been trending up for years now, but it’s really accelerated during COVID.

The rich who own stocks and financial assets have seen a big recovery from the bottom. The poor who work service or frontline jobs have seen retrenchments or paycuts. And frankly, it’s hard to see that changing in the coming months.

It’s no coincidence that the 1930s Great Depression ended in World War II.

Inequality leads to political change.

When people feel the system is unfair and doesn’t look after their interests, they will change the system. In democracies, they will vote for the candidates that can deliver what they want. In autocracies, they topple governments.

Happens all throughout history. Either the system changes by choice, or the system changes by force.

We’re still at the early days for this one. But I think the years to come will bring more social and political instability, that will surprise most of us.

Inflation, or Deflation?

Imagine this – As a government, you have two choices:

- Choice A: In response to COVID, you go into austerity. You raise taxes, and cut government spending. This causes soaring unemployment, increased social instability – but you balance your budget.

- Choice B: In response to COVID, you run a fiscally irresponsible budget. You spend more than you earn in tax revenue, and you flood the economy with stimulus. This reduces unemployment, improves consumer / business confidence up, and the population is happy. The cost is that you run a big budget deficit, which results in inflation and a weaker currency.

Which choice do you go with?

It’s a no brainer right. You go with B.

With A – you run the country into the ground, and eventually you get voted out, to be replaced by someone who goes with B.

With B – you solve the short-term problems, in exchange for longer term problems. But hey – in the longer term we are all dead, so let’s save the longer-term problems for someone else.

Well, the exact same thing played out in the 1930s. When faced with this choice, the world eventually embarked on Choice B.

In fact, the easiest way to solve the budget deficit is also via Choice B – inflation.

Think of it this way, you have a mortgage on your house. The house is worth $1 million, and the mortgage is worth $500,000. If the value of your house goes up to $2 million due to inflation, the value of your mortgage drops drastically relative to the house, because the mortgage amount doesn’t change.

Now imagine you’re the US and you owe the world $22 trillion. And then imagine that your central banks sets monetary policy for the whole world, and you can create inflation if you want.

Same logic here.

How should investors position their portfolio?

The positioning for each scenario is clear:

- If its inflation – you want to own stocks, REITs, real estate, gold, commodities. You want to sell treasuries, bonds and cash.

- If its deflation – you want to own treasuries, safe government bonds and cash. You want to sell stocks, REITs, real estate, gold, commodities.

And that’s exactly the problem.

If you position for inflation, and it turns out to be deflation, you get killed. And vice versa.

Which will we see?

My own view is that mid-term, it will be inflation. It has to be inflation.

The deflationary path is so painful that few governments will be able to withstand it for long. Think about Japan during the 1990s, but multiply that for the whole world. It’s a decade of low growth, soaring inequality, and rising poverty. It’s really the 21st century version of the Great Depression.

It would undo the good work achieved by humanity over the past few decades.

So I don’t believe the deflationary track will last long.

Timing is tricky though. The exact timing depends on the 3 factors above, what governments do, what central banks do, what the virus does. This cannot be predicted with a high degree of certainty, so it pays to be flexible and nimble here.

Interest Rate Increase

One of the Patrons (as did the EndowUs CIO) pointed out to me that if inflation truly gets underway, the classic response is to raise interest rates, which will hit asset prices.

That’s a really good point to be honest.

My personal view though, is that this time is different. I think this time around, the budget deficits the US government are running are so high that interest rates cannot be allowed to go up, otherwise the cost of financing the debt would become prohibitive.

Some of the latest comments from Jerome Powell hint at this as well, that they’re going to run an irresponsible monetary policy that allows inflation to overshoot their 2% target.

Because of this, I think the Feds will eventually implement yield curve control – where they artificially set interest rates from the short end to the long end, and buy as much treasuries as required to effect that.

The last time this was done was in the 1940s, where there was a soaring budget deficit (to fund WWII) coupled with zero interest rates due to the Great Depression.

Very similar dynamic today – where a soaring budget deficit (to fight the effects of COVID19) meets zero interest rates due to the end of the long term debt cycle that started in the 1970s.

If so, Feds will buy all the new treasuries issued by the US government to keep long term interest rates low, and the US government will take that money and spend on whatever they want (unemployment checks, infrastructure investment etc). That would be inflationary.

I could be wrong of course. Time will tell.

Update: Had some really great comments and discussions with readers. To sum up my views here:

1. We were nearing the end of the long term debt cycle even pre-COVID, so this was always going to happen. What was unexpected was that it was a pandemic that set everything off.

2. COVID is short term deflationary, but the eventual response here will *most likely* be inflationary in the mid term.

3. So from a positioning perspective, if I am right – it will be for deflation short term, transitioning into inflation mid term.

4. The timing is tricky though, because no one knows when deflation transitions into inflation (some may argue we are already transitioning into inflation as we speak). As investors, options are to go early, or build a balanced portfolio, or try to remain flexible and nimble.

5. And the worry comes in because very few of us alive have experience investing in an inflationary environment. The last one was 1970s (and before that the 1940s). Both were very volatile periods in global financial markets. Stocks may have gone up, but picking the right ones, and ensuring they outpace inflation, were not so straightforward.

Love to hear your views!:)

Closing Thoughts: Am I being overly dramatic?

Some people may think I’m being hyperbole horse here.

And you know what, I hope they’re right.

I hope I’m wrong, and after COVID, everything goes back to normal. The economy recovers, unemployment drops, interest rates go back to normal, and we have low inflation. That’s the best case outcome here.

But I genuinely don’t see that happening. I think whether we like it or now, we’re on the cusp of the greatest financial, economic and geopolitical reset since World War II.

We have the end of the long term debt cycle, together with a once in a 100 year pandemic that triggered the biggest economic downturn since World War II, together with record levels of inequality and unemployment. Throw in a rising China seeking to disrupt the existing status quo, and we have the receipe for massive change.

As the quote by Lenin goes: “There are decades where nothing happens; and there are weeks where decades happen”.

The pre-COVID world has ended. The world we emerge into, will be fundamentally different from the one that went into COVID.

Denying that, will not prevent it.

Better to embrace it early, and to figure out where we want to stand in this new world.

Love to hear your thoughts below!

BTW: Anniversary Promo for the FH Course and REITs MasterClass ends this Sunday! Don’t miss the chance to pick up both courses at big discounts – with big freebies thrown in! Check it out here.

Support the site as a Patron and get access to my personal stock watch list, as well as my personal portfolio allocation.

Do like and follow our Facebook Page, or join the Telegram Channel. Never miss another post from Financial Horse!

Join our Facebook Group to continue the discussion, everyone is welcome!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Both are THE best quality investment courses available to Singapore investors out there!

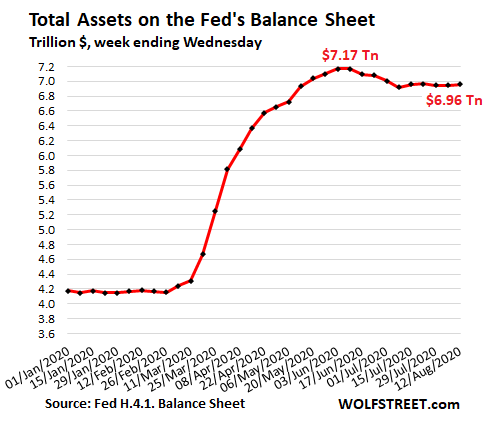

Hi Financialhorse, why is the balance sheet of Fed going down slightly while they continue to buy asset e.g. corporate bonds and keep up with quantitative easing?

Good question actually. It’s because they’re letting some of their existing programs run off. Things like swap lines etc.

So the ones that end are larger than the continuing QE, hence we have a decline in Fed Balance Sheet.

Hi Financial Horse, I really like your articles and they are one of the things I look forward to the weekends for.

However, for this article, I am abit confused by the messaging. For a start, the subject “Why I am worried about the next Phase in stocks” seems to suggest you think the stock market will do badly in the next phase, hence, the worry. You then go on to talk about the “The Insolvency Phase”, which suggests the economy should do badly. (This is the conclusion I draw, apologies if my assumptions are badly mistaken).

The last part talks about government response and how they are almost certainly to go down route B which will lead to inflation. And in an inflationary environment, you would want to own stocks.

And herein lies my confusion, these 2 messaging seems to be conflicting in how the outlook for the stock markets is.

Hi Bin,

Thanks for the support – really appreciate it!

My apologies if the messaging was unclear in this article. To sum my views, it would be:

1. We were nearing the end of the long term debt cycle even pre-COVID, so this was always going to happen. What was unexpected was that it was a pandemic that set everything off.

2. COVID is short term deflationary, but the eventual response here will most likely be inflationary in the mid term.

3. So from a positioning perspective, if I am right – it will be for deflation short term, transitioning into inflation mid term.

4. The timing is tricky though, because no one knows when deflation transitions into inflation (some may argue we are already transitioning into inflation as we speak). As investors, options are to go early, or build a balanced portfolio, or try to remain flexible and nimble.

5. And the worry comes in because very few of us alive have experience investing in an inflationary environment. The last one was 1970s (and before that the 1940s). Both were very volatile periods in global financial markets. Stocks may have gone up, but picking the right ones, and ensuring they outpace inflation, were not so straightforward.

Hope that this clarifies. Let me know your thoughts! 🙂

Cheers.

Hi FH, it would be useful to distinguish between Singapore and US based investors. The US has run huge deficits through the longest bull run in history, the federal budget is out of control, however Singapore is comparatively stable and well managed. Price shocks can transmit across borders, though flexible exchange rates do provide a cushion. Weimar hyperinflation didn’t affect the French Franc for example (though the French had their own problems!). SGD has appreciated against all the major currencies over the last two decades, that’s likely to continue with the ongoing debasement of USD, GBP, EUR and JPY. In such a scenario just holding SGD assets is a USD inflation insurance. So what’s the case for Singaporeans being adversely impacted by US inflation?

Hi Matt, that’s a really great point actually. Thanks for raising this. And you may be right actually.

Some personal views:

1. SGD is weighted against a basket of currencies, of which the USD and RMB have heavy weightage. If both currencies are debased, it would be unlikely for the SGD to remain strong for long, because that would severely hit Singapore’s competitiveess.

2. Singapore’s economy is very open. With massive global stimulus, some of that money will flow into Singapore. Post 2008, we saw strong inflationary pressures on SGD assets.

I definitely take your point though. Perhaps one way to hedge will be to own SGD assets.

The question then is what kind of SGD assets? Bonds yield too low to be good long term investments. Stocks carry their own risk, especially as SG companies are weighted towards old world industries, some of which may not fare so well going forward. If its say a company / REIT with foreign assets, then the underlying exposure is still to foreign assets.

Again, really great point that I will take into consideration going forward.

Thanks for your response. Very interesting. I don’t know enough about how the SGD is managed but it’s certainly logical to assume an highly open economy like Singapore’s would not be immune from a wave of global inflation.

Hi FH, thanks for taking the time out to respond and engage with your readers!

My 2 cents worth – I think alot of my viewpoints are probably influenced and shaped by what I read here. At the risk of sounding like an echo chamber, I think the COVID-led recession is going to be deflationary (recession is almost by textbook definition deflationary), but the government response to the recession will be inflationary. The timeframe and impact of deflation will be so negligible, that we might not even see or feel it, and the inflationary response will take over.

As an investor, I think we not only need to recognize where we are and where we are headed, but also how to position and potentially benefitting from it. In a “post-COVID” new world, the obvious winners are the big techs, and that is what everyone else has recognized and priced in, as evident by the big techs at or around their all-time highs. And here is where the conundrum lies for me. Whether to bite the bullet and buy at record highs, or hold out and not get sucked into this frenzy rally and risk missing out altogether.

Hi Bin

No problem at all, I love hearing from readers, so never hesitate to leave a comment / query!

Yes, I do agree with that. Deflation short term into inflation mid term, but the uncertainty is over timing, and how we get there. The immediate short term doesn’t look so straightforward, because of how COVID is playing out unevenly globally, and fiscal and monetary stimulus are no longer at the levels we saw earlier this year. So there could be some volatility heading into year end.

The rest of 2020 will be an interesting time to watch.

Yeah I do get the dilemma. The solution ultimately has to take into account your own personal situation as well (current asset allocation, job security, risk appetite etc). For me I’ve been averaging in since March, and I plan to continue doing so over the next 6 to 12 months as COVID continues to play out. The questions then are when to increase / decrease pace of buying, and what counters to buy. And which positions to close or take profits.

Thanks for your informative articles on investing especially on the Singapore Stock Market. As I live in the West Indies, Singapore is a fascinating Country and I am interested in investing here – diversify some. As I am more familiar with the US/UK/Can market, my comment would be based on these markets. Basically all stock go up, down, sideways and after the recent run up in Tech stocks there will be downward swing.Based on herd behaviour, panic we will see a potential sell off in stocks for good and bad reasons. Add to this the current Covid situation and it may just get a bit ugly. Best bet is to follow your above recommendations and hold on for a hard ride ( easier said than done ). The problem though with bonds, cash and treasuries – low to zero yield.

Some cash is useful for “dry powder” as is often said.

Thank for writing in! Absolutely agree with you. 🙂

Hi FH,

Thank you for the article, my favourite source of economy insights.

Have a question on bonds and Reits, hope you can share your thoughts, thank you.

In your example, it sounds like stagflation.

Low economy growth, high unemployment, zero interest rate, high inflation.

If stagflation does play out, it is likely that we will get zero interest rate for years to come.

Question about bonds

High inflation will erode future cash payments but this applies to both bonds and Reits.

And if interest rate remains at zero, wouldn’t this be good for both Bonds and Reits?

New bonds will have a coupon payment comparable to the old bonds

Specially if the Fed applies yield curve control?

Question about Reits

In stagflation, wouldn’t Reits have problem renting our their space?

Lower FFO = lower share price?

If stagflation is good for Reits, is it because high inflation will result in higher property prices which will allow them to leverge more since interest rate is zero thus allowing Reits to acquire more properties. This in turn will improve their FFO and eventually improving their share price and yield?

Buying more properties, despite a higher vacancy rate, as long as the yield on the property is still positive is sufficient?

Sorry if i had mixed up some points and sound confusing.

Hi Simsnatelan,

Thanks for writing in!

My thoughts:

1. The problem with bonds is that if interest rates are at zero, the coupon you get on your new bonds will be close to zero as well. So the bonds you bought pre-COVID will still pay good returns, but when they are redeemed and you need to buy new bonds, you will be getting poo rreturns on those.

2. Theoretically and historically, in stagflation style scenarios, REITs do well because real estate is seen as a hedge against inflation, driving up demand for real estate and real estate prices. If you buy high quality real estate, the rental prices can also rise in line with inflation because they will have pricing power.

Hope this helps! 🙂

I like your comment on inequality. Think Covid has super charged the gulf between the have and have nots (new economy sectors vs old economy sectors, capital vs labor, white collar vs blue collar) even further. I highly recommend this article.

http://www.collaborativefund.com/blog/here-we-are-5-stories-that-got-us-to-now/

I think this is the proverbial slow boiling frog that is not being priced in by the markets. It has the potential to upend our current economic and political systems if not properly addressed.

Thanks for the link! Yes I do agree that inequality is going to have big consequences down the road. We’re already seeing that expressed in social and political unrest, and given how COVID has exacerbated the entire situation, I do expect this to get worse going forward.

Hi Sir

I tthought the global share markets already priced in for a possible global recession in March through requiring a higher risk premium so going forward from this point even if the virus were to disrupt regular international business and trade is it possible to crash again? But you also mentioned the US FederalReserves are providing all the liquidity to financial markets with QE and 0% rate there is no chance that the actual future deflation can do any more damage? I am worried for my sons college fees. Thankyou

Hi Tan,

Well no one knows for certain, and the market has a habit of making fools out of very smart people.

My personal view is that COVID has caused unprecedented damage to the global economy. The stock market now is being propped up by massive monetary and fiscal stimulus. If that continues, stocks will continue to go up. But short term, I genuinely cannot rule out the possibility of another turn downwards short term – eg. if a real second wave comes back, a delay in vaccine timeline, withdrawal of fiscal stimulus, virus mutates into a more deadly strain etc. The range of possibilities in the short term are still very big.

Hi there FH

I realised now admit I didnt understand it that well

“Since early March, high-yield spreads have skyrocketed notwithstanding recent declines, particularly in the sectors most affected by the pandemic like air travel and energy. Similarly, leveraged loan prices have fallen sharply—about half the drop seen during the global financial crisis at one point. As a result, ratings agencies have revised upward their speculative-grade default forecasts to recessionary levels, and market-implied defaults have also risen sharply”

Source : https://blogs.imf.org/2020/04/14/covid-19-crisis-poses-threat-to-financial-stability

Lets hope this virus gives humanity a chance

Hi Tan!

Thanks for commenting! Not quite sure if I get your question though.

As you pointed out, credit has tightened in the short term, which plays into our thesis of short term deflationary pressures, as companies run into insolvency risk. The question then is whether the govt and regulators can do enough to offset these deflationary pressures for the overall economy. 🙂

Hasn’t Japan been running budget deficits and printing money for decades now? Yet they’re still struggling with deflation, as you pointed out. Is it necessarily true that the US doing the same things will lead to inflation? Or maybe Japan is different because there are more powerful deflationary forces at work there?

That’s a really great question, that I expect will be a defining question for the current era.

My view is that the US is different. Because of culture, population demographics, reserve currency status, and because they have the case study of Japan to learn from. US will do the same moves, but with an aim to avoiding exactly what Japan did wrong. So I did think it will lead to inflation in the US medium term.

Could be wrong though. We are well into the realm of forecasting here.

Hi FH,

I absolutely agree with all your points listed above. The only difference is that i would argue is that we are already in an inflationary environment. I expect the overall sentiment will be fearful where investors will flock to safe havens like gold. Investors see a lot of uncertainty and they just dont like it. And for that reason i believe precious metals, tech and biotech will continue to do well

Another important point to consider would be the US presidental elections in November and the possible added stimulus to the american public in order to gain more votes. Inflationary, of course. American politics being what they are, i suspect the overall sentiment would be increased fear over the uncertainty. Add on the riots due to inequality and you have quite a bit of a wild ride.

Good article!

Yeah that’s an interesting view. I do agree that certain parts of the economy (like groceries) are already in inflation. But the broader economy, if I had to guess, I would say is still deflationary.

But you are absolutely right that it depends on the part of the world you are in. US can emerge faster than Europe/Singapore. And in China, it was already inflationary back in Q2.

Agree that the elections are a big one. The days leading up to the elections will be crucial to watch!

Also, did you hear about the repo market crash in sept 2019. That was when the fed pumped in $53 billion into the money markets

Haha, back in Sept 2019 I couldn’t figure out why the repo fix from the Feds were needed. Only this year did it become clear that it was due to the actions from the Hedge Funds.