The last time I sold stocks in a big way was in Jan 2022.

Well – this past week I started selling stocks again.

And I do see myself selling more stocks over the next 1 – 2 months.

So I wanted to share why I did so in this piece, and hopefully it might help some of you guys out there.

3 Reasons why I sold stocks

It came down to 3 reasons for me:

- Is recession coming?

- Equity valuations too high (for this stage of the cycle)

- Uncertainty over what happens next is high

Let’s walk through each of them.

Is recession coming?

As many of you may know, we are at the tail end of the rate hike cycle.

Sure, you can debate whether or not there is 1 final rate hike before the Feds pause.

But almost nobody is arguing that after the next rate hike (assuming there is even one) we’ll be done for this cycle.

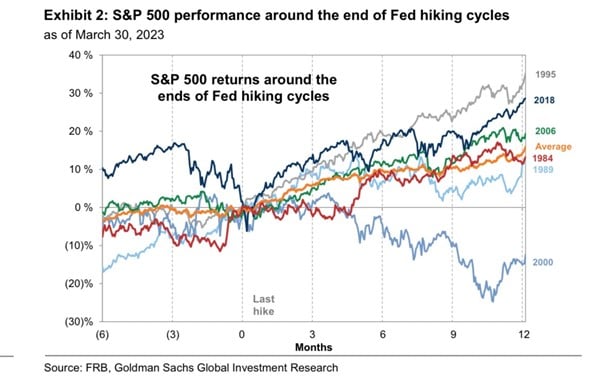

How do stocks do after the end of a Fed hiking cycle?

Here’s the data below:

Let me summarise it for you.

If we don’t get a recession, stocks do decently well after the Fed hike cycle.

If we get a recession, then stocks don’t do so well.

So… do we get a recession in 2023/2024?

Very much will depend on whether we get a recession in 2023 / 2024.

For the record, this is one of the hardest cycles to read in decades.

Because while a lot of leading indicators are turning down, the labour market and inflation remains stubbornly hot, which complicates a lot of signals.

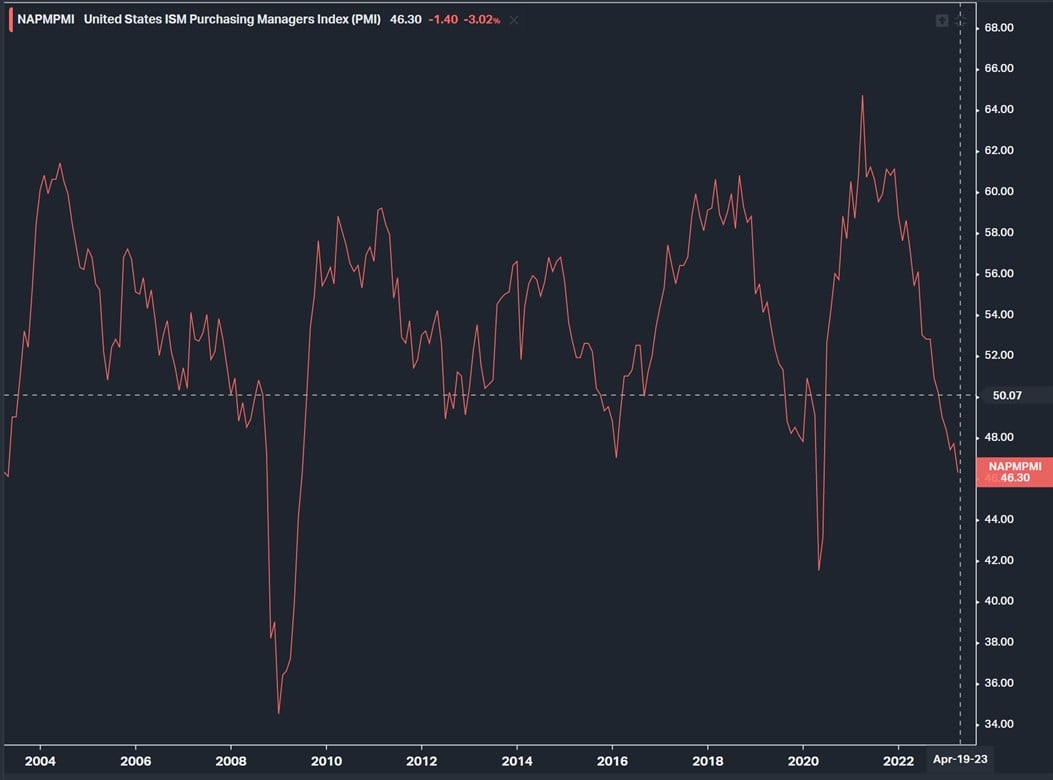

PMI suggests incoming recession…

Here’s the US Purchasing Managers Index (PMI), which is one of the most reliable leading indicators for economic strength.

PMI is currently sitting at 46.3.

The only 2 other times it went this low the past 20 years was in 2008 and 2020, and in both cases the economy was already in deep trouble back then.

This time around PMI is deep negative, and the Feds may not even be done with rate hikes.

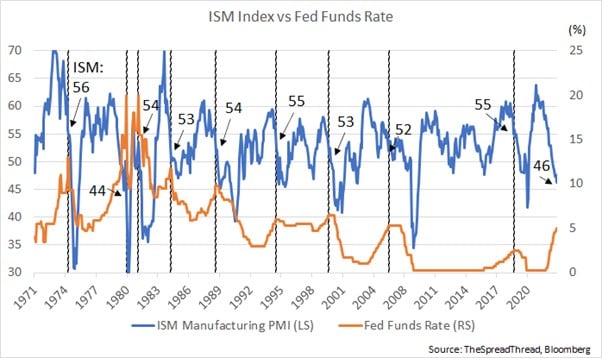

You can see this more clearly below – in almost every other case the past 40 years, the Feds paused rate hikes with PMI much higher than where it is now.

Or in plain English – in this cycle, the Feds will pause rate hikes with the economy in a much weaker starting spot than it was at any other pause in the past 40 years.

This is a very strong argument in favour of an incoming recession.

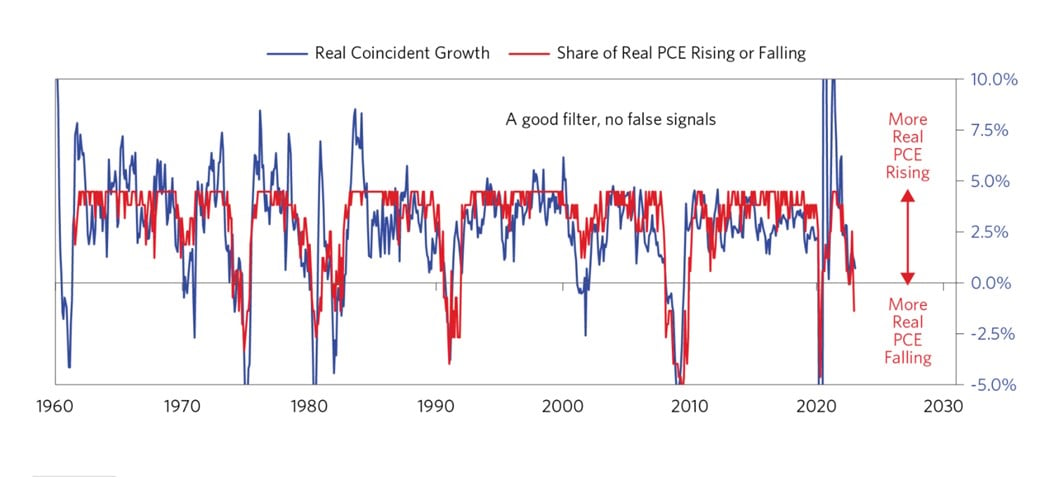

Bridgewater’s proprietary index also suggests recession

Interestingly, Bridgewater has a diffusion index they use to predict recessions.

I extract the key section below:

A diffusion index of monthly real PCE goods demand has been a good filter of recessions.

As shown below, since 1960, in each of the six prior cases that the diffusion index was negative, there was a contraction in growth.

On the other hand, when growth dropped negative but the diffusion index was positive, the apparent downturn quickly reversed.

The diffusion index recently breached the zero line for only the seventh time since 1960—another indication that we’re headed for a third stage of the tightening cycle.

Now this is a proprietary model so we don’t really know what goes into the inputs to independently verify the data.

But still – not looking good.

Equity valuations too high (for this stage of the cycle)

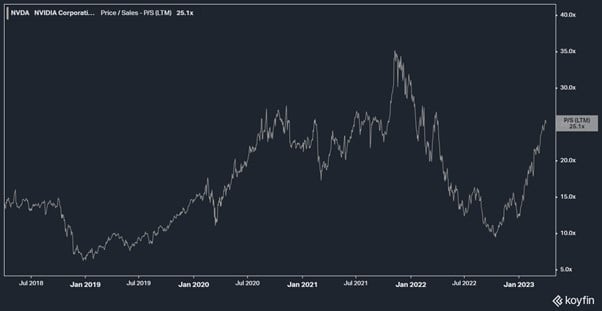

In the spirit of full disclosure – the stock I sold this week was NVIDIA.

I sold about a third of my position (may sell more in the next 1 – 2 months).

Depending on how markets play out the next 2 – 3 months, I may well take profit in further tech stock / REIT positions. Patreon members will get updates as and when I do so.

Why did I sell NVIDIA specifically?

Now I get that bulls will tell me how NVIDIA has a multi decade bull run ahead of it because of the secular trend of Artificial Intelligence and Machine Learning.

But hey, if there’s one thing I know about investing – it is that when everyone thinks a stock can only go up, I am selling. And when everyone thinks a stock can only go down, I am buying.

NVIDIA at 25x Price/Sales.

With the overall macro backdrop, and Fed Funds at 5%.

I think that’s quite richly valued.

Sure the stock may go even higher, but at these prices the risk-reward is no longer attractive – especially after a 150% rally over 6 months.

I was up easily 100% or more from my buy in price, so I figured I would just lock in the gain and go to cash.

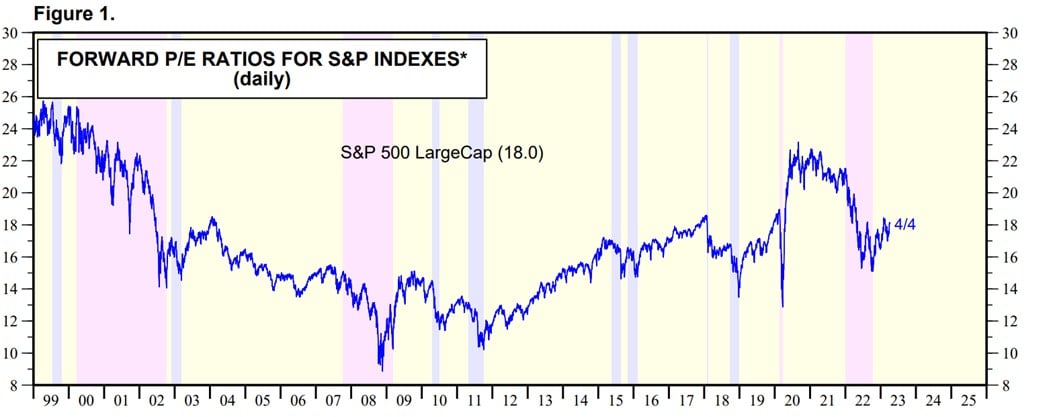

What about stocks more generally?

Forward P/E ratio for the S&P500 sits at 18.0x.

Note that this assumes no earnings decline in 2024.

But if we assume no earnings decline in 2024, that would mean we don’t see a recession.

And if we don’t see a recession, then why would the Fed cut interest rates?

And if interest rates are going to stay at 5%, does a 18x forward multiple make sense?

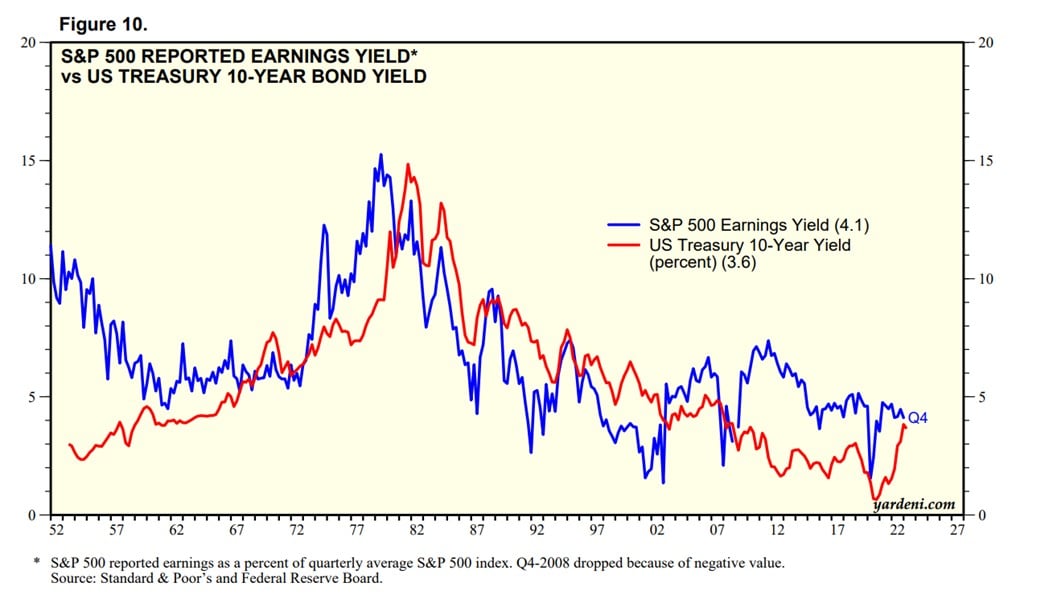

Bonds are attractive vs Equities for the first time in 20 years

If you’ve been following institutional research from the likes of Blackrock and JP Morgan.

You’ll notice that a lot of these sell side desks are now starting to favour bonds (or fixed income) over equities.

You need only look at the chart below to understand why.

For much of the past 20 years since the Dot Com bubble – bond yields were meaningfully below equities yields.

This meant stocks were more attractive than bonds.

But for the first time in 20 years – bond yields are catching up to equity yields.

For the first time in 20 years, bonds or fixed income are starting to look attractive relative to equities.

Which means that for investors, there is now a meaningful alternative to buying stocks.

Retail investors may not be terribly excited by bonds.

But the big boys like Pension Funds and Sovereign Wealth Funds?

If they even start reallocating a small amount of their asset allocation from equities to bonds, that could spark a pretty big move.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

Uncertainty over what happens next is high

Again, I’m just going to put it out there that this is one of the hardest business cycles in decades.

Because inflation is so sticky, the labour market so tight, and consumer balance sheets so strong, many of the signals we use over the past 40 years may not be so reliable here.

I get that.

So a healthy dose of humility is required here.

I have my own thinking on how 2023 / 2024 will play out (that I will share below).

But at the very least, you need to appreciate that the range of possibilities over what happens next is very high.

Equity risk premium needs to go up to reflect that uncertainty.

And in my view, equities just don’t offer sufficient equity risk premium right now.

The risk-reward for owning equities here is not that attractive, relative to bonds.

What needs to happen for a meaningful equity rally?

Let’s discuss what needs to happen to see a meaningful equity rally.

Couple of scenarios I can think of:

- Godilocks (market pricing)

- “Soft landing”

- Big Fed rate cuts

Goldilocks (Market Pricing this in)

This is the scenario where inflation goes down to 2% by end of 2023.

Without a meaningful recession.

Allowing the Feds to cut interest rates by 100 bps (1.0%) by end of 2023.

This is what the market is pricing in right now.

Personally I don’t see this as likely.

I see inflation as too sticky because of the tight labour market.

Realistically you need a 1 – 2% increase in unemployment (minimum) before you can see inflation return to the 2% level.

So unemployment needs to go to 4.5 – 5.5% before inflation can drop back to 2%.

And I don’t think you get that outside of a recession, and in any case not by end 2023.

Simple view – I think this outcome is fantasy.

“Soft Landing”

The other possibility is for a “Soft Landing”.

In this scenario, inflation goes down to the 3 – 4% range.

Without a meaningful recession, or earnings decline.

For the record, I think that this is actually possible.

The main problem with this scenario is that without a recession, the Feds don’t have a reason to cut interest rates.

And if interest rates stay at 5%, I find it hard to see a sustained equities rally.

In any case, a lot of the recent economic data is showing economic weakness incoming, so I’m not sure if we manage to avoid a recession.

Big Fed rate cuts

The final reason of course, is big Fed rate cuts.

If Feds cut rates by 100 bps by end of 2023 like the market is pricing in, I don’t doubt that stocks are going to fly.

The million dollar question though – is what needs to happen for the Feds to cut rates?

You probably need a big recession, or some kind of big equities sell-off, or some kind of liquidity event that threatens systemic risk.

In which case, do you really want to be buying stocks ahead of this event?

My personal views – Do we see a 2023/2024 recession?

Gun to my head though, I think we’ll probably see a shallow recession over a few quarters.

With the leading economic data, all the signs are pointing towards a period of economic weakness in 2H 2023 – 1H 2024.

I shared the charts in last week’s post, and basically this period will see:

- Consumer balance sheets weakening

- COVID era stimulus running off

- G7 central banks at terminal interest rates

- Inflation stabilising at the 3 – 4% range hitting consumer spending power

Paradoxically, because we had a “banking crisis” quite early on this cycle that scared the Feds off, we may not see that big a recession.

Nothing as big as 2008.

So base case I would say we see a shallow recession.

But when the recession comes, the Feds will panic and cut interest rates.

And that will pave the way for a second round of inflation, setting up the next big play.

What will I do with the cash after selling stocks?

I’ll probably sit in the cash for a while and let things play out.

The yield on cash is good, close to 4% depending on how hard I hunt around for Fixed Deposits or T-Bills.

And cash gives me optionality to buy in the months ahead.

There are quite a few REITs like Keppel KBS US REIT, Digital Core REIT, Daiwa House Logistics Trust, Lendlease REIT, Keppel REIT etc that catch my eye, and which I may buy in the months ahead.

I wrote quite a lengthy for for Patreons this week on Keppel KBS US REIT, and at the right price I could see myself buying a position.

Quite a number of tech stocks like Cloudflare interest me as a long term position as well.

As do energy stocks if we get a recession induced sell-off.

So I’m freeing up the cash to give myself optionality in the months ahead.

What worries me – Everyone is underweight equities

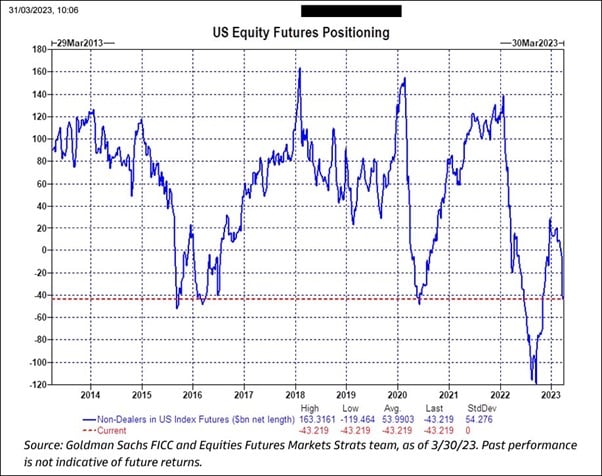

What does worry me though, is that everyone seems to be underweight equities.

You can see this below, most hedge funds and institutional investors are running their lightest equity allocation in a decade.

Because of this, there could be room for the market to continue to run up in the months ahead.

Market likes to take the path of max pain – so if everyone is underweight, the path of max pain is up to force buyers on the sidelines in.

This matters if you are an institutional buyer (because if you miss out on a rally your clients will fire you).

But for retail investors, I don’t see a need to chase this market.

At least until the fundamentals / monetary policy start to change.

What about S-REIT valuations?

Now the discussion above was mainly for stocks.

But what about REITs?

Are REITs overvalued at this price?

Just some quick numbers:

- CICT’s long term dividend yield is about 4.76% (2.6% spread vs risk free)

- CICT’s current dividend yield is 5.07% (2.26% vs risk free)

So… slightly overvalued vs historical levels.

But nothing too crazy.

My Personal View on REITs?

REITs are in a funny place where the small cap REITs like Keppel KBS US REIT can be trading at 50% discount to book and 15% dividend yields.

While the blue chip REITs like CICT are still slightly overvalued vs historical yields.

Reasoning from first principles – if we have a mild recession that forces the Feds to cut rates.

And we don’t get a liquidity event.

Then maybe these blue chip REITs won’t drop much – given that they are holding Singapore real estate, and backed by strong sponsors.

And they just trade sideways for a bit, until interest rates go down and allow them to rally.

For the record I can actually see this happening.

But… does risk-reward make sense?

But again, it just goes back to equity risk premium here.

It feels like a situation where if everything goes right for REITs, I get to collect my 5% a year dividend.

But if something goes wrong, I could eat a fairly big capital loss.

In a climate where I can get close to 4% risk free on cash, I’m not sure if the risk-reward makes sense.

So if we get a meaningful rally, I do see myself taking profit selectively in REIT positions that I think are richly valued.

Patreons will get updates on my latest thinking as and when I do.

Why I sold stocks this week

So to sum up.

We are now approaching the part of the cycle where bad news is bad news.

This is a big change from 6 – 12 months ago when bad news was good news (because it meant less rate hikes).

This is a big paradigm shift, and indicates that investors should be more concerned about recession going forward (than rate hikes).

And with the range of possibilities over what happens next very high, I just feel equity risk premium is underpriced here.

So I took profit in certain positions that I thought were richly valued, and may continue to do so going forward.

I am by no means bringing equity allocation down to zero though.

There are still long term positions in ETFs, banks, REITs, tech and energy that I continue to hold.

But hey – that’s just me.

Love to hear what you think!

This article is written on 7 April 2023 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon, together with weekly premium macro updates like this one. You can access my full personal portfolio to check out how I am positioned as well.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

WeBull Account – Get up to USD 500 worth of fractional shares (expires 28 April)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares.

You just need to:

- Sign up here and fund any amount

- Maintain for 30 days

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Yeah there’s a line that I like, “bonds are pricing in recession and equities are pricing in AI”, I’m sure we know how this will end.

Haha love it!

I’ve subscribed to Hedgeye for market timing since 2018 and they’ve been right, both on the bull and bear side. They now expect a recession:

https://www.youtube.com/watch?v=iuKTvwgXsq4

Not much to do now, just studying companies to buy for the next bull.

Yeah that would be my base case as well. What is less clear is how deep the economic slowdown will be? And how (and when) the Feds start to cut interest rates?

Those will determine what and when to buy, so there is still much to play out!

Given there’s no mention about gold or precious metals, I presume it’s not an asset class in your consideration? If so why?

I do actually. I used to trade in and out of precious metals in the past (gold / silver), but hold no trading positions at the moment.

I also hold fairly meaningful amounts of physical gold as well, but those are intended more as long term holdings and not so much for trading.

Dear FH

Thanks

This is a difficult predicament for most serious investors

While I fully agree on taking some profits , overall it might be a better idea to stick on as there are several factors favouring equities here

We are probably already in the early throes of recession and more data will be coming in but of no value to us as they are lagging indicators

Inflation is not the worry anymore even if this week Pce disappoints

On the contrary, if the figures are better, you will see the SPY at 4200 by Thursday! Tech will lead the rally and although it is overvalued on paper, it will be chased !

I took a very small amount off the XLK but hold most of it

At 152/3, I will start selling again but sell more only with higher prices

The SG market is ok to hang on to

The REITS are fairly valued and I will buy at weakness, not sell now and hope to buy later

The banks will be good long term and are holds with both REITS and banks yielding good cash

In short, high valuations might cause me to lighten up on XLK but not by much

Earnings starts this week- banks might assume higher liability and make provisions issuing cautious statements

This might trigger weakness and I will in fact buy good quality blue chip financials in the US, even with a looming recession risk, as much of it if not all is baked in the price

Regards

Venkatesh

Fair enough! I can get on board with this.

I think it really depends on each individual’s asset allocation vs risk appetite. Those with a high risk appetite and low allocation to equities currently can of course keep the risk exposure.

REITs are interesting in that the blue chips from CapitaLand/Mapletree look fairly valued (although a bit on the expensive side). While some of the smaller cap REITs are pricing in quite severe distress in CRE. Whether the small cap REITs or blue chip REITs will turn out to be right in the next 12 months, is a very interesting question!

Hey FH, thanks again for the comprehensive article. Always a quality read. Regarding your chart on US futures positioning and the takeaway that many hedge funds and institutions are underweight equities – how might this possibly suggest a short-term continued bull run (and for how long)? I don’t fully understand the reasons why “if everyone is underweight, the path of max pain is up to force buyers on the sidelines in”.

Also, who provides the data for this graph? Is it only Goldman’s trading desk (ie, what are the chances that HFs and instis might hold different futures positions with other trading desks)? Thanks a ton.

Because if many people are underweight equities – that means they are less inclined to sell further (already underweight), and have a lot of cash on the sidelines that would be forced in if the market goes up.

This doesn’t hold true in all cases though, so it is just one data point to take note of.

Yes you are right on the data. This is not perfect data because of collection methodology, so take it with a pinch of salt. 🙂