I’ve been getting quite a few questions on the path for interest rates in 2023, especially after the series of bank failures last month.

I’ve been doing quite a bit of thinking on this as well – and I still think the market is pricing this wrong.

And quite a few interesting developments this week both on Singapore Savings Bonds and T-Bills that I wanted to talk about as well.

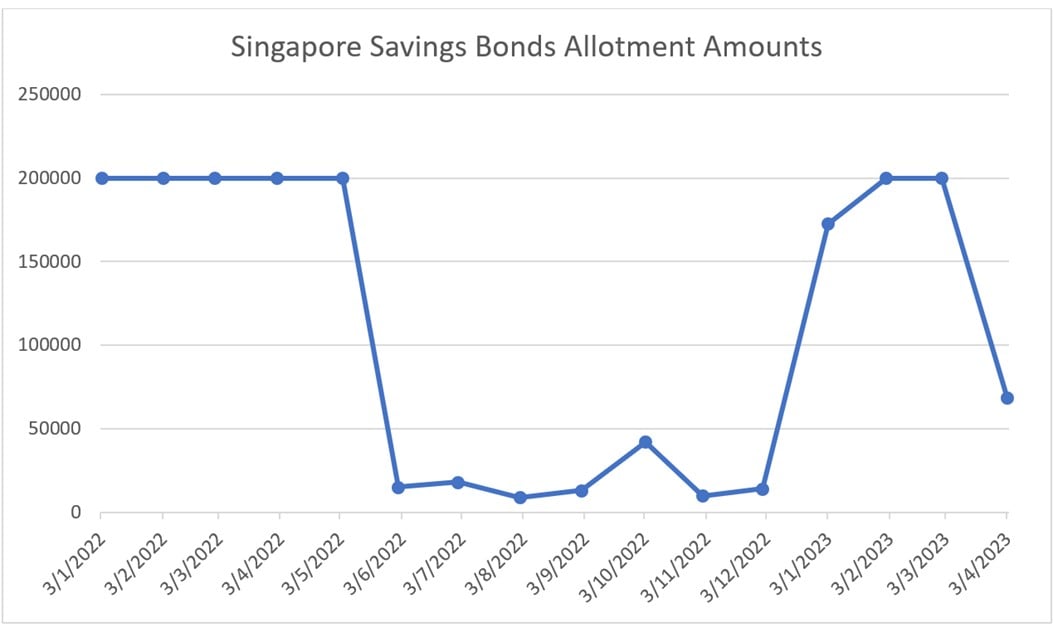

Singapore Savings Bonds Oversubscribed – Up to $69,000 allotment per person

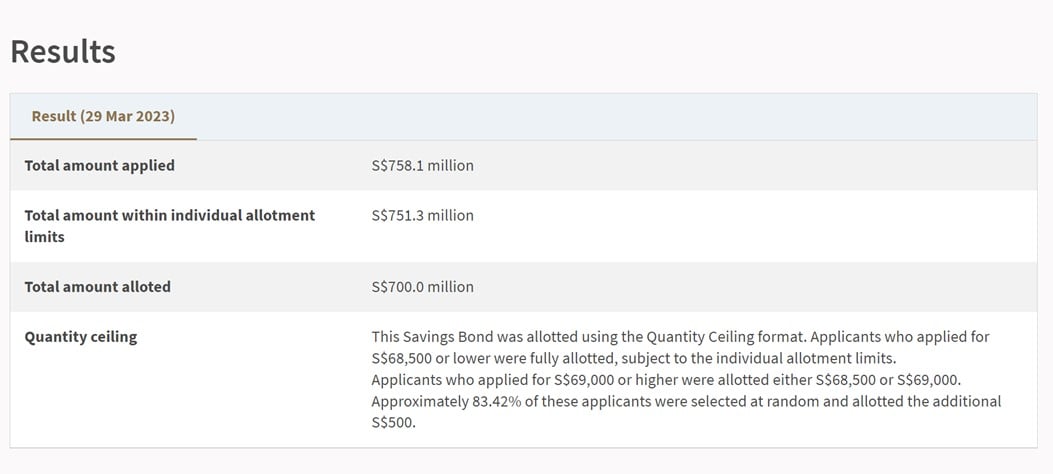

First off – Allotment results for the latest Singapore Savings Bonds.

I shared previously that with the rapid decline in short term interest rates globally, the 3.15% yielding Singapore Savings Bonds suddenly became a decent buy as a way to hedge against rapidly declining interest rates (if the market is right).

True enough – we see a sharp increase in demand for the Singapore Savings Bonds

For the first time in 3 months, Singapore Savings Bonds are oversubscribed again.

Each person only gets up to $69,000 worth of Singapore Savings Bonds.

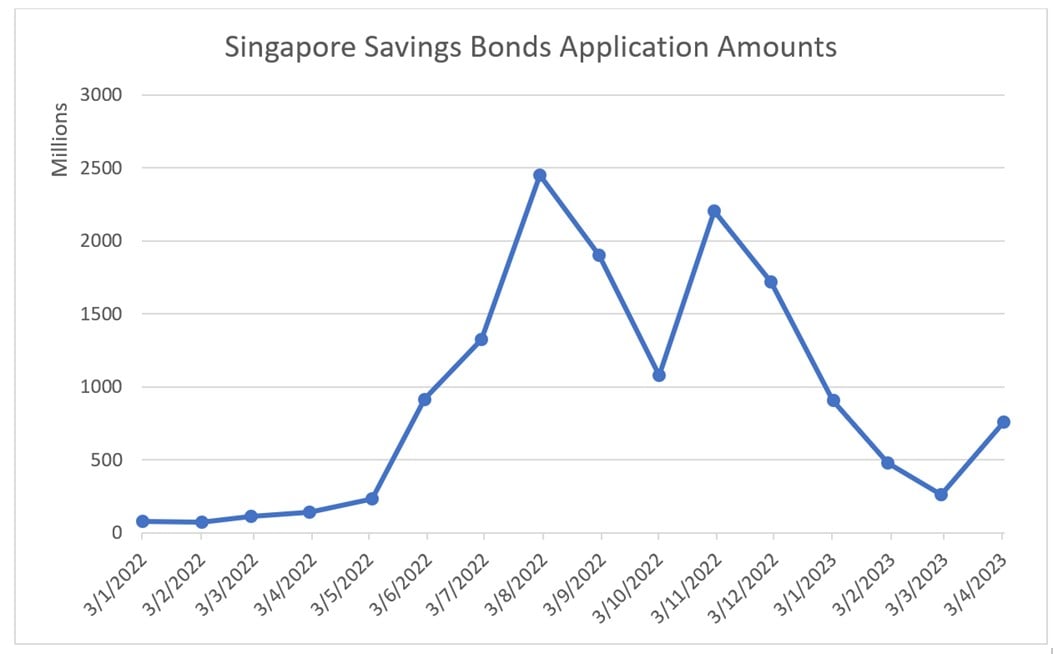

You can see this visualised in chart form below.

Demand for Singapore Savings Bonds is up

Application amount for Singapore Savings Bonds jumped quite sharply from the past 2 months.

But still down very significantly from the late 2022 peak.

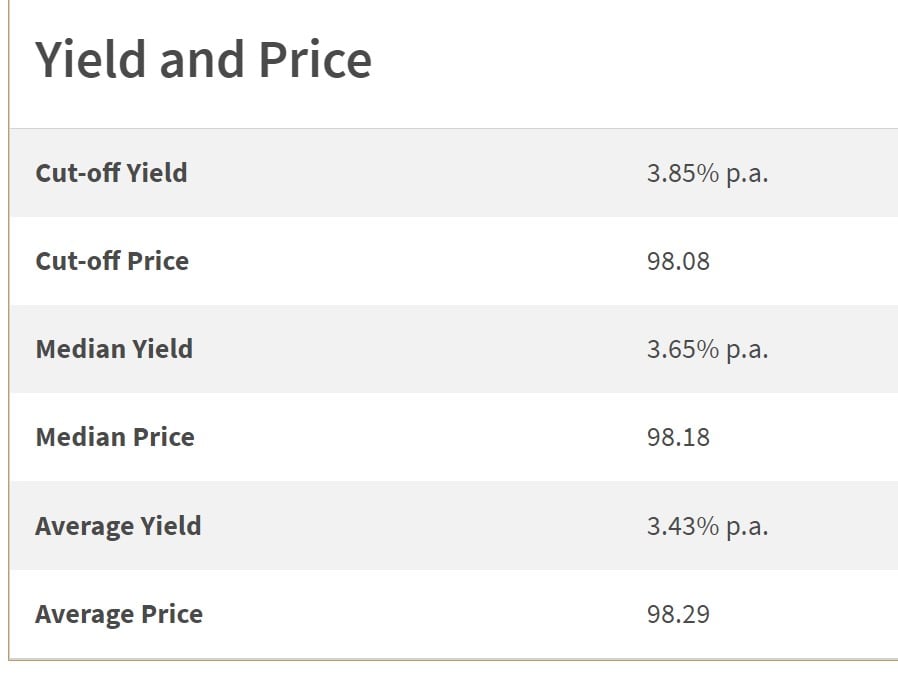

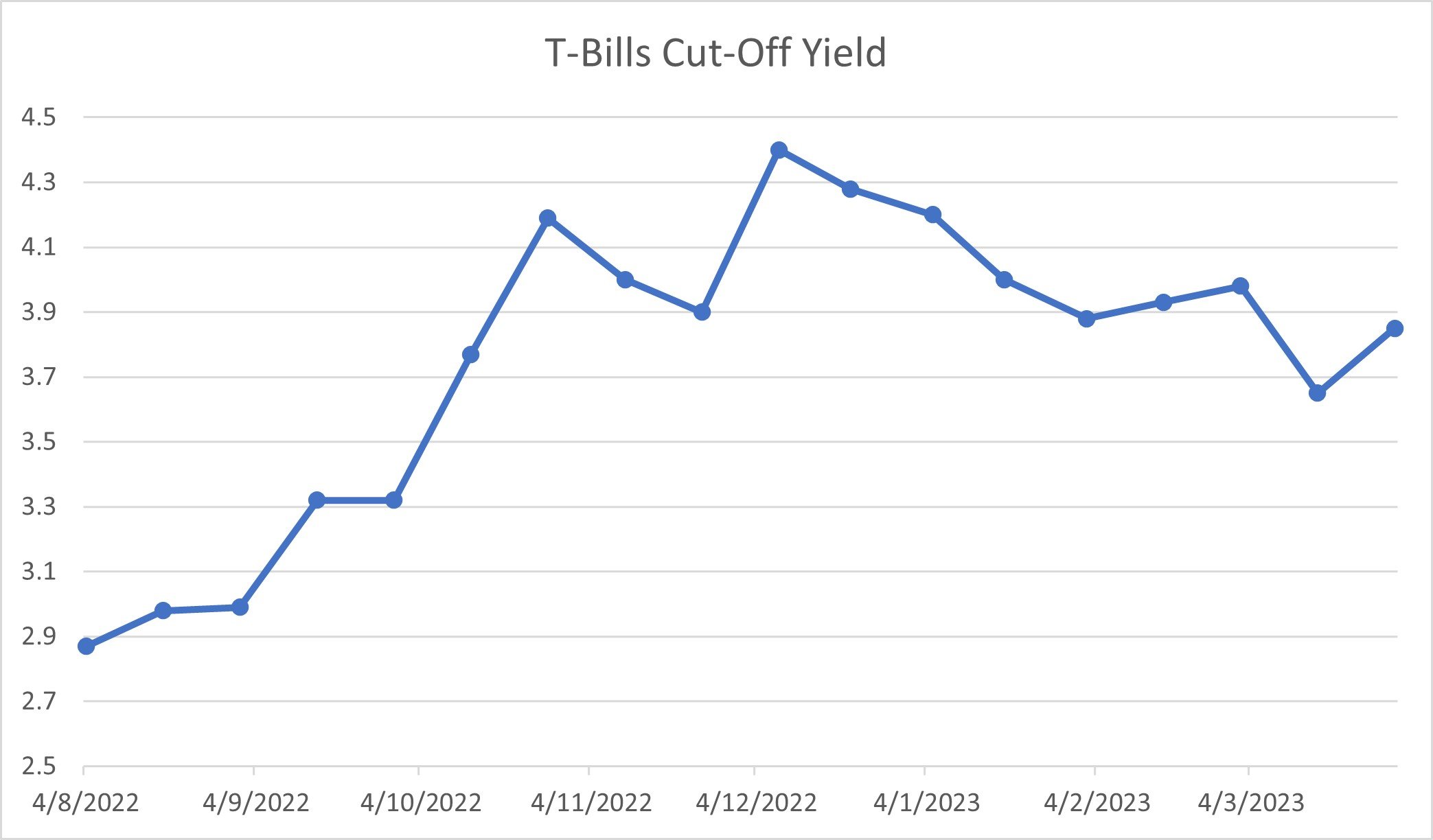

T-Bills issued at 3.85% cut-off yield (30 March 2023 Auction)

At the same time, T-Bills yields also rebounded quite meaningfully to 3.85%.

This is in contrast to 3.65% the previous auction – which was a bit of a freak result due to the flight to safety after the failure of Silicon Valley Bank and Credit Suisse.

You can see this plotted in chart form below – yields are up from the last auction, but still in a downtrend from Dec 2022’s peak:

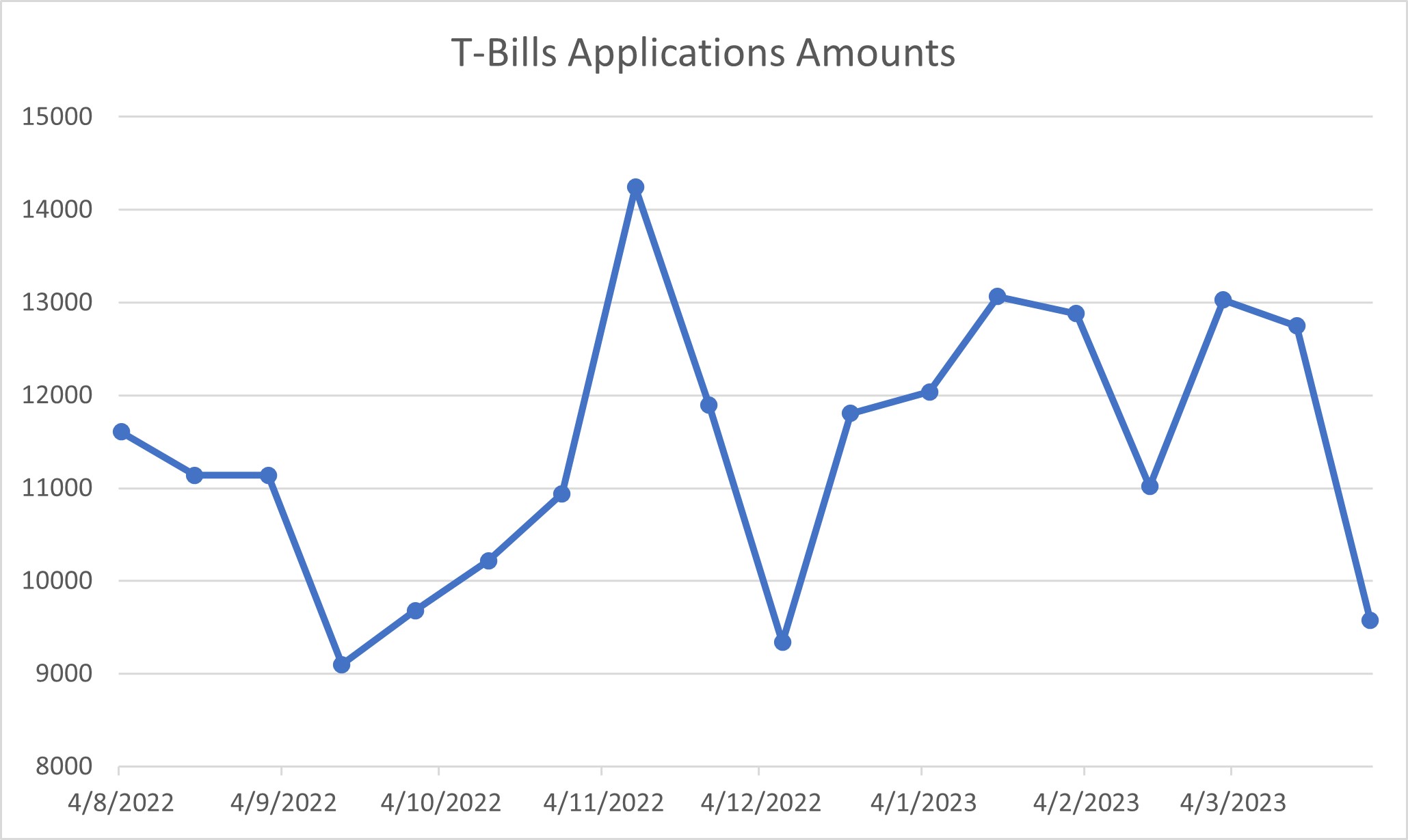

Application Amounts for T-Bills fell drastically

What is interesting is that the application amounts for T-Bills actually fell quite drastically.

From close to $13 billion the previous auction, to $9.6 billion this time around.

That’s almost a 25% drop in application amount.

Why is demand for T-Bills down, while demand for Singapore Savings Bonds up?

Higher demand for Singapore Savings Bonds makes sense since the interest rates for the April Singapore Savings Bonds were decent, especially given the global flight to safety after the failure of Silicon Valley Bank and Credit Suisse.

With the market pricing in rapid interest rate cuts in 2H 2023, didn’t hurt to lock in the interest rates just in case the market was right on this.

Worst case you can just redeem any time and get your principal back with accrued interest.

As to why T-Bills application amounts fell so drastically though, I don’t have any easy answers to this one.

Perhaps investors were shocked by the 3.65%, and decided to switch to Fixed Deposits instead?

Maybe investors were afraid interest rates would get cut in 2H 2023, and decided to lock in a longer duration product via Singapore Savings Bonds or fixed deposits?

Where will interest rates go in 2023?

Let’s now try to answer the more interesting question – where do I think interest rates will go in 2023?

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

I also share great tips on Twitter.

Don’t forget to sign up for our free weekly newsletter too!

[mc4wp_form id=”173″]

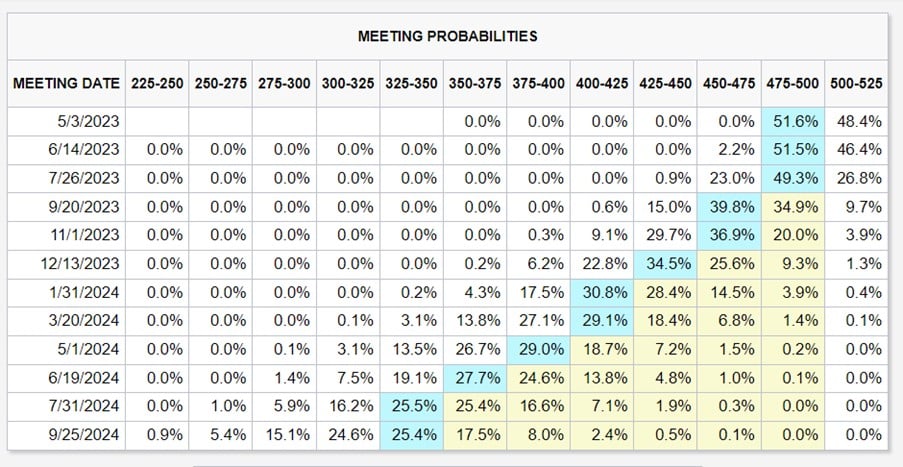

What is the market expecting on interest rates?

Let’s first look at what the market is pricing into the interest rates curve.

The markets are pricing in about a 50% chance of another 25 bps interest rate hike from here.

But it expects at least 2 – 3 interest rate cuts by end 2023.

And another 4 – 5 rate cuts by end 2024.

That’s… very aggressive.

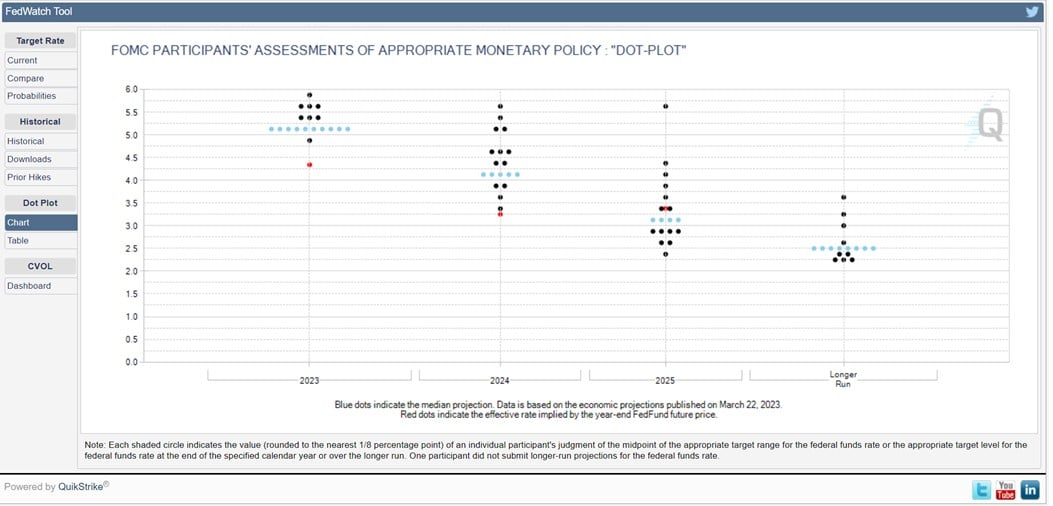

What is the Federal Reserve expecting on interest rates?

By contrast, the Fed Dot plot is much more “realistic”?

It shows interest rates staying at current levels until end 2023.

With 4 interest rate cuts by end 2024.

So basically – the Feds and the market agrees on terminal interest rates being around current levels (or 1 more 25 bps hike from here).

But they differ wildly on the timing of interest rate cuts.

Who is going to be right here?

How do I see interest rates playing out in 2023?

My personal view for now, is as follows.

Terminal Interest Rate – How high will interest rates go?

I think there is about a 50/50 chance of 1 final interest rate hike in the tank, to come into play by mid 2023.

So basically, I agree with the Feds and the market on how high interest rates will go.

Interest Rate Cuts – When will we see interest rate cuts?

I don’t think we’ll see any meaningful interest rate cuts in 2023.

So basically, I agree with the Feds on no interest rate cuts in 2023.

I think the market is way too aggressive on the timing of the interest rate cuts.

Why I think the market is wrong on interest rates?

I shared in a previous piece that I still don’t see a banking crisis this time around.

I see the ground zero for this crisis as not the banking sector.

But the sectors that were overexposed to a decade of low interest rates – Commercial Real Estate, Venture Capital, Private Equity, loss-making startups / tech.

That’s the true ground zero here.

The markets started pricing in rapid interest rate cuts due to the weakness in the banking sector.

But with the Fed’s injection of emergency liquidity, and the “bailout” of Credit Suisse, I think the immediate weakness is contained.

This means there isn’t a reason for rapid interest rate cuts in 2023 just yet.

Which means the cycle can be allowed to extend a bit more.

So… how long until interest rate cuts?

How long though?

How long until the economy weakens to the point where the Feds are forced to cut interest rates?

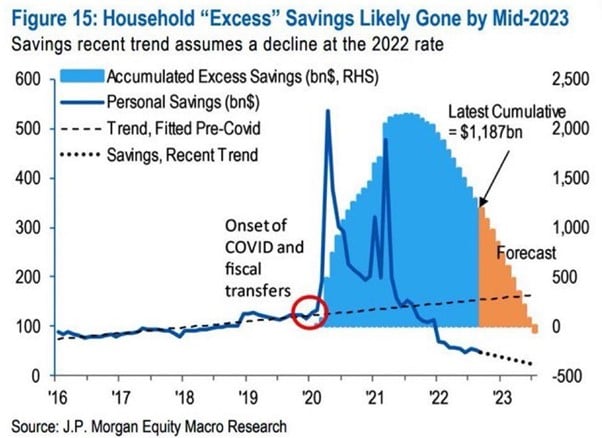

Much of the problems we face today can be traced back to the responses to COVID.

When governments unleashed massive amounts of fiscal stimulus to consumers stuck at home.

This allowed them to build up massive savings – driving a huge wave of consumption both during and post COVID.

So in a cycle that has been dominated by excess consumption – the key will be to look at the consumer.

Strength of the US consumer will fade by 2H 2023

And if you ask me, I think the economic weakness will start to bite in 2H 2023.

Couple of reasons why.

Firstly – by the second half of 2023, consumers will start to run down all the excess savings built up during COVID:

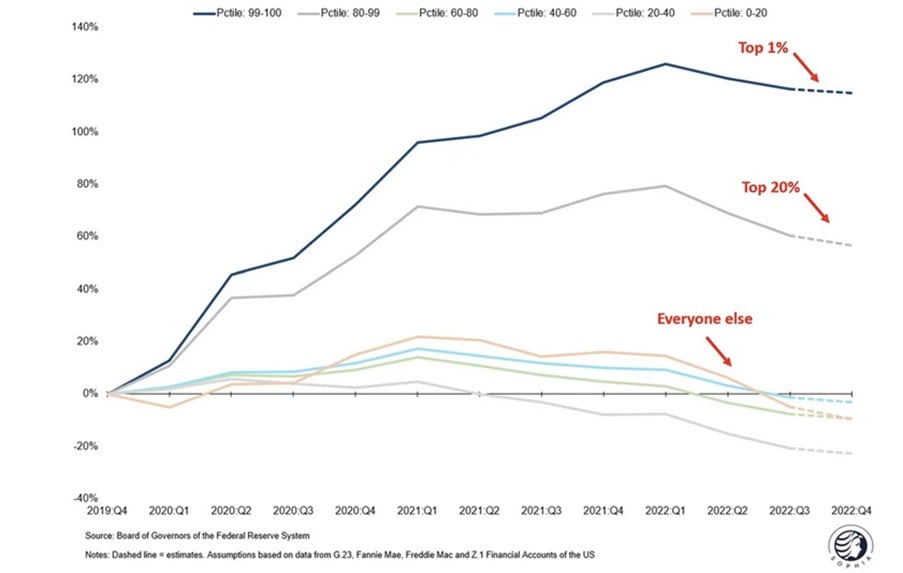

At the same time, higher inflation will start to bite for everyone outside of the top 20% of earners.

While most of the G7 central banks will be at terminal interest rates.

While COVID era stimulus programs start to roll off.

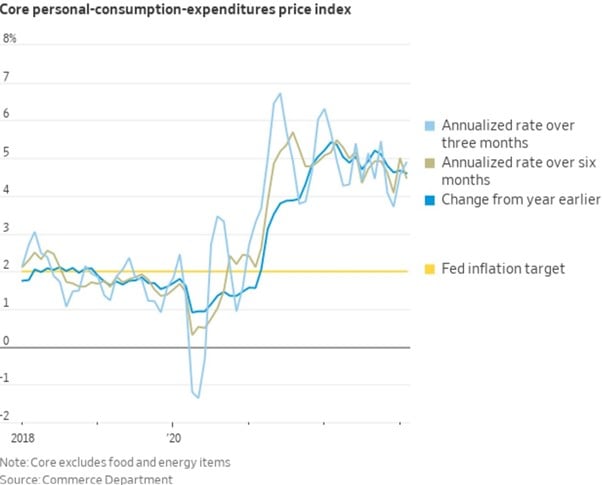

All while inflation starts to stabilise at a 4% range – which bites into consumer purchasing power.

So the stars are starting to align for a period of economic weakness in 2H 2023 – 1H 2024.

How long from economic weakness until Powell is forced to cut interest rates?

Really depends on what breaks, and Powell’s desire to fight inflation vs avoid a recession.

But whatever the case, market pricing on the timing of interest rate cuts looks too aggressive (read: early).

Impact on interest rates?

To sum up, this is one of the hardest business cycles to read in decades because of all the noise.

But I think this cycle has a bit more juice left in the tank.

I don’t think you see rapid interest rate cuts just yet, given that the “banking crisis” is contained.

Maybe 1 more 25 bps rate hike, but interest rates to stay at these levels for all of 2023.

Impact on equities?

Impact on equities is far more nuanced.

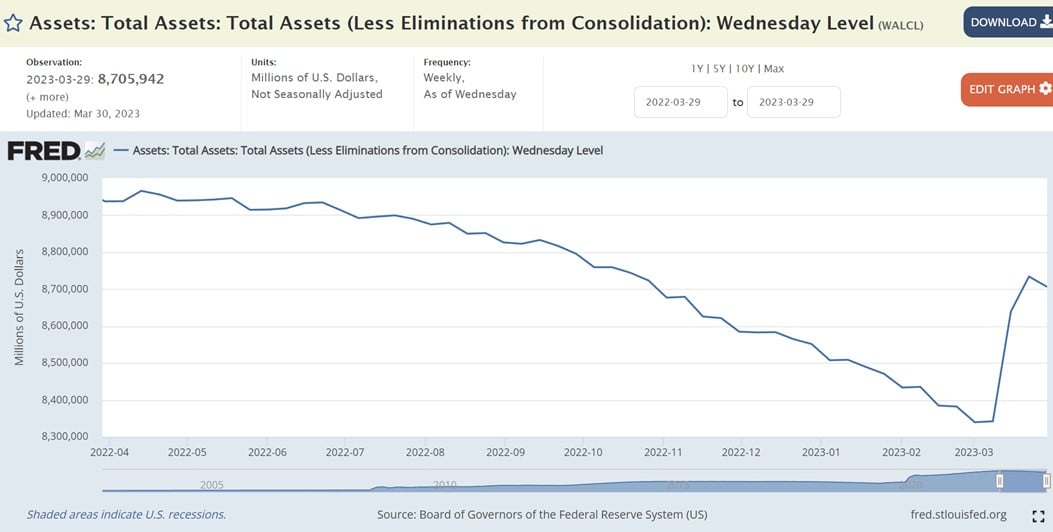

Short term you have massive liquidity injection from the Feds from the Bank Term Funding Program (BTFP).

See how the March 2023 bank failures effectively resulted in liquidity injections that undid the past 6 months of Quantitative Tightening (QT):

This coupled with very underweight equities allocation from institutional investors could create a short term rally (already in the process of playing out).

But look beyond the immediate term, and the factors I set out above will start to come into play.

In 2H 2023 – 1H 2024, you’ll start to see the impact of a weakening consumer and a weakening economy.

Which will start to hit corporate earnings, with unemployment going up, and a cut in corporate capex.

How to invest in the short term?

I’ve been getting quite a few questions from you guys on how to position in times like that.

I’ve set out my macro views above, and I do hope it helps.

It ultimately goes back to individual risk appetite, and your timeframe.

Short term, the liquidity and the lopsided positioning could create a meaningful rally.

But look out beyond a few months, and a lot of stars are aligning for a rough patch for the economy.

So short term traders are free to try their hand at trading.

Longer term buy and hold investors – I still think there’s no need to be a hero in this market. Bide your time, and let the market come to you.

This article is written on 1 April 2023 and will not be updated going forward.

If you are keen, my full REIT and stock watchlist (with price targets) is available on Patreon, together with weekly premium macro updates like this one. You can access my full personal portfolio to check out how I am positioned as well.

Trust Bank Account (Partnership between Standard Chartered and NTUC)

Sign up for a Trust Bank Account and get:

- $35 NTUC voucher

- 1.5% base interest on your first $75,000 (up to 2.5%)

- Whole bunch of freebies

Fully SDIC insured as well.

It’s worth it in my view, a lot of freebies for very little effort.

Full review here, or use Promo Code N0D61KGY when you sign up to get the vouchers!

WeBull Account – Get up to USD 500 worth of fractional shares (expires 28 April)

I did a review on WeBull and I really like this brokerage – Free US Stock, Options and ETF trading, in a very easy to use platform.

I use it for my own trades in fact.

They’re running a promo now with up to USD 500 free fractional shares.

You just need to:

- Sign up here and fund any amount

- Maintain for 30 days

Looking for a low cost broker to buy US, China or Singapore stocks?

Get a free stock and commission free trading Webull.

Get a free stock and commission free trading with MooMoo.

Get a free stock and commission free trading with Tiger Brokers.

Special account opening bonus for Saxo Brokers too (drop email to [email protected] for full steps).

Or Interactive Brokers for competitive FX and commissions.

Do like and follow our Facebook and Instagram, or join the Telegram Channel. Never miss another post from Financial Horse!

Looking for a comprehensive guide to investing that covers stocks, REITs, bonds, CPF and asset allocation? Check out the FH Complete Guide to Investing.

Or if you’re a more advanced investor, check out the REITs Investing Masterclass, which goes in-depth into REITs investing – everything from how much REITs to own, which economic conditions to buy REITs, how to pick REITs etc.

Want to learn everything there is to know about stocks? Check out our Stocks Masterclass – learn how to pick growth and dividend stocks, how to position size, when to buy stocks, how to use options to supercharge returns, and more!

All are THE best quality investment courses available to Singapore investors out there!

Like this article. Probably the best of your recent posts. Keep it up.

Thanks, appreciate the kind words!

Dear FH

Excellent and very relevant

Fully concur with your observations

This is a treacherous market and trading is also going to be very difficult – money cannot be easily made and even if made, can be lost in the next trade!

I am trying to lighten my US positions and raise cash levels actually using this “tech rally”

Valuations are really getting stretched, even for profitable mega cap tech – the forthcoming earnings season is crucial

The US banks report in less than 2 weeks and this might set the scene for moves either way , more likely to the downside!

I will sell more if this rally continues and the SPY might reach 4200 next week

Am happy to harvest small gains and miss out a bit more upside

Ultimately, earnings need to be good enough to justify higher valuations

The local banks might drop in sync with US financials and I am hoping to add more then

In short, with the dollar weakening and oil staying lower with recessionary fears, SG might fare better than US relatively

US healthcare and staples might hold better though they might drop if earnings unexpectedly are robust as “hot money” will rotate more into tech thereby creating another “tech bubble”. The next black swan or credit event will pop that bubble for sure

Best wishes

Garudadri

Agree on this.

Depending on how this Q2 rally plays out, I might take profit in some positions as well. Market looks overly optimistic on rates here.

We look to be heading into a patch of economic weakness in 2H23, doesn’t hurt to lighten up on positions a little.