Like any other Singaporean investor, I follow Singapore property news with a lot of interest.

So when there was a flurry of recent articles on why Singapore Residential Property is no longer a good investment, that really caught my eye.

First – DBS came out with an extensive report on why Singapore Property is no longer a “Pot of Gold”.

Then it was a BT article on why it may make more sense to rent a home rather than buy.

And this week, MND came out with a consultation report suggesting public support for possible changes to HDB rules going forward – including a longer MOP, no rental of whole flat even after MOP, limits on who can buy on the resale market etc.

And then on Wednesday, Minister for National Development Desmond Lee gave a speech where he suggested that a new public housing model would be unveiled soon for HDB flats in prime locations.

Call me a paranoid horse, but that smells like the winds of change to me.

It looks like the narrative around housing is starting to shift.

And when the narrative shifts, it’s wise to pay attention.

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

Check out Part I on How to Pick a Property in Singapore.

Basics: Lots of Commentary about Singapore property not being a good investment

Before we dive into the commentary, it’s important to understand what exactly has been said the past few weeks.

MND: Outreach & Consultation On Public Housing In Prime Locations

We’ll start with the MND report.

The background here is that the government is going to be building new HDBs in the Greater Southern Waterfront Area soon.

The whole Pasir Panjang – next to Reflections / Vivocity area:

As you can imagine, a BTO in that area is going to be hot.

Really hot.

If you’re lucky enough to win the lottery and get a 5 room, you’re probably looking at an easy $400k-$500k profit after the 5 year Minimum Occupation Period (MOP).

Accordingly, it was felt that a change to the existing HDB rules was required, especially for HDBs in these prime locations.

So MND went out in 2020 and did a big survey of what Singaporeans think.

The results were out this week.

The full report is here, but to summarise:

- Majority of those surveyed support new policy conditions for HDBs and think it is fair

- They think the goal should be to ensure affordability at point of purchase and resale

In terms of policy moves:

- Majority support a longer Minimum Occupation Period (MOP)

- Others feel that shorter leases or smaller flats can help with affordability

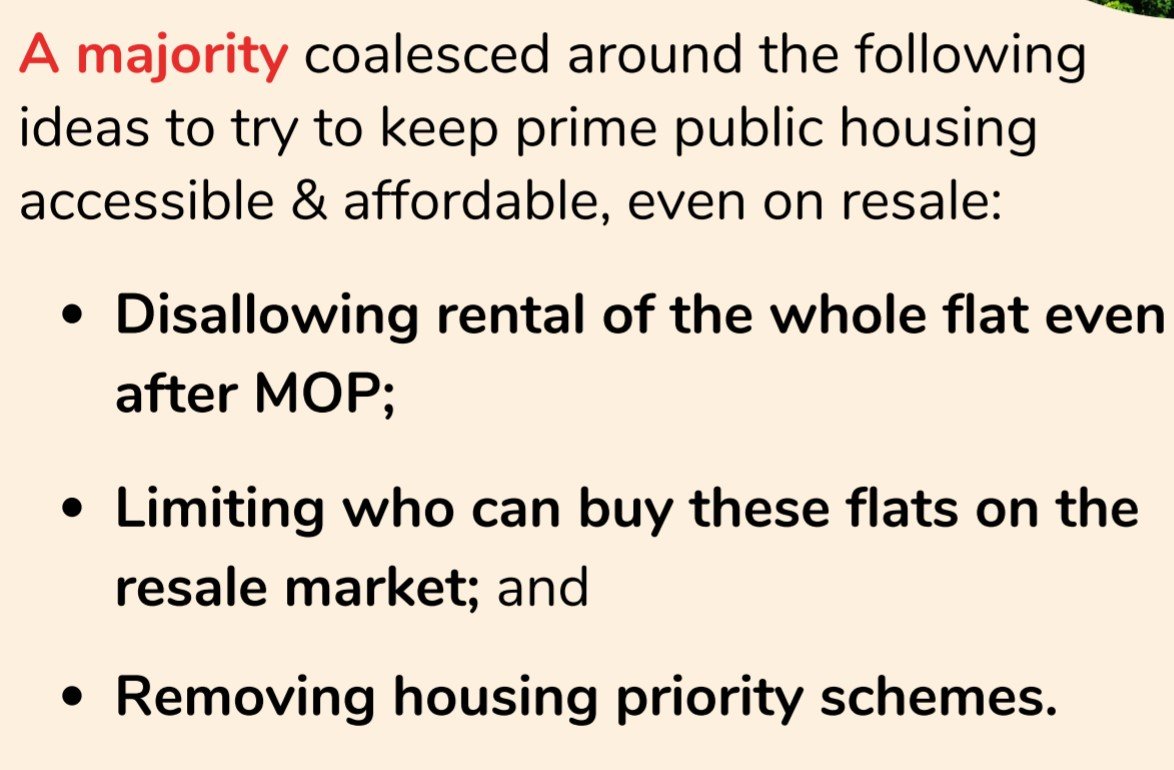

- Majority support:

- No rental of the whole flat even after MOP

- Limit who can buy on the resale market

- Removing housing priority schemes

The consensus seems to be that any changes will only apply to new HDBs going forward though, so if you already bought you shouldn’t be affected.

Speech by Minister Desmond Lee

And then MND Minister Desmond Lee gave a speech this week.

Full speech is here, but I extracted his closing remarks below (emphasis mine):

“Public housing in Singapore goes far beyond putting roofs over people’s heads. It touches almost every aspect of our lives and our society. It enables Singaporeans of different backgrounds to share common experiences, and helps us to build a more cohesive society.

It helps us to build strong family ties, across generations, and it supports vulnerable households to progress in their lives. It supports our health and well-being, at all stages of our lives, especially as we age.

In short, HDB living is an important part of who we are and how we live, here in Singapore.

Virtually no other city in the world is like us in this respect, where such a large proportion of people live in quality public housing, which you build, alongside our colleagues at HDB, where so many households own their homes.

But as much as we have achieved, we must keep pressing on to continually improve our HDB flats and our housing policies in support of the progress of our people and our society, so that Singapore remains strong and united for many generations to come.”

BT Article: Renting is better than owning a private home

Then BT published this commentary by Leslie Yee, which suggests that renting may be better than buying.

Leslie Yee is ex Link REIT Head of Research and then a GM at Guocoland, and now is a Senior Fellow at Institute of Real Estate NUS. So I assume he knows his way around the local real estate scene.

The thought process is very interesting.

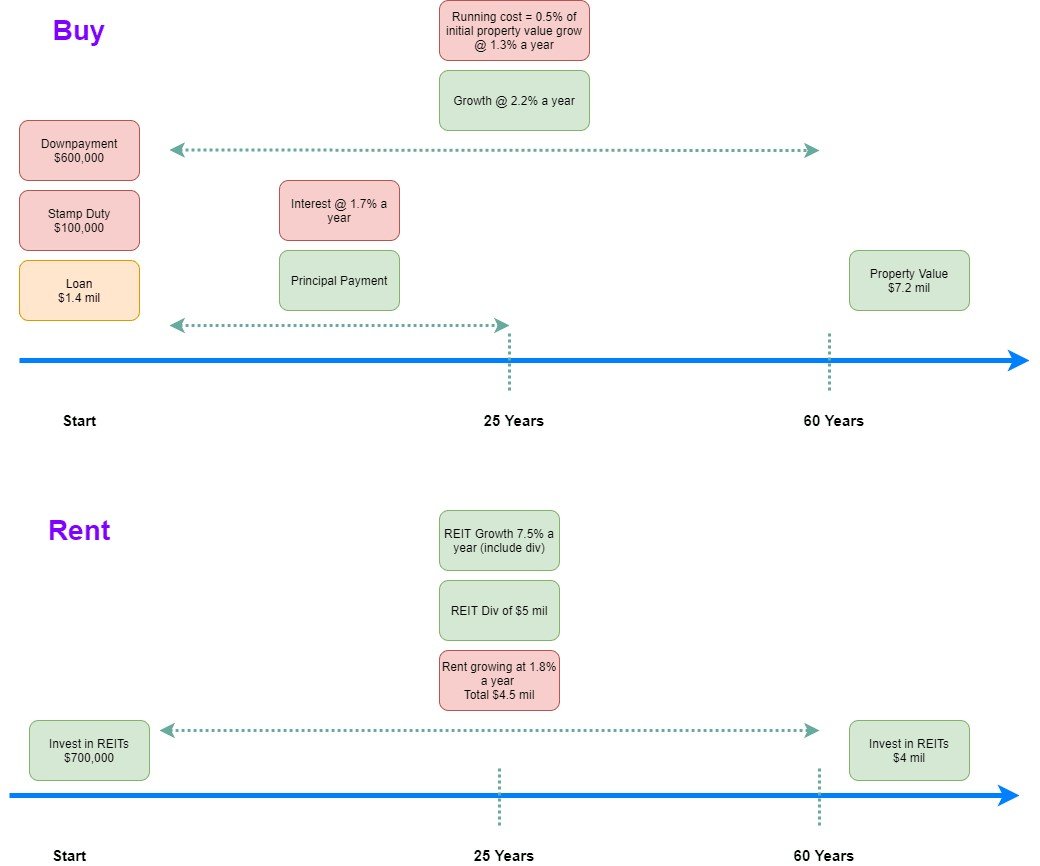

He basically compares 2 scenarios: a buyer and a renter.

The buyer:

- Buys a $2 million home

- Pays $600,000 upfront, $100,000 stamp duty and expenses, and borrows $1.4 million at 1.7% over 25 years

- Value of the house rises at 2.2% over 60 years

The renter:

- Rents a house at $3,500 a month, which increases at 1.8% annually

- Takes the $700,000 cash to invest in REITs, that return 7.5% annually over 60 years

After 60 years:

- The buyer makes $4.6 million (Property value is 7.2 million, less loan plus interest)

- The renter makes $4.6 million (REIT portfolio has value of $4 million and returns 5.1 million in distribution, less off rental)

Both make the same – so renting could be a viable alternative to buying?

You can see this in picture form below:

Source: https://investmentmoats.com/money/permanent-renting-owning-a-private-property/

I know not all the assumptions above are realistic (and we’ll discuss more on this later), but for now, let’s focus on the point that Leslie is trying to make.

Which is that in this market, renting and using the freed up cash to invest could make as much sense as buying a home at record high prices.

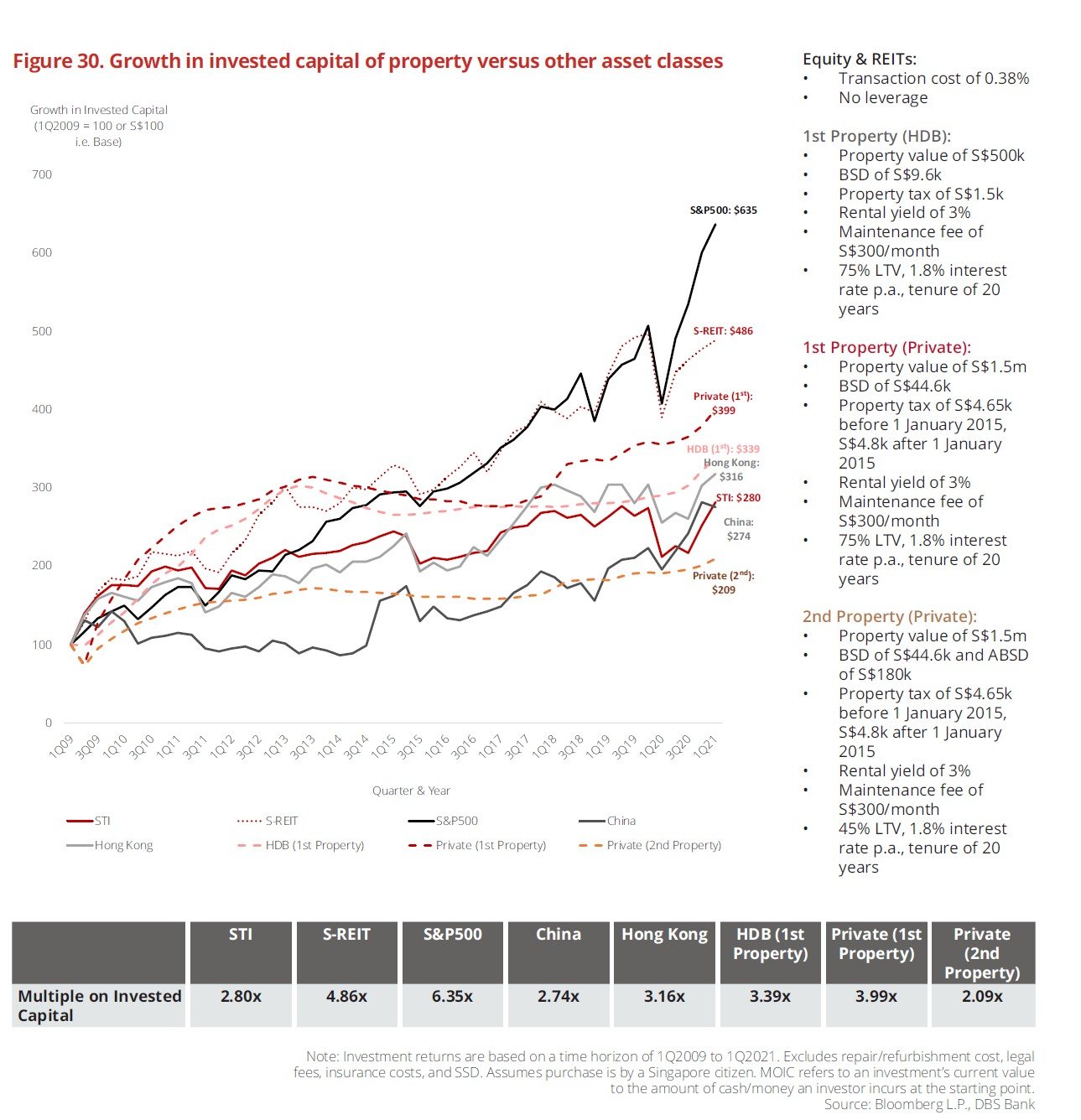

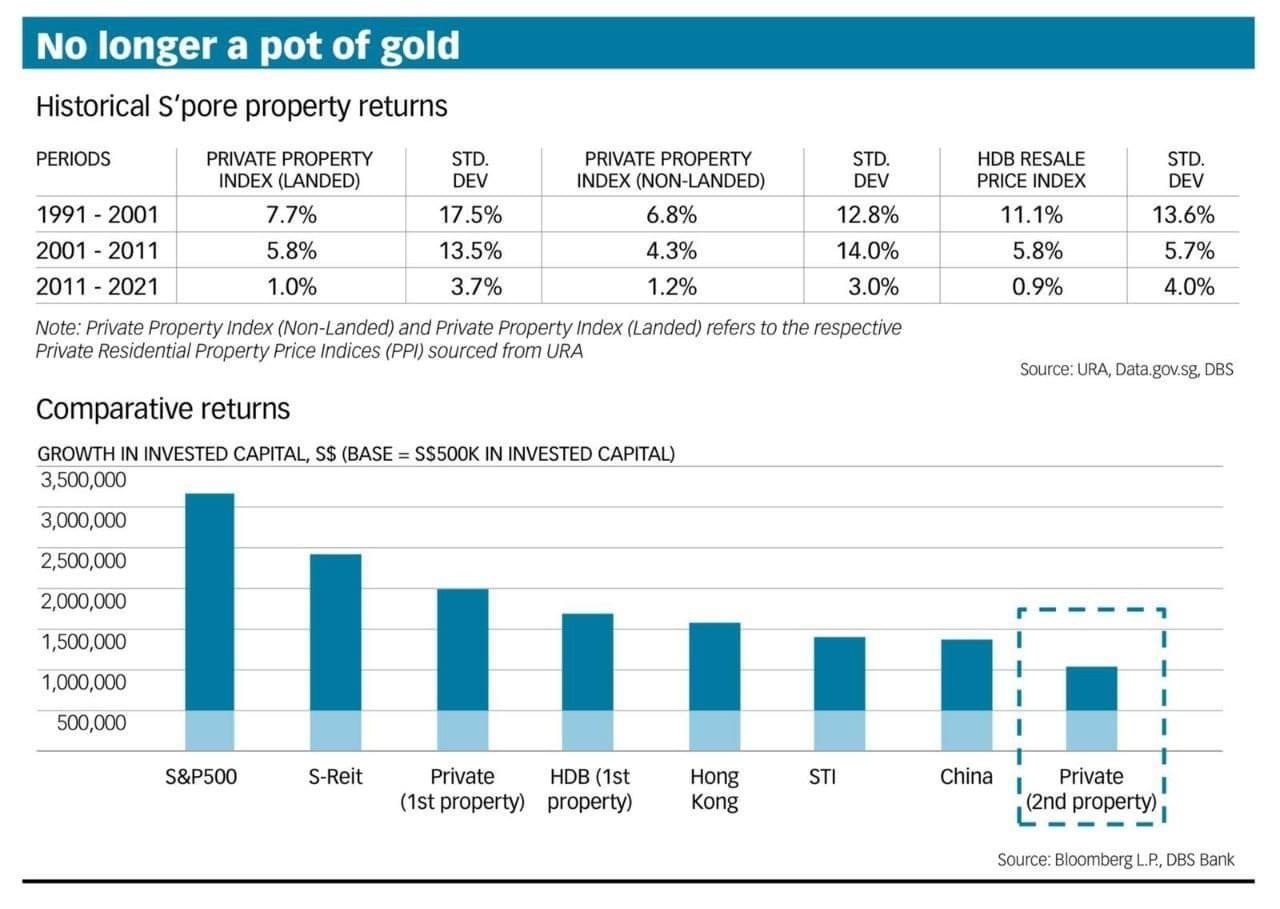

DBS Report: Will property still be your pot of gold?

And finally, the report from DBS, titled:

“Will Property Still Be Your Pot of Gold?

Why More Isn’t Always Better for Your Financial Planning”

I mean the title itself is pretty self explanatory.

The key points are:

- Property worked well for past generations of Singaporeans, but may not work so well going forward

- Ageing population and tighter manpower policies are secular headwinds for Singapore property

- Increase in property prices outpacing salary growth and may be unsustainable long term

- Don’t rely on property as your only source of investment – diversify into stocks and REITs

“房子是来住的、不是来炒的。”Houses for Living, not for Speculation

This quote was first uttered by Xi Jinping during the Party Congress back in 2017:

“坚持房子是用来住的、不是用来炒的定位。”

For the non-Chinese readers, it translates roughly into “Houses are for living, not for speculation”.

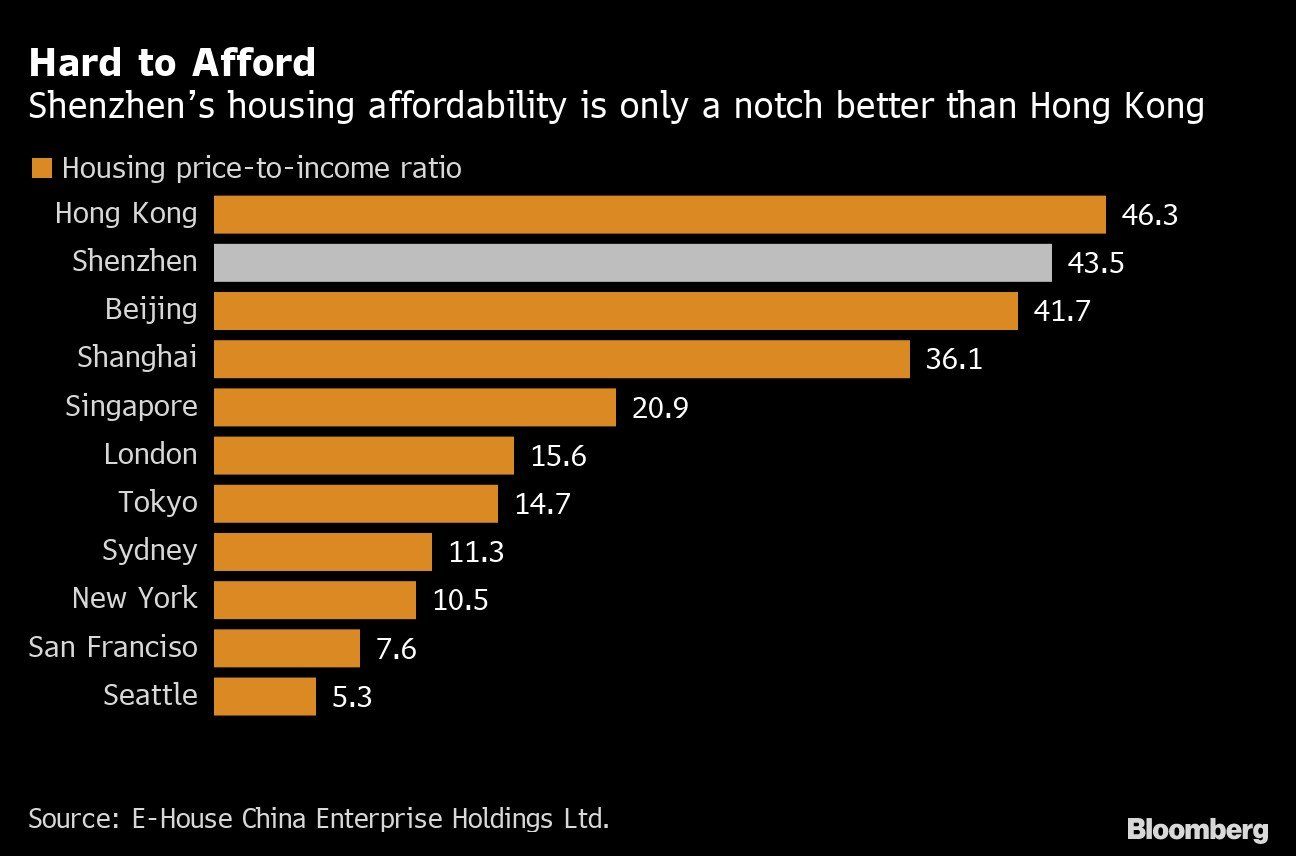

Now the Chinese understand what it means to have an expensive house.

Price to income ratio for a house in Beijing is 41.7 times.

This means that the average house price in Beijing costs 41.7 years average salary, which is just nuts.

Singapore at 20.9 looks tame by comparison.

Since the Xi Jinping speech in 2017, China has been trying to tackle house prices for a while now, with varying degrees of success.

The latest narrative from Singapore reminds me a lot of this philosophy.

Narrative shifts are important to track because they always lead policy changes. It is always the narrative that shifts first, then policy, then finally prices.

BTW – we share commentary on Singapore Investments every week, so do join our Telegram Channel (or Telegram Group), Facebook and Instagram to stay up to date!

[mc4wp_form id=”173″]

Flaws in the DBS Study + BT Article

That said, there are a couple of flaws in the DBS study and BT article worth pointing out.

I’m willing to gloss over a lot of the smaller points for the sake of discussion, but there are 2 big ones that stand out for me.

Historical Returns from the past 10 years

Both the DBS study and BT article use returns from the past 10 years, to extrapolate into the next 30 – 60 years.

That doesn’t make sense to me.

The past 10 years was very weak for Singapore real estate due to cooling measures.

Whereas the past 10 years was very strong for stocks and REITs because of quantitative easing (QE) from the Feds, and a decade of easy monetary policy.

So it’s not really fair to take 10 year historical returns and extrapolate that into the future.

Past performance really is not an indicator of future performance.

Second Property versus First Property

The other problem, is that the DBS report uses returns on a second property.

I don’t think this is the right way to do it, because the people who are deliberately paying a 12% ABSD rate to buy a second property are not like you or me.

They are not doing it for capital gains, they are doing it for capital preservation.

These are the high net worth individuals that are mainly using property as a long term inflation hedge to preserve the value of their wealth.

Anyone that seriously wants to use property as an investment would decouple from their spouse or use their children’s name to get around ABSD rules (and show funds to max out the 75% mortgage).

So DBS reaching their conclusion based on a second property doesn’t make sense to me.

As you can see below, once you look at the returns for a private first property, returns become very much higher.

That’s even after tracking returns over the past 10 years which was a weak period for Singapore property.

But they do raise good points

There are a few other flaws like stamp duty being too high, using an inflation rate that’s too low, not reinvesting dividends etc.

But we’ll just look at the big picture points here.

And the DBS report / BT Article does raise some great points.

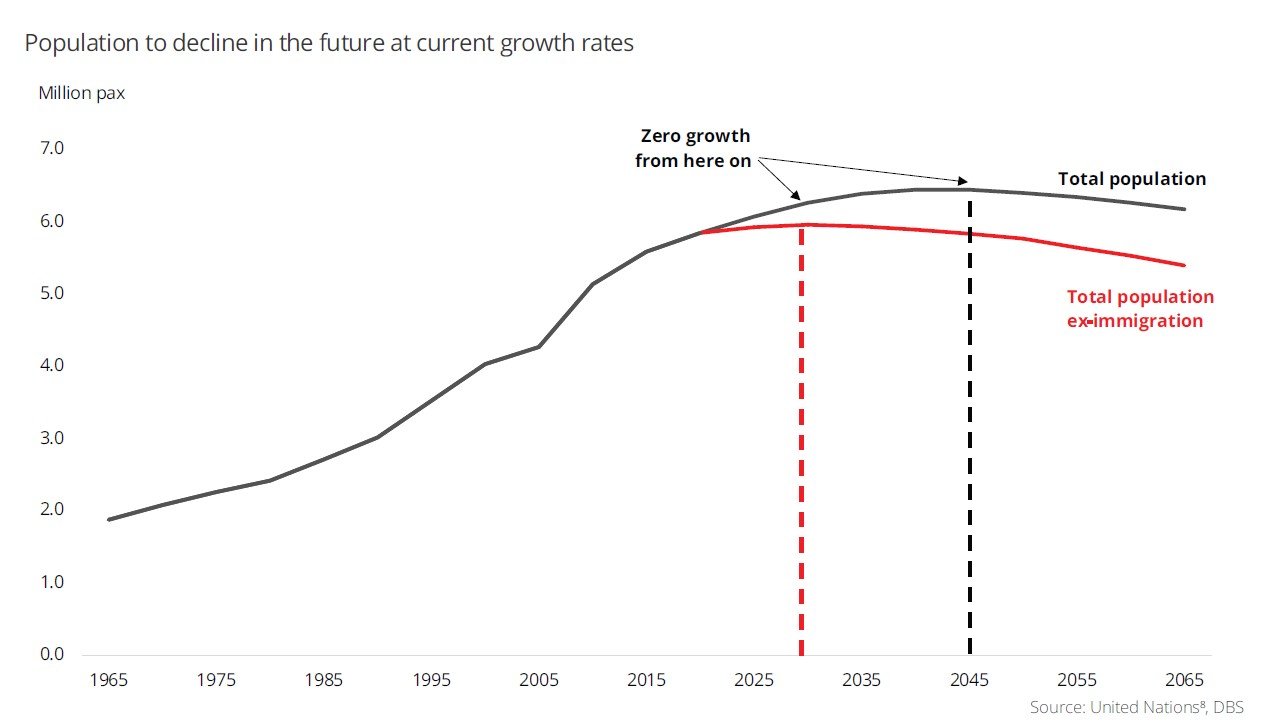

Secular headwinds from Demographics + Manpower

The first is that population growth for Singapore may plateau going forward – due to less babies and declining immigration.

Less people means less demand for housing, which translates into slower price growth.

The counter argument here is that the policy may change going forward.

Perhaps in 5 years the government may decide to welcome expats again, and population resumes its uptrend.

It’s very hard to predict 2 – 3 years out, let alone 40 years like DBS is doing.

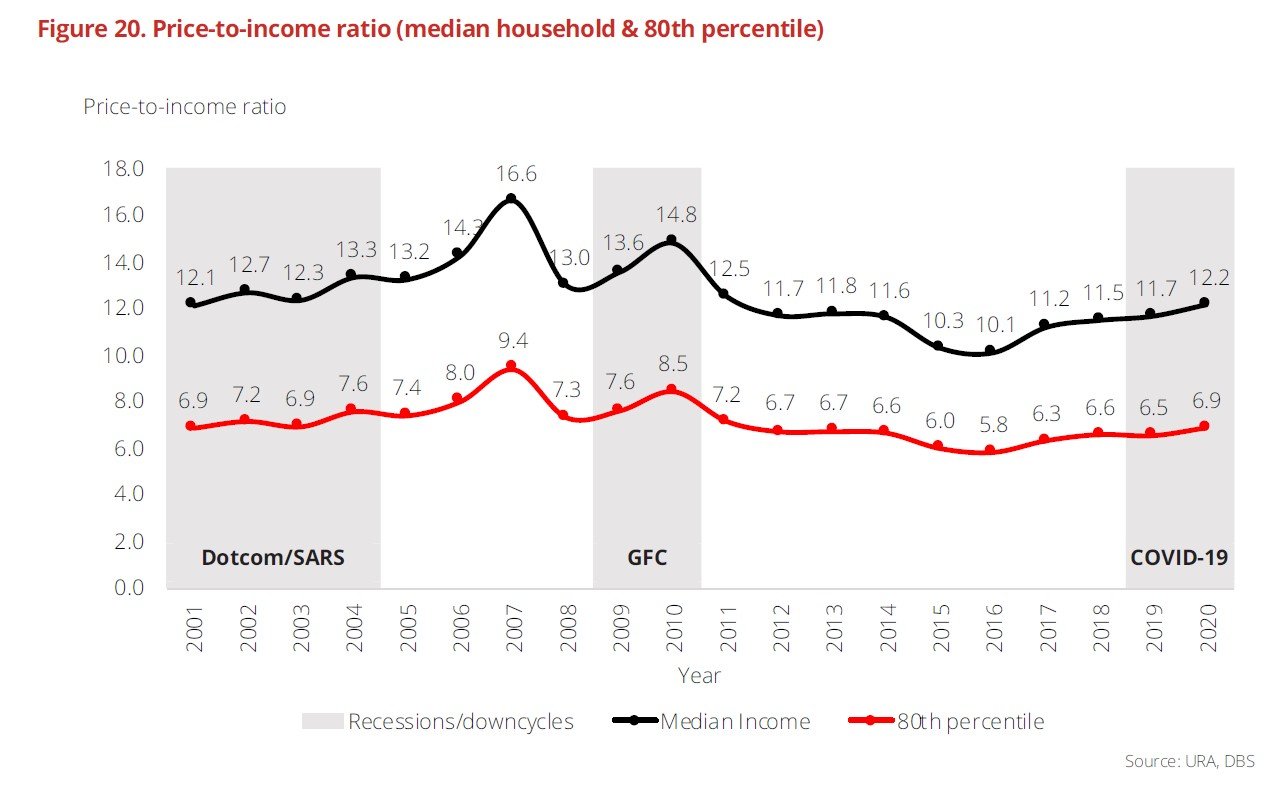

Affordability – starting from a very high base

DBS meant this chart as a way to show that property prices are the most expensive they’ve been since 2012.

Which means that price gains going forward are limited.

But when I look at it the conclusion that jumps out is that property prices are still not as expensive as they were in 2007 and 2010.

That said, this was pre-cooling measures though, so it’s possible that things have changed.

My Personal View?

Loyal readers of Financial Horse will know that I purchased a second property this year.

Okay technically my “First”, because I decoupled from my spouse so that I wouldn’t need to pay ABSD.

So you have a rough idea where I stand in this debate.

The point I wanted to make though, is that both sides are right.

I absolutely agree that Singapore property today won’t see the same returns earlier generations saw.

The past 50 years was Singapore rising from backwater town to first world financial center. No way that real estate prices will replicate that kind of returns going forward.

But I’m not sure if I agree that property is a poor investment, so much that you should rent and put all your money into stocks/REITs instead.

I think for those who can afford it, property still makes sense for a few reasons.

Inflation Hedge + Leverage

If I am right that we are moving into a more inflationary decade, then property might be one of the better ways to hedge purchasing power.

With a property you’re using 75% leverage to buy a hard asset.

If inflation goes up, the value of the house goes up, but the amount you owe the bank stays the same.

And with 75% leverage, you get to benefit if central banks stick with another decade of low interest rates and easy monetary policy.

Singapore as a Financial Centre

Singapore’s business model of late seems to be that of a global financial center, and wealth management / Technology hub.

That means attracting more high net worth individuals to come here. More tech professionals. More expats.

And don’t forget you need a whole supporting cast. Everyone from finance professionals to lawyers to construction workers to waiters.

So I’m not so sure if DBS’s prediction of flat population growth is right. I agree on the no babies part, but less so on the immigration part.

But I could be wrong on this one. Maybe population just flatlines at 7 million like DBS predicts.

The devil is in the details – What is your allocation to property?

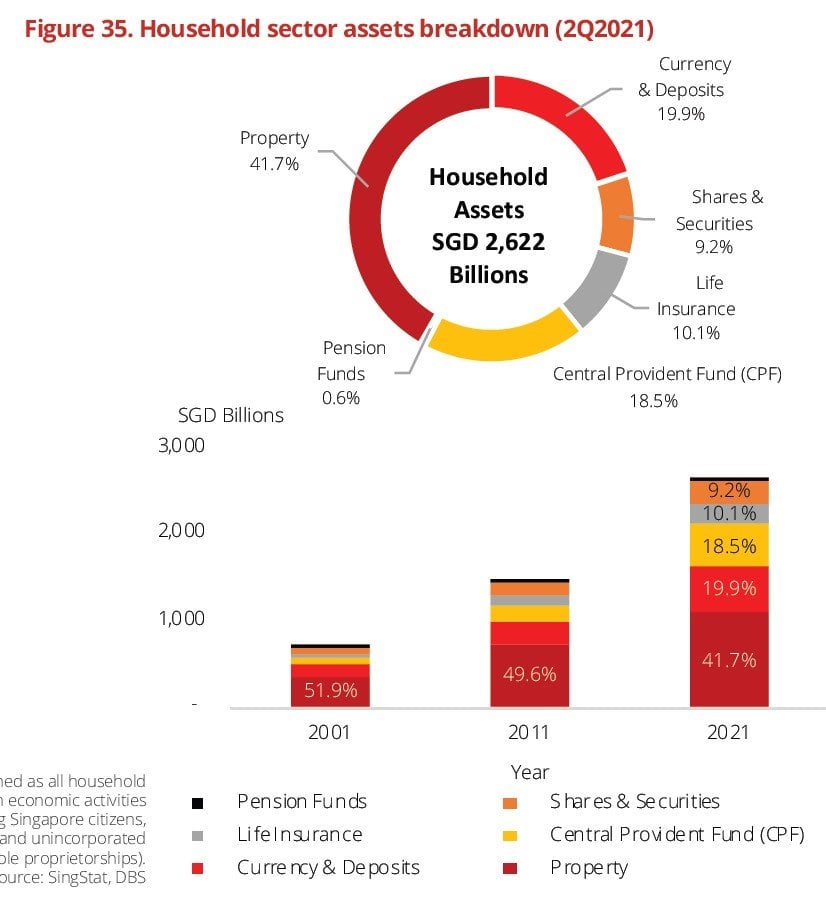

DBS has this fascinating chart which shows the breakdown of household assets in Singapore.

It show that average Singapore household has 41% of their assets in property.

18% in CPF, 20% in cash.

And only 9% in shares.

My point here – is that whether property is a good investment, depends on how much allocation you plan to have.

If you plan on having 80% of your wealth in property, then yeah I agree with DBS. This isn’t the 1980s anymore, you don’t want to own real estate only – exposure to stocks and REITs makes sense.

But if your exposure to real estate is only 5%, then perhaps there could be room to bring it up.

The right number will depend on the stage of life you are in.

The chart above puts the average at 41%, which I think is fair (but the 9% allocation to stocks is way too low).

For me personally it’s about 20% – 30%. But this one really depends on your individual circumstances. You can see my full portfolio breakdown on Patreon if you’re keen.

Pricing and What you buy matters

And finally – one massive caveat.

Each piece of property is unique.

Whether you’re buying a HDB or Condo or Landed, whether you’re buying in Punggol or Woodlands, each market has slightly different dynamics.

I’ve generally approached the issue from a very high level top down approach in this article, but there will be a lot of nuance on the ground.

Even if property as a whole has average returns, you can still outperform by picking well, or buying at a good price – just like with stocks.

In fact I’m planning to launch a full series on “How to Buy a Property in Singapore” – with guides on everything from how to pick a property, how to determine price, how to finance the purchase etc that will dive into such issues.

It’s going to be completely free of charge as my way of giving back to the community, and should launch in the coming weeks – so do stay tuned for the release.

Hopefully, that will help those of you looking to buy a property in this tough market.

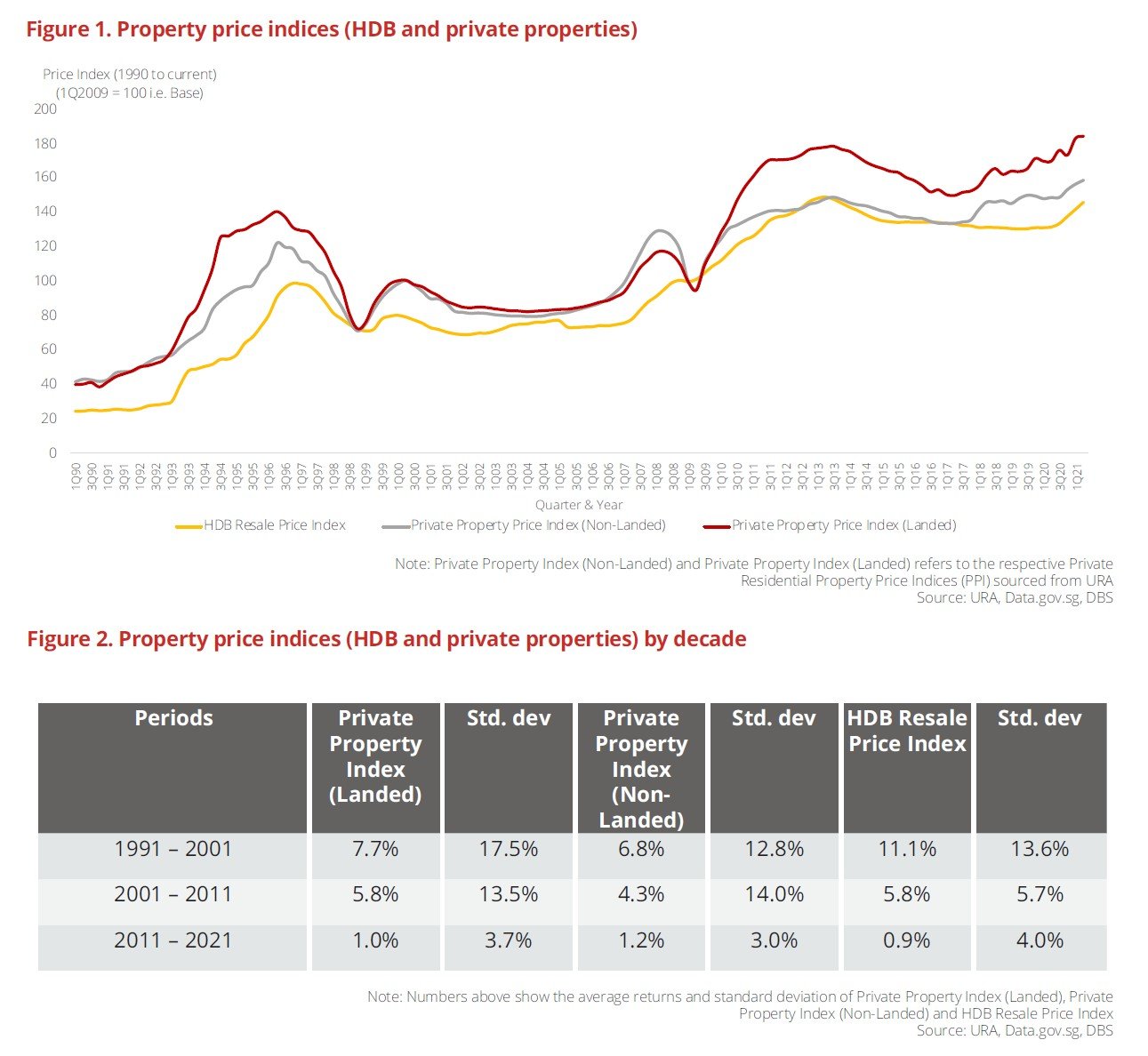

Closing Thoughts: Property is Cyclical

It’s been a monster of an article, and I do hope this helps in your decision making.

I wanted to leave you with this chart below.

Property is a cyclical business.

You can split it up into 3 different cycles – 1991 to 2001, 2001 to 2011, and 2011 to 2021.

The biggest price changes usually come from the shift from one cycle to another. A regime change if you like.

So the question then is – are we at the cusp of a new cycle? Or are we destined for another decade of low returns like DBS suggests?

Love to hear what you think!

FYI – We just launched the FH Property Series. Everything you need to know to buy a property in Singapore, completely free of charge.

Check out Part I on How to Pick a Property in Singapore.

Stupid analysis.. lol

Do you mean the BT one or the DBS one? Or mine? Curious to hear more.

Ignore the previous silly comment Financial Horse. I thought your article is pretty good. The DBS assets allocation is interesting. I wonder if the property is the 2nd property, or it includes the property that household LIVES IN?

Keep up the good work.

Thanks Ken! Appreciate the kind words.

Yeah good point. I suspect it is an aggregate across the board for all Singaporean households tracked. So it includes the first, second, and third properties (for those who have them). But it’s interesting because the final number of 40% makes a lot of sense. I can see how younger households would have a higher number, and older households lower, giving an average of 40%.

Yeah.. DBS should be more specific. Typically if we talk about asset allocation, it should not count the property you are living in (it’s a roof over the head and a shelter, not investment, in my opinion). Also, I wonder if this is net after mortgage. Property is usually the largest component so any assumptions can skew the pie chart.

As you said.. devil is in the details. 🙂

Yeah, that would be a huge improvement on the number (excluding primary residence). I do hope that it is net after mortgage though. Otherwise the number would make absolutely no sense! I’m sure DBS wouldn’t make a mistake like that… right?

Dear FH

Thanks for sharing your thoughts here.

Many young couples are feeling disgruntled on the ground with the housing options currently available to them:

– Genuine housing needs for their own place to settle down

– Unable to get BTO allocation (see the BTO oversubscription rate)

– HDB resale prices all time-high (22 Oct 2021)

– Private home properties rising for 6th consecutive quarters (22 Oct 2021)

Authorities have said earlier this year that they are “monitoring the property market developments very closely” but the market has yet to see any significant announcements yet.

In your opinion, will the authorities be pressured to act on the situation given the potential sociopolitical impacts and negative sentiments that such a situation may cause?

PS: Certainly looking forward to your new “How to Buy a Property in Singapore“ series!

Thanks for the support! If all goes well I should be able to launch the first article by this weekend.

Okay personal view here – I think govt will be forced to intervene in some form because the negative sentiment is getting very strong. If you’re a young couple and priced out of the market, that’s a really horrible feeling.

That said, the options are limited here, mainly because it is a structural demand supply imbalance. This isn’t rampant speculation driving prices up, it seems to be a case of real demand from homebuyers, coupled with insufficient supply because of COVID issues.

Long term the problem will be solved once you can bring new supply online, but short term it’s really hard to see what can be done to effectively solve the problem.

I enjoy reading your blog.

If you’re just starting from scratch, it maaaybe makes sense to rent instead and go into other investments. But if you have a lump of cash, better to buy a property with a low interest rate housing loan for the leverage and go into other investments yielding better, especially if its your first.

Rule of wealth is simply to own desirable assets. I believe that the right Singapore property is a good investment because Singapore is a desirable and safe place to live.

On one hand population is ageing but on the other hand the gov’t won’t let the economy stagnate and will bring in new people. I expect life expectancy to keep increasing as well so people will still be alive and need houses, especially when their lease expires.

I also agree that inflation is higher than what the CPI suggests so it make sense to own hard assets.

And yes it is all about your portfolio allocation, and each person’s situation is different.

Yes spot on. The personal situation is very, very important, and the key factor here.

For those with the cash and income to support it, and who recognise you’re not going to get 7% returns but low single digits, I still see a role for property in the portfolio. But like you said, for those with less cash set aside, I can see how renting and putting the rest of the money into higher yielding investments could make sense too.

Whole idea of investing isn’t about getting rich but gaining financial independence in life.

Investing in property is one of those tools. But not necessarily the sharpest tool in the toolbox. Need to see out of the box to find better opportunities.

Makes me laugh at those young YouTubers advocating property investments, property agents hawking high end properties on the net. These people who are obviously either green S’poreans or new citizen converts trying to stir the S’pore property market up by collective force of trying. If there’s any money to be made, the past would have been it, not now! Now is trying to flog a near dead horse into winning a race!

In any investments; ROI, the capital opportunity costs, time frame & liquidity preference are all important to a seasoned investor.

Frankly, the S’pore property market has somewhat gotten one-sided in the marketplace. It means the risk/return are getting assymetrical ie. high risk on the psf pricing, low rewards. And the time frame has extended further over the horizon!

There are better investment opportunities out there. Don’t just look inside a tunnel named S’pore!

Yes! Really agree with this.

The days of 10% returns on real estate are probably over. Low single digits from here on out (but juiced with leverage). It would still make sense for many people who have the cash and income, but trying to get rich off property today is probably not the best tool. You need to get your pot of gold elsewhere, then put it into real estate to preserve wealth / purchasing power.

The future of SG real estate will not be like “the high tide that raises all boats” type of across-the-board prosperity we’ve had experienced in the 1992-1996, 2006-2007 & 2011-2013.

It would take great ingenuity, a keen eye to spot the underappreciated locations that will provide mega returns.

The future eco-system favours those with ground level experience, ability to do research & investors who know what they’re doing.

With SG psf already so high, the game favours the seasoned investor, not the novice! The internet, YouTube creates a lot of property scamsters!

Always ask yourself this, if they’re so good, why they’re willing to teach others their money making secrets?

There are better wealth preservation assets than simply real estate!

Good point, appreciate the sharing! 🙂

Good job, FH!

As per your prediction, new HDB rules were indeed announced! 🙂

Now that MND has given its position on the upcoming Prime BTOs, do you think they will tackle the high property prices (both private and HDB resale) as well?

Been thinking the exact same thing myself! Will do a full article this weekend to share my views. ????